Latin America Food Packaging Market (2026-2032) | COVID-19 IMPACT, Size, Outlook, Forecast, Revenue, Companies, Analysis, Trends, Growth, Share, Value & Industry

Market Forecast by Application (dairy products, meat, poultry & seafood, fruits & vegetables, sauce & dressings, bakery & confectionary and others), by Product Type (rigid, semi-rigid and flexible), by Material Type (paper & board, plastic, metal, glass and others), By Countries (Mexico, Chile, Brazil, Argentina and rest of Latin America) and Competitive Landscape

| Product Code: ETC054547 | Publication Date: Apr 2021 | Product Type: Report | ||

| Publisher: 6Wresearch | Author: Ravi Bhandari | No. of Pages: 200 | No. of Figures: 90 | No. of Tables: 30 |

Latin America Food Packaging Market Size, Share & Growth Rate

The Latin America Food Packaging Market was estimated at USD 226 Million in 2025 and is projected to reach USD 316 Million by 2032, growing at a CAGR of 4.9% from 2026 to 2032. The anticipated growth trajectory is driven by a noticeable shift in consumer habits, with an increased appetite for convenience foods, particularly in burgeoning urban areas. Furthermore, the ongoing rise of the middle-class population and growing demand for sustainable packaging solutions play crucial roles in propelling this market forward.

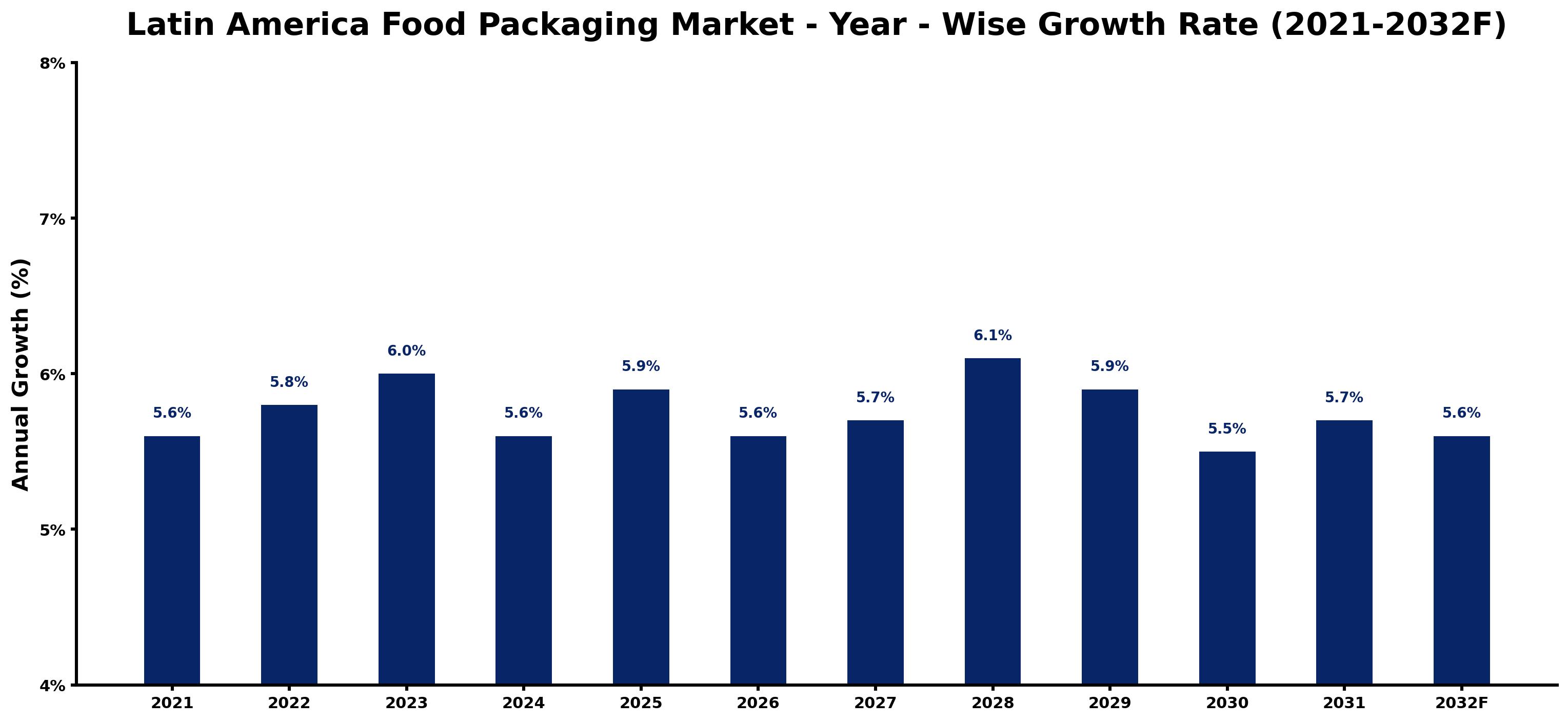

Latin America Food Packaging Market Growth Rate Analysis (2021-2032)

The Latin America food packaging market is experiencing stable growth, with notable increases in demand driven by evolving consumer preferences and a shift towards sustainable packaging solutions. Growth rates have shown a modest rise, from 5.6% in 2021 to 6.0% in 2023, before stabilizing around 5.7% to 5.9% in subsequent years. Factors contributing to this trend include enhanced agricultural productivity, technological advancements in packaging manufacturing, and heightened regulations promoting eco-friendly materials. The anticipated growth to 6.1% in 2028 reflects ongoing investments in digitalization and infrastructure improvements, which are crucial for meeting the rising consumer demand for convenience and sustainability in food packaging options.

Latin America Food Packaging Market Year-wise Growth Rate and Key Drivers

This graph highlights how the Latin America Food Packaging Market has steadily grown over the past five years, supported by major growth factors.

The table below presents the year‑wise growth rates along with the key drivers influencing the market

| Year | Growth Rate | Major Drivers |

| 2021 | 5.6% | Rapid growth in telecom and data center sectors |

| 2022 | 5.8% | Rapid growth in telecom and data center sectors |

| 2023 | 6.0% | Government infrastructure modernization initiatives |

| 2024 | 5.6% | Rising electricity demand across industries |

| 2025 | 5.9% | Increasing industrial automation investments |

| 2026 | 5.6% | Growing renewable energy integration projects |

| 2027 | 5.7% | Increasing industrial infrastructure investments |

| 2028 | 6.1% | Increasing smart city development projects |

| 2029 | 5.9% | Expansion of transportation and logistics networks |

| 2030 | 5.5% | Increasing industrial automation investments |

| 2031 | 5.7% | Increasing adoption of advanced technologies |

| 2032 | 5.6% | Increasing adoption of advanced technologies |

Note - Market size estimations and growth projections presented in this report are based on 6Wresearch’s advanced forecasting approach, validated with industry datasets as of June 2026.

Latin America Food Packaging Market Synopsis

The most significant force shaping the Latin America Food Packaging Market today is the escalating demand for processed and convenience food products. As lifestyle changes accelerate, consumers are prioritizing convenience, leading to an uptick in the popularity of ready-to-eat meals and packaged foods.

In addition, innovations in packaging technology, such as modified atmosphere packaging, are gaining traction. This trend is partially fueled by increasing consumer expectations for product transparency and minimal processing, signifying a major shift in the food packaging landscape of the region.

Latin America Food Packaging Market Key Takeaways

- The Latin America Food Packaging Market is poised for significant growth, with Brazil and Mexico as key players.

- Urbanization and an expanding middle class are accelerating demand for convenience foods, thereby boosting packaging needs.

- Emerging trends in sustainability are driving innovations in packaging solutions across the region.

- Consumer preferences are shifting toward products that offer longer shelf life and reduced environmental impact.

- Investment in modified atmosphere packaging is increasing due to consumer demand for fresher, minimally processed foods.

Evaluation of Restraints in Latin America Food Packaging Market

Despite the promising outlook for the Latin America Food Packaging Market, several factors may impede growth. Economic fluctuations and inflation rates can affect consumer purchasing power, limiting expenditures on packaged foods. Additionally, regulatory challenges surrounding packaging materials and environmental standards may pose hurdles for manufacturers. The lingering effects of the COVID-19 pandemic have also led to shifts in production capacities and supply chain disruptions, which could continue to impact market dynamics in the near term.

Latin America Food Packaging Market Trends

Several trends are shaping the Latin America Food Packaging Market today. A notable trend is the rise in demand for flexible packaging solutions, which offer versatility and convenience for both manufacturers and consumers. Additionally, there is a growing focus on environmentally sustainable packaging options as consumers become increasingly eco-conscious. These trends indicate a shift towards greater innovation and adaptability in food packaging, responding to the evolving preferences of consumers.

Latin America Food Packaging Market Opportunities

The Latin America Food Packaging Market presents numerous growth opportunities for stakeholders. The expansion of e-commerce and the food delivery sector has created a surge in demand for effective packaging solutions that can maintain product integrity during transportation. Moreover, investment in research and development for smart packaging technologies, such as tamper-evident and QR-coded packaging, can provide additional avenues for growth. Engaging in partnerships with local manufacturers can also facilitate entry into underserved regions, boosting market reach.

Government Initiatives in the Latin America Food Packaging Market

Governments across Latin America are implementing various initiatives to promote the food packaging sector. These include grants and funding programs aimed at fostering innovation in packaging materials and processes. Environmental regulations are encouraging companies to shift towards more sustainable practices, often accompanied by government incentives for adopting eco-friendly packaging solutions. Such measures not only help in compliance with regulations but also enhance market competitiveness by aligning with consumer expectations.

Future Insights of the Latin America Food Packaging Market

Looking ahead to 2026-2032, the Latin America Food Packaging Market is expected to witness continued expansion driven by urbanization and rising disposable incomes. Increased consumer focus on health and nutrition is likely to further elevate demand for packaged goods that offer convenience without compromising quality. Furthermore, as technology continues to evolve, we can expect advancements in packaging innovations that address both functional needs and environmental concerns, positioning this market for robust growth in the coming years.

Latin America Food Packaging Market Latest Developments (May 2025 - June 2026)

In recent months, the Latin America Food Packaging Market has seen significant shifts towards sustainable practices. Many manufacturers are investing in biodegradable materials and innovative recycling programs. Furthermore, collaboration among various stakeholders, including packaging designers and food producers, has intensified as they seek to address the increasing consumer demand for transparency and safety in food packaging. Companies are also leveraging technology to enhance supply chain efficiencies and optimize packaging processes.

Latin America Food Packaging Market - Key Attractiveness of the Report

- 10 Years of Market Numbers

- Historical Data Starting from 2022 to 2025

- Base Year: 2025

- Forecast Data until 2032

- Key Performance Indicators Impacting the Market

- Major Upcoming Developments and Projects

Latin America Food Packaging Market - Frequently Asked Questions

The growth is primarily driven by the increasing demand for convenience foods and the ongoing rise in urbanization. As consumers seek more packaged and processed food options, the demand for effective food packaging solutions continues to surge.

The COVID-19 pandemic led to initial disruptions in production and supply chains; however, it has also heightened consumer awareness around hygiene and packaging safety, further emphasizing the importance of robust food packaging solutions.

The Latin America Food Packaging Market was estimated at USD 226 Million in 2025 and is projected to reach USD 316 Million by 2032, growing at a CAGR of 4.9% from 2026 to 2032.

Brazil and Mexico are the leading countries driving growth in the Latin America Food Packaging Market, supported by increasing urbanization and a growing middle class.

Key trends include a shift towards sustainable packaging materials, increased adoption of flexible packaging, and the development of smart packaging solutions that enhance consumer convenience and safety.

Opportunities lie in the burgeoning demand for e-commerce and food delivery services, alongside a growing interest in sustainable packaging solutions. Companies are encouraged to innovate and explore partnerships to maximize their market presence.

6Wresearch actively monitors the Latin America Food Packaging Market and publishes its comprehensive annual report, highlighting emerging trends, growth drivers, revenue analysis, and forecast outlook. Our insights help businesses to make data-backed strategic decisions with ongoing market dynamics. Our analysts track relevent industries related to the Latin America Food Packaging Market, allowing our clients with actionable intelligence and reliable forecasts tailored to emerging regional needs.

Yes, we provide customisation as per your requirements. To learn more, feel free to contact us on sales@6wresearch.com

|

1. Executive Summary |

|

2. Introduction |

|

2.1. Key Highlights of the Report |

|

2.2. Report Description |

|

2.3. Market Scope & Segmentation |

|

2.4. Research Methodology |

|

2.5. Assumptions |

|

3. Latin America Food Packaging Market Overview |

|

3.1. Latin America Food Packaging Market Revenues, 2022 & 2032F |

|

3.2. Latin America Food Packaging Market - Industry Life Cycle |

|

3.3. Latin America Food Packaging Market - Porter's Five Forces |

|

3.4. Latin America Food Packaging Market Revenue Share, By Application, 2022 & 2032F |

|

3.5. Latin America Food Packaging Market Revenue Share, By Material Type, 2022 & 2032F |

|

3.6. Latin America Food Packaging Market Revenue Share, By Product Type, 2022 & 2032F |

|

3.7. Latin America Food Packaging Market Revenue Share, By Countries, 2022 & 2032F |

|

4. Latin America Food Packaging Market Dynamics |

|

4.1. Impact Analysis |

|

4.2. Market Drivers |

|

4.3. Market Restraints |

|

5. Latin America Food Packaging Market Trends |

|

6. Latin America Food Packaging Market, By Application |

|

6.1. Latin America Food Packaging Market, By Application |

|

6.1.1. Overview and Analysis |

|

6.1.2. Latin America Food Packaging Market Revenues, By Bakery & Confectionery, 2022-2032F |

|

6.1.3. Latin America Food Packaging Market Revenues, By Dairy Products, 2022-2032F |

|

6.1.4. Latin America Food Packaging Market Revenues, By Fruits & Vegetables, 2022-2032F |

|

6.1.5. Latin America Food Packaging Market Revenues, By Meat, Poultry & Seafood, 2022-2032F |

|

6.1.6. Latin America Food Packaging Market Revenues, By Sauces & Dressings, 2022-2032F |

|

6.1.7. Latin America Food Packaging Market Revenues, By Others, 2022-2032F |

|

7. Latin America Food Packaging Market, By Material Type |

|

7.1. Latin America Food Packaging Market, By Material Type |

|

7.1.1. Overview and Analysis |

|

7.1.2. Latin America Food Packaging Market Revenues, By Paper & Board, 2022-2032F |

|

7.1.3. Latin America Food Packaging Market Revenues, By Plastic, 2022-2032F |

|

7.1.4. Latin America Food Packaging Market Revenues, By Metal, 2022-2032F |

|

7.1.5. Latin America Food Packaging Market Revenues, By Glass, 2022-2032F |

|

7.1.6. Latin America Food Packaging Market Revenues, By Others, 2022-2032F |

|

8. Latin America Food Packaging Market, By Product Type |

|

8.1. Latin America Food Packaging Market, By Product Type |

|

8.1.1. Overview and Analysis |

|

8.1.2. Latin America Food Packaging Market Revenues, By Rigid, 2022-2032F |

|

8.1.3. Latin America Food Packaging Market Revenues, By Semi-rigid Range, 2022-2032F |

|

8.1.4. Latin America Food Packaging Market Revenues, By Flexible, 2022-2032F |

|

10. Chile Food Packaging Market |

|

10.1. Chile Food Packaging Market, By Application |

|

10.2. Chile Food Packaging Market, By Material Type |

|

10.3. Chile Food Packaging Market, By Product Type |

|

10.4. Chile Food Packaging Market, By Countries |

|

11. Argentina Food Packaging Market |

|

11.1. Argentina Food Packaging Market, By Application |

|

11.2. Argentina Food Packaging Market, By Material Type |

|

11.3. Argentina Food Packaging Market, By Product Type |

|

11.4. Argentina Food Packaging Market, By Countries |

|

12. Brazil Food Packaging Market |

|

12.1. Brazil Food Packaging Market, By Application |

|

12.2. Brazil Food Packaging Market, By Material Type |

|

12.3. Brazil Food Packaging Market, By Product Type |

|

12.4. Brazil Food Packaging Market, By Countries |

|

13. Mexico Food Packaging Market |

|

13.1. Mexico Food Packaging Market, By Application |

|

13.2. Mexico Food Packaging Market, By Material Type |

|

13.3. Mexico Food Packaging Market, By Product Type |

|

13.4. Mexico Food Packaging Market, By Countries |

|

14. Rest of Latin America Food Packaging Market |

|

14.1. Rest of Latin America Food Packaging Market Overview |

|

15. Latin America Food Packaging Market Import-Export Trade Statistics |

|

15.1. Latin America Food Packaging Market Export to Major Countries |

|

15.2. Latin America Food Packaging Market Imports from Major Countries |

|

16. Latin America Food Packaging Market Key Performance Indicators |

|

17. Latin America Food Packaging Market - Opportunity Assessment |

|

17.1. Latin America Food Packaging Market Opportunity Assessment, By Application, 2022 & 2032F |

|

17.2. Latin America Food Packaging Market Opportunity Assessment, By Material Type, 2022 & 2032F |

|

18. Latin America Food Packaging Market - Competitive Landscape |

|

18.1. Latin America Food Packaging Market Revenue Share, By Companies, 2025 |

|

18.2. Latin America Food Packaging Market Competitive Benchmarking, By Operating and Technical Parameters |

|

19. Company Profiles |

|

20. Recommendations |

|

21. Disclaimer |

Global Go To Market Strategy - 2030

Export potential enables firms to identify high-growth global markets with greater confidence by combining advanced trade intelligence with a structured quantitative methodology. The framework analyzes emerging demand trends and country-level import patterns while integrating macroeconomic and trade datasets such as GDP and population forecasts, bilateral import–export flows, tariff structures, elasticity differentials between developed and developing economies, geographic distance, and import demand projections. Using weighted trade values from 2020–2024 as the base period to project country-to-country export potential for 2030, these inputs are operationalized through calculated drivers such as gravity model parameters, tariff impact factors, and projected GDP per-capita growth. Through an analysis of hidden potentials, demand hotspots, and market conditions that are most favorable to success, this method enables firms to focus on target countries, maximize returns, and global expansion with data, backed by accuracy.

By factoring in the projected importer demand gap that is currently unmet and could be potential opportunity, it identifies the potential for the Exporter (Country) among 190 countries, against the general trade analysis, which identifies the biggest importer or exporter.

To discover high-growth global markets and optimize your business strategy:

Click Here

Pricing

- Single User License$ 4,560

- Department License$ 5,055

- Site License$ 5,595

- Global License$ 6,000

Leadership Perspectives from Industry Events

Search

Thought Leadership and Analyst Meet

Our Clients

6WResearch In News

- India Air Conditioner Market Set for Strong Rebound in 2026 After Weather-Led Correction and GST-Driven Recovery: 6Wresearch

- ADAS in India: How Automatic Emergency Braking, Blind Spot Detection & Driver Monitoring are Transforming Road Safety

- Doha a strategic location for EV manufacturing hub: IPA Qatar

- Demand for luxury TVs surging in the GCC, says Samsung

- Empowering Growth: The Thriving Journey of Bangladesh’s Cable Industry

- Demand for luxury TVs surging in the GCC, says Samsung

Latest Reports

- Nicaragua RPG Gaming Market (2026-2032)

- New Zealand RPG Gaming Market (2026-2032)

- Netherlands RPG Gaming Market (2026-2032)

- Nauru RPG Gaming Market (2026-2032)

- Namibia RPG Gaming Market (2026-2032)

- Mozambique RPG Gaming Market (2026-2032)

- Montenegro RPG Gaming Market (2026-2032)

- Mongolia RPG Gaming Market (2026-2032)

- Monaco RPG Gaming Market (2026-2032)

- Micronesia RPG Gaming Market (2026-2032)

Industry Events and Analyst Meet

HIMTEX 2026

India Refining Summit 2026

India EV Show 2026

EV tech India Expo 2026

Auto Tech Asia 2026

Whitepaper

- Middle East & Africa Commercial Security Market Click here to view more.

- Middle East & Africa Fire Safety Systems & Equipment Market Click here to view more.

- GCC Drone Market Click here to view more.

- Middle East Lighting Fixture Market Click here to view more.

- GCC Physical & Perimeter Security Market Click here to view more.