Europe 5G Services Market (2026-2032) | Trends, Revenue, Analysis, Industry, Companies, Value, Size, Growth, Forecast & Share

Market Forecast by Countries (Germany, United Kingdom, France, Italy, Russia, Spain, Rest of Europe), By End Users (Consumers, Enterprises), By Enterprises (Manufacturing, Energy and Utilities, Media and Entertainment, Government, Transportation and Logistics, Healthcare, Others), By Communication Types (FWA, eMBB, URLLC, MMTC) And Competitive Landscape

| Product Code: ETC4609350 | Publication Date: Jul 2023 | Updated Date: Jul 2026 | Product Type: Report | |

| Publisher: 6Wresearch | Author: Ravi Bhandari | No. of Pages: 200 | No. of Figures: 90 | No. of Tables: 30 |

Europe 5G Services Market Size & Growth Rate

According to 6Wresearch internal database and industry insights, the Europe 5G Services Market was accounted at nearly USD 20 billion in 2025 and is projected to reach nearly USD 670 billion by 2032, exhibiting a compound annual growth rate (CAGR) of around 14.2%during the forecast period (2026–2032).

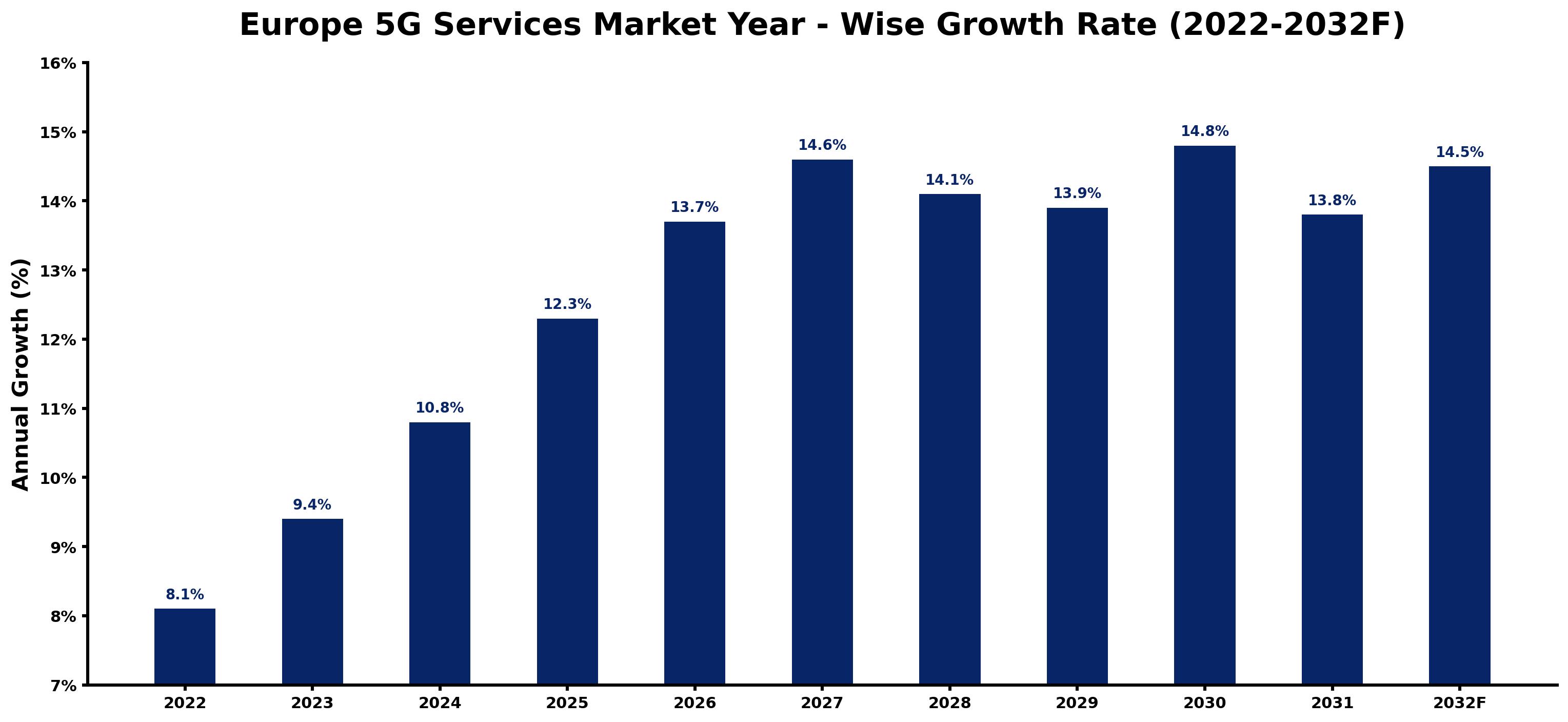

Europe 5G Services Market Year-wise Growth Rate and Key Drivers

This graph illustrates the annual growth rates of the Europe 5G Services Market from 2022 to 2032, highlighting stable industrial expansion, infrastructure-driven demand, and increasing adoption of precision finishing solutions.

The following table summarizes the historical and forecasted growth rates of the Europe 5G Services Market, along with the rationale behind each year’s performance.

| Year | Estimated Growth (%) | Market Rationale |

| 2022 | 8.1% | Early commercialization of standalone and non-standalone 5G networks across major European economies. |

| 2023 | 9.4% | Increased enterprise adoption, expanding 5G coverage, and rising consumer subscriptions. |

| 2024 | 10.8% | Growing deployment of private 5G networks and accelerated infrastructure investments. |

| 2025 | 12.3% | Broader industrial digitalization, IoT expansion, and enhanced network capacity. |

| 2026 | 13.7% | Rapid rollout of standalone 5G architecture and increasing demand for ultra-low-latency services. |

| 2027 | 14.6% | Strong enterprise adoption across manufacturing, healthcare, logistics, and smart city projects. |

| 2028 | 14.1% | Expansion of edge computing and network slicing supporting advanced industrial applications. |

| 2029 | 13.9% | Continued subscriber growth with steady investments in rural and suburban 5G coverage. |

| 2030 | 14.8% | Rising adoption of AI-enabled connectivity, autonomous systems, and mission-critical applications. |

| 2031 | 13.8% | Mature service ecosystem with sustained demand from enterprise and public-sector digital transformation. |

| 2032 | 14.5% | Ongoing innovation in 5G-enabled services, private networks, and next-generation connected applications. |

Topics Covered in the Europe 5G Services Market Report

The Europe 5G Services Market report thoroughly covers the market by countries, end users, enterprises and communication types. The report provides an unbiased and detailed analysis of ongoing market trends, opportunities/high-growth areas, and market drivers that will help stakeholders devise and align strategies according to current and future market dynamics.

Europe 5G Services Market Highlights

| Report Name | Europe 5G Services Market |

| Forecast period | 2026-2032 |

| CAGR | 14.2% |

| Market Size | USD 670 billion by 2032 |

| Growing Sector | Telecommunications & Digital Connectivity |

Europe 5G Services Market Synopsis

Europe 5G Services Industry is set to expand rapidly as telecom operators, enterprises and public authorities monetize high-speed, low-latency networks for both consumer and business use cases. Operators provide 5G mobile broadband, fixed wireless access, private and campus networks, as well as edge-enabled services that support Industry 4.0, smart cities and next-generation media. Across the region, 5G services are being adopted to improve user experience, automate industrial processes and support mission-critical communications for transportation, healthcare and public safety.

Evaluation of Growth Drivers in the Europe 5G Services Market

Below mentioned are some prominent drivers and their influence on the Europe 5G Services Market dynamics:

| Drivers | Primary Segments Affected | Why it Matters |

| Growth of Fixed Wireless Access (FWA) | UK, France, Rest of Europe; Consumers; Enterprises; FWA | FWA delivers fast broadband in underserved areas, increasing 5G uptake and ARPU. |

| Industry 4.0 and Private 5G | Italy, Germany, Spain; Manufacturing, Logistics, Energy; URLLC, mMTC | Private 5G provides automation, robotics and real-time data exchange across industrial facilities. |

| Rising Demand for Immersive Consumer Services | Russia, Rest of Europe; Consumers; eMBB | Cloud gaming, UHD video and XR need high-speed, low latency 5G connectivity. |

| Smart City and Public-sector Digitalization | France, Spain, Rest of Europe; Government; mMTC, eMBB | 5G enables smart lighting, surveillance and traffic systems, raising public-sector adoption. |

Europe 5G Services Market is expected to grow strongly at around 14.2% CAGR between 2026 and 2032. Market growth is propelled by higher expansion of 5G coverage, rising spectrum availability and the shift towards data-intensive applications in both consumer and enterprise domains. Telecom operators increasingly rely on 5G to differentiate through quality of experience, converged fixed-mobile offerings and tailored enterprise solutions. Manufacturing, logistics, healthcare and energy organizations use 5G services to connect machines, sensors and workers, unlocking higher productivity and safety. At the same time, consumer adoption is accelerated by affordable 5G handsets, bundled media and gaming services and the migration of households to FWA for high-speed broadband.

Evaluation of Restraints in the Europe 5G Services Market

Below mentioned are some major restraints and their influence on the Europe 5G Services Market dynamics:

| Restraints | Primary Segments Affected | What This Means |

| High Network Deployment and Spectrum Costs | Enterprises; Operators for Consumers & Enterprises; eMBB, FWA | High network and spectrum costs slow rollout and strain profits. |

| Regulatory Complexity and Fragmented Spectrum Policies | Government; All Communication Types | Differing regulations delay deployment across countries. |

| Monetization Challenges Beyond Connectivity | Enterprises; URLLC, mMTC | Hard-to-price advanced services restrict 5G revenue. |

| Security and Privacy Concerns | Healthcare, Government, Transportation & Logistics; URLLC, mMTC | Security problems hamper with mission-critical 5G adoption. |

Europe 5G Services Market Challenges

Europe 5G Services Market encounters various challenges such as balancing aggressive coverage obligations with constrained telecom margins, harmonizing spectrum and infrastructure policies across member states and ensuring dependable performance for mission-critical use cases. Operators must incorporate 5G with existing 4G cores, legacy OSS/BSS and enterprise IT environments while managing network complexity and energy consumption.

Europe 5G Services Market Trends

Several significant trends are impacting Europe 5G Services Industry:

- Rising deployment of standalone (SA) 5G cores and network slicing: Operators shift to SA networks, enabling dedicated slices for gaming, industry and public safety.

- Acceleration of private and campus 5G networks: Industrial sites deploy private 5G for automation, monitoring and worker safety.

- Growth of 5G fixed wireless access for home and business broadband: FWA emerges as a major fiber alternative, improving coverage in underserved areas.

- Integration of 5G with edge computing and cloud platforms: 5G combines with edge and cloud to support low-latency AI, IoT and AR/VR applications.

- Development of 5G-enabled smart mobility and V2X services: Transport sectors use 5G for connected vehicles, smarter traffic and real-time fleet management.

Investment Opportunities in the Europe 5G Services Industry

Some of the notable investment opportunities are:

- 5G-enabled enterprise solutions and managed services: Vertical-specific private networks, managed connectivity and edge services create strong recurring revenues.

- Expansion of 5G FWA and converged home services: FWA investments open new broadband markets and support bundled TV, gaming and IoT services.

- Network slicing and QoS-based premium services: Slice-based offerings for media, gaming and critical communications enable monetization of higher performance tiers.

- 5G-powered smart city and public safety projects: Municipal partnerships for analytics, smart lighting and emergency response drive long-term service demand.

- Ecosystem platforms for 5G applications and marketplaces: Developer and enterprise platforms with APIs and analytics help scale innovative 5G use cases.

Top 5 Leading Players in the Europe 5G Services Market

Below is the list of prominent companies leading in the Europe 5G Services Market Share:

1. Vodafone Group Plc

| Company Name | Vodafone Group Plc |

| Established Year | 1984 |

| Headquarters | Newbury, United Kingdom |

| Official Website | Click Here |

Vodafone Group provides extensive 5G mobile and fixed services across Europe, including consumer 5G plans, FWA and private network solutions for enterprises in manufacturing, transport and public services.

2. Deutsche Telekom AG

| Company Name | Deutsche Telekom AG |

| Established Year | 1995 |

| Headquarters | Bonn, Germany |

| Official Website | Click Here |

Deutsche Telekom operates wide 5G coverage in Germany and other European markets, offering enhanced mobile broadband, campus networks, edge services and integrated connectivity for industrial and automotive customers.

3. Orange S.A.

| Company Name | Orange S.A. |

| Established Year | 1990 |

| Headquarters | Paris, France |

| Official Website | Click Here |

Orange delivers 5G services in France and multiple European countries, focusing on enhanced consumer experience, FWA, B2B connectivity and co-innovation with enterprises in sectors such as healthcare, transport and smart cities.

4. Telefónica S.A.

| Company Name | Telefónica S.A. |

| Established Year | 1924 |

| Headquarters | Madrid, Spain |

| Official Website | Click Here |

Telefónica, through brands such as Movistar and O2, offers 5G mobile, FWA and private network services, supporting digital transformation in manufacturing, logistics and media across Spain, Germany, UK and other markets.

5. Nokia Corporation

| Company Name | Nokia Corporation |

| Established Year | 1865 |

| Headquarters | Espoo, Finland |

| Official Website | Click Here |

Nokia provides 5G network equipment and private wireless solutions and works with European operators and enterprises to deliver 5G services, edge platforms and industry-specific applications.

Government Regulations Introduced in the Europe 5G Services Market:

Government-driven several initiatives are supporting the expansion of Europe 5G Services Market Size. The European Union’s 5G Action Plan and the Digital Decade targets encourage coordinated 5G rollout along major transport corridors and in all urban areas, setting clear coverage and performance objectives. National regulators across Germany, France, Italy and Spain have conducted multi-band spectrum auctions in 700 MHz, 3.5 GHz and 26 GHz, enabling commercial deployments while imposing coverage and rural-connectivity obligations.

Future Insights of the Europe 5G Services Market

Europe 5G Services Market Growth is expected to continue gaining momentum as stakeholders transition from connectivity-focused offerings to advanced digital services that bundle 5G with cloud, edge and analytics. Over the forecast period, services for enterprises are likely to outpace pure consumer revenue growth, driven by private networks, industrial automation and managed connectivity solutions. Standalone 5G and network slicing are projected to support more granular SLAs and mission-critical communications, especially in transport, energy and public safety.

Market Segmentation Analysis

The report offers a comprehensive study of the subsequent market segments and their leading categories.

By Countries – Germany to Dominate the Market

According to Navnita, Senior Research Analyst, 6Wresearch, Germany leads the Europe 5G Services Market Size, supported by strong spectrum allocations, dense urban populations, powerful industrial base and substantial investments from major operators.

By End Users – Enterprises to Dominate the Market

Enterprises are anticipated to dominate the Europe 5G Services Market as organizations across manufacturing, transportation, energy, government and healthcare increasingly adopt 5G to power mission-critical and IoT-centric applications.

By Enterprises – Manufacturing to Dominate the Market

Within enterprise end users, Manufacturing is projected to dominate the Europe 5G Services Market, as factories and industrial parks use 5G for robotics, AGVs, real-time quality control, video analytics and predictive maintenance.

By Communication Types – eMBB to Dominate the Market

Within the specified communication types, eMBB (enhanced Mobile Broadband) is projected to dominate in value terms, as it underpins mass-market 5G smartphone services, FWA broadband, high-definition video streaming and cloud gaming.

Key Attractiveness of the Report

- 10 Years of Market Numbers

- Historical Data Starting from 2022 to 2025

- Base Year: 2025

- Forecast Data until 2032

- Key Performance Indicators Impacting the Market

- Major Upcoming Developments and Projects

Key Highlights of the Report:

- Europe 5G Services Market Outlook

- Market Size of Europe 5G Services Market, 2025

- Forecast of Europe 5G Services Market, 2032

- Historical Data and Forecast of Europe 5G Services Revenues & Volume for the Period 2022 - 2032

- Europe 5G Services Market Trend Evolution

- Europe 5G Services Market Drivers and Challenges

- Europe 5G Services Price Trends

- Europe 5G Services Porter's Five Forces

- Europe 5G Services Industry Life Cycle

- Historical Data and Forecast of Europe 5G Services Market Revenues & Volume By End Users for the Period 2022 - 2032

- Historical Data and Forecast of Europe 5G Services Market Revenues & Volume By Consumers for the Period 2022 - 2032

- Historical Data and Forecast of Europe 5G Services Market Revenues & Volume By Enterprises for the Period 2022 - 2032

- Historical Data and Forecast of Germany 5G Services Market Revenues & Volume By End Users for the Period 2022 - 2032

- Historical Data and Forecast of Germany 5G Services Market Revenues & Volume By Consumers for the Period 2022 - 2032

- Historical Data and Forecast of Germany 5G Services Market Revenues & Volume By Enterprises for the Period 2022 - 2032

- Historical Data and Forecast of United Kingdom 5G Services Market Revenues & Volume By End Users for the Period 2022 - 2032

- Historical Data and Forecast of United Kingdom 5G Services Market Revenues & Volume By Consumers for the Period 2022 - 2032

- Historical Data and Forecast of United Kingdom 5G Services Market Revenues & Volume By Enterprises for the Period 2022 - 2032

- Historical Data and Forecast of France 5G Services Market Revenues & Volume By End Users for the Period 2022 - 2032

- Historical Data and Forecast of France 5G Services Market Revenues & Volume By Consumers for the Period 2022 - 2032

- Historical Data and Forecast of France 5G Services Market Revenues & Volume By Enterprises for the Period 2022 - 2032

- Historical Data and Forecast of Italy 5G Services Market Revenues & Volume By End Users for the Period 2022 - 2032

- Historical Data and Forecast of Italy 5G Services Market Revenues & Volume By Consumers for the Period 2022 - 2032

- Historical Data and Forecast of Italy 5G Services Market Revenues & Volume By Enterprises for the Period 2022 - 2032

- Historical Data and Forecast of Russia 5G Services Market Revenues & Volume By End Users for the Period 2022 - 2032

- Historical Data and Forecast of Russia 5G Services Market Revenues & Volume By Consumers for the Period 2022 - 2032

- Historical Data and Forecast of Russia 5G Services Market Revenues & Volume By Enterprises for the Period 2022 - 2032

- Historical Data and Forecast of Spain 5G Services Market Revenues & Volume By End Users for the Period 2022 - 2032

- Historical Data and Forecast of Spain 5G Services Market Revenues & Volume By Consumers for the Period 2022 - 2032

- Historical Data and Forecast of Spain 5G Services Market Revenues & Volume By Enterprises for the Period 2022 - 2032

- Historical Data and Forecast of Rest of Europe 5G Services Market Revenues & Volume By End Users for the Period 2022 - 2032

- Historical Data and Forecast of Rest of Europe 5G Services Market Revenues & Volume By Consumers for the Period 2022 - 2032

- Historical Data and Forecast of Rest of Europe 5G Services Market Revenues & Volume By Enterprises for the Period 2022 - 2032

- Historical Data and Forecast of Europe 5G Services Market Revenues & Volume By Enterprises for the Period 2022 - 2032

- Historical Data and Forecast of Europe 5G Services Market Revenues & Volume By Manufacturing for the Period 2022 - 2032

- Historical Data and Forecast of Europe 5G Services Market Revenues & Volume By Energy and Utilities for the Period 2022 - 2032

- Historical Data and Forecast of Europe 5G Services Market Revenues & Volume By Media and Entertainment for the Period 2022 - 2032

- Historical Data and Forecast of Europe 5G Services Market Revenues & Volume By Government for the Period 2022 - 2032

- Historical Data and Forecast of Europe 5G Services Market Revenues & Volume By Transportation and Logistics for the Period 2022 - 2032

- Historical Data and Forecast of Europe 5G Services Market Revenues & Volume By Healthcare for the Period 2022 - 2032

- Historical Data and Forecast of Europe 5G Services Market Revenues & Volume By Others for the Period 2022 - 2032

- Historical Data and Forecast of Germany 5G Services Market Revenues & Volume By Enterprises for the Period 2022 - 2032

- Historical Data and Forecast of Germany 5G Services Market Revenues & Volume By Manufacturing for the Period 2022 - 2032

- Historical Data and Forecast of Germany 5G Services Market Revenues & Volume By Energy and Utilities for the Period 2022 - 2032

- Historical Data and Forecast of Germany 5G Services Market Revenues & Volume By Media and Entertainment for the Period 2022 - 2032

- Historical Data and Forecast of Germany 5G Services Market Revenues & Volume By Government for the Period 2022 - 2032

- Historical Data and Forecast of Germany 5G Services Market Revenues & Volume By Transportation and Logistics for the Period 2022 - 2032

- Historical Data and Forecast of Germany 5G Services Market Revenues & Volume By Healthcare for the Period 2022 - 2032

- Historical Data and Forecast of Germany 5G Services Market Revenues & Volume By Others for the Period 2022 - 2032

- Historical Data and Forecast of United Kingdom 5G Services Market Revenues & Volume By Enterprises for the Period 2022 - 2032

- Historical Data and Forecast of United Kingdom 5G Services Market Revenues & Volume By Manufacturing for the Period 2022 - 2032

- Historical Data and Forecast of United Kingdom 5G Services Market Revenues & Volume By Energy and Utilities for the Period 2022 - 2032

- Historical Data and Forecast of United Kingdom 5G Services Market Revenues & Volume By Media and Entertainment for the Period 2022 - 2032

- Historical Data and Forecast of United Kingdom 5G Services Market Revenues & Volume By Government for the Period 2022 - 2032

- Historical Data and Forecast of United Kingdom 5G Services Market Revenues & Volume By Transportation and Logistics for the Period 2022 - 2032

- Historical Data and Forecast of United Kingdom 5G Services Market Revenues & Volume By Healthcare for the Period 2022 - 2032

- Historical Data and Forecast of United Kingdom 5G Services Market Revenues & Volume By Others for the Period 2022 - 2032

- Historical Data and Forecast of France 5G Services Market Revenues & Volume By Enterprises for the Period 2022 - 2032

- Historical Data and Forecast of France 5G Services Market Revenues & Volume By Manufacturing for the Period 2022 - 2032

- Historical Data and Forecast of France 5G Services Market Revenues & Volume By Energy and Utilities for the Period 2022 - 2032

- Historical Data and Forecast of France 5G Services Market Revenues & Volume By Media and Entertainment for the Period 2022 - 2032

- Historical Data and Forecast of France 5G Services Market Revenues & Volume By Government for the Period 2022 - 2032

- Historical Data and Forecast of France 5G Services Market Revenues & Volume By Transportation and Logistics for the Period 2022 - 2032

- Historical Data and Forecast of France 5G Services Market Revenues & Volume By Healthcare for the Period 2022 - 2032

- Historical Data and Forecast of France 5G Services Market Revenues & Volume By Others for the Period 2022 - 2032

- Historical Data and Forecast of Italy 5G Services Market Revenues & Volume By Enterprises for the Period 2022 - 2032

- Historical Data and Forecast of Italy 5G Services Market Revenues & Volume By Manufacturing for the Period 2022 - 2032

- Historical Data and Forecast of Italy 5G Services Market Revenues & Volume By Energy and Utilities for the Period 2022 - 2032

- Historical Data and Forecast of Italy 5G Services Market Revenues & Volume By Media and Entertainment for the Period 2022 - 2032

- Historical Data and Forecast of Italy 5G Services Market Revenues & Volume By Government for the Period 2022 - 2032

- Historical Data and Forecast of Italy 5G Services Market Revenues & Volume By Transportation and Logistics for the Period 2022 - 2032

- Historical Data and Forecast of Italy 5G Services Market Revenues & Volume By Healthcare for the Period 2022 - 2032

- Historical Data and Forecast of Italy 5G Services Market Revenues & Volume By Others for the Period 2022 - 2032

- Historical Data and Forecast of Russia 5G Services Market Revenues & Volume By Enterprises for the Period 2022 - 2032

- Historical Data and Forecast of Russia 5G Services Market Revenues & Volume By Manufacturing for the Period 2022 - 2032

- Historical Data and Forecast of Russia 5G Services Market Revenues & Volume By Energy and Utilities for the Period 2022 - 2032

- Historical Data and Forecast of Russia 5G Services Market Revenues & Volume By Media and Entertainment for the Period 2022 - 2032

- Historical Data and Forecast of Russia 5G Services Market Revenues & Volume By Government for the Period 2022 - 2032

- Historical Data and Forecast of Russia 5G Services Market Revenues & Volume By Transportation and Logistics for the Period 2022 - 2032

- Historical Data and Forecast of Russia 5G Services Market Revenues & Volume By Healthcare for the Period 2022 - 2032

- Historical Data and Forecast of Russia 5G Services Market Revenues & Volume By Others for the Period 2022 - 2032

- Historical Data and Forecast of Spain 5G Services Market Revenues & Volume By Enterprises for the Period 2022 - 2032

- Historical Data and Forecast of Spain 5G Services Market Revenues & Volume By Manufacturing for the Period 2022 - 2032

- Historical Data and Forecast of Spain 5G Services Market Revenues & Volume By Energy and Utilities for the Period 2022 - 2032

- Historical Data and Forecast of Spain 5G Services Market Revenues & Volume By Media and Entertainment for the Period 2022 - 2032

- Historical Data and Forecast of Spain 5G Services Market Revenues & Volume By Government for the Period 2022 - 2032

- Historical Data and Forecast of Spain 5G Services Market Revenues & Volume By Transportation and Logistics for the Period 2022 - 2032

- Historical Data and Forecast of Spain 5G Services Market Revenues & Volume By Healthcare for the Period 2022 - 2032

- Historical Data and Forecast of Spain 5G Services Market Revenues & Volume By Others for the Period 2022 - 2032

- Historical Data and Forecast of Rest of Europe 5G Services Market Revenues & Volume By Enterprises for the Period 2022 - 2032

- Historical Data and Forecast of Rest of Europe 5G Services Market Revenues & Volume By Manufacturing for the Period 2022 - 2032

- Historical Data and Forecast of Rest of Europe 5G Services Market Revenues & Volume By Energy and Utilities for the Period 2022 - 2032

- Historical Data and Forecast of Rest of Europe 5G Services Market Revenues & Volume By Media and Entertainment for the Period 2022 - 2032

- Historical Data and Forecast of Rest of Europe 5G Services Market Revenues & Volume By Government for the Period 2022 - 2032

- Historical Data and Forecast of Rest of Europe 5G Services Market Revenues & Volume By Transportation and Logistics for the Period 2022 - 2032

- Historical Data and Forecast of Rest of Europe 5G Services Market Revenues & Volume By Healthcare for the Period 2022 - 2032

- Historical Data and Forecast of Rest of Europe 5G Services Market Revenues & Volume By Others for the Period 2022 - 2032

- Historical Data and Forecast of Europe 5G Services Market Revenues & Volume By Communication Types for the Period 2022 - 2032

- Historical Data and Forecast of Europe 5G Services Market Revenues & Volume By FWA for the Period 2022 - 2032

- Historical Data and Forecast of Europe 5G Services Market Revenues & Volume By eMBB for the Period 2022 - 2032

- Historical Data and Forecast of Europe 5G Services Market Revenues & Volume By URLLC for the Period 2022 - 2032

- Historical Data and Forecast of Europe 5G Services Market Revenues & Volume By MMTC for the Period 2022 - 2032

- Historical Data and Forecast of Germany 5G Services Market Revenues & Volume By Communication Types for the Period 2022 - 2032

- Historical Data and Forecast of Germany 5G Services Market Revenues & Volume By FWA for the Period 2022 - 2032

- Historical Data and Forecast of Germany 5G Services Market Revenues & Volume By eMBB for the Period 2022 - 2032

- Historical Data and Forecast of Germany 5G Services Market Revenues & Volume By URLLC for the Period 2022 - 2032

- Historical Data and Forecast of Germany 5G Services Market Revenues & Volume By MMTC for the Period 2022 - 2032

- Historical Data and Forecast of United Kingdom 5G Services Market Revenues & Volume By Communication Types for the Period 2022 - 2032

- Historical Data and Forecast of United Kingdom 5G Services Market Revenues & Volume By FWA for the Period 2022 - 2032

- Historical Data and Forecast of United Kingdom 5G Services Market Revenues & Volume By eMBB for the Period 2022 - 2032

- Historical Data and Forecast of United Kingdom 5G Services Market Revenues & Volume By URLLC for the Period 2022 - 2032

- Historical Data and Forecast of United Kingdom 5G Services Market Revenues & Volume By MMTC for the Period 2022 - 2032

- Historical Data and Forecast of France 5G Services Market Revenues & Volume By Communication Types for the Period 2022 - 2032

- Historical Data and Forecast of France 5G Services Market Revenues & Volume By FWA for the Period 2022 - 2032

- Historical Data and Forecast of France 5G Services Market Revenues & Volume By eMBB for the Period 2022 - 2032

- Historical Data and Forecast of France 5G Services Market Revenues & Volume By URLLC for the Period 2022 - 2032

- Historical Data and Forecast of France 5G Services Market Revenues & Volume By MMTC for the Period 2022 - 2032

- Historical Data and Forecast of Italy 5G Services Market Revenues & Volume By Communication Types for the Period 2022 - 2032

- Historical Data and Forecast of Italy 5G Services Market Revenues & Volume By FWA for the Period 2022 - 2032

- Historical Data and Forecast of Italy 5G Services Market Revenues & Volume By eMBB for the Period 2022 - 2032

- Historical Data and Forecast of Italy 5G Services Market Revenues & Volume By URLLC for the Period 2022 - 2032

- Historical Data and Forecast of Italy 5G Services Market Revenues & Volume By MMTC for the Period 2022 - 2032

- Historical Data and Forecast of Russia 5G Services Market Revenues & Volume By Communication Types for the Period 2022 - 2032

- Historical Data and Forecast of Russia 5G Services Market Revenues & Volume By FWA for the Period 2022 - 2032

- Historical Data and Forecast of Russia 5G Services Market Revenues & Volume By eMBB for the Period 2022 - 2032

- Historical Data and Forecast of Russia 5G Services Market Revenues & Volume By URLLC for the Period 2022 - 2032

- Historical Data and Forecast of Russia 5G Services Market Revenues & Volume By MMTC for the Period 2022 - 2032

- Historical Data and Forecast of Spain 5G Services Market Revenues & Volume By Communication Types for the Period 2022 - 2032

- Historical Data and Forecast of Spain 5G Services Market Revenues & Volume By FWA for the Period 2022 - 2032

- Historical Data and Forecast of Spain 5G Services Market Revenues & Volume By eMBB for the Period 2022 - 2032

- Historical Data and Forecast of Spain 5G Services Market Revenues & Volume By URLLC for the Period 2022 - 2032

- Historical Data and Forecast of Spain 5G Services Market Revenues & Volume By MMTC for the Period 2022 - 2032

- Historical Data and Forecast of Rest of Europe 5G Services Market Revenues & Volume By Communication Types for the Period 2022 - 2032

- Historical Data and Forecast of Rest of Europe 5G Services Market Revenues & Volume By FWA for the Period 2022 - 2032

- Historical Data and Forecast of Rest of Europe 5G Services Market Revenues & Volume By eMBB for the Period 2022 - 2032

- Historical Data and Forecast of Rest of Europe 5G Services Market Revenues & Volume By URLLC for the Period 2022 - 2032

- Historical Data and Forecast of Rest of Europe 5G Services Market Revenues & Volume By MMTC for the Period 2022 - 2032

- Europe 5G Services Market - Key Performance Indicators

- Europe 5G Services Market - Import Export Trade Statistics

- Europe 5G Services Market - Opportunity Assessment By Countries

- Europe 5G Services Market - Opportunity Assessment By End Users

- Europe 5G Services Market - Opportunity Assessment By Enterprises

- Europe 5G Services Market - Opportunity Assessment By Communication Types

- Europe 5G Services Market - Top Companies Market Share

- Europe 5G Services Market - Top Companies Profiles

- Europe 5G Services Market - Comparison of Players in Technical and Operating Parameters

- Europe 5G Services Market - Strategic Recommendations

Market Covered

The report offers a comprehensive study of the subsequent market segments:

By Countries

- Germany

- United Kingdom

- France

- Italy

- Russia

- Spain

- Rest of Europe

By End Users

- Consumers

- Enterprises

By Enterprises

- Manufacturing

- Energy and Utilities

- Media and Entertainment

- Government

- Transportation and Logistics

- Healthcare

- Others

By Communication Types

- FWA

- eMBB

- URLLC

- MMTC

Europe 5G Services Market (2026-2032): FAQ's

The Europe 5G Services Market is projected to grow at a CAGR of around 14.2%during the forecast period.

The Europe 5G Services Market was valued at nearly USD 20 billion in 2024 and is projected to reach nearly USD 670 billion by 2032.

Enterprises are anticipated to lead the market, as organizations across manufacturing, logistics, energy, government and healthcare increasingly adopt 5G services.

Government initiatives such as coordinated spectrum auctions, digital connectivity targets and incentives for rural coverage are accelerating region-wide 5G rollout.

Key challenges include high deployment and spectrum costs, monetization constraints for advanced services, security and privacy concerns.

6Wresearch actively monitors the Europe 5G Services Market and publishes its comprehensive annual report, highlighting emerging trends, growth drivers, revenue analysis, and forecast outlook. Our insights help businesses to make data-backed strategic decisions with ongoing market dynamics. Our analysts track relevent industries related to the Europe 5G Services Market, allowing our clients with actionable intelligence and reliable forecasts tailored to emerging regional needs.

Yes, we provide customisation as per your requirements. To learn more, feel free to contact us on sales@6wresearch.com

| 1 Executive Summary |

| 2 Introduction |

| 2.1 Key Highlights of the Report |

| 2.2 Report Description |

| 2.3 Market Scope & Segmentation |

| 2.4 Research Methodology |

| 2.5 Assumptions |

| 3 Europe 5G Services Market Overview |

| 3.1 Europe Regional Macro Economic Indicators |

| 3.2 Europe 5G Services Market Revenues & Volume, 2022 & 2032F |

| 3.3 Europe 5G Services Market - Industry Life Cycle |

| 3.4 Europe 5G Services Market - Porter's Five Forces |

| 3.5 Europe 5G Services Market Revenues & Volume Share, By Countries, 2022 & 2032F |

| 3.6 Europe 5G Services Market Revenues & Volume Share, By End Users, 2022 & 2032F |

| 3.7 Europe 5G Services Market Revenues & Volume Share, By Enterprises, 2022 & 2032F |

| 3.8 Europe 5G Services Market Revenues & Volume Share, By Communication Types, 2022 & 2032F |

| 4 Europe 5G Services Market Dynamics |

| 4.1 Impact Analysis |

| 4.2 Market Drivers |

| 4.3 Market Restraints |

| 5 Europe 5G Services Market Trends |

| 6 Europe 5G Services Market, 2022 - 2032 |

| 6.1 Europe 5G Services Market, Revenues & Volume, By End Users, 2022 - 2032 |

| 6.2 Europe 5G Services Market, Revenues & Volume, By Enterprises, 2022 - 2032 |

| 6.3 Europe 5G Services Market, Revenues & Volume, By Communication Types, 2022 - 2032 |

| 7 Germany 5G Services Market, 2022 - 2032 |

| 7.1 Germany 5G Services Market, Revenues & Volume, By End Users, 2022 - 2032 |

| 7.2 Germany 5G Services Market, Revenues & Volume, By Enterprises, 2022 - 2032 |

| 7.3 Germany 5G Services Market, Revenues & Volume, By Communication Types, 2022 - 2032 |

| 8 United Kingdom 5G Services Market, 2022 - 2032 |

| 8.1 United Kingdom 5G Services Market, Revenues & Volume, By End Users, 2022 - 2032 |

| 8.2 United Kingdom 5G Services Market, Revenues & Volume, By Enterprises, 2022 - 2032 |

| 8.3 United Kingdom 5G Services Market, Revenues & Volume, By Communication Types, 2022 - 2032 |

| 9 France 5G Services Market, 2022 - 2032 |

| 9.1 France 5G Services Market, Revenues & Volume, By End Users, 2022 - 2032 |

| 9.2 France 5G Services Market, Revenues & Volume, By Enterprises, 2022 - 2032 |

| 9.3 France 5G Services Market, Revenues & Volume, By Communication Types, 2022 - 2032 |

| 10 Italy 5G Services Market, 2022 - 2032 |

| 10.1 Italy 5G Services Market, Revenues & Volume, By End Users, 2022 - 2032 |

| 10.2 Italy 5G Services Market, Revenues & Volume, By Enterprises, 2022 - 2032 |

| 10.3 Italy 5G Services Market, Revenues & Volume, By Communication Types, 2022 - 2032 |

| 11 Russia 5G Services Market, 2022 - 2032 |

| 11.1 Russia 5G Services Market, Revenues & Volume, By End Users, 2022 - 2032 |

| 11.2 Russia 5G Services Market, Revenues & Volume, By Enterprises, 2022 - 2032 |

| 11.3 Russia 5G Services Market, Revenues & Volume, By Communication Types, 2022 - 2032 |

| 12 Spain 5G Services Market, 2022 - 2032 |

| 12.1 Spain 5G Services Market, Revenues & Volume, By End Users, 2022 - 2032 |

| 12.2 Spain 5G Services Market, Revenues & Volume, By Enterprises, 2022 - 2032 |

| 12.3 Spain 5G Services Market, Revenues & Volume, By Communication Types, 2022 - 2032 |

| 13 Rest of Europe 5G Services Market, 2022 - 2032 |

| 13.1 Rest of Europe 5G Services Market, Revenues & Volume, By End Users, 2022 - 2032 |

| 13.2 Rest of Europe 5G Services Market, Revenues & Volume, By Enterprises, 2022 - 2032 |

| 13.3 Rest of Europe 5G Services Market, Revenues & Volume, By Communication Types, 2022 - 2032 |

| 14 Europe 5G Services Market Key Performance Indicators |

| 15 Europe 5G Services Market - Opportunity Assessment |

| 15.1 Europe 5G Services Market Opportunity Assessment, By Countries, 2022 & 2032F |

| 15.2 Europe 5G Services Market Opportunity Assessment, By End Users, 2022 & 2032F |

| 15.3 Europe 5G Services Market Opportunity Assessment, By Enterprises, 2022 & 2032F |

| 15.4 Europe 5G Services Market Opportunity Assessment, By Communication Types, 2022 & 2032F |

| 16 Europe 5G Services Market - Competitive Landscape |

| 16.1 Europe 5G Services Market Revenue Share, By Companies, 2025 |

| 16.2 Europe 5G Services Market Competitive Benchmarking, By Operating and Technical Parameters |

| 17 Company Profiles |

| 18 Recommendations |

| 19 Disclaimer |

Global Go To Market Strategy - 2030

Export potential enables firms to identify high-growth global markets with greater confidence by combining advanced trade intelligence with a structured quantitative methodology. The framework analyzes emerging demand trends and country-level import patterns while integrating macroeconomic and trade datasets such as GDP and population forecasts, bilateral import–export flows, tariff structures, elasticity differentials between developed and developing economies, geographic distance, and import demand projections. Using weighted trade values from 2020–2024 as the base period to project country-to-country export potential for 2030, these inputs are operationalized through calculated drivers such as gravity model parameters, tariff impact factors, and projected GDP per-capita growth. Through an analysis of hidden potentials, demand hotspots, and market conditions that are most favorable to success, this method enables firms to focus on target countries, maximize returns, and global expansion with data, backed by accuracy.

By factoring in the projected importer demand gap that is currently unmet and could be potential opportunity, it identifies the potential for the Exporter (Country) among 190 countries, against the general trade analysis, which identifies the biggest importer or exporter.

To discover high-growth global markets and optimize your business strategy:

Click Here

Pricing

- Single User License$ 4,560

- Department License$ 5,055

- Site License$ 5,595

- Global License$ 6,000

Leadership Perspectives from Industry Events

Search

Thought Leadership and Analyst Meet

Our Clients

6WResearch In News

- India Air Conditioner Market Set for Strong Rebound in 2026 After Weather-Led Correction and GST-Driven Recovery: 6Wresearch

- ADAS in India: How Automatic Emergency Braking, Blind Spot Detection & Driver Monitoring are Transforming Road Safety

- Doha a strategic location for EV manufacturing hub: IPA Qatar

- Demand for luxury TVs surging in the GCC, says Samsung

- Empowering Growth: The Thriving Journey of Bangladesh’s Cable Industry

- Demand for luxury TVs surging in the GCC, says Samsung

Latest Reports

- Nicaragua RPG Gaming Market (2026-2032)

- New Zealand RPG Gaming Market (2026-2032)

- Netherlands RPG Gaming Market (2026-2032)

- Nauru RPG Gaming Market (2026-2032)

- Namibia RPG Gaming Market (2026-2032)

- Mozambique RPG Gaming Market (2026-2032)

- Montenegro RPG Gaming Market (2026-2032)

- Mongolia RPG Gaming Market (2026-2032)

- Monaco RPG Gaming Market (2026-2032)

- Micronesia RPG Gaming Market (2026-2032)

Industry Events and Analyst Meet

EV India Expo 2026

HIMTEX 2026

India Refining Summit 2026

India EV Show 2026

EV tech India Expo 2026

Whitepaper

- Middle East & Africa Commercial Security Market Click here to view more.

- Middle East & Africa Fire Safety Systems & Equipment Market Click here to view more.

- GCC Drone Market Click here to view more.

- Middle East Lighting Fixture Market Click here to view more.

- GCC Physical & Perimeter Security Market Click here to view more.