Canada Carbon Market (2026-2032) | Companies, Value, Trends, Revenue, Share, Segmentation, Outlook, Size, Analysis, Growth, Industry & Forecast

Market Forecast By Product Types (Amorphous Carbon, Graphite, Diamond), By Applications (Automotive, Construction, Engineering Industries, Aerospace, Others) And Competitive Landscape

| Product Code: ETC4654217 | Publication Date: Nov 2023 | Updated Date: Mar 2026 | Product Type: Market Research Report | |

| Publisher: 6Wresearch | Author: Shubham Padhi | No. of Pages: 60 | No. of Figures: 30 | No. of Tables: 5 |

Canada Carbon Market: Import Trend Analysis

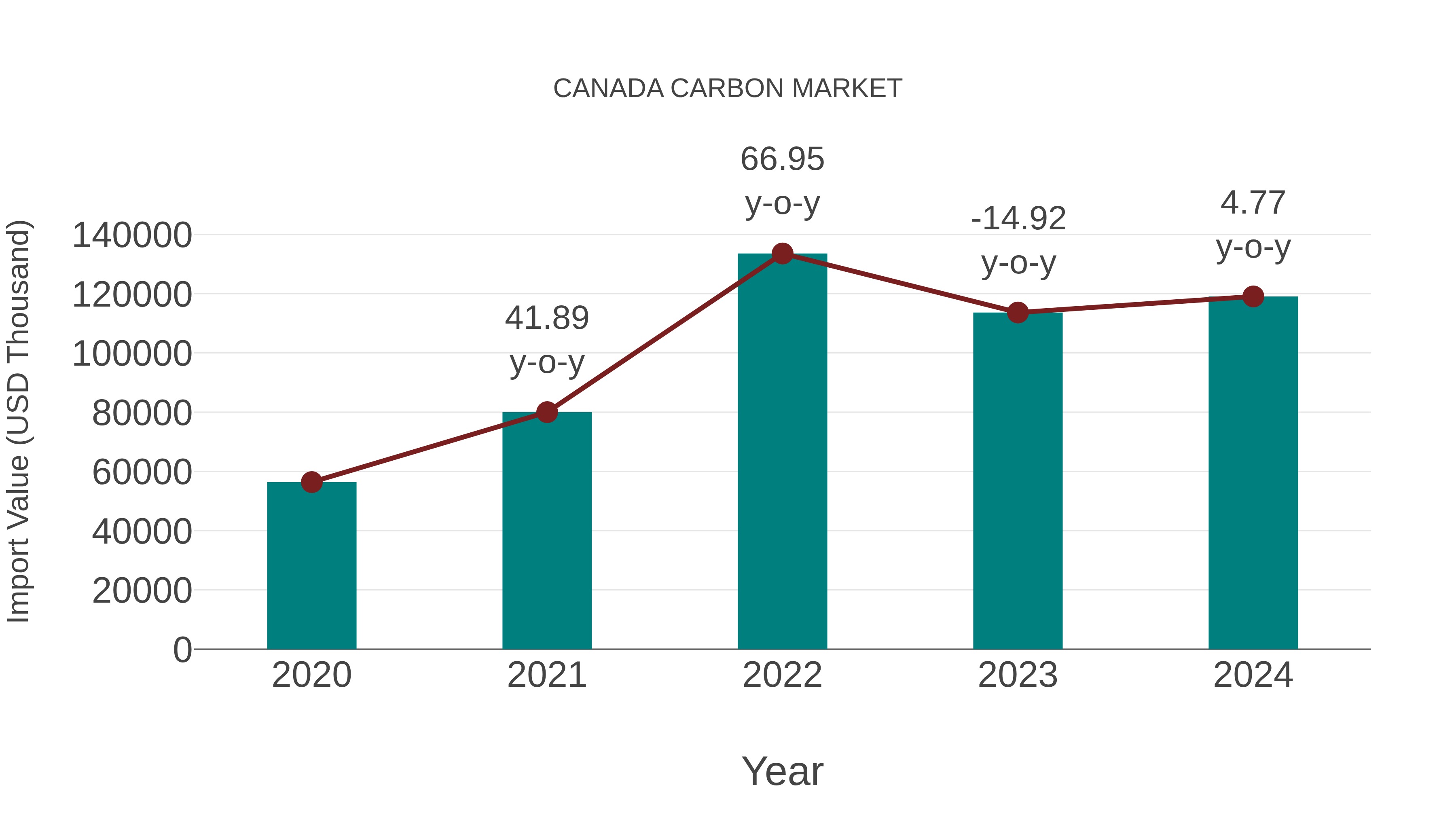

During 2020-2024, Canada`s carbon market imports exhibited a Compound Annual Growth Rate (CAGR) of 20.55%. In 2023-2024, the year-on-year growth rate was 4.77%, indicating a steady increase in imports. These figures reflect a consistent upward trend in the import of carbon market products in Canada during the specified period.

Canada Carbon Market Growth Rate

According to 6Wresearch internal database and industry insights, the Canada Carbon Market is projected to grow at a compound annual growth rate (CAGR) of 6.1% during the forecast period (2026–2032).

Five-Years Growth Trajectory of the Canada Carbon Market with Core Drivers

Below is the evaluation of the year-wise growth rate along with key drivers:

| Years | Estimated Annual Growth (%) | Growth Drivers |

| 2021 | 3.9 | Increasing use of carbon materials in automotive and industrial components |

| 2022 | 4.4 | Growth in construction activities and demand for high-strength materials |

| 2023 | 4.9 | Expansion of engineering industries and infrastructure modernization |

| 2024 | 5.4 | Rising adoption of advanced carbon materials in aerospace and manufacturing |

| 2025 | 5.8 | Government-backed clean technology programs and low-emission material initiatives |

Topics Covered in the Canada Carbon Market Report

The Canada Carbon Market report thoroughly covers the market by Product Types and Applications. The report provides a detailed analysis of ongoing market trends, opportunities/high-growth areas, and market drivers that will help stakeholders devise and align strategies according to current and future market dynamics.

Canada Carbon Market Highlights

| Report Name | Canada Carbon Market |

| Forecast period | 2026–2032 |

| CAGR | 6.1% |

| Growing Sector | Advanced Materials and Industrial Manufacturing |

Canada Carbon Market Synopsis

The Canada Carbon Industry is experiencing strong growth supported by increasing demand from automotive, construction, and engineering industries. Rising concentration on lightweight, durable, and high-performance materials is accelerating the adoption of carbon-based products. Development of aerospace manufacturing and advanced engineering applications is further bolstering the requirement of carbon material. Government-led efforts encouraging clean technologies, eco-efficient materials, and modern manufacturing procedures are supporting overall market development.

Evaluation of Growth Drivers in the Canada Carbon Market

Below are some prominent drivers and their influence on the Canada Carbon Market dynamics:

| Drivers | Primary Segments Affected | Why it Matters |

| Rising Automotive Lightweighting | By Applications (Automotive) | Lightweight carbon materials help enhance fuel efficiency and vehicle performance. |

| Infrastructure Development | By Applications (Construction) | Expanding infrastructure projects increase demand for strong and durable carbon materials. |

| Expansion of Engineering Industries | By Applications (Engineering Industries) | Advanced carbon products support high-performance and precision industrial applications. |

| Government Clean Technology Support | By Product Types (Amorphous Carbon, Graphite, Diamond) | Promotes adoption of low-emission, energy-efficient, and high-performance carbon materials. |

The Canada Carbon Market Size is projected to grow at a CAGR of 6.1% during the forecast period (2026–2032). The market is catapulted by the automotive and construction sectors demand, the upsurge of carbon materials usage in engineering, and the aerospace manufacturing to the extent of adoption. The Canada carbon market growth is additionally boosted by the government-led programs that encourage clean manufacturing practices, materials research, and emissions reduction. The market opportunities are also getting wider with increased investments in the development of high-performance and lightweight material solutions. Besides, the durability and energy efficiency attributes are pushing the carbon material adoption faster. The technological innovations in carbon processing along with the manufacturing techniques are also reinforcing the market expansion.

Evaluation of Restraints in the Canada Carbon Market

Below are some prominent restraints and their influence on the Canada Carbon Market dynamics:

| Restraints | Primary Segments Affected | What this Means |

| High Production Costs | By Product Types (Amorphous Carbon, Graphite, Diamond) | Elevated processing and energy costs increase product pricing. |

| Complex Manufacturing Processes | By Product Types | Need skilled labor, modern technology and precision control. |

| Supply Chain Volatility | By Applications | Changes in material availability impacts with the production planning. |

| Environmental Compliance Costs | By Applications | Adds to total regulatory and operating expenditures. |

Canada Carbon Market Challenges

The Canada Carbon Market comes across myriad of issues like hefty production expenses, complicated manufacturing processes, and irregular supply of raw materials. Besides this, strict environmental rules and compliance requirements add operational complexity for manufacturers. The producers in the market are still struggling to keep their costs reasonable along with high performance and sustainability expectations, especially due to the demand for top-quality and low-emission carbon materials.

Canada Carbon Market Trends

Several key trends are shaping the growth of the Canada Carbon Market:

- Increasing Use of Lightweight Materials: Automotive and aerospace industries are hugely using carbon materials to enhance efficiency and performance.

- Growth in Graphite Demand: Graphite is gaining popularity due to its wide usage in industrial and energy-related applications.

- Expansion of Clean Manufacturing: Carbon materials aiding low-emission production are seeing higher adoption.

- Advanced Engineering Applications: High-performance carbon products are highly used in precision engineering industries.

Investment Opportunities in the Canada Carbon Market

Some notable investment opportunities include:

- Advanced Carbon Manufacturing: Investing in high-performance carbon materials help with industrial development.

- Aerospace Carbon Components: Lightweight and sturdy carbon products generate strong need in aerospace manufacturing.

- Sustainable Material Development: Carbon materials that are aligned with emissions reduction goals present long-term opportunities.

- Engineering Industry Supply: Growing engineering applications drive consistent demand for specialized carbon products.

Top 5 Leading Players in the Canada Carbon Market

Some leading players operating in the Canada Carbon Market include:

1. GrafTech Canada Ltd.

| Company Name | GrafTech Canada Ltd. |

| Established Year | 1886 |

| Headquarters | Toronto, Canada |

| Official Website | Click Here |

GrafTech specializes in high-performance graphite materials for industrial and engineering applications.

2. SGL Carbon Canada

| Company Name | SGL Carbon Canada |

| Established Year | 1992 |

| Headquarters | Ontario, Canada |

| Official Website | Click Here |

SGL Carbon provides advanced carbon-based solutions for automotive, aerospace, and industrial sectors.

3. Tokai Carbon Canada

| Company Name | Tokai Carbon Canada |

| Established Year | 1918 |

| Headquarters | Quebec, Canada |

| Official Website | Click Here |

Tokai Carbon manufactures carbon and graphite products supporting engineering and construction applications.

4. Mersen Canada

| Company Name | Mersen Canada |

| Established Year | 1892 |

| Headquarters | Montreal, Canada |

| Official Website | Click Here |

Mersen offers carbon-based materials and electrical solutions for industrial and energy markets.

5. Element Six Canada

| Company Name | Element Six Canada |

| Established Year | 1946 |

| Headquarters | Ontario, Canada |

| Official Website | Click Here |

Element Six focuses on synthetic diamond solutions for advanced engineering and industrial applications.

Government Regulations Introduced in the Canada Carbon Market

According to Canadian government data, initiatives such as the Clean Technology Investment Program, Net-Zero Manufacturing Strategy, and Advanced Materials Innovation Fund are aiding market growth. Government measures which include of funding for low-emission material research, incentives for clean manufacturing, support for advanced carbon material development, and policies promoting sustainable industrial production. Additionally, grants for research institutions and partnerships with private players are encouraging innovation and commercialization of advanced carbon technologies.

Future Insights of the Canada Carbon Market

The Canada Carbon Market Share is anticipated to grow s firmly due to the surging demand from automotive, construction, aerospace, and engineering industries. Government emphasis on clean manufacturing and emissions reduction will further strengthen market development. Rising incorporation of advanced, lightweight, and high-performance carbon materials will continue to shape market growth in the coming years. Increasing investments in research and development and wider use of carbon materials in emerging industrial applications will further support long-term expansion.

Market Segmentation Analysis

The report offers a comprehensive study of the following market segments and their leading categories:

By Product Type – Graphite to Lead the Market

According to Rashika, Senior Research Analyst at 6Wresearch, Graphite dominates the Canada Carbon Market due to its extensive use in industrial manufacturing, construction applications, and engineering industries.

By Application – Automotive to Lead the Market

Automotive applications dominate the market driven by increasing demand for lightweight materials, improved fuel efficiency, and enhanced vehicle performance. Rising adoption of carbon-based components in electric and hybrid vehicles is further strengthening demand in this segment.

Key Attractiveness of the Report

- 10 Years of Market Numbers

- Historical Data Starting from 2022 to 2025

- Base Year: 2025

- Forecast Data until 2032

- Key Performance Indicators Impacting the Market

- Major Upcoming Developments and Projects

Key Highlights of the Report:

- Canada Carbon Market Outlook

- Market Size of Canada Carbon Market, 2025

- Forecast of Canada Carbon Market, 2032

- Historical Data and Forecast of Canada Carbon Revenues & Volume for the Period 2022-2032

- Canada Carbon Market Trend Evolution

- Canada Carbon Market Drivers and Challenges

- Canada Carbon Price Trends

- Canada Carbon Porter`s Five Forces

- Canada Carbon Industry Life Cycle

- Historical Data and Forecast of Canada Carbon Market Revenues & Volume By Product Types for the Period 2022-2032

- Historical Data and Forecast of Canada Carbon Market Revenues & Volume By Amorphous Carbon for the Period 2022-2032

- Historical Data and Forecast of Canada Carbon Market Revenues & Volume By Graphite for the Period 2022-2032

- Historical Data and Forecast of Canada Carbon Market Revenues & Volume By Diamond for the Period 2022-2032

- Historical Data and Forecast of Canada Carbon Market Revenues & Volume By Applications for the Period 2022-2032

- Historical Data and Forecast of Canada Carbon Market Revenues & Volume By Automotive for the Period 2022-2032

- Historical Data and Forecast of Canada Carbon Market Revenues & Volume By Construction for the Period 2022-2032

- Historical Data and Forecast of Canada Carbon Market Revenues & Volume By Engineering Industries for the Period 2022-2032

- Historical Data and Forecast of Canada Carbon Market Revenues & Volume By Aerospace for the Period 2022-2032

- Historical Data and Forecast of Canada Carbon Market Revenues & Volume By Others for the Period 2022-2032

- Canada Carbon Import Export Trade Statistics

- Market Opportunity Assessment By Product Types

- Market Opportunity Assessment By Applications

- Canada Carbon Top Companies Market Share

- Canada Carbon Competitive Benchmarking By Technical and Operational Parameters

- Canada Carbon Company Profiles

- Canada Carbon Key Strategic Recommendations

Markets Covered

The report offers a comprehensive study of the following market segments:

By Material Type

- Plastic

- Wood

- Metal

- Other

By Application

- Residential

- Commercial

Canada Carbon Market (2026-2032): FAQs

The Canada Carbon Market is projected to grow at a CAGR of 6.1% during the forecast period 2026–2032.

Cost-intensive production, technical manufacturing complexity, and environmental compliance pressures present key hurdles to market development.

Automotive lightweighting, infrastructure development, aerospace expansion, and engineering applications are driving market demand.

Government initiatives promoting clean technology, advanced materials research, and low-emission manufacturing are strengthening market growth.

6Wresearch actively monitors the Canada Carbon Market and publishes its comprehensive annual report, highlighting emerging trends, growth drivers, revenue analysis, and forecast outlook. Our insights help businesses to make data-backed strategic decisions with ongoing market dynamics. Our analysts track relevent industries related to the Canada Carbon Market, allowing our clients with actionable intelligence and reliable forecasts tailored to emerging regional needs.

Yes, we provide customisation as per your requirements. To learn more, feel free to contact us on sales@6wresearch.com

| 1 Executive Summary |

| 2 Introduction |

| 2.1 Key Highlights of the Report |

| 2.2 Report Description |

| 2.3 Market Scope & Segmentation |

| 2.4 Research Methodology |

| 2.5 Assumptions |

| 3 Canada Carbon Market Overview |

| 3.1 Canada Country Macro Economic Indicators |

| 3.2 Canada Carbon Market Revenues & Volume, 2022 & 2032F |

| 3.3 Canada Carbon Market - Industry Life Cycle |

| 3.4 Canada Carbon Market - Porter's Five Forces |

| 3.5 Canada Carbon Market Revenues & Volume Share, By Product Types, 2022 & 2032F |

| 3.6 Canada Carbon Market Revenues & Volume Share, By Applications, 2022 & 2032F |

| 4 Canada Carbon Market Dynamics |

| 4.1 Impact Analysis |

| 4.2 Market Drivers |

| 4.2.1 Increasing awareness and adoption of clean energy solutions in Canada |

| 4.2.2 Government regulations promoting carbon emission reduction initiatives |

| 4.2.3 Growing demand for sustainable practices and products in various industries |

| 4.3 Market Restraints |

| 4.3.1 Fluctuating carbon prices in the market |

| 4.3.2 Volatility in global energy markets impacting carbon trading activities |

| 4.3.3 Lack of standardized carbon pricing mechanisms and policies |

| 5 Canada Carbon Market Trends |

| 6 Canada Carbon Market Segmentations |

| 6.1 Canada Carbon Market, By Product Types |

| 6.1.1 Overview and Analysis |

| 6.1.2 Canada Carbon Market Revenues & Volume, By Amorphous Carbon, 2022-2032F |

| 6.1.3 Canada Carbon Market Revenues & Volume, By Graphite, 2022-2032F |

| 6.1.4 Canada Carbon Market Revenues & Volume, By Diamond, 2022-2032F |

| 6.2 Canada Carbon Market, By Applications |

| 6.2.1 Overview and Analysis |

| 6.2.2 Canada Carbon Market Revenues & Volume, By Automotive, 2022-2032F |

| 6.2.3 Canada Carbon Market Revenues & Volume, By Construction, 2022-2032F |

| 6.2.4 Canada Carbon Market Revenues & Volume, By Engineering Industries, 2022-2032F |

| 6.2.5 Canada Carbon Market Revenues & Volume, By Aerospace, 2022-2032F |

| 6.2.6 Canada Carbon Market Revenues & Volume, By Others, 2022-2032F |

| 7 Canada Carbon Market Import-Export Trade Statistics |

| 7.1 Canada Carbon Market Export to Major Countries |

| 7.2 Canada Carbon Market Imports from Major Countries |

| 8 Canada Carbon Market Key Performance Indicators |

| 8.1 Renewable energy capacity additions in Canada |

| 8.2 Number of carbon offset projects registered in the market |

| 8.3 Carbon intensity reduction targets achieved by key industries |

| 8.4 Compliance rate with carbon pricing regulations |

| 8.5 Investment inflow in carbon capture and storage technologies |

| 9 Canada Carbon Market - Opportunity Assessment |

| 9.1 Canada Carbon Market Opportunity Assessment, By Product Types, 2022 & 2032F |

| 9.2 Canada Carbon Market Opportunity Assessment, By Applications, 2022 & 2032F |

| 10 Canada Carbon Market - Competitive Landscape |

| 10.1 Canada Carbon Market Revenue Share, By Companies, 2022-2032F |

| 10.2 Canada Carbon Market Competitive Benchmarking, By Operating and Technical Parameters |

| 11 Company Profiles |

| 12 Recommendations |

| 13 Disclaimer |

Global Go To Market Strategy - 2030

Export potential enables firms to identify high-growth global markets with greater confidence by combining advanced trade intelligence with a structured quantitative methodology. The framework analyzes emerging demand trends and country-level import patterns while integrating macroeconomic and trade datasets such as GDP and population forecasts, bilateral import–export flows, tariff structures, elasticity differentials between developed and developing economies, geographic distance, and import demand projections. Using weighted trade values from 2020–2024 as the base period to project country-to-country export potential for 2030, these inputs are operationalized through calculated drivers such as gravity model parameters, tariff impact factors, and projected GDP per-capita growth. Through an analysis of hidden potentials, demand hotspots, and market conditions that are most favorable to success, this method enables firms to focus on target countries, maximize returns, and global expansion with data, backed by accuracy.

By factoring in the projected importer demand gap that is currently unmet and could be potential opportunity, it identifies the potential for the Exporter (Country) among 190 countries, against the general trade analysis, which identifies the biggest importer or exporter.

To discover high-growth global markets and optimize your business strategy:

Click Here

Pricing

- Single User License$ 1,995

- Department License$ 2,400

- Site License$ 3,120

- Global License$ 3,795

Leadership Perspectives from Industry Events

Search

Thought Leadership and Analyst Meet

Our Clients

6WResearch In News

- Doha a strategic location for EV manufacturing hub: IPA Qatar

- Demand for luxury TVs surging in the GCC, says Samsung

- Empowering Growth: The Thriving Journey of Bangladesh’s Cable Industry

- Demand for luxury TVs surging in the GCC, says Samsung

- Video call with a traditional healer? Once unthinkable, it’s now common in South Africa

- Intelligent Buildings To Smooth GCC’s Path To Net Zero

Latest Reports

- Taiwan Airport Wireless Infrastructure Market (2026-2032)

- Vietnam Airport Wireless Infrastructure Market (2026-2032)

- Thailand Airport Wireless Infrastructure Market (2026-2032)

- South Korea Airport Wireless Infrastructure Market (2026-2032)

- Romania Airport Wireless Infrastructure Market (2026-2032)

- Qatar Airport Wireless Infrastructure Market (2026-2032)

- Philippines Airport Wireless Infrastructure Market (2026-2032)

- Japan Airport Wireless Infrastructure Market (2026-2032)

- Taiwan Airport Winter Services Market (2026-2032)

- Vietnam Airport Winter Services Market (2026-2032)

Industry Events and Analyst Meet

HIMTEX 2026

India Refining Summit 2026

India EV Show 2026

EV tech India Expo 2026

Auto Tech Asia 2026

Whitepaper

- Middle East & Africa Commercial Security Market Click here to view more.

- Middle East & Africa Fire Safety Systems & Equipment Market Click here to view more.

- GCC Drone Market Click here to view more.

- Middle East Lighting Fixture Market Click here to view more.

- GCC Physical & Perimeter Security Market Click here to view more.