Brazil Beer Market (2025-2031) | Share, Size, Industry, Forecast, Companies, Value, Revenue, Growth, Analysis, Trends & Outlook

Market Forecast By Type (Lager, Ale, Stout & Porter, Malt, Others), By Category (Popular Price, Premium, Super Premium), By Packaging (Glass, PET Bottle, Metal Can, Others), By Production (Macro-brewery, Micro-brewery, Craft Brewery, Others) And Competitive Landscape

| Product Code: ETC048282 | Publication Date: Jan 2021 | Updated Date: Oct 2025 | Product Type: Report | |

| Publisher: 6Wresearch | Author: Ravi Bhandari | No. of Pages: 70 | No. of Figures: 35 | No. of Tables: 5 |

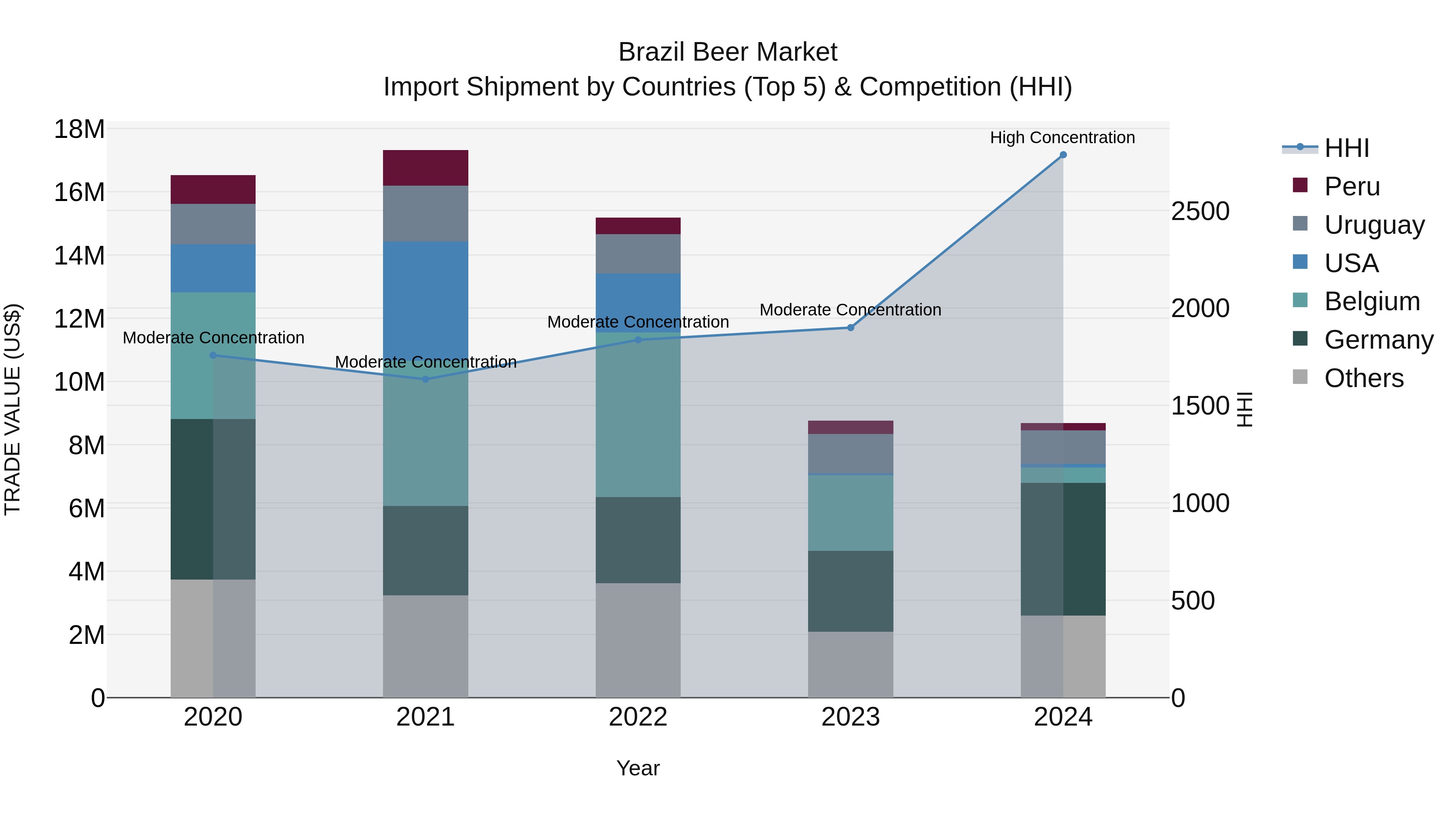

Brazil Beer Market Top 5 Importing Countries and Market Competition (HHI) Analysis

Brazil`s beer import market saw a shift in concentration levels from moderate to high in 2024, with top exporting countries being Germany, Argentina, Uruguay, Belgium, and the UK. Despite a negative Compound Annual Growth Rate (CAGR) of -14.87% from 2020 to 2024, the market experienced a slightly improved growth rate of -0.94% in 2024 compared to the previous year. This data suggests a challenging environment for beer importers in Brazil, potentially influenced by changing consumer preferences or market dynamics. Stakeholders may need to adapt strategies to navigate the evolving landscape and maintain competitiveness.

Brazil Beer Market Growth Rate

According to 6Wresearch internal database and industry insights,

Brazil Beer Market Highlights

| Report Name | Brazil Beer Market |

| Forecast period | 2025-2031 |

| CAGR | 6.2% |

| Growing Sector | Premiumization & On-trade Recovery |

Topics Covered in the Brazil Beer Market Report

The Brazil Beer Market report thoroughly covers the market by type, category, packaging, and production. The market report provides an unbiased and detailed analysis of ongoing market trends, opportunities/high growth areas, and market drivers, which would help stakeholders to devise and align their market strategies according to the current and future market dynamics.

Brazil Beer Market Synopsis

Brazil Beer Market is expected to grow during the forecast period due to tourism, the middle-class population, and a rise in disposable income. The major global and domestic Key Players are mostly helping the growing industry. Beer is an alcoholic drink made mainly from water, malted grains hops, and yeast.

The government is actively working through initiatives to help the Brazil beer market become an even bigger contributor to the economy. In the future, the rise of the middle class and tourism is expected to continue to create growth opportunities for the beer market, though it will be met with continuing challenges such as high taxation and economic instability.

Evaluation of Growth Drivers in the Brazil Beer Market

Below mentioned are some progressive drivers and their influence on the market arena:

|

Drivers |

Primary Segments Affected |

Why it matters (evidence) |

|

Premiumization & Changing Tastes |

Premium, Super Premium, Craft; On-trade & E-commerce |

Brazilian consumers are advancing towards luxurious and craft beers for taste, variety, and occasion-driven consumption, growing per-liter value and promoting higher margins. |

|

On-trade & Event Recovery |

Glass, Metal Can; On-trade channels |

Reopening of bars, restaurants, and festivals rises draft and luxurious brand consumption, developing visibility and volumes. |

|

Distribution & Export Support |

Macro-brewery, Micro-brewery; PET and Metal Can |

Export support programs and incentives allow craft and microbrewers to scale and access foreign markets, improving production utilization. |

|

E-commerce & Omnichannel Sales |

Packaging: PET, Can, Glass; All Categories |

Growth in online and direct-to-consumer channels enables breweries to reach urban consumers and niche audiences efficiently. |

The Brazil Beer Market size is projected to grow at the CAGR of 6.2% during the forecast period of 2025-2031. One of the most significant drivers of the Brazil beer market growth is tourism. Brazil is considered a top tourist destination and beer plays a crucial role in the country's tourism industry. Beer is an essential part of the Brazilian culture and people often associate their travels with sampling local beer.

Additionally, the rising disposable income among Brazilians is also a significant driver of beer market growth. Another driver is the growing middle-class population. This demographic is more likely to consume premium beers, contributing to the overall growth of the market. The growing economy has led to an increase in purchasing power, which has contributed to the growth of the Brazil Beer Market.

Evaluation of Restraints in the Brazil Beer Market

Below mentioned are some major restraints and their influence on the market landscape:

|

Restraints |

Primary Segments Affected |

What this means (evidence) |

|

Tax & Regulatory Complexity |

All Categories |

Complex indirect tax structure (IPI, PIS/COFINS, state taxes) raises cost and pricing complexity, affecting margins for both large and small brewers. |

|

Input Cost Volatility |

Macro-brewery & Craft |

Rising malt, hops, packaging, logistics, and energy costs increase production expenses and compress margins. |

|

Competition from Other Alcoholic & Non-Alcoholic Drinks |

Popular Price & RTD segments |

Consumers are moving towards low-alcohol and non-alcoholic beverages side-tracks consumption, therefore the beer market will be needing reformulation and creativity. |

|

Distribution Concentration |

Macro-brewery (largest players) |

Distribution chains concentration gives special treatment to large brewers, creating obstacles for small and regional entrants. |

Brazil Beer Market Challenges

The Brazil Beer Market is facing several challenges. One of the main challenges is the high tax rate on alcoholic beverages. This has made beer expensive, and it is inaccessible to a large section of the population. Additionally, the Brazil beer market is highly regulated, and companies face several bureaucratic procedures to operate in the market. This makes it challenging for new entrants to establish themselves in the market. Therefore, it becomes difficult for many new entrants to allocate money in this sector and enter the market.

Brazil Beer Market Trends

Some of notable trends shaping the market landscape are:

Hybrid Portfolios: Major brewers are extending non-alcoholic, flavoured, and low-alcohol lines. This is being done to meet health-conscious and occasional drinkers requirement.

Premium & Craft Momentum: Premium and craft segments persist to develop faster than mainstream volumes. Thus, it will be attracting investments and M&A activities.

On-trade Experience & Events: Festivals, gastronomy, and on-trade activations spurs brand trial and consumer loyalty.

Packaging Innovation & Sustainability: Shift to cans, lightweight packaging, and water-saving practices for environmental compliance.

Digital & Direct Sales: Breweries leveraging e-commerce, subscription, and D2C channels to reach urban and premium consumers.

Investment Opportunities in the Brazil Beer Industry

There are numerous leading investment opportunities in the market which are:

Premium & Craft Capacity Expansion: Invest in brewery capacity, taprooms, and regional create adventures to align with increasing requirement.

Export-oriented Craft Brands: Utilize export programs and agribusiness linkages to scale production and access foreign markets.

Sustainable Packaging & Water Efficiency: Make recyclable/returnable packaging and use water-saving brewing technologies.

Ready-to-Drink & Low-Alcohol Lines: Introduce low-alcohol and flavoured RTD beers which will appeal to health-oriented and occasional drinkers.

On-trade Partnerships & Event Activation: Partner with venues, festivals, and hospitality groups to get brand exposure and premium placement.

Top 5 Leading Players in the Brazil Beer Market

Some leading players operating in the market include:

Ambev S.A.

Established Year: 1999 (current corporate form)

Headquarters: São Paulo, Brazil

Official Website: https://www.ambev.com.br

Ambev is Brazil’s biggest brewer and beverage company in Latin America, owning brands such as Skol, Brahma, and Antarctica, as well as non-alcoholic beverages. Its scale, distribution chains, and malting abilities make it a market leader.

Heineken Brasil (Grupo Heineken)

Established Year (Brazil presence): 2010

Headquarters: São Paulo, Brazil

Official Website: https://www.heinekenbrasil.com.br

Heineken Brasil is the second-largest brewer in Brazil by value, with a multi-brand portfolio consisting of Devassa, Eisenbahn, and Baden Baden. Its strategy focuses craft/premium extention and sustainability initiatives.

Grupo Petrópolis

Established Year: 1994

Headquarters: Petrópolis, Brazil

Official Website: https://www.grupopetropolis.com.br

Grupo Petrópolis is a leading domestic brewer with brands such as Itaipava and Crystal, functioning several plants and concentrating on national sourcing and regional distribution.

Cervejaria Backer / Regional Craft Leaders

Established Year: Various

Headquarters: Multiple locations

Official Website: https://www.cervejariatreslobos.com.br

Backer and other regional craft breweries focus on premium and specialty beers, leveraging local flavors and limited-edition brews to capture niche markets.

Brasil Kirin (now part of Heineken acquisition portfolio)

Established Year: 2000 (Brazil operations)

Headquarters: São Paulo, Brazil

Official Website: https://www.heinekenbrasil.com.br

Brasil Kirin produces several local brands and regional beers, focussing on traditional Brazilian styles and combining modern brewing technologies.

Government Regulations Introduced in the Brazil Beer Market

According to Brazilian government data, initiatives to support the growth of the beer market has been implemented by the Brazilian government. One such initiative is the reduction in the amount of bureaucracy and the simplification of the legal framework for beer production, distribution, and sale. Additionally, the government has a program called "Mais Cerveja" (More Beer), which aims to stimulate the production and consumption of beer in Brazil, supporting small- and medium-sized beer companies.

Future Insights of the Brazil Beer Market

The Brazil Beer Industry is expected to continue to grow, driven by several factors. The rising middle class, urbanization, and tourism are expected to continue to play a significant role in the future of the market. Additionally, innovation in the industry, such as the development of craft beers and the use of technology in the manufacturing process, will help the industry stay competitive. Challenges such as high taxation and economic instability are expected to continue, but the industry is well-positioned to overcome these challenges and continue to grow.

Market Segmentation Analysis

The report offers a comprehensive study of the subsequent market segments and their leading categories.

Ale to Dominate the Market - By Type

The type of beer that is expected to grow the most in the Brazilian beer market in the forecast period is ale. Ales are generally more flavourful and complex than lagers, and consumers in Brazil are increasingly interested in trying new and innovative beer styles.

Premium to Dominate the Market By Category

The premium segment of the Brazil Beer Market Share is expected to see the highest growth. Premium beers are more expensive than mainstream beers and typically have a higher alcohol content and more complex flavours. This segment appeals to consumers who are looking for a higher quality drinking experience and are willing to pay more for it.

PET bottle to Dominate the Market By Packaging

According to Parth, Senior Research Analyst, 6Wresearch, PET bottle is anticipated to see the most growth, as they are cheaper to manufacture and transport than other packaging formats. PET bottles are also more environmentally friendly than other types of packaging.

Macro-brewery to Dominate the Market - By Production

Macro-brewery to lead production and distribution nationwide, leveraging scale and logistics. Micro and craft breweries are also expanding rapidly, especially in urban centers and premium-focused channels, capitalizing on innovation, local sourcing, and regional storytelling.

Key Highlights of the Report:

- Brazil Beer Market Outlook

- Market Size of Brazil Beer Market, 2024

- Forecast of Brazil Beer Market, 2031

- Historical Data and Forecast of Brazil Beer Revenues & Volume for the Period 2021- 2031

- Brazil Beer Market Trend Evolution

- Brazil Beer Market Drivers and Challenges

- Brazil Beer Price Trends

- Brazil Beer Porter's Five Forces

- Brazil Beer Industry Life Cycle

- Historical Data and Forecast of Brazil Beer Market Revenues & Volume By Type for the Period 2021- 2031

- Historical Data and Forecast of Brazil Beer Market Revenues & Volume By Lager for the Period 2021- 2031

- Historical Data and Forecast of Brazil Beer Market Revenues & Volume By Ale for the Period 2021- 2031

- Historical Data and Forecast of Brazil Beer Market Revenues & Volume By Stout & Porter for the Period 2021- 2031

- Historical Data and Forecast of Brazil Beer Market Revenues & Volume By Malt for the Period 2021- 2031

- Historical Data and Forecast of Brazil Beer Market Revenues & Volume By Others for the Period 2021- 2031

- Historical Data and Forecast of Brazil Beer Market Revenues & Volume By Category for the Period 2021- 2031

- Historical Data and Forecast of Brazil Beer Market Revenues & Volume By Popular Price for the Period 2021- 2031

- Historical Data and Forecast of Brazil Beer Market Revenues & Volume By Premium for the Period 2021- 2031

- Historical Data and Forecast of Brazil Beer Market Revenues & Volume By Super Premium for the Period 2021- 2031

- Historical Data and Forecast of Brazil Beer Market Revenues & Volume By Packaging for the Period 2021- 2031

- Historical Data and Forecast of Brazil Beer Market Revenues & Volume By Glass for the Period 2021- 2031

- Historical Data and Forecast of Brazil Beer Market Revenues & Volume By PET Bottle for the Period 2021- 2031

- Historical Data and Forecast of Brazil Beer Market Revenues & Volume By Metal Can for the Period 2021- 2031

- Historical Data and Forecast of Brazil Beer Market Revenues & Volume By Others for the Period 2021- 2031

- Historical Data and Forecast of Brazil Beer Market Revenues & Volume By Production for the Period 2021- 2031

- Historical Data and Forecast of Brazil Beer Market Revenues & Volume By Macro-brewery for the Period 2021- 2031

- Historical Data and Forecast of Brazil Beer Market Revenues & Volume By Micro-brewery for the Period 2021- 2031

- Historical Data and Forecast of Brazil Beer Market Revenues & Volume By Craft Brewery for the Period 2021- 2031

- Historical Data and Forecast of Brazil Beer Market Revenues & Volume By Others for the Period 2021- 2031

- Brazil Beer Import Export Trade Statistics

- Market Opportunity Assessment By Type

- Market Opportunity Assessment By Category

- Market Opportunity Assessment By Packaging

- Market Opportunity Assessment By Production

- Brazil Beer Top Companies Market Share

- Brazil Beer Competitive Benchmarking By Technical and Operational Parameters

- Brazil Beer Company Profiles

- Brazil Beer Key Strategic Recommendations

Market Covered

The report offers a comprehensive study of the subsequent market segments:

By Type

- Lager

- Ale

- Stout & Porter

- Malt

- Others

By Category

- Popular Price

- Premium

- Super Premium

By Packaging

- Glass

- PET Bottle

- Metal Can

- Others

By Production

- Macro-Brewery

- Micro-Brewery

- Craft Brewery

- Others

Brazil Beer Market (2025-2031): FAQs

The Brazil Beer Market is predicted to grow at a CAGR of approximately 6.2% during 2025–2031.

Key drivers consist of rising disposable incomes, strong cultural preference for beer, and increasing popularity of premium and craft variants.

Policies supporting domestic hops and barley cultivation, as well as stringent regulations on alcohol marketing and taxation, are shaping the competitive arena of the market.

Challenges consist of high taxation, competition from spirits and non-alcoholic beverages, regulatory compliance prices, and changing raw material prices.

6Wresearch actively monitors the Brazil Beer Market and publishes its comprehensive annual report, highlighting emerging trends, growth drivers, revenue analysis, and forecast outlook. Our insights help businesses to make data-backed strategic decisions with ongoing market dynamics. Our analysts track relevent industries related to the Brazil Beer Market, allowing our clients with actionable intelligence and reliable forecasts tailored to emerging regional needs.

Yes, we provide customisation as per your requirements. To learn more, feel free to contact us on sales@6wresearch.com

| 1 Executive Summary |

| 2 Introduction |

| 2.1 Key Highlights of the Report |

| 2.2 Report Description |

| 2.3 Market Scope & Segmentation |

| 2.4 Research Methodology |

| 2.5 Assumptions |

| 3 Brazil Beer Market Overview |

| 3.1 Brazil Country Macro Economic Indicators |

| 3.2 Brazil Beer Market Revenues & Volume, 2021 & 2031F |

| 3.3 Brazil Beer Market - Industry Life Cycle |

| 3.4 Brazil Beer Market - Porter's Five Forces |

| 3.5 Brazil Beer Market Revenues & Volume Share, By Type, 2021 & 2031F |

| 3.6 Brazil Beer Market Revenues & Volume Share, By Category, 2021 & 2031F |

| 3.7 Brazil Beer Market Revenues & Volume Share, By Packaging, 2021 & 2031F |

| 3.8 Brazil Beer Market Revenues & Volume Share, By Production, 2021 & 2031F |

| 4 Brazil Beer Market Dynamics |

| 4.1 Impact Analysis |

| 4.2 Market Drivers |

| 4.2.1 Increasing disposable income of consumers in Brazil leading to higher spending on beer. |

| 4.2.2 Growing popularity of craft and specialty beers among consumers. |

| 4.2.3 Rising tourism in Brazil, boosting demand for beer in bars, restaurants, and hotels. |

| 4.3 Market Restraints |

| 4.3.1 Stringent government regulations and taxes on alcohol sales impacting profit margins. |

| 4.3.2 Health concerns and changing consumer preferences towards healthier beverages. |

| 4.3.3 Competition from other alcoholic and non-alcoholic beverages affecting market share. |

| 5 Brazil Beer Market Trends |

| 6 Brazil Beer Market, By Types |

| 6.1 Brazil Beer Market, By Type |

| 6.1.1 Overview and Analysis |

| 6.1.2 Brazil Beer Market Revenues & Volume, By Type, 2021 - 2031F |

| 6.1.3 Brazil Beer Market Revenues & Volume, By Lager, 2021 - 2031F |

| 6.1.4 Brazil Beer Market Revenues & Volume, By Ale, 2021 - 2031F |

| 6.1.5 Brazil Beer Market Revenues & Volume, By Stout & Porter, 2021 - 2031F |

| 6.1.6 Brazil Beer Market Revenues & Volume, By Malt, 2021 - 2031F |

| 6.1.7 Brazil Beer Market Revenues & Volume, By Others, 2021 - 2031F |

| 6.2 Brazil Beer Market, By Category |

| 6.2.1 Overview and Analysis |

| 6.2.2 Brazil Beer Market Revenues & Volume, By Popular Price, 2021 - 2031F |

| 6.2.3 Brazil Beer Market Revenues & Volume, By Premium, 2021 - 2031F |

| 6.2.4 Brazil Beer Market Revenues & Volume, By Super Premium, 2021 - 2031F |

| 6.3 Brazil Beer Market, By Packaging |

| 6.3.1 Overview and Analysis |

| 6.3.2 Brazil Beer Market Revenues & Volume, By Glass, 2021 - 2031F |

| 6.3.3 Brazil Beer Market Revenues & Volume, By PET Bottle, 2021 - 2031F |

| 6.3.4 Brazil Beer Market Revenues & Volume, By Metal Can, 2021 - 2031F |

| 6.3.5 Brazil Beer Market Revenues & Volume, By Others, 2021 - 2031F |

| 6.4 Brazil Beer Market, By Production |

| 6.4.1 Overview and Analysis |

| 6.4.2 Brazil Beer Market Revenues & Volume, By Macro-brewery, 2021 - 2031F |

| 6.4.3 Brazil Beer Market Revenues & Volume, By Micro-brewery, 2021 - 2031F |

| 6.4.4 Brazil Beer Market Revenues & Volume, By Craft Brewery, 2021 - 2031F |

| 6.4.5 Brazil Beer Market Revenues & Volume, By Others, 2021 - 2031F |

| 7 Brazil Beer Market Import-Export Trade Statistics |

| 7.1 Brazil Beer Market Export to Major Countries |

| 7.2 Brazil Beer Market Imports from Major Countries |

| 8 Brazil Beer Market Key Performance Indicators |

| 8.1 Consumer sentiment towards craft and specialty beers. |

| 8.2 Number of tourists visiting Brazil and their spending on beer. |

| 8.3 Innovation rate in product offerings in the beer market. |

| 9 Brazil Beer Market - Opportunity Assessment |

| 9.1 Brazil Beer Market Opportunity Assessment, By Type, 2021 & 2031F |

| 9.2 Brazil Beer Market Opportunity Assessment, By Category, 2021 & 2031F |

| 9.3 Brazil Beer Market Opportunity Assessment, By Packaging, 2021 & 2031F |

| 9.4 Brazil Beer Market Opportunity Assessment, By Production, 2021 & 2031F |

| 10 Brazil Beer Market - Competitive Landscape |

| 10.1 Brazil Beer Market Revenue Share, By Companies, 2024 |

| 10.2 Brazil Beer Market Competitive Benchmarking, By Operating and Technical Parameters |

| 11 Company Profiles |

| 12 Recommendations |

| 13 Disclaimer |

Global Go To Market Strategy - 2030

Export potential enables firms to identify high-growth global markets with greater confidence by combining advanced trade intelligence with a structured quantitative methodology. The framework analyzes emerging demand trends and country-level import patterns while integrating macroeconomic and trade datasets such as GDP and population forecasts, bilateral import–export flows, tariff structures, elasticity differentials between developed and developing economies, geographic distance, and import demand projections. Using weighted trade values from 2020–2024 as the base period to project country-to-country export potential for 2030, these inputs are operationalized through calculated drivers such as gravity model parameters, tariff impact factors, and projected GDP per-capita growth. Through an analysis of hidden potentials, demand hotspots, and market conditions that are most favorable to success, this method enables firms to focus on target countries, maximize returns, and global expansion with data, backed by accuracy.

By factoring in the projected importer demand gap that is currently unmet and could be potential opportunity, it identifies the potential for the Exporter (Country) among 190 countries, against the general trade analysis, which identifies the biggest importer or exporter.

To discover high-growth global markets and optimize your business strategy:

Click Here

Pricing

- Single User License$ 1,995

- Department License$ 2,400

- Site License$ 3,120

- Global License$ 3,795

Leadership Perspectives from Industry Events

Search

Thought Leadership and Analyst Meet

Our Clients

6WResearch In News

- India Air Conditioner Market Set for Strong Rebound in 2026 After Weather-Led Correction and GST-Driven Recovery: 6Wresearch

- ADAS in India: How Automatic Emergency Braking, Blind Spot Detection & Driver Monitoring are Transforming Road Safety

- Doha a strategic location for EV manufacturing hub: IPA Qatar

- Demand for luxury TVs surging in the GCC, says Samsung

- Empowering Growth: The Thriving Journey of Bangladesh’s Cable Industry

- Demand for luxury TVs surging in the GCC, says Samsung

Latest Reports

- Poland Fire Protection Systems Market (2026-2032)

- Cape Verde Portable Hand-Thrown Extinguisher Market (2026-2032)

- Canada Portable Hand-Thrown Extinguisher Market (2026-2032)

- Cameroon Portable Hand-Thrown Extinguisher Market (2026-2032)

- Burundi Portable Hand-Thrown Extinguisher Market (2026-2032)

- Burkina Faso Portable Hand-Thrown Extinguisher Market (2026-2032)

- Bulgaria Portable Hand-Thrown Extinguisher Market (2026-2032)

- Brunei Portable Hand-Thrown Extinguisher Market (2026-2032)

- Botswana Portable Hand-Thrown Extinguisher Market (2026-2032)

- Bosnia and Herzegovina Portable Hand-Thrown Extinguisher Market (2026-2032)

Industry Events and Analyst Meet

HIMTEX 2026

India Refining Summit 2026

India EV Show 2026

EV tech India Expo 2026

Auto Tech Asia 2026

Whitepaper

- Middle East & Africa Commercial Security Market Click here to view more.

- Middle East & Africa Fire Safety Systems & Equipment Market Click here to view more.

- GCC Drone Market Click here to view more.

- Middle East Lighting Fixture Market Click here to view more.

- GCC Physical & Perimeter Security Market Click here to view more.