China Kitchenware Market (2025-2029) | Outlook ,Companies, Analysis, Size, Forecast, Revenue, Trends, Industry, Share, Value & Growth

Market Forecast By Product Type (Cookware, Bakeware, Others), By End User (Residential Kitchen, Commercial Kitchens), By Sales Channel (Online, Offline) And Competitive Landscape

| Product Code: ETC377061 | Publication Date: Aug 2022 | Updated Date: Oct 2025 | Product Type: Market Research Report | |

| Publisher: 6Wresearch | Author: Shubham Padhi | No. of Pages: 75 | No. of Figures: 35 | No. of Tables: 20 |

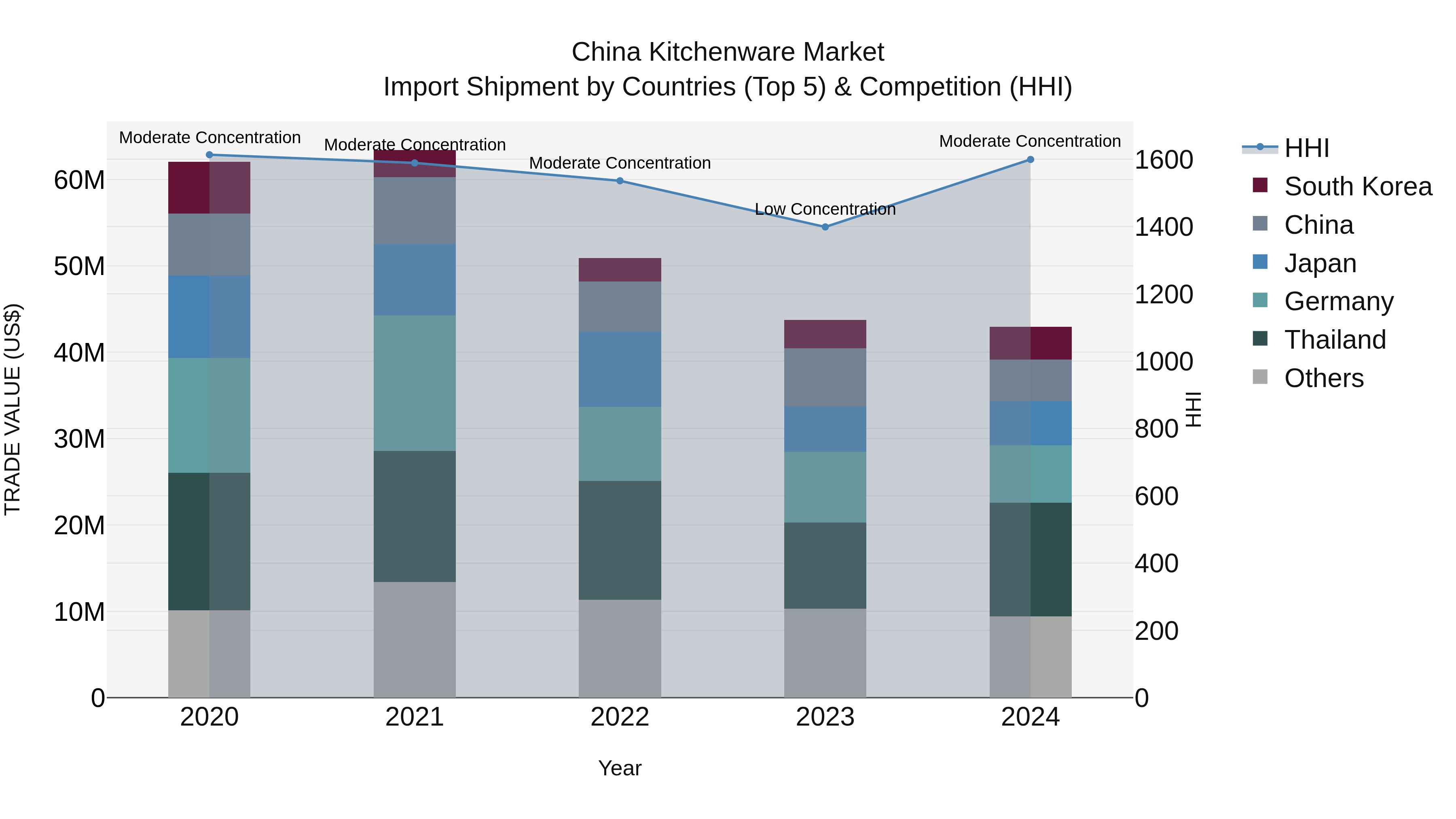

China Kitchenware Market Top 5 Importing Countries and Market Competition (HHI) Analysis

China kitchenware import market saw a shift in concentration levels from low to moderate in 2024, with top exporting countries being Thailand, Germany, Japan, China, and South Korea. Despite a negative Compound Annual Growth Rate (CAGR) of -8.8% from 2020 to 2024, there was a slight improvement in the growth rate from 2023 to 2024, decreasing by -1.86%. This indicates a challenging market environment, possibly influenced by various factors such as changing consumer preferences, economic conditions, and global trade dynamics impacting the kitchenware industry.

China Kitchenware Market Highlights

| Report Name | China Kitchenware Market |

| Forecast period | 2025-2029 |

| CAGR | 6.18% |

| Growing Sector | Residential |

Topics Covered in the China Kitchenware Market Report

The China Kitchenware Market report thoroughly covers the market by product type, end user, and sales channel. The report provides an unbiased and detailed analysis of the ongoing market trends, opportunities, growth areas, and market drivers to help stakeholders align their strategies with current and future market dynamics.

China Kitchenware Market Synopsis

The China kitchenware market is consistently progressing, driven by the shifting consumer lifestyles, increasing urbanization, and growing interest in home cooking. The increasing population of middle-income consumers and transition to modern retail formats are accelerating the demand for quality kitchenware. Domestic and global brands are competing by providing a varied range of products, including bakeware, cookware, and kitchen tools, attracting both modern and traditional users in semi-urban and urban areas.

The China Kitchenware Market is anticipated to grow at a CAGR of 6.18% during the forecast period 2025-2029. Major factors driving the China kitchenware market include the rising home ownership, increasing disposable income, and diversifying modern retail infrastructure. The rising attractiveness of culinary culture, driven by social media and cooking shows, has fueled household spending on functional and stylish kitchen equipment. Furthermore, an expanding e-commerce ecosystem has enhanced accessibility, allowing buyers to explore different products, brands, and designs from the comfort of their homes, which further supports China kitchenware market growth.

China Kitchenware Market Challenges

The China imitation jewelry market encounters several obstacles that hinder its growth. Major challenges include restrained access to high-quality materials for domestic producers. The dominance of low-cost imported commodities is also a key hurdle that interferes with market growth. Market revenue is impacted by volatile raw material prices. Informal sector competition often leads to pricing pressures for established brands. In addition, consumer choice for long-lasting products causes slower replacement cycles. Supply chain disruptions, particularly during global economic fluctuations, also act as barriers to maintaining steady product availability nationwide.

China Kitchenware Market Trends

Significant trends in the China kitchenware industry include rising consumer preference for non-toxic, environmentally friendly, and sustainable kitchenware. There’s a growing demand for space-saving and multifunctional tools, particularly in urban households with a lack of space. Minimalist, sleek designs and colorful cookware are appealing to the younger population. Technological integration, such as non-stick advancements and induction compatibility, is further influencing product development. Furthermore, digital platforms are shaping purchasing behavior, with online product demonstrations and reviews steering customer preferences.

Investment Opportunities in the China Kitchenware Market

There are plenty of prospects for investment in premium kitchenware, especially aiming at millennial and urban middle-class consumers. Expansion of offline and online retail channels provides opportunities for market entrance. Domestic production partnerships can help reduce import reliance and promote cost-effective production. Advancements in eco-friendly and smart kitchen tools provide niche markets for new entrants. Companies emphasizing durability, modern aesthetics, and value-added features are well-positioned to succeed in this developing ecosystem.

Leading Players in the China Kitchenware Market

Both local and international firms lead the market. Prominent local firms that dominate the market include Joyoung, Supor, Midea, Zwilling J.A. Henckels, and Supor Cookware. Leading global brands include Tefal and Philips. Market share of local players is on the rise due to competitively priced, durable, and innovative cookware adjusted according to regional cooking styles, while international brands dominate the premium and luxury product segments.

Government Regulations in the China Kitchenware Market

The kitchenware market is subject to quality and safety standards that ensure consumer protection. Regulations cover material safety, particularly for items in contact with food, and environmental guidelines for waste management. The government encourages domestic production through various industrial incentives. Import regulations, labeling requirements, and health certifications are enforced to ensure product compliance. These regulatory frameworks help maintain industry standards and foster responsible market practices.

Future Insights of the China Kitchenware Market

The future of the China kitchenware market seems promising. With growing consumer preference for lifestyle-driven kitchen solutions, the industry is expected to grow vigorously. The implementation of smart technologies, increasing awareness of sustainable lifestyles, and developing consumer tastes will redefine the industry. More households will prefer modern kitchen upgrades, and the potential for advancement and brand differentiation will develop with increasing urbanization. Brands that support sustainability, health, and convenience trends are well-positioned to gain a competitive edge.

Market Segmentation Analysis

The report offers a comprehensive study of the subsequent market segments and their leading categories.

Cookware to Dominate the Market – By Product Type

Cookware dominates the China Kitchenware Market by product type. This is because Chinese households and restaurants rely heavily on cookware items such as woks, pans, and pots for daily meal preparation. The culture’s emphasis on stir-frying, steaming, and boiling makes cookware indispensable, thereby giving it the largest share compared to bakeware and other categories.

Residential to Dominate the Market – By End User

The Residential Kitchen segment leads the market by end user. With a growing middle-class population, rising disposable incomes, and increasing home ownership, demand for kitchenware products in households has surged. Urbanization and lifestyle changes have also boosted home cooking, especially among younger families, driving higher consumption of residential kitchenware.

Key Attractiveness of the Report

- 10 Years of Market Numbers.

- Historical Data Starting from 2021 to 2024.

- Base Year: 2024

- Forecast Data until 2029.

- Key Performance Indicators Impacting the Market.

- Major Upcoming Developments and Projects.

Key Highlights of the Report:

- China Kitchenware Market Outlook

- Market Size of China Kitchenware Market, 2024

- Forecast of China Kitchenware Market, 2029

- Historical Data and Forecast of China Kitchenware Revenues & Volume for the Period 2019 - 2029

- China Kitchenware Market Trend Evolution

- China Kitchenware Market Drivers and Challenges

- China Kitchenware Price Trends

- China Kitchenware Porter's Five Forces

- China Kitchenware Industry Life Cycle

- Historical Data and Forecast of China Kitchenware Market Revenues & Volume By Product Type for the Period 2019 - 2029

- Historical Data and Forecast of China Kitchenware Market Revenues & Volume By Cookware for the Period 2019 - 2029

- Historical Data and Forecast of China Kitchenware Market Revenues & Volume By Bakeware for the Period 2019 - 2029

- Historical Data and Forecast of China Kitchenware Market Revenues & Volume By Others for the Period 2019 - 2029

- Historical Data and Forecast of China Kitchenware Market Revenues & Volume By End User for the Period 2019 - 2029

- Historical Data and Forecast of China Kitchenware Market Revenues & Volume By Residential Kitchen for the Period 2019 - 2029

- Historical Data and Forecast of China Kitchenware Market Revenues & Volume By Commercial Kitchens for the Period 2019 - 2029

- Historical Data and Forecast of China Kitchenware Market Revenues & Volume By Sales Channel for the Period 2019 - 2029

- Historical Data and Forecast of China Kitchenware Market Revenues & Volume By Online for the Period 2019 - 2029

- Historical Data and Forecast of China Kitchenware Market Revenues & Volume By Offline for the Period 2019 - 2029

- China Kitchenware Import Export Trade Statistics

- Market Opportunity Assessment By Product Type

- Market Opportunity Assessment By End User

- Market Opportunity Assessment By Sales Channel

- China Kitchenware Top Companies Market Share

- China Kitchenware Competitive Benchmarking By Technical and Operational Parameters

- China Kitchenware Company Profiles

- China Kitchenware Key Strategic Recommendations

Markets Covered

The market report provides a detailed analysis of the following market segments:

By Product Type:

- Cookware

- Bakeware

- Others

By End User:

- Residential Kitchen

- Commercial Kitchens

By Sales Channel:

- Online

- Offline

China Kitchenware Market (2025-2029) : FAQ's

The China Kitchenware Market is expected to grow at a CAGR of approximately 6.18% from 2025 to 2029.

Key drivers include rising disposable incomes, modern lifestyle adoption, and government-backed eco-friendly initiatives.

Cookware dominates due to continuous demand from both residential and commercial kitchens.

Challenges include raw material price volatility, counterfeit products in online channels, and pressure for sustainable production.

6Wresearch actively monitors the China Kitchenware Market and publishes its comprehensive annual report, highlighting emerging trends, growth drivers, revenue analysis, and forecast outlook. Our insights help businesses to make data-backed strategic decisions with ongoing market dynamics. Our analysts track relevent industries related to the China Kitchenware Market, allowing our clients with actionable intelligence and reliable forecasts tailored to emerging regional needs.

Yes, we provide customisation as per your requirements. To learn more, feel free to contact us on sales@6wresearch.com

Global Go To Market Strategy - 2030

Export potential enables firms to identify high-growth global markets with greater confidence by combining advanced trade intelligence with a structured quantitative methodology. The framework analyzes emerging demand trends and country-level import patterns while integrating macroeconomic and trade datasets such as GDP and population forecasts, bilateral import–export flows, tariff structures, elasticity differentials between developed and developing economies, geographic distance, and import demand projections. Using weighted trade values from 2020–2024 as the base period to project country-to-country export potential for 2030, these inputs are operationalized through calculated drivers such as gravity model parameters, tariff impact factors, and projected GDP per-capita growth. Through an analysis of hidden potentials, demand hotspots, and market conditions that are most favorable to success, this method enables firms to focus on target countries, maximize returns, and global expansion with data, backed by accuracy.

By factoring in the projected importer demand gap that is currently unmet and could be potential opportunity, it identifies the potential for the Exporter (Country) among 190 countries, against the general trade analysis, which identifies the biggest importer or exporter.

To discover high-growth global markets and optimize your business strategy:

Click Here

Pricing

- Single User License$ 1,995

- Department License$ 2,400

- Site License$ 3,120

- Global License$ 3,795

Leadership Perspectives from Industry Events

Search

Thought Leadership and Analyst Meet

Our Clients

6WResearch In News

- India Export Attractiveness Tracker 2026

- India Air Conditioner Market Set for Strong Rebound in 2026 After Weather-Led Correction and GST-Driven Recovery: 6Wresearch

- ADAS in India: How Automatic Emergency Braking, Blind Spot Detection & Driver Monitoring are Transforming Road Safety

- Doha a strategic location for EV manufacturing hub: IPA Qatar

- Demand for luxury TVs surging in the GCC, says Samsung

- Empowering Growth: The Thriving Journey of Bangladesh’s Cable Industry

Latest Reports

- Nicaragua RPG Gaming Market (2026-2032)

- New Zealand RPG Gaming Market (2026-2032)

- Netherlands RPG Gaming Market (2026-2032)

- Nauru RPG Gaming Market (2026-2032)

- Namibia RPG Gaming Market (2026-2032)

- Mozambique RPG Gaming Market (2026-2032)

- Montenegro RPG Gaming Market (2026-2032)

- Mongolia RPG Gaming Market (2026-2032)

- Monaco RPG Gaming Market (2026-2032)

- Micronesia RPG Gaming Market (2026-2032)

Industry Events and Analyst Meet

EV India Expo 2026

HIMTEX 2026

India Refining Summit 2026

India EV Show 2026

EV tech India Expo 2026

Whitepaper

- Middle East & Africa Commercial Security Market Click here to view more.

- Middle East & Africa Fire Safety Systems & Equipment Market Click here to view more.

- GCC Drone Market Click here to view more.

- Middle East Lighting Fixture Market Click here to view more.

- GCC Physical & Perimeter Security Market Click here to view more.