China Cheese Market (2025 - 2029) | Companies, Outlook, Forecast, Share, Value, Industry, Revenue, Growth, Size, Trends & Analysis

Market Forecast By Type (Natural, Processed), By Product (Mozzarella, Cheddar, Feta, Parmesan, Roquefort, Others), By Source (Cow Milk, Sheep Milk, Goat Milk, Buffalo), By Distribution Channel (Hypermarkets, Supermarkets, Food Specialty Stores, Convenience Stores, Others) And Competitive Landscape

| Product Code: ETC180280 | Publication Date: Jan 2022 | Updated Date: Oct 2025 | Product Type: Market Research Report | |

| Publisher: 6Wresearch | Author: Dhaval Chaurasia | No. of Pages: 70 | No. of Figures: 35 | No. of Tables: 5 |

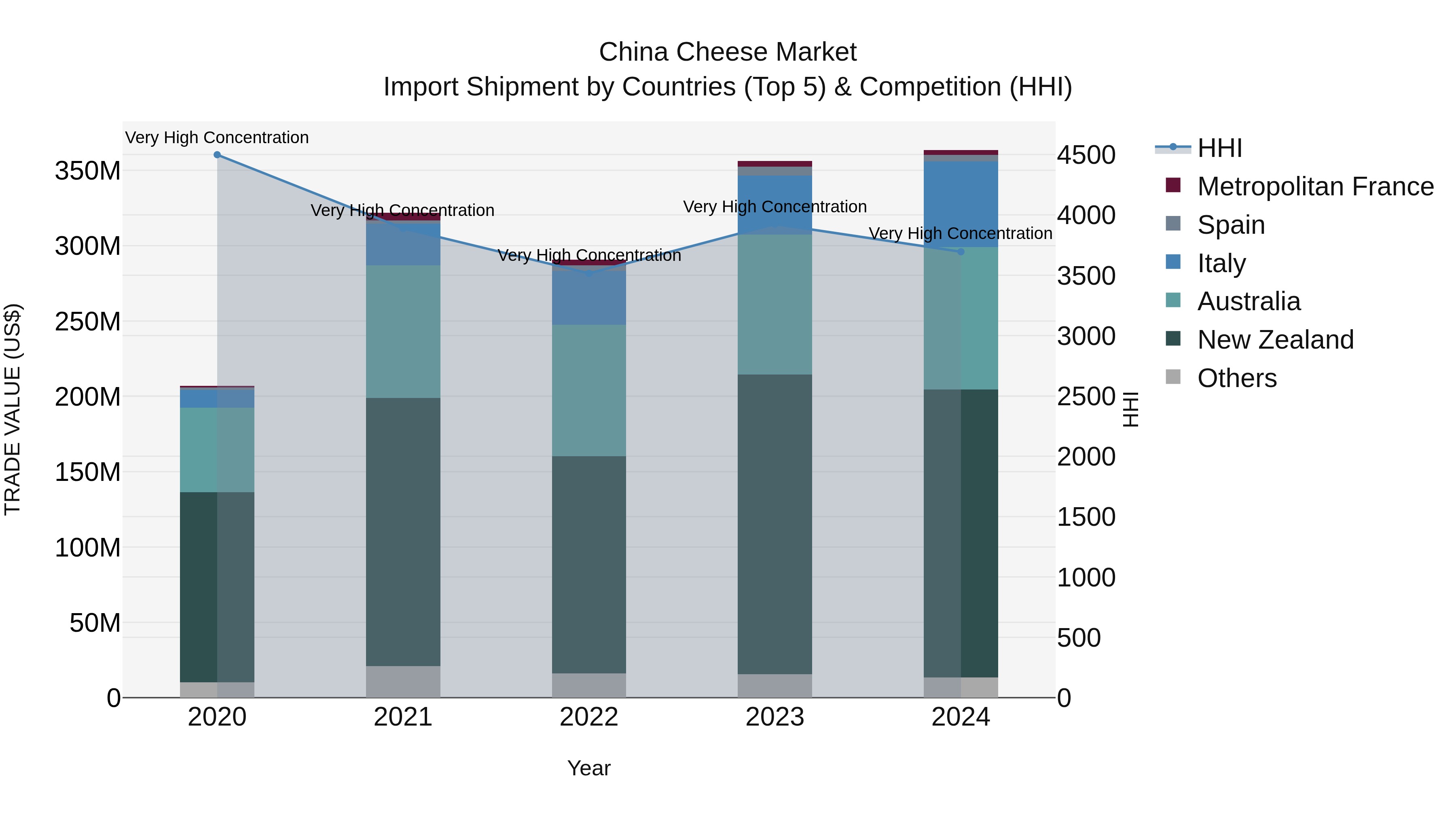

China Cheese Market Top 5 Importing Countries and Market Competition (HHI) Analysis

China cheese import market continued to witness strong growth in 2024, with top exporting countries like New Zealand, Australia, Italy, Spain, and Metropolitan France dominating the scene. The high Herfindahl-Hirschman Index (HHI) indicates a concentrated market, while the impressive compound annual growth rate (CAGR) of 15.12% from 2020 to 2024 underscores the increasing demand for cheese in China. Despite a slightly lower growth rate in 2024 at 2.01%, the market remains promising for cheese exporters looking to tap into China growing appetite for dairy products.

China Cheese Market Highlights

| Report Name | China Cheese Market |

| Forecast period | 2025-2029 |

| CAGR | 7.59% |

| Growing Sector | Processed Cheese |

Topics Covered in the China Cheese Market Report

The China Cheese Market report thoroughly covers the market by type, product, source, and distribution channels. It delivers an unbiased and comprehensive analysis of ongoing trends, investment opportunities, and market drivers. This helps stakeholders formulate strategies based on current and anticipated market dynamics, emphasizing demand patterns, supply chain challenges, and evolving consumer preferences in cheese consumption.

China Cheese Market Synopsis

China Cheese Market is expected to grow significantly owing to rising westernized diets, increased dairy consumption, and expanding foodservice sectors. Additionally, heightened awareness of cheese’s nutritional benefits along with innovations in flavor and packaging drives demand. The market gains from rising urban disposable incomes, fast retail growth, and growing cold-chain infrastructure investments, which together support the expansion of diverse cheese products through retail and institutional channels.

China Cheese Market is expected to grow at a compound annual growth rate (CAGR) of 7.59% during the forecast period of 2025-2029. Growth is fueled by the expansion of quick-service restaurants and bakery sectors incorporating cheese products. Increasing consumer experimentation with international cuisines and the growing availability of imported cheese varieties contribute significantly. Furthermore, government programs promoting modernization of the dairy sector and investments in cold storage and distribution infrastructure aid market growth in metropolitan and emerging cities.

China Cheese Market Challenges

The market confronts issues such as high import duties on foreign cheese, inconsistent local raw milk supply, and variable raw material costs. Cultural preferences for traditional dairy products and limited consumer awareness of specialty cheeses slow widespread acceptance. Also, inefficient supply chains and lacking cold-chain infrastructure, especially in rural and lower-tier cities, increase operational costs and constrain market access. These factors collectively limit the growth and reach of specialty cheese products across diverse consumer segments.

China Cheese Market Trends

Key trends in the China Cheese Industry are rising preference for artisanal and organic cheese, growing demand for lactose-free options, and expanded use of cheese in ready-to-eat snacks. Adoption of smart packaging and blockchain improves supply chain transparency. International cheese brands collaborate with local retailers to increase accessibility, while nutrition awareness efforts inform consumers about cheese benefits, supporting the expanding interest in diverse cheese products across urban markets.

Investment Opportunities in the China Cheese Industry

There are significant investment prospects in improving cold-chain logistics, setting up cheese processing units in major dairy regions, and creating flavors tailored to local tastes. Startups offering organic, low-fat, and specialty cheeses are attracting venture capital interest. Government initiatives like the National Dairy Industry Development Plan support innovation and modernization. This creates a favorable ecosystem for new entrants and tech-driven growth in both urban and emerging rural cheese markets across China.

Leading Players of the China Cheese Market

The China Cheese Market Share features key players like Mengniu Dairy, Yili Group, Arla Foods, and Fonterra. These companies focus on expanding product portfolios with premium and processed cheese options and strengthening distribution via hypermarkets and convenience stores. Local artisanal producers and international importers also compete by offering niche and gourmet cheese varieties to cater to evolving consumer preferences.

Government Regulations Introduced in the China Cheese Market

According to Chinese government data, measures such as the Dairy Industry Development Plan and enhanced food safety standards under the Food Safety Law stress traceability and quality assurance. Adjustments to dairy import tariffs aim to balance domestic production and global trade. Additionally, subsidies for cold-chain infrastructure and tech upgrades help boost product safety and reliability. These regulatory changes collectively build consumer trust while encouraging modernization and competitiveness in China’s expanding cheese industry.

Future Insights of the China Cheese Market

The future of China cheese market will be influenced by AI for analyzing consumer behavior, blockchain for supply chain transparency, and advanced dairy farming technologies. Plant-based and fortified cheese products are predicted to see growing demand. Market expansion into tier-3 and rural areas will gain pace with ongoing infrastructure development. Additionally, the growing impact of e-commerce and app-based grocery platforms will improve accessibility and drive convenient, on-demand cheese consumption across demographics.

Market Segmentation Analysis

Processed Cheese to Dominate the Market - By Type

According to Guneet Kaur, Senior Research Analyst, 6Wresearch dominates the China Cheese Market due to its longer shelf life, affordability, and versatility in cooking and foodservice applications. Consumers prefer processed cheese for sandwiches, snacks, and fast foods, contributing to its widespread adoption. Natural cheese is growing steadily but still trails processed varieties, primarily in urban areas and premium segments, driven by rising health consciousness and demand for authentic cheese flavors.

Mozzarella to Dominate the Market - By Product

Mozzarella holds the largest share within the China Cheese Market, favored by its use in pizzas, pasta, and bakery items. Cheddar follows closely due to its popularity in sandwiches and ready-to-eat meals. Specialty cheeses such as Feta and Parmesan are gradually gaining recognition, driven by western food trends and increased fine dining options in metropolitan regions, while Roquefort and other blue cheeses remain niche.

Cow Milk Cheese to Dominate the Market - By Source

Cow milk cheese dominates due to China’s extensive dairy farming and consumer familiarity. Sheep and goat milk cheeses are niche but growing in health-conscious urban consumers seeking alternative dairy sources. Buffalo milk cheese is still limited, primarily used in specialty products. Increasing investment in dairy farming techniques aims to improve milk quality and diversify cheese production, enhancing source variety in the coming years.

Hypermarkets to Dominate the Market - By Distribution Channel

Hypermarkets dominate the distribution of cheese products in China, offering wide product variety and competitive pricing. Supermarkets also hold significant share, especially in tier-1 and tier-2 cities. Food specialty stores cater to premium and imported cheeses, attracting niche consumers. Convenience stores are growing due to urban lifestyle changes, providing easy access to processed cheese snacks, while e-commerce channels continue to expand rapidly.

Key Attractiveness of the Report

- 10 Years of Market Numbers

- Historical Data Starting from 2021 to 2024

- Base Year: 2024

- Forecast Data until 2029

- Key Performance Indicators Impacting the Market

- Major Upcoming Developments and Projects

Key Highlights of the Report:

- China Cheese Market Outlook

- Market Size of China Cheese Market, 2024

- Forecast of China Cheese Market, 2029

- Historical Data and Forecast of China Cheese Revenues & Volume for the Period 2019-2029

- China Cheese Market Trend Evolution

- China Cheese Market Drivers and Challenges

- China Cheese Price Trends

- China Cheese Porter's Five Forces

- China Cheese Industry Life Cycle

- Historical Data and Forecast of China Cheese Market Revenues & Volume By Type for the Period 2019-2029

- Historical Data and Forecast of China Cheese Market Revenues & Volume By Natural for the Period 2019-2029

- Historical Data and Forecast of China Cheese Market Revenues & Volume By Processed for the Period 2019-2029

- Historical Data and Forecast of China Cheese Market Revenues & Volume By Product for the Period 2019-2029

- Historical Data and Forecast of China Cheese Market Revenues & Volume By Mozzarella for the Period 2019-2029

- Historical Data and Forecast of China Cheese Market Revenues & Volume By Cheddar for the Period 2019-2029

- Historical Data and Forecast of China Cheese Market Revenues & Volume By Feta for the Period 2019-2029

- Historical Data and Forecast of China Cheese Market Revenues & Volume By Parmesan for the Period 2019-2029

- Historical Data and Forecast of China Cheese Market Revenues & Volume By Roquefort for the Period 2019-2029

- Historical Data and Forecast of China Cheese Market Revenues & Volume By Others for the Period 2019-2029

- Historical Data and Forecast of China Cheese Market Revenues & Volume By Source for the Period 2019-2029

- Historical Data and Forecast of China Cheese Market Revenues & Volume By Cow Milk for the Period 2019-2029

- Historical Data and Forecast of China Cheese Market Revenues & Volume By Sheep Milk for the Period 2019-2029

- Historical Data and Forecast of China Cheese Market Revenues & Volume By Goat Milk for the Period 2019-2029

- Historical Data and Forecast of China Cheese Market Revenues & Volume By Buffalo for the Period 2019-2029

- Historical Data and Forecast of China Cheese Market Revenues & Volume By Distribution Channel for the Period 2019-2029

- Historical Data and Forecast of China Cheese Market Revenues & Volume By Hypermarkets for the Period 2019-2029

- Historical Data and Forecast of China Cheese Market Revenues & Volume By Supermarkets for the Period 2019-2029

- Historical Data and Forecast of China Cheese Market Revenues & Volume By Food Specialty Stores for the Period 2019-2029

- Historical Data and Forecast of China Cheese Market Revenues & Volume By Convenience Stores for the Period 2019-2029

- Historical Data and Forecast of China Cheese Market Revenues & Volume By Others for the Period 2019-2029

- China Cheese Import Export Trade Statistics

- Market Opportunity Assessment By Type

- Market Opportunity Assessment By Product

- Market Opportunity Assessment By Source

- Market Opportunity Assessment By Distribution Channel

- China Cheese Top Companies Market Share

- China Cheese Competitive Benchmarking By Technical and Operational Parameters

- China Cheese Company Profiles

- China Cheese Key Strategic Recommendations

Market Covered

The market report provides a detailed analysis of the following market segments:

By Type

- Natural

- Processed

By Product

- Mozzarella

- Cheddar

- Feta

- Parmesan

- Roquefort

- Others

By Source

- Cow Milk

- Sheep Milk

- Goat Milk

- Buffalo

By Distribution Channel

- Hypermarkets

- Supermarkets

- Food Specialty Stores

- Convenience Stores

- Others

China Cheese Market (2025 - 2029) : FAQ's

China Cheese Market is projected to grow at a CAGR of approximately 7.59% during the forecast period.

Key growth factors include rising western dietary adoption, urbanization, expansion of the foodservice sector, and increased dairy product awareness.

Key trends include rising demand for artisanal and organic cheeses, lactose-free options, smart packaging, and collaborations between global brands and local retailers.

Challenges include high import duties, inconsistent local milk supply, cultural preference for traditional dairy, supply chain inefficiencies, and limited cold-chain infrastructure in rural areas.

6Wresearch actively monitors the China Cheese Market and publishes its comprehensive annual report, highlighting emerging trends, growth drivers, revenue analysis, and forecast outlook. Our insights help businesses to make data-backed strategic decisions with ongoing market dynamics. Our analysts track relevent industries related to the China Cheese Market, allowing our clients with actionable intelligence and reliable forecasts tailored to emerging regional needs.

Yes, we provide customisation as per your requirements. To learn more, feel free to contact us on sales@6wresearch.com

| 1 Executive Summary |

| 2 Introduction |

| 2.1 Key Highlights of the Report |

| 2.2 Report Description |

| 2.3 Market Scope & Segmentation |

| 2.4 Research Methodology |

| 2.5 Assumptions |

| 3 China Cheese Market Overview |

| 3.1 China Country Macro Economic Indicators |

| 3.2 China Cheese Market Revenues & Volume, 2019 & 2029F |

| 3.3 China Cheese Market - Industry Life Cycle |

| 3.4 China Cheese Market - Porter's Five Forces |

| 3.5 China Cheese Market Revenues & Volume Share, By Type, 2019 & 2029F |

| 3.6 China Cheese Market Revenues & Volume Share, By Product, 2019 & 2029F |

| 3.7 China Cheese Market Revenues & Volume Share, By Source, 2019 & 2029F |

| 3.8 China Cheese Market Revenues & Volume Share, By Distribution Channel, 2019 & 2029F |

| 4 China Cheese Market Dynamics |

| 4.1 Impact Analysis |

| 4.2 Market Drivers |

| 4.2.1 Increasing disposable income and changing dietary habits leading to higher cheese consumption |

| 4.2.2 Growth in the foodservice industry and demand for cheese-based dishes |

| 4.2.3 Rising health consciousness and preference for protein-rich foods driving cheese consumption |

| 4.3 Market Restraints |

| 4.3.1 High import tariffs and limited domestic cheese production affecting market growth |

| 4.3.2 Cultural preferences for traditional Chinese foods over cheese products |

| 4.3.3 Lack of awareness and familiarity with cheese in certain regions of China |

| 5 China Cheese Market Trends |

| 6 China Cheese Market, By Types |

| 6.1 China Cheese Market, By Type |

| 6.1.1 Overview and Analysis |

| 6.1.2 China Cheese Market Revenues & Volume, By Type, 2019 - 2029F |

| 6.1.3 China Cheese Market Revenues & Volume, By Natural, 2019 - 2029F |

| 6.1.4 China Cheese Market Revenues & Volume, By Processed, 2019 - 2029F |

| 6.2 China Cheese Market, By Product |

| 6.2.1 Overview and Analysis |

| 6.2.2 China Cheese Market Revenues & Volume, By Mozzarella, 2019 - 2029F |

| 6.2.3 China Cheese Market Revenues & Volume, By Cheddar, 2019 - 2029F |

| 6.2.4 China Cheese Market Revenues & Volume, By Feta, 2019 - 2029F |

| 6.2.5 China Cheese Market Revenues & Volume, By Parmesan, 2019 - 2029F |

| 6.2.6 China Cheese Market Revenues & Volume, By Roquefort, 2019 - 2029F |

| 6.2.7 China Cheese Market Revenues & Volume, By Others, 2019 - 2029F |

| 6.3 China Cheese Market, By Source |

| 6.3.1 Overview and Analysis |

| 6.3.2 China Cheese Market Revenues & Volume, By Cow Milk, 2019 - 2029F |

| 6.3.3 China Cheese Market Revenues & Volume, By Sheep Milk, 2019 - 2029F |

| 6.3.4 China Cheese Market Revenues & Volume, By Goat Milk, 2019 - 2029F |

| 6.3.5 China Cheese Market Revenues & Volume, By Buffalo, 2019 - 2029F |

| 6.4 China Cheese Market, By Distribution Channel |

| 6.4.1 Overview and Analysis |

| 6.4.2 China Cheese Market Revenues & Volume, By Hypermarkets, 2019 - 2029F |

| 6.4.3 China Cheese Market Revenues & Volume, By Supermarkets, 2019 - 2029F |

| 6.4.4 China Cheese Market Revenues & Volume, By Food Specialty Stores, 2019 - 2029F |

| 6.4.5 China Cheese Market Revenues & Volume, By Convenience Stores, 2019 - 2029F |

| 6.4.6 China Cheese Market Revenues & Volume, By Others, 2019 - 2029F |

| 7 China Cheese Market Import-Export Trade Statistics |

| 7.1 China Cheese Market Export to Major Countries |

| 7.2 China Cheese Market Imports from Major Countries |

| 8 China Cheese Market Key Performance Indicators |

| 8.1 Average cheese consumption per capita |

| 8.2 Number of new cheese product launches in the Chinese market |

| 8.3 Percentage increase in cheese imports from key supplying countries |

| 9 China Cheese Market - Opportunity Assessment |

| 9.1 China Cheese Market Opportunity Assessment, By Type, 2019 & 2029F |

| 9.2 China Cheese Market Opportunity Assessment, By Product, 2019 & 2029F |

| 9.3 China Cheese Market Opportunity Assessment, By Source, 2019 & 2029F |

| 9.4 China Cheese Market Opportunity Assessment, By Distribution Channel, 2019 & 2029F |

| 10 China Cheese Market - Competitive Landscape |

| 10.1 China Cheese Market Revenue Share, By Companies, 2024 |

| 10.2 China Cheese Market Competitive Benchmarking, By Operating and Technical Parameters |

| 11 Company Profiles |

| 12 Recommendations |

| 13 Disclaimer |

Export potential assessment - trade Analytics for 2030

Export potential enables firms to identify high-growth global markets with greater confidence by combining advanced trade intelligence with a structured quantitative methodology. The framework analyzes emerging demand trends and country-level import patterns while integrating macroeconomic and trade datasets such as GDP and population forecasts, bilateral import–export flows, tariff structures, elasticity differentials between developed and developing economies, geographic distance, and import demand projections. Using weighted trade values from 2020–2024 as the base period to project country-to-country export potential for 2030, these inputs are operationalized through calculated drivers such as gravity model parameters, tariff impact factors, and projected GDP per-capita growth. Through an analysis of hidden potentials, demand hotspots, and market conditions that are most favorable to success, this method enables firms to focus on target countries, maximize returns, and global expansion with data, backed by accuracy.

By factoring in the projected importer demand gap that is currently unmet and could be potential opportunity, it identifies the potential for the Exporter (Country) among 190 countries, against the general trade analysis, which identifies the biggest importer or exporter.

To discover high-growth global markets and optimize your business strategy:

Click Here

Pricing

- Single User License$ 1,995

- Department License$ 2,400

- Site License$ 3,120

- Global License$ 3,795

Search

Thought Leadership and Analyst Meet

Our Clients

Latest Reports

- France Thermally Conductive Filler Dispersants Market (2026-2032) | Challenges, Restraints, Value, Share, Size, segmentation, Analysis, Trends, Investment Opportunities, Outlook, Pricing, Demand, Forecast, Revenue, Companies, Growth, Drivers, Strategy, Insights, Competition

- Egypt Thermally Conductive Filler Dispersants Market (2026-2032) | Competition, Forecast, Strategy, Value, Insights, Outlook, Investment Opportunities, Pricing, Demand, Share, segmentation, Drivers, Size, Companies, Restraints, Growth, Trends, Revenue, Challenges, Analysis

- Czech Republic Thermally Conductive Filler Dispersants Market (2026-2032) | Forecast, Pricing, Analysis, Drivers, Insights, Size, Demand, Growth, Challenges, segmentation, Competition, Outlook, Trends, Investment Opportunities, Companies, Strategy, Revenue, Share, Value, Restraints

- Colombia Thermally Conductive Filler Dispersants Market (2026-2032) | segmentation, Trends, Share, Drivers, Strategy, Companies, Demand, Insights, Size, Challenges, Value, Competition, Analysis, Growth, Revenue, Restraints, Forecast, Pricing, Outlook, Investment Opportunities

- China Thermally Conductive Filler Dispersants Market (2026-2032) | Restraints, Investment Opportunities, Pricing, Companies, Share, Size, Challenges, Trends, Outlook, Value, Analysis, Competition, Revenue, Drivers, Forecast, Demand, Insights, Growth, Strategy, segmentation

- Chile Thermally Conductive Filler Dispersants Market (2026-2032) | Investment Opportunities, Trends, Value, Restraints, Share, Companies, Forecast, segmentation, Pricing, Challenges, Demand, Size, Analysis, Drivers, Outlook, Growth, Competition, Strategy, Revenue, Insights

- Cambodia Thermally Conductive Filler Dispersants Market (2026-2032) | Analysis, Share, Outlook, Strategy, Pricing, Demand, Size, Growth, segmentation, Insights, Revenue, Forecast, Challenges, Competition, Companies, Investment Opportunities, Trends, Restraints, Value, Drivers

- Brazil Thermally Conductive Filler Dispersants Market (2026-2032) | Restraints, Forecast, Competition, Size, Revenue, Value, Investment Opportunities, Trends, Insights, Outlook, Growth, Analysis, Drivers, segmentation, Pricing, Challenges, Strategy, Share, Companies, Demand

- Bangladesh Thermally Conductive Filler Dispersants Market (2026-2032) | Restraints, Trends, Analysis, Competition, Insights, Forecast, Value, Investment Opportunities, Pricing, Share, Demand, Outlook, Revenue, segmentation, Companies, Drivers, Growth, Size, Challenges, Strategy

- Bahrain Thermally Conductive Filler Dispersants Market (2026-2032) | Trends, Outlook, Pricing, Demand, Value, Competition, Forecast, Growth, segmentation, Revenue, Companies, Analysis, Insights, Size, Drivers, Challenges, Strategy, Investment Opportunities, Share, Restraints

Industry Events and Analyst Meet

HIMTEX 2026

India Refining Summit 2026

India EV Show 2026

EV tech India Expo 2026

Auto Tech Asia 2026

Whitepaper

- Middle East & Africa Commercial Security Market Click here to view more.

- Middle East & Africa Fire Safety Systems & Equipment Market Click here to view more.

- GCC Drone Market Click here to view more.

- Middle East Lighting Fixture Market Click here to view more.

- GCC Physical & Perimeter Security Market Click here to view more.

6WResearch In News

- Doha a strategic location for EV manufacturing hub: IPA Qatar

- Demand for luxury TVs surging in the GCC, says Samsung

- Empowering Growth: The Thriving Journey of Bangladesh’s Cable Industry

- Demand for luxury TVs surging in the GCC, says Samsung

- Video call with a traditional healer? Once unthinkable, it’s now common in South Africa

- Intelligent Buildings To Smooth GCC’s Path To Net Zero