Brazil Palm Oil Market (2025-2029) | Outlook, Value, Companies, Forecast, Size, Industry, Growth, Revenue, Share, Trends & Analysis

Market Forecast By Nature (Organic, Conventional), By Product (CPO, RBD Palm Oil, Palm Kernel Oil, Fractionated Palm Oil), By End-use (Food & Beverage, Personal Care & Cosmetics, Biofuel & Energy, Pharmaceuticals, Others) And Competitive Landscape

| Product Code: ETC383762 | Publication Date: Aug 2022 | Updated Date: Sep 2025 | Product Type: Market Research Report | |

| Publisher: 6Wresearch | Author: Shubham Padhi | No. of Pages: 75 | No. of Figures: 35 | No. of Tables: 20 |

Brazil Palm Oil Market Size Growth Rate

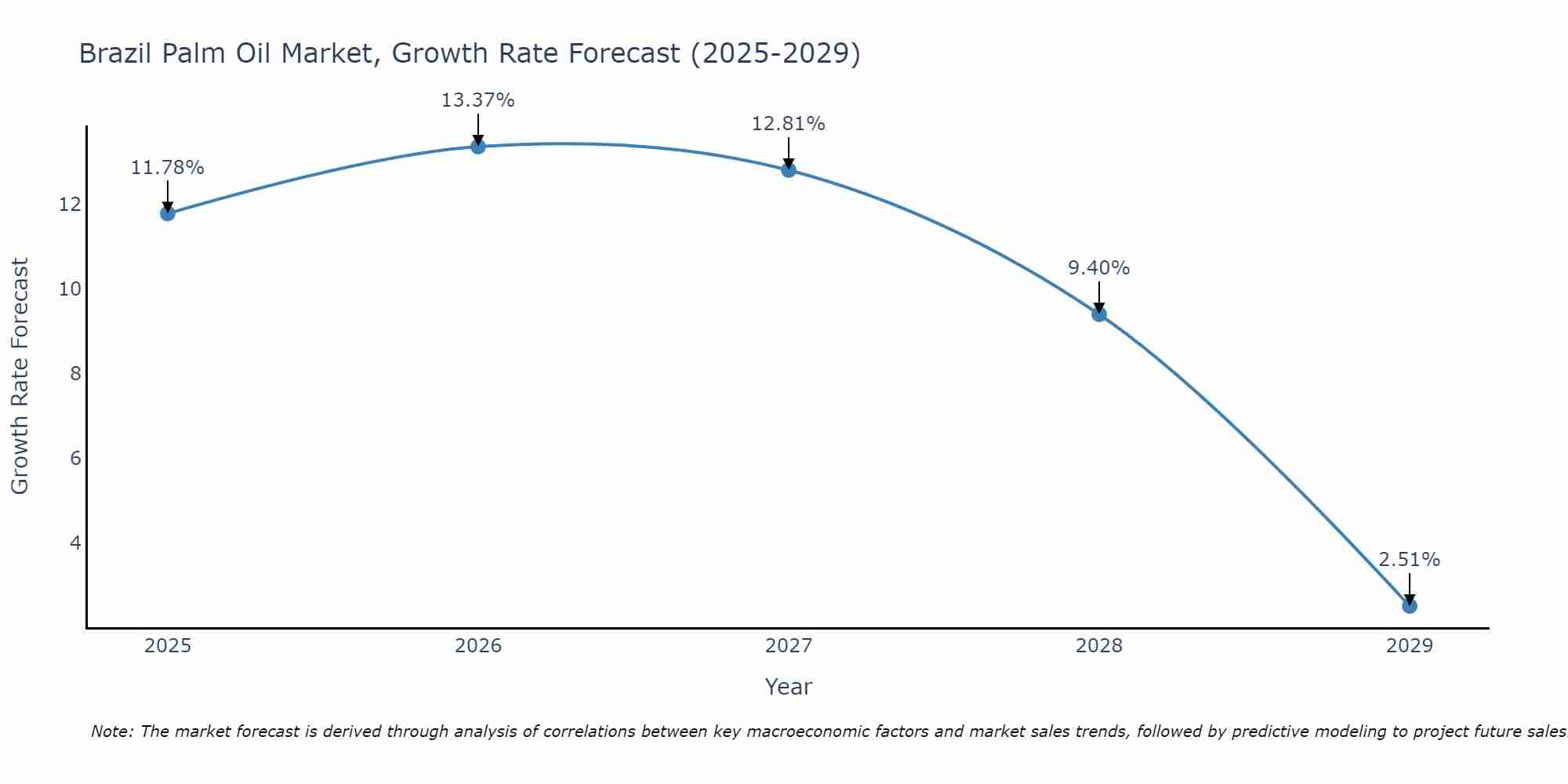

The Brazil Palm Oil Market is projected to witness mixed growth rate patterns during 2025 to 2029. Growth accelerates to 13.37% in 2026, following an initial rate of 11.78%, before easing to 2.51% at the end of the period.

Brazil Palm Oil Market Highlights

| Report Name | Brazil Palm Oil Market |

| Forecast Period | 2025-2029 |

| CAGR | 2.51% |

| Growing Sector | Personal care & Cosmetics |

Topics Covered in the Brazil Palm Oil Market Report

The Brazil Palm Oil Market report thoroughly covers the market by Nature, by Product and by End-users. The market report provides an unbiased and detailed analysis of the ongoing market trends, opportunities/high growth areas, and market drivers which would help the stakeholders to devise and align their market strategies according to the current and future market dynamics.

Brazil Palm Oil Market Synopsis

Brazil Palm Oil Market holds a significant position in the agro-industrial landscape of the Brazil who serves major sectors such as food & beverage, biofuels, personal care, and pharmaceuticals. Both domestic producers and global players are actively participating, the market continues to evolve with a growing focus on sustainable practices and certification standards.

Brazil Palm Oil Market is predicted to expand at a substantial CAGR of 2.51% during the forecast period 2025-2029. There are numerous growth factors which are contributing in the expansion of the market. Most of the demand comes from the industries, particularly food & beverage, biofuels, and personal care. Renewable energy is mainly focused by the manufactures of the palm oil, due to which gained momentum as a feedstock for biodiesel under the RenovaBio program, creating significant growth potential. The increasing consumer shift toward plant-based ingredients and natural oils in cosmetics and pharmaceuticals further supports market expansion.

Despite its potential, the Brazil Palm Oil Market has few notable challenges due to which growth of market affects. Particularly, environmental and sustainability concerns are need to be addressed. Palm oil cultivation is expanding that often raises fears of deforestation and biodiversity loss, which has brought stricter environmental regulations from IBAMA. Also, production costs, volatile global palm oil prices, and dependence on imports for certain derivatives also hinder profitability. Further competition is growing from alternative vegetable oils such as soybean and sunflower oil puts additional pressure on the industry, furthermore limiting the pace of expansion in Brazil.

Brazil Palm Oil Market Trends

Brazil Palm Oil Market is witnessing notable growth in the recent years with strong trends which include the rising demand in the food & beverage sector and increasing use in biofuels. Further, sustainability concerns are pushing producers toward eco-friendly and certified practices. Advancements are occurring in technology, especially in refining and processing which are improving efficiency and product quality. Further, growing consumer awareness about plant-based oils is fuelling broader adoption across industries.

Investment Opportunities in the Brazil Palm Oil Market

There are several opportunities in the Brazil palm oil market lie, especially in sustainable cultivation and value-added product manufacturing. Expansion is occurring into biofuel production presents strong potential as Brazil promotes renewable energy initiatives. There is also scope for investment in personal care and cosmetics, where palm derivatives are in high demand. Further, the partnerships with local producers can enhance supply chain integration and market reach.

Leading Players of the Brazil Palm Oil Market

Brazil Palm Oil Market is reshaped by the presence of key players including both domestic and international players who are majorly focusing on capacity expansion and sustainable practices. Some of those leading companies are Agropalma S.A., Palmaplan S/A, and global firms like Cargill Inc., Archer Daniels Midland (ADM), and Bunge Limited. These players are investing in certification programs to meet the RSPO (Roundtable on Sustainable Palm Oil) standards. Further, strategic alliances and acquisitions are further shaping the competitive landscape.

Government Regulations Introduced in the Brazil Palm Oil Market

According to Brazilian Government Data, regulations and policies implemented in the Brazil Palm Oil Market to ensure sustainability and fair trade. The Agro-Ecological Zoning of Oil Palm (ZAE Palm) policy restricts the plantations to degraded lands, which reduce the risk of deforestation. Compliance with the National Biofuels Policy (RenovaBio) also supports palm oil’s role in clean energy initiatives. Further, alignment with Environmental Licensing Regulations (IBAMA guidelines) ensures the strict adherence to ecological preservation. Further, Agro-Ecological Zoning of Oil Palm (ZAE Palm) encourage sustainable cultivation on degraded lands, attracting investments and promoting long-term growth.

Future Insights of the Brazil Palm Oil Market

The Brazil palm oil market is projected to expand gradually between 2025 and 2029. As the emphasis is growing on sustainable cultivation and certified production, the market is continued to rise. Renewable energy policies are set to support the demand for palm-based biofuels, further will gain momentum. Innovations in processing technologies and diversification into high-value derivatives will enhance the profitability. The future outlook remains optimistic, provided environmental challenges are addressed effectively.

Market Segmentation Analysis

The report offers a comprehensive study of the subsequent market segments and their leading categories.

Organic Palm Oil to Dominate the Market – By Nature

According to Sachin, Senior Research Analyst, 6Wresearch, organic palm oil is expected to gain traction in the market due to increasing consumer preference for natural and chemical-free products. Cosmetics segments where demand for premium, sustainable products is growing. Conventional palm oil continues to dominate overall consumption given its cost-effectiveness and wide-scale availability for industrial applications.

CPO to Dominate the Market – By Product

Among product types, Crude Palm Oil (CPO) is projected to dominate the Brazil palm oil market as it forms the raw material base for food, biofuel, and industrial uses. RBD Palm Oil (Refined, Bleached, and Deodorized) is also gaining significant demand due to its use in edible oil and processed foods.

Food & Beverage to Dominate the Market – By End-use

Food & beverage sector is set to capture the largest Brazil Palm Oil Market share, due to widespread use of palm oil in cooking oils, processed foods, and bakery products. Personal care & cosmetics is another fast-growing segment with palm oil derivatives being widely used in soaps, shampoos, and skincare items.

Key Attractiveness of the Report

- 10 Years of Market Numbers.

- Historical Data Starting from 2021 to 2024.

- Base Year: 2024

- Forecast Data until 2029.

- Key Performance Indicators Impacting the Market.

- Major Upcoming Developments and Projects.

Key Highlights of the Report:

- Brazil Palm Oil Market Outlook

- Market Size of Brazil Palm Oil Market, 2024

- Forecast of Brazil Palm Oil Market, 2029

- Historical Data and Forecast of Brazil Palm Oil Revenues & Volume for the Period 2019 - 2029F

- Brazil Palm Oil Market Trend Evolution

- Brazil Palm Oil Market Drivers and Challenges

- Brazil Palm Oil Price Trends

- Brazil Palm Oil Porter's Five Forces

- Brazil Palm Oil Industry Life Cycle

- Historical Data and Forecast of Brazil Palm Oil Market Revenues & Volume By Nature for the Period 2019 - 2029F

- Historical Data and Forecast of Brazil Palm Oil Market Revenues & Volume By Organic for the Period 2019 - 2029F

- Historical Data and Forecast of Brazil Palm Oil Market Revenues & Volume By Conventional for the Period 2019 - 2029F

- Historical Data and Forecast of Brazil Palm Oil Market Revenues & Volume By Product for the Period 2019 - 2029F

- Historical Data and Forecast of Brazil Palm Oil Market Revenues & Volume By CPO for the Period 2019 - 2029F

- Historical Data and Forecast of Brazil Palm Oil Market Revenues & Volume By RBD Palm Oil for the Period 2019 - 2029F

- Historical Data and Forecast of Brazil Palm Oil Market Revenues & Volume By Palm Kernel Oil for the Period 2019 - 2029F

- Historical Data and Forecast of Brazil Palm Oil Market Revenues & Volume By Fractionated Palm Oil for the Period 2019 - 2029F

- Historical Data and Forecast of Brazil Palm Oil Market Revenues & Volume By End-use for the Period 2019 - 2029F

- Historical Data and Forecast of Brazil Palm Oil Market Revenues & Volume By Food & Beverage for the Period 2019 - 2029F

- Historical Data and Forecast of Brazil Palm Oil Market Revenues & Volume By Personal Care & Cosmetics for the Period 2019 - 2029F

- Historical Data and Forecast of Brazil Palm Oil Market Revenues & Volume By Biofuel & Energy for the Period 2019 - 2029F

- Historical Data and Forecast of Brazil Palm Oil Market Revenues & Volume By Pharmaceuticals for the Period 2019 - 2029F

- Historical Data and Forecast of Brazil Palm Oil Market Revenues & Volume By Others for the Period 2019 - 2029F

- Brazil Palm Oil Import Export Trade Statistics

- Market Opportunity Assessment By Nature

- Market Opportunity Assessment By Product

- Market Opportunity Assessment By End-use

- Brazil Palm Oil Top Companies Market Share

- Brazil Palm Oil Competitive Benchmarking By Technical and Operational Parameters

- Brazil Palm Oil Company Profiles

- Brazil Palm Oil Key Strategic Recommendations

Market Covered

The report has been segmented and sub-segmented into the following categories:

By Nature

- Organic

- Conventional

By Product

- CPO (Crude Palm Oil)

- RBD Palm Oil (Refined, Bleached, and Deodorized)

- Palm Kernel Oil

- Fractionated Palm Oil

By End-use

- Food & Beverage

- Personal Care & Cosmetics

- Biofuel & Energy

- Pharmaceuticals

- Others

Brazil Palm Oil Market (2025-2029): FAQs

Brazil Palm Oil Market is predicted to grow at a CAGR of 2.51% during 2025-2029.

Key players include Agropalma S.A., Palmaplan S/A, Cargill Inc., Archer Daniels are key players.

Major challenges include environmental concerns, deforestation risks, regulatory compliance, high production costs.

Rising demand in food & beverages, biofuels under RenovaBio, personal care & cosmetics, and government support for sustainable cultivation.

6Wresearch actively monitors the Brazil Palm Oil Market and publishes its comprehensive annual report, highlighting emerging trends, growth drivers, revenue analysis, and forecast outlook. Our insights help businesses to make data-backed strategic decisions with ongoing market dynamics. Our analysts track relevent industries related to the Brazil Palm Oil Market, allowing our clients with actionable intelligence and reliable forecasts tailored to emerging regional needs.

Yes, we provide customisation as per your requirements. To learn more, feel free to contact us on sales@6wresearch.com

| 1. Executive Summary |

| 1.1 Key Findings & Takeaways |

| 1.2 Market Size Snapshot (Value & Volume) and 2025–2030 CAGR |

| 1.3 Growth Drivers, Challenges, and Opportunities |

| 1.4 High-Impact Trends (Sustainability, Traceability, Biofuels, Clean Label) |

| 1.5 Analyst’s Outlook & Strategic Recommendations |

| 2. Research Methodology |

| 2.1 Scope & Definitions (Palm Oil, CPO, RBD, PKO, Fractionated, Organic vs. Conventional) |

| 2.2 Forecasting Framework & Assumptions |

| 2.3 Data Sources (Primary & Secondary) |

| 2.4 Market Modeling Approach (Top-down/Bottom-up, Triangulation) |

| 2.5 Limitations & Notes |

| 3. Market Overview & Context |

| 3.1 Brazil at a Glance (Macro Indicators, Inflation, FX, Consumer Incomes) |

| 3.2 Palm Oil: Properties, Grades, Processing, and Uses |

| 3.3 Supply Chain Map (Plantations → Mills → Refineries → Distributors → End Users) |

| 3.4 Logistics & Infrastructure (Major Producing Regions, Key Ports, Road/Rail) |

| 3.5 Price Formation & Benchmarks (Domestic vs. International Parities) |

| 4. Regulatory & Policy Landscape |

| 4.1 National Regulations (agro/food safety, labeling, ANVISA/MAPA highlights) |

| 4.2 Biodiesel & Biofuel Policies (blend mandates, RenovaBio implications) |

| 4.3 Trade & Tariff Regime (Import duties, NTBs, sanitary/phyto requirements) |

| 4.4 Sustainability & ESG (traceability, deforestation-free procurement, certifications) |

| 4.5 Municipal/State-Level Considerations (notable regional incentives/restrictions) |

| 5. Market Dynamics |

| 5.1 Drivers (F&B demand, cost competitiveness vs. other oils, biofuel pull) |

| 5.2 Restraints (land-use constraints, ESG scrutiny, price volatility) |

| 5.3 Opportunities (value-added fractions, specialty fats, oleochemicals, cosmetics) |

| 5.4 Risk Analysis (climate/El Niño, pests/disease, policy shifts, FX risk) |

| 5.5 Porter’s Five Forces |

| 6. Brazil Palm Oil Market Size & Forecast (2019–2030) |

| 6.1 Historical Performance (2019–2024): Value, Volume, Average Prices |

| 6.2 Base-Year Structure (2024/2025): Split by Nature, Product, End-use |

| 6.3 Forecast (2025–2030): Value, Volume, and CAGR |

| 6.4 Scenario Analysis (Base / Optimistic / Conservative) |

| 6.5 Sensitivity to Key Variables (price, blend mandates, GDP growth) |

| 7. Segmentation by Nature |

| 7.1 Organic Palm Oil |

| 7.1.1 Market Size & Forecast (Value/Volume) |

| 7.1.2 Certification & Compliance Landscape |

| 7.1.3 Demand Drivers (premium F&B, natural personal care) |

| 7.1.4 Pricing & Margin Analysis |

| 7.1.5 Key Buyers & Case Examples |

| 7.2 Conventional Palm Oil |

| 7.2.1 Market Size & Forecast (Value/Volume) |

| 7.2.2 Industrial Demand Anchors (F&B processing, biodiesel) |

| 7.2.3 Cost Competitiveness vs. Soy/Sunflower/Canola |

| 7.2.4 Supply & Import Reliance Dynamics |

| 7.2.5 Procurement Best Practices |

| 8. Segmentation by Product |

| 8.1 Crude Palm Oil (CPO) |

| 8.1.1 Market Size & Forecast |

| 8.1.2 Refining Capacity & Utilization in Brazil |

| 8.1.3 Price Movements & Parity with Global Benchmarks |

| 8.1.4 Trade Flows (imports/exports) |

| 8.2 RBD Palm Oil (Refined, Bleached, Deodorized) |

| 8.2.1 Market Size & Forecast |

| 8.2.2 Applications (Frying oils, bakery fats, snacks) |

| 8.2.3 Distribution Channels & Private Label Penetration |

| 8.2.4 Quality/Specification Trends |

| 8.3 Palm Kernel Oil (PKO) |

| 8.3.1 Market Size & Forecast |

| 8.3.2 Oleochemicals & Personal Care Pull |

| 8.3.3 Price Spreads vs. CPO & Coconut Oil |

| 8.3.4 Import Dependence & Sourcing Strategies |

| 8.4 Fractionated Palm Oil (including Stearin/Olein & Specialty Fats) |

| 8.4.1 Market Size & Forecast |

| 8.4.2 Applications (confectionery coatings, bakery shortenings) |

| 8.4.3 Specialty Fats Innovations (trans-fat-free, structured lipids) |

| 8.4.4 Profit Pools & Contracting Models |

| 9. Segmentation by End-use |

| 9.1 Food & Beverage |

| 9.1.1 Market Size & Forecast |

| 9.1.2 Sub-segments: Bakery, Confectionery, Snacks, HoReCa, Packaged Foods |

| 9.1.3 Reformulation Trends (trans-fat compliance, clean label, RSPO) |

| 9.1.4 Buyer Landscape (processors, QSR/foodservice chains) |

| 9.2 Personal Care & Cosmetics |

| 9.2.1 Market Size & Forecast |

| 9.2.2 PKO-derived Surfactants & Emollients |

| 9.2.3 Natural/Organic Positioning & Claims |

| 9.2.4 Brand Sourcing & Traceability Expectations |

| 9.3 Biofuel & Energy |

| 9.3.1 Market Size & Forecast |

| 9.3.2 Mandates, Credits, and Feedstock Competition |

| 9.3.3 Economics vs. Soy Oil & Used Cooking Oil |

| 9.3.4 Capacity Pipeline & Technology Notes |

| 9.4 Pharmaceuticals |

| 9.4.1 Market Size & Forecast |

| 9.4.2 Excipient/Carrier Oil Applications |

| 9.4.3 GMP & Quality Requirements |

| 9.4.4 Import vs. Local Supply Considerations |

| 9.5 Others (Household, Industrial, Animal Feed, Oleochemicals) |

| 9.5.1 Market Size & Forecast |

| 9.5.2 Use-Cases & Growth Niches |

| 9.5.3 Pricing & Substitution Dynamics |

| 10. Regional & Route-to-Market Analysis |

| 10.1 Regional Demand & Supply Mapping (North, Northeast, Southeast, South, Center-West) |

| 10.2 Plantation Footprint & Expansion Potential (including Pará and neighboring states) |

| 10.3 Distribution & Wholesale Structures (national vs. regional players) |

| 10.4 Import Gateways & Port Analysis (e.g., Santos, Paranaguá, Itaqui) |

| 10.5 E-commerce & Modern Trade Penetration for B2B/B2C Oils |

| 11. Trade, Pricing & Cost Analysis |

| 11.1 Historical Import/Export Trends (Volumes, Values, Partners) |

| 11.2 Landed Cost Build-Up (FOB/CIF, freight, duties, taxes) |

| 11.3 Domestic vs. International Price Correlations |

| 11.4 Inventory Cycles & Seasonality |

| 11.5 Hedging & Risk Management (contracts, indices) |

| 12. Technology, Processing & Sustainability |

| 12.1 Milling & Refining Technology Landscape |

| 12.2 Fractionation & Specialty Fat Formulation |

| 12.3 Waste Valorization (biomass/biogas, glycerin) |

| 12.4 ESG, Traceability & Certification Pathways (RSPO and others) |

| 12.5 Deforestation-Free Supply Chains & Corporate Commitments |

| 13. Consumer & Industry Trends |

| 13.1 Health & Nutrition Perceptions; Labeling Impacts |

| 13.2 Premiumization vs. Value Segments |

| 13.3 Innovation Pipeline (fortification, specialty shortenings, plant-based) |

| 13.4 Marketing & Retail Shelf Dynamics |

| 14. Competitive Landscape |

| 14.1 Market Structure & Concentration (Producers, Refiners, Traders, Importers) |

| 14.2 Market Share Analysis (Value/Volume; by Product where available) |

| 14.3 Strategic Moves (M&A, JVs, capacity additions, partnerships) |

| 14.4 Competitive Benchmarking (production/refining capacity, footprint, certifications, customers) |

| 14.5 Company Profiles (Indicative List) |

| Domestic Producers/Refiners |

| Global Traders/Refiners with Brazil Presence |

| Biofuel Integrators & Large F&B Buyers |

| (Each profile to include: overview, product mix, capacity, sourcing, certifications, financial highlights where available, key customers, recent developments, SWOT) |

| 15. Procurement & Strategy Playbook |

| 15.1 Sourcing Strategies (domestic vs. imports, long-term vs. spot) |

| 15.2 Supplier Qualification & Audit Checklists |

| 15.3 Cost-Saving Opportunities (spec optimization, blends, logistics) |

| 15.4 Sustainability & Compliance Roadmap (KPIs, reporting, audits) |

| 16. Forecast Deep Dives & Scenarios |

| 16.1 Nature Split Outlook (Organic vs. Conventional) with Scenario Bands |

| 16.2 Product Split Outlook (CPO, RBD, PKO, Fractionated) with Sensitivities |

| 16.3 End-use Outlook (F&B, Personal Care & Cosmetics, Biofuel & Energy, Pharmaceuticals, Others) |

| 16.4 Macroeconomic & Policy Shock Scenarios (FX, mandates, import policy) |

| 16.5 Long-Term Outlook Beyond 2030 (qualitative) |

| 17. Appendices |

| 17.1 Glossary of Terms & Abbreviations |

| 17.2 Conversion Factors & Technical Specs |

| 17.3 List of Data Tables, Figures & Charts |

| 17.4 Interview Guides & Survey Instruments (if applicable) |

| 17.5 Company/Organization Directory |

| 17.6 Notes on Compliance, Ethics & Data Privacy |

Global Go To Market Strategy - 2030

Export potential enables firms to identify high-growth global markets with greater confidence by combining advanced trade intelligence with a structured quantitative methodology. The framework analyzes emerging demand trends and country-level import patterns while integrating macroeconomic and trade datasets such as GDP and population forecasts, bilateral import–export flows, tariff structures, elasticity differentials between developed and developing economies, geographic distance, and import demand projections. Using weighted trade values from 2020–2024 as the base period to project country-to-country export potential for 2030, these inputs are operationalized through calculated drivers such as gravity model parameters, tariff impact factors, and projected GDP per-capita growth. Through an analysis of hidden potentials, demand hotspots, and market conditions that are most favorable to success, this method enables firms to focus on target countries, maximize returns, and global expansion with data, backed by accuracy.

By factoring in the projected importer demand gap that is currently unmet and could be potential opportunity, it identifies the potential for the Exporter (Country) among 190 countries, against the general trade analysis, which identifies the biggest importer or exporter.

To discover high-growth global markets and optimize your business strategy:

Click Here

Pricing

- Single User License$ 1,995

- Department License$ 2,400

- Site License$ 3,120

- Global License$ 3,795

Leadership Perspectives from Industry Events

Search

Thought Leadership and Analyst Meet

Our Clients

6WResearch In News

- India Export Attractiveness Tracker 2026

- India Air Conditioner Market Set for Strong Rebound in 2026 After Weather-Led Correction and GST-Driven Recovery: 6Wresearch

- ADAS in India: How Automatic Emergency Braking, Blind Spot Detection & Driver Monitoring are Transforming Road Safety

- Doha a strategic location for EV manufacturing hub: IPA Qatar

- Demand for luxury TVs surging in the GCC, says Samsung

- Empowering Growth: The Thriving Journey of Bangladesh’s Cable Industry

Latest Reports

- Greece Insulated Sandwich Panels Market (2026-2032)

- Qatar Access and Home Network Market (2026-2032)

- Nicaragua RPG Gaming Market (2026-2032)

- New Zealand RPG Gaming Market (2026-2032)

- Netherlands RPG Gaming Market (2026-2032)

- Nauru RPG Gaming Market (2026-2032)

- Namibia RPG Gaming Market (2026-2032)

- Mozambique RPG Gaming Market (2026-2032)

- Montenegro RPG Gaming Market (2026-2032)

- Mongolia RPG Gaming Market (2026-2032)

Industry Events and Analyst Meet

EV India Expo 2026

HIMTEX 2026

India Refining Summit 2026

India EV Show 2026

EV tech India Expo 2026

Whitepaper

- Middle East & Africa Commercial Security Market Click here to view more.

- Middle East & Africa Fire Safety Systems & Equipment Market Click here to view more.

- GCC Drone Market Click here to view more.

- Middle East Lighting Fixture Market Click here to view more.

- GCC Physical & Perimeter Security Market Click here to view more.