Singapore Insulation Products Market (2026-2032) | Outlook, Value, Size, Trends, Forecast, Companies, Growth, Share, Revenue, Analysis & Industry

Market Forecast By Insulation Type (Thermal, Acoustic & others), By Material Type (Mineral Wool, Fiberglass, Stone wool, Polyurethane Foam (PUF), Flexible Elastomeric Foam (FEF), Other Insulations), By End Use (Building & Construction, Industrial, Transportation, Consumer) And Competitive Landscape

| Product Code: ETC265587 | Publication Date: Aug 2022 | Updated Date: Mar 2026 | Product Type: Market Research Report | |

| Publisher: 6Wresearch | Author: Ravi Bhandari | No. of Pages: 75 | No. of Figures: 11 | No. of Tables: 10 |

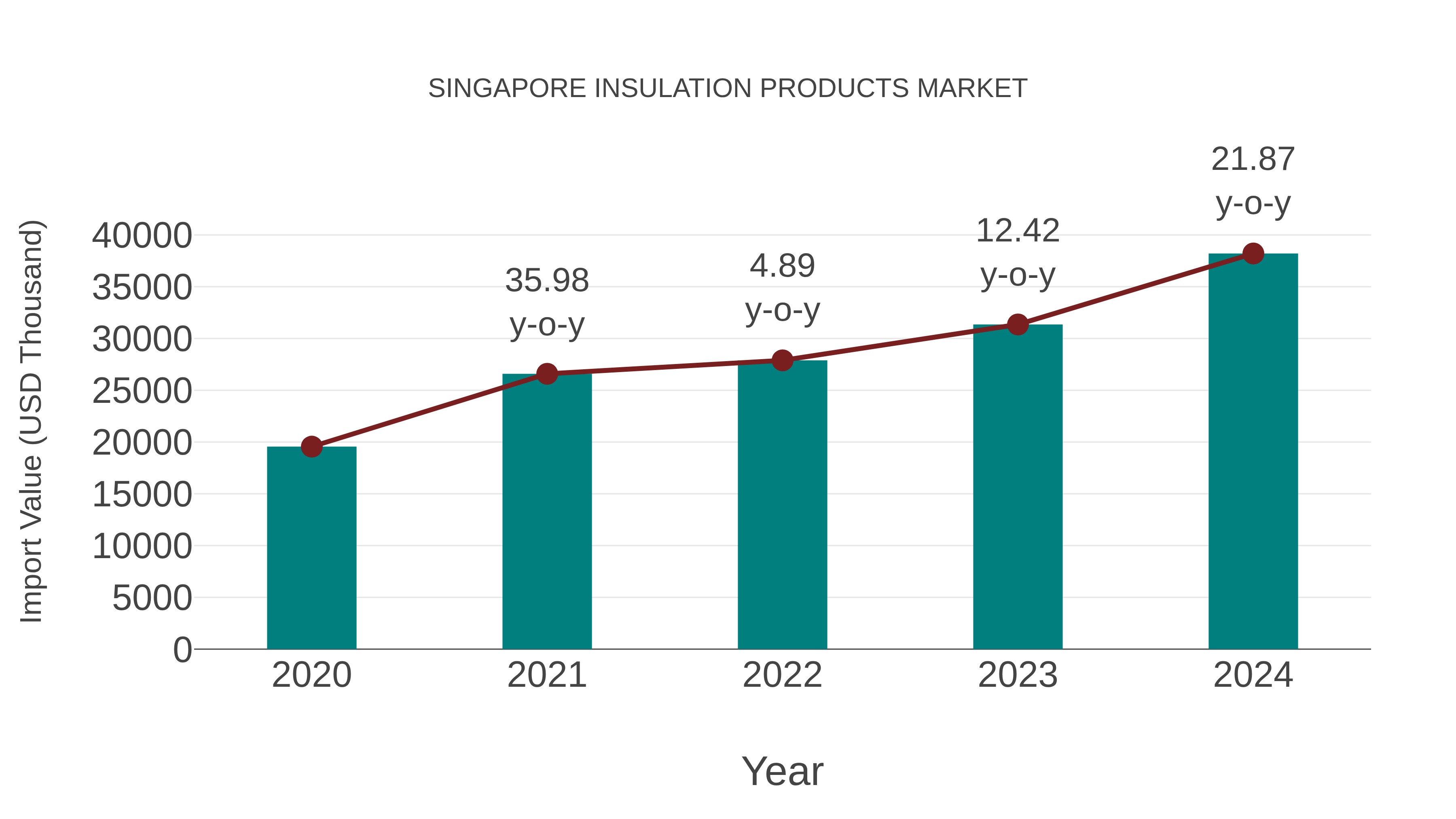

Singapore Insulation Products Market: Import Trend Analysis

In the Singapore insulation products market, the import trend showed a notable growth rate of 21.87% from 2023 to 2024, with a compound annual growth rate (CAGR) of 18.23% for the period 2020-2024. This surge in imports can be attributed to the increasing demand for energy-efficient solutions and the market`s stability in response to evolving building regulations.

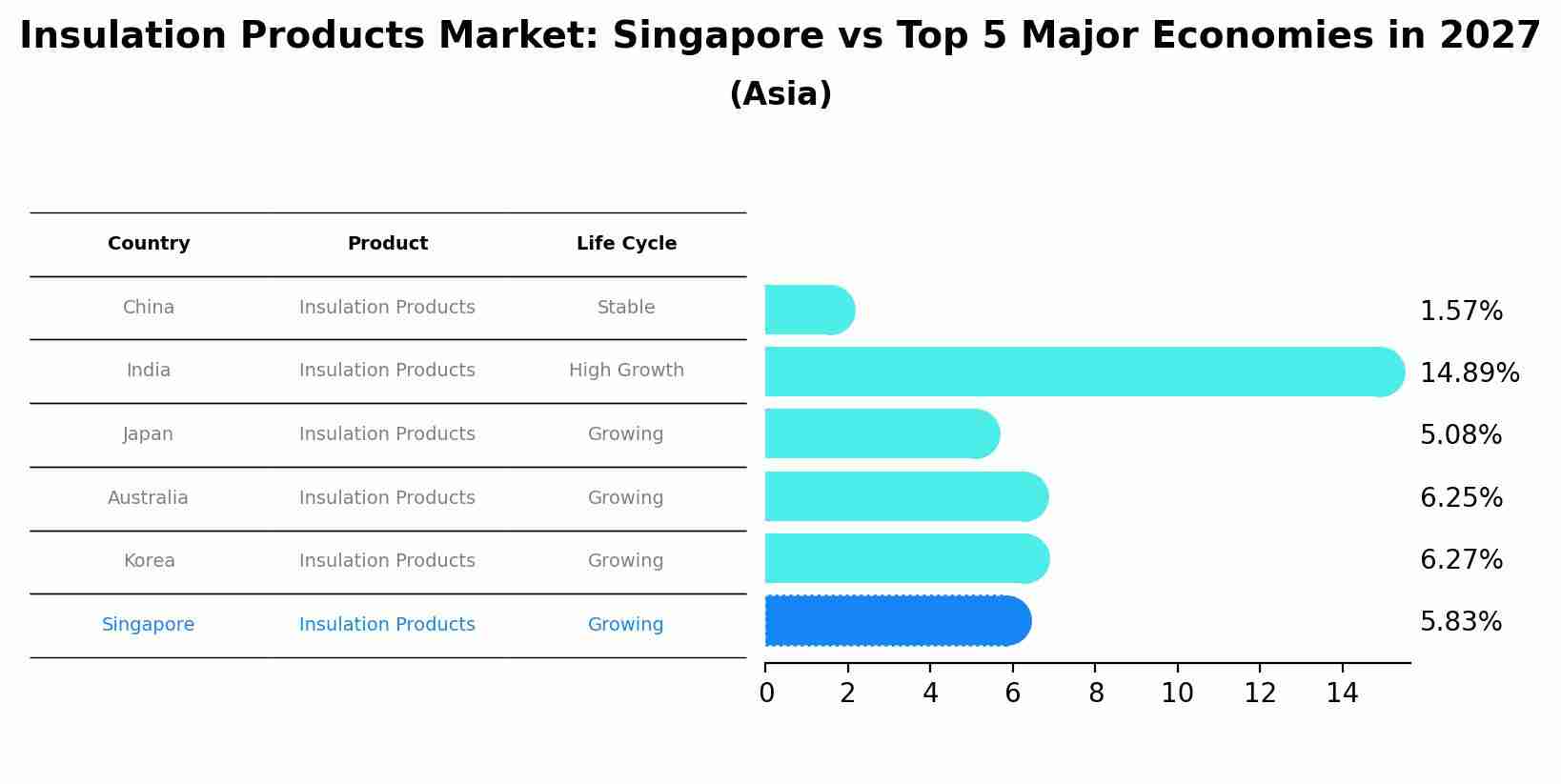

Insulation Products Market: Singapore vs Top 5 Major Economies in 2027 (Asia)

By 2027, Singapore's Insulation Products market is forecasted to achieve a growing growth rate of 5.83%, with China leading the Asia region, followed by India, Japan, Australia and South Korea.

Topics Covered in Singapore Insulation Products Market Report

Singapore Insulation Products Market Report thoroughly covers the market by insulation type, material type and end-use. Singapore Insulation Products Market Outlook report provides an unbiased and detailed analysis of the ongoing Singapore Insulation Products Market trends, opportunities/high growth areas, and market drivers. This would help stakeholders devise and align their market strategies according to the current and future market dynamics.

Singapore Insulation Products Market Synopsis

The Singapore insulation products market has been experiencing growth, driven by the country's infrastructure development, increasing demand for energy-efficient buildings, and strict government regulations promoting sustainability. As one of the most developed economies in Asia, Singapore continues to prioritize “Green Building Initiatives”, particularly with the “Singapore Green Building Masterplan 2030 launched in Mar 2021”, which aims to make most of the buildings in Singapore green by 2030. This has been propelling the demand for insulation products, which play a vital role in improving energy efficiency and reducing environmental footprints. Additionally, in 2023, the construction sector in Singapore grew tremendously, reflecting a steady growth trajectory driven by both public and private investments in real estate and commercial infrastructure. Also, residential and commercial building projects, particularly those certified under the Building and Construction Authority (BCA) Green Mark Scheme, have seen a marked increase in the integration of advanced insulation technologies. These buildings often require materials that not only provide thermal comfort but also meet stringent noise and fire safety standards.

According to 6Wresearch, the Singapore Insulation Products Market is projected to grow at a CAGR of 6.7% from 2025 to 2031, driven by the increasing adoption of green building standards, as well as the ongoing urbanization and expansion of industrial infrastructure. As of 2024, Singapore’s real estate market remains resilient, with certain residential units expected to be sold by 2025, alongside several commercial and mixed-use developments. This surge in construction projects, coupled with a growing awareness of the long-term cost savings associated with insulation, would continue to drive the market forward.

Also, the government’s efforts, such as the Jurong Lake District (JLD) master plan and developments as Springleaf, further boost the market. The JLD aims to transform the area into Singapore's largest business district outside the CBD, while Springleaf would offer an ecologically-sensitive residential estate with green spaces, reflecting the country’s emphasis on sustainable, nature-integrated urban planning. Additionally, Singapore’s industrial and manufacturing sectors, particularly the semiconductor and electronics industries, are undergoing significant expansions. This growth is accompanied by an increased demand for insulated solutions to meet the stringent requirements for temperature control, noise reduction, and fire safety in production environments. The government’s Industry Transformation Map (ITM) for manufacturing and the Smart Industry Readiness Index (SIRI) continue to focus on sustainability and resource efficiency, further promoting the use of advanced insulation materials in industrial applications.

Market Segmentation By Insulation Type

Thermal is expected to garner maximum revenue size in 2031 and would also witness fastest growth during 2025-2031 due to Singapore’s push for net-zero carbon emissions, growing demand for sustainable building materials, and massive cold storage investments for pharmaceuticals and food logistics. Government incentives for low-carbon construction and green retrofitting of existing buildings would further drive adoption. The fastest-growing areas within thermal insulation would be next-gen aerogel and vacuum insulation panels, EV battery thermal management, and high-performance insulation for semiconductor fabs. Stricter green financing criteria and new carbon taxation policies would accelerate the transition to advanced insulation solutions.

Market Segmentation By Material Type

Mineral wool would continue to dominate Singapore’s insulation products market by revenue size in 2031 as fire safety codes are expected to become even more stringent, particularly in public infrastructure and data centers as well as the material’s non-combustibility and recyclability aligns with Singapore’s sustainability goals, Moreover, its rising use in energy-efficient facades and acoustic insulation for urban environments would boost the demand even more.

However, PUF and PIR foams would witness fastest growth during 2025 to 2031 due to rising adoption in cold chain logistics and lightweight construction panels. Their superior thermal efficiency, moisture resistance, and space-saving properties would make them ideal for refrigeration units, pharmaceutical storage, and modular buildings, driving their rapid market expansion.

Thus, it is advised to focus on both these segments to gain maximum competitive advantage in the coming years.

Market Segmentation By End-Use

Building & construction segment is expected to garner maximum revenue size in 2031 driven by next-generation sustainable and high-performance facade technologies, higher thermal efficiency standards in retrofitted structures, and expanding underground developments for instance mass rapid transit (MRT) stations and subterranean malls, requiring advanced insulation. The push for mass engineered timber (MET) and sustainable prefabricated materials in construction would further increase insulation demand, particularly for modular and low-carbon buildings.

However, HVAC & refrigeration would witness fastest growth during 2025 to 2031 due to advancements in phase-change materials (PCMs) for thermal storage, high-efficiency duct insulation in smart buildings, and Singapore’s push for integrated cooling in urban planning for instance smart estates such as Tengah. Moreover, rise of decentralized cooling units in mixed-use developments would accelerate its adoption. Thus, players must focus on both these segments to gain competitive edge in the coming years.

Key Attractiveness of the Report

- 10 Years Market Numbers.

- Historical Data Starting from 2021 to 2024

- Base Year: 2024

- Forecast Data until 2031

- Key Performance Indicators Impacting the Market.

- Major Upcoming Developments and Projects.

Key Highlights of the Report:

- Singapore Insulation Products Market Overview

- Singapore Insulation Products Market Outlook

- Singapore Insulation Products Market Forecast

- Historical Data and Forecast of Singapore Insulation Products Market Revenues for the Period 2022-2032F

- Historical Data and Forecast of Market Revenues, By Insulation Type, for the Period 2022-2032F

- Historical Data and Forecast of Market Revenues, By Material Type, for the Period 2022-2032F

- Historical Data and Forecast of Market Revenues, By End-Use, for the Period 2022-2032F

- Singapore Insulation Products Market Drivers and Restraints

- Industry Life Cycle

- Porter’s Five Force Analysis

- Singapore Insulation Products Market Trends & Evolution

- Market Opportunity Assessment

- Singapore Insulation Products Market Revenue Ranking, By Companies

- Competitive Benchmarking

- Company Profiles

- Key Strategic Recommendations

Market Scope and Segmentation

Thereportprovides a detailed analysis of the following market segments:

By Insulation Type

- Thermal

- Acoustic

- Others (includes fireproofing, moisture resistance, electrical insulation, and chemical resistance)

By Material Type

- Mineral Wool

- Fiberglass

- PUF (Polyurethane) and PIR (Polyisocyanurate) Foams

- EPS (Expanded Polystyrene) and XPS (Extruded Polystyrene)

- FEF (Elastomeric Foam)

- Others (includes Calcium Silicate, Aerogel Insulation, etc.)

By End-Use

- Building & Construction

- HVAC & Refrigeration

- Industrial, Manufacturing & Energy

- Transportation

- Consumer Goods

Singapore Insulation Products Market (2026-2032): FAQs

Singapore Insulation Products Market is projected to grow at a CAGR of 6.7% from 2025 to 2031

Rising construction activities in Singapore, including large-scale developments and sustainable building initiatives, would drive increased demand for insulation products.

Singapore's insulation products market would face hinderance from high material costs, environmental concerns, and limited awareness.

Singapore Insulation Products Market Report thoroughly covers the market by insulation type, material type and end-use.

6Wresearch actively monitors the Singapore Insulation Products Market and publishes its comprehensive annual report, highlighting emerging trends, growth drivers, revenue analysis, and forecast outlook. Our insights help businesses to make data-backed strategic decisions with ongoing market dynamics. Our analysts track relevent industries related to the Singapore Insulation Products Market, allowing our clients with actionable intelligence and reliable forecasts tailored to emerging regional needs.

Yes, we provide customisation as per your requirements. To learn more, feel free to contact us on sales@6wresearch.com

| 2.3. Market Scope & Segmentation |

| 2.4. Research Methodology |

| 2.5. Assumptions |

| 3. Singapore Insulation Products Market Overview |

| 3.1. Singapore Insulation Products Market Revenues, 2022-2032F |

| 3.2. Singapore Insulation Products Market – Industry Life Cycle |

| 3.3. Singapore Insulation Products Market – Porter’s Five Forces |

| 4. Singapore Insulation Products Market Dynamics |

| 4.1. Impact Analysis |

| 4.2. Market Drivers |

| 4.2.1 Increasing demand for energy-efficient buildings in Singapore |

| 4.2.2 Stringent regulations promoting the use of insulation products for environmental sustainability |

| 4.2.3 Growth in construction activities and infrastructure development projects in Singapore |

| 4.3. Market Restraints |

| 4.3.1 High initial costs associated with insulation products |

| 4.3.2 Limited awareness and education about the benefits of insulation products among consumers and businesses |

| 5. Singapore Insulation Products Market Trends |

| 6. Singapore Insulation Products Market Overview, By Insulation Type |

| 6.1. Singapore Insulation Products Market Revenue Share, By Insulation Type, 2032 & 2031F |

| 6.1.1 Singapore Insulation Products Market Revenues, By Thermal, 2021- 2031F |

| 6.1.2 Singapore Insulation Products Market Revenues, By Acoustic, 2021- 2031F |

| 6.1.3 Singapore Insulation Products Market Revenues, By Others, 2021- 2031F |

| 7. Singapore Insulation Products Market Overview, By Material Type |

| 7.1 Singapore Insulation Products Market Revenue Share, By Material Type, 2032 & 2031F |

| 7.1.1 Singapore Insulation Products Market Revenues, By Mineral Wool, 2021- 2031F |

| 7.1.2 Singapore Insulation Products Market Revenues, By Fiberglass, 2021- 2031F |

| 7.1.3 Singapore Insulation Products Market Revenues, By PUF (Polyurethane) and PIR (Polyisocyanurate) Foams, 2021- 2031F |

| 7.1.4 Singapore Insulation Products Market Revenues, By EPS (Expanded Polystyrene) and XPS (Extruded Polystyrene), 2021- 2031F |

| 7.1.5 Singapore Insulation Products Market Revenues, By FEF (Elastomeric Foam), 2021- 2031F |

| 7.1.6 Singapore Insulation Products Market Revenues, By Others, 2021- 2031F |

| 8. Singapore Insulation Products Market Overview, By End-Use |

| 8.1 Singapore Insulation Products Market Revenue Share, By End-Use, 2032 & 2031F |

| 8.1.1 Singapore Insulation Products Market Revenues, By Building & Construction, 2021- 2031F |

| 8.1.2 Singapore Insulation Products Market Revenues, By HVAC & Refrigeration, 2021- 2031F |

| 8.1.3 Singapore Insulation Products Market Revenues, By Industrial, Manufacturing & Energy, 2021- 2031F |

| 8.1.4 Singapore Insulation Products Market Revenues, By Transportation, 2021- 2031F |

| 8.1.5 Singapore Insulation Products Market Revenues, By Consumer Goods, 2021- 2031F |

| 9. Singapore Insulation Products Market Key Performance Indicators |

| 9.1 Energy savings achieved by using insulation products |

| 9.2 Number of new construction projects incorporating insulation products |

| 9.3 Percentage increase in adoption of insulation products in the market |

| 10. Singapore Insulation Products Market Opportunity Assessment |

| 10.1. Singapore Insulation Products Market Opportunity Assessment, By Insulation Type, 2031F |

| 10.2. Singapore Insulation Products Market Opportunity Assessment, By Material Type, 2031F |

| 10.3. Singapore Insulation Products Market Opportunity Assessment, By End-Use, 2031F |

| 11. Singapore Insulation Products Market Competitive Landscape |

| 11.1 Singapore Insulation Products Market Revenue Ranking, By Top 3 Companies, CY2032 |

| 11.2 Singapore Insulation Products Market Key Companies Competitive Benchmarking, By Operating Parameters |

| 11.3 Singapore Insulation Products Market Key Companies Competitive Benchmarking, By Technical Parameters |

| 12. Company Profiles |

| 12.1 Knauf Insulation Singapore |

| 12.2 Armacell Asia Pte Ltd |

| 12.3 ROCKWOOL Building Materials (Singapore) Pte. Ltd. |

| 12.4 Top Foam Industries Pte Ltd |

| 12.5 Owens Corning |

| 12.6 KROSSLINKER |

| 12.7 Sealumet Singapore Pte Ltd |

| 12.8 Morgan Advanced Materials plc |

| 12.9 Covestro AG |

| 12.10 Saint-Gobain (Singapore) Pte Ltd |

| 12.11 Kingspan Singapore |

| 12.12 Huntsman International LLC |

| 12.13 SOPREMA, Inc. |

| 12.14 NICHIAS Singapore Pte. Ltd. |

| 12.15 PGF Insulation Sdn. Bhd. |

| 13. Key Strategic Recommendations |

| 14. Disclaimer |

| List of Figures |

| 1. Singapore Insulation Products Market Revenues, 2022-2032F ($ Million) |

| 2. Singapore Number of Private Residential Units Supply in Pipeline, 2032E-2028F |

| 3. Singapore Insulation Products Market Revenue Share, By Insulation Type, 2032 & 2031F |

| 4. Singapore Insulation Products Market Revenue Share, By Material Type, 2032 & 2031F |

| 5. Singapore Insulation Products Market Revenue Share, By End-Use, 2032 & 2031F |

| 6. Singapore Number of Hotel Rooms Supply in Pipeline, 2032E Onwards |

| 7. Singapore Retail Spaces Supply, 2032E Onwards (000 sq m gross) |

| 8. Singapore Insulation Products Market Opportunity Assessment, By Insulation Type, 2031F |

| 9. Singapore Insulation Products Market Opportunity Assessment, By Material Type, 2031F |

| 10. Singapore Insulation Products Market Opportunity Assessment, By End-Use, 2031F |

| 11. Singapore Insulation Products Market Revenue Ranking, By Companies, CY2032 |

| List of Table |

| 1. Singapore Major Construction Projects, 2025E-2028F |

| 2. Singapore Ongoing Energy Efficiency Initiatives/Strategy |

| 3. Singapore ICT Ecosystem Developments Initiatives/Investments |

| 4. Singapore Under Construction Data Centres, As of Feb 2032 |

| 5. Singapore Insulation Products Market Revenues, By Insulation Type, 2022-2032F ($ Million) |

| 6. Singapore Insulation Products Market Revenues, By Material Type, 2022-2032F ($ Million) |

| 7. Singapore Insulation Products Market Revenues, By End-Use, 2022-2032F ($ Million) |

| 8. Singapore Luxury Residential Transactions in H2 2023 |

| 9. Singapore Major Office Projects, 2032 |

| 10. Singapore Ongoing and Upcoming Major Construction Projects, 2026F-28F |

Global Go To Market Strategy - 2030

Export potential enables firms to identify high-growth global markets with greater confidence by combining advanced trade intelligence with a structured quantitative methodology. The framework analyzes emerging demand trends and country-level import patterns while integrating macroeconomic and trade datasets such as GDP and population forecasts, bilateral import–export flows, tariff structures, elasticity differentials between developed and developing economies, geographic distance, and import demand projections. Using weighted trade values from 2020–2024 as the base period to project country-to-country export potential for 2030, these inputs are operationalized through calculated drivers such as gravity model parameters, tariff impact factors, and projected GDP per-capita growth. Through an analysis of hidden potentials, demand hotspots, and market conditions that are most favorable to success, this method enables firms to focus on target countries, maximize returns, and global expansion with data, backed by accuracy.

By factoring in the projected importer demand gap that is currently unmet and could be potential opportunity, it identifies the potential for the Exporter (Country) among 190 countries, against the general trade analysis, which identifies the biggest importer or exporter.

To discover high-growth global markets and optimize your business strategy:

Click Here

Pricing

- Single User License$ 1,995

- Department License$ 2,400

- Site License$ 3,120

- Global License$ 3,795

Leadership Perspectives from Industry Events

Search

Thought Leadership and Analyst Meet

Our Clients

6WResearch In News

- India Export Attractiveness Tracker 2026

- India Air Conditioner Market Set for Strong Rebound in 2026 After Weather-Led Correction and GST-Driven Recovery: 6Wresearch

- ADAS in India: How Automatic Emergency Braking, Blind Spot Detection & Driver Monitoring are Transforming Road Safety

- Doha a strategic location for EV manufacturing hub: IPA Qatar

- Demand for luxury TVs surging in the GCC, says Samsung

- Empowering Growth: The Thriving Journey of Bangladesh’s Cable Industry

Latest Reports

- Greece Insulated Sandwich Panels Market (2026-2032)

- Qatar Access and Home Network Market (2026-2032)

- Nicaragua RPG Gaming Market (2026-2032)

- New Zealand RPG Gaming Market (2026-2032)

- Netherlands RPG Gaming Market (2026-2032)

- Nauru RPG Gaming Market (2026-2032)

- Namibia RPG Gaming Market (2026-2032)

- Mozambique RPG Gaming Market (2026-2032)

- Montenegro RPG Gaming Market (2026-2032)

- Mongolia RPG Gaming Market (2026-2032)

Industry Events and Analyst Meet

EV India Expo 2026

HIMTEX 2026

India Refining Summit 2026

India EV Show 2026

EV tech India Expo 2026

Whitepaper

- Middle East & Africa Commercial Security Market Click here to view more.

- Middle East & Africa Fire Safety Systems & Equipment Market Click here to view more.

- GCC Drone Market Click here to view more.

- Middle East Lighting Fixture Market Click here to view more.

- GCC Physical & Perimeter Security Market Click here to view more.