Philippines Cheese Market (2026-2032) | Outlook, Companies, Industry, Value, Trends, Growth, Analysis, Revenue, Share, Forecast & Size

Market Forecast By Type (Natural, Processed), By Product (Mozzarella, Cheddar, Feta, Parmesan, Roquefort, Others), By Source (Cow Milk, Sheep Milk, Goat Milk, Buffalo), By Distribution Channel (Hypermarkets, Supermarkets, Food Specialty Stores, Convenience Stores, Others) And Competitive Landscape

| Product Code: ETC180288 | Publication Date: Jan 2022 | Updated Date: Mar 2026 | Product Type: Market Research Report | |

| Publisher: 6Wresearch | Author: Ravi Bhandari | No. of Pages: 70 | No. of Figures: 35 | No. of Tables: 5 |

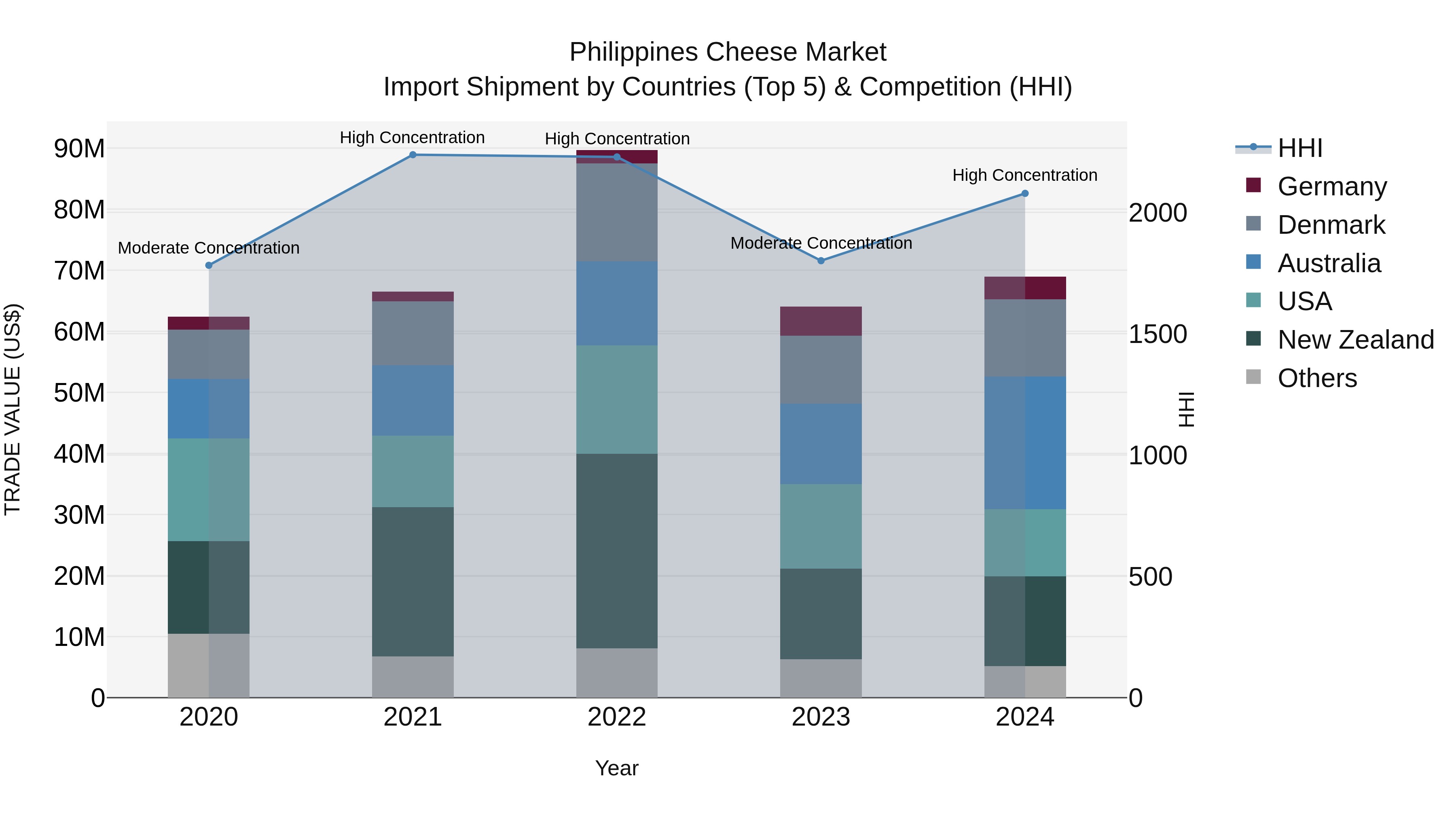

Philippines Cheese Market Top 5 Importing Countries and Market Competition (HHI) Analysis

The Philippines experienced a notable increase in cheese import shipments in 2024, with top exporting countries being Australia, New Zealand, Denmark, USA, and Germany. The market saw a shift from moderate to high concentration, indicating a more focused supplier base. The compound annual growth rate (CAGR) from 2020 to 2024 stood at 2.53%, with a significant growth rate of 7.6% in 2024 alone. This trend suggests a growing demand for imported cheese in the Philippines, potentially driven by changing consumer preferences and a thriving food industry.

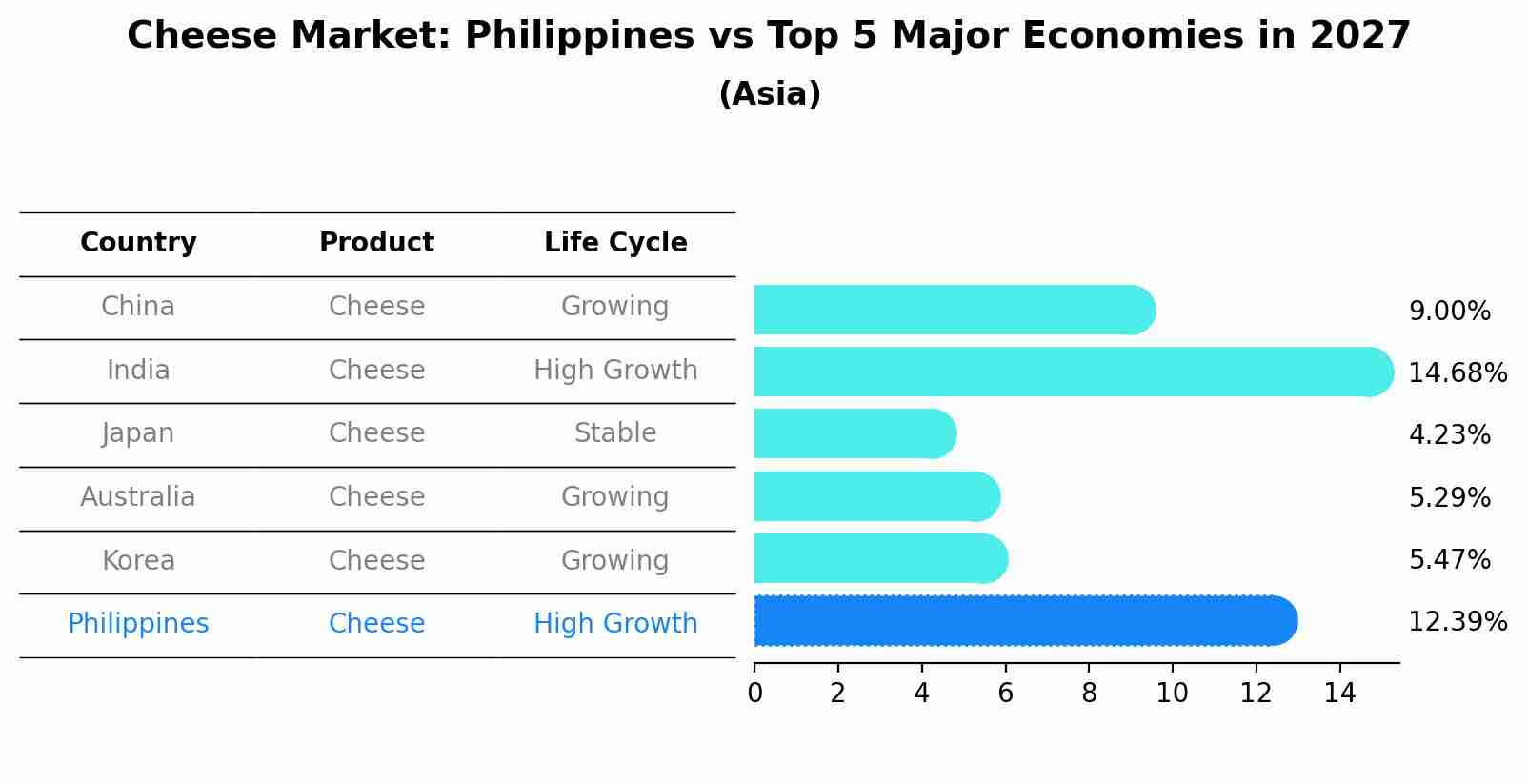

Cheese Market: Philippines vs Top 5 Major Economies in 2027 (Asia)

By 2027, Philippines's Cheese market is forecasted to achieve a high growth rate of 12.39%, with China leading the Asia region, followed by India, Japan, Australia and South Korea.

Philippines Cheese Market Growth Rate

According to 6Wresearch internal database and industry insights, the Philippines Cheese Market is projected to grow at a compound annual growth rate (CAGR) of 5.8% during the forecast period from 2026 to 2032.

Topics Covered in the Philippines Cheese Market Report

The Philippines Cheese Market report thoroughly covers the market by type, product, source, and distribution channel. It provides an unbiased and detailed analysis of ongoing market trends, opportunities, challenges, and market drivers, helping stakeholders align their strategies with current and future market dynamics.

Philippines Cheese Market Highlights

| Report Name | Philippines Cheese Market |

| Forecast Period | 2026–2032 |

| CAGR | 5.8% |

| Growing Sector | Dairy and Food Processing |

Philippines Cheese Market Synopsis

Philippines Cheese Market has been rising steadily due to changes in the eating habits of the people. A busy lifestyle and increasing income drive the widespread usage of cheese at home, along with restaurants. Additionally, Cities like Metro Manila, Cebu, and Davao are major centres for cheese consumption, where both international and local brands are active due to rapid urbanisation and shifting people's eating habits. Moreover, the influence of fast-food chains, the rising popularity of Western food, and the increase in home cooking are some major factors supporting the stable Philippines cheese market across the country.

Evaluation of Growth Drivers in the Philippines Cheese Market

Below mentioned are some prominent drivers and their impact on the Philippines Cheese Market dynamics:

| Drivers | Primary Segment Affected | Why It Matters (Evidence) |

| Rising Fast Food Consumption | Processed, Mozzarella | The rapid growth of pizza chains and burger outlets drives a massive volume of cheese consumption in urban centers. |

| Westernization of Palates | Natural, Cheddar | Natural cheeses are becoming more popular among young Filipino customers for everyday breakfasts and charcuterie platters. |

| Growth of E-commerce | All Segments | Online shopping platforms have made specialty and foreign cheeses more accessible to buyers outside of big cities. |

| Health and Wellness Trends | Natural, Goat Milk | Natural and non-cow milk cheese variants are becoming increasingly popular as consumers seek out clean-label and nutrient-rich snacks. |

| Expansion of Retail Chains | Distribution Channels | The expansion of hypermarkets and specialist delis enables improved product visibility and specialized storage for fragile cheeses. |

Philippines Cheese Market is projected to grow at a CAGR of 5.8% from 2026 to 2032. The increasing demand for tasty, convenient, and versatile food items is propelling the demand for various types of cheese. Additionally, the higher demand for quick meals that include cheese boosts due to the busy lifestyle of people. Health-conscious consumers are also preferring cheese as it is a good source of protein and calcium, further supporting the market growth. Moreover, the ongoing expansion of fast food restaurants, cloud kitchens, and food delivery apps also boosts the Philippines Cheese Market Growth.

Evaluation of Restraints in the Philippines Cheese Market

Below mentioned are some major restraints and their influence on the Philippines Cheese Market dynamics:

| Restraints | Primary Segment Affected | What This Means (Evidence) |

| High Import Dependency | Natural, Premium | High reliance on imported cheese from Australia and the US makes the market vulnerable to currency fluctuations and global supply chain shifts. |

| Cold Chain Limitations | Natural, Specialty | Inadequate refrigerated transport in rural areas leads to product spoilage and limits the market reach of temperature-sensitive cheeses. |

| Lactose Intolerance Awareness | All Segments | A significant portion of the Asian population is lactose sensitive, which can limit the per capita consumption of traditional dairy cheese. |

| High Price of Premium Cheese | Food Specialty Stores | Inflation and high tariffs on gourmet cheeses make them luxury items, deterring price-sensitive mass-market consumers. |

| Low Local Milk Production | Source (Cow Milk) | The Philippines produces less than 1% of its dairy requirement locally, creating a bottleneck for domestic cheese manufacturing. |

Philippines Cheese Market Challenges

Philippines Cheese Industry confronts many challenges such as high logistics costs for refrigerated goods, heavy reliance on international suppliers for raw materials, and intense competition from low-cost dairy alternatives. The tropical climate poses significant hurdles for the storage of natural cheeses, requiring high energy consumption for cooling. Despite all these challenges, the government support for small-scale dairy cooperatives and new advancements in packaging technology is likely to continue to drive demand in this market. Furthermore, many retailers are investing in broad cheese portfolios as consumers become more aware of cheese culinary versatility and the potential for long-term growth in the hospitality industry.

Emerging Trends in the Philippines Cheese Market

Trends driving the Philippines Cheese Market include:

- Rise of Plant-Based Alternatives: The trend of plant-based cheeses, particularly those made from nuts and coconut oil, as people become more conscious about their health and the common problem of lactose intolerance.

- Korean-Inspired Cheese Applications: Stretchy mozzarella is in high demand due to the "cheese pull" trend in street foods like corn dogs and tteokbokki.

- Artisanal and Local Craft Cheese: Small-batch cheesemakers in areas like Davao and Laguna are gaining traction by producing high-quality Kesong Puti and goat cheeses.

- Snackification of Cheese: Cheese sticks and cubes are becoming a business and school lunch box staple, as they are simple to prepare.

- Digital Culinary Influencers: On social media, “Mukbangs" and recipes are introducing consumers to ways that they can use a variety of types of cheese including Parmesan and Feta, in their home cooking.

Investment Opportunities in the Philippines Cheese Market

Key investment avenues in the Philippines Cheese Market are:

- Cold Chain Infrastructure: Building refrigerated storage and delivery systems to ensure product integrity across the archipelago.

- Local Dairy Farming Modernization: Creating high-tech dairy farms to boost local milk supply and minimize reliance on costly imports.

- Processed Cheese Manufacturing: Establishing regional processing facilities to meet the high volume of demand from the nearby bakery and fast-food sectors.

- Specialty Cheese Retail: Establishing cheese boutiques or “cheese rooms” in upscale shopping malls to take advantage of the increasing premium cheese markets.

- Functional Cheese Products: To appeal to Filipino parents who are health-conscious, cheese fortified with vitamins or probiotics is being developed.

Top 5 Leading Players in the Philippines Cheese Market

Below is the list of prominent companies leading in the Philippines Cheese Market:

1. Mondelez Philippines, Inc.

| Company Name | Mondelez Philippines, Inc. |

|---|---|

| Established Year | 1963 |

| Headquarters | Parañaque City, Philippines |

| Official Website | Click Here |

As the maker of the iconic Eden brand, Mondelez is the market leader in the processed cheese segment, known for its creamy texture suited to the Filipino palate.

2. Arla Foods Philippines

| Company Name | Arla Foods Philippines |

|---|---|

| Established Year | 1958 (Global) |

| Headquarters | Makati City, Philippines (Regional Office) |

| Official Website | Click Here |

A major European dairy cooperative, Arla provides a wide range of natural cheeses, including slices, cream cheese, and feta, targeting the health-conscious urban segment.

3. Magnolia Inc.

| Company Name | Magnolia Inc. |

|---|---|

| Established Year | 1925 |

| Headquarters | Pasig City, Philippines |

| Official Website | - |

A household name in the Philippines, Magnolia produces a variety of cheese products ranging from traditional processed blocks to quick-melt variants for culinary use.

4. Nestlé Philippines, Inc.

| Company Name | Nestlé Philippines, Inc. |

|---|---|

| Established Year | 1911 |

| Headquarters | Makati City, Philippines |

| Official Website | Click Here |

Nestlé plays a significant role in the dairy market, offering cheese-flavored products and cream-based cheeses that are staples in Filipino dessert making.

5. Century Pacific Food, Inc.

| Company Name | Century Pacific Food, Inc. (Snowy Mountain) |

|---|---|

| Established Year | 1978 |

| Headquarters | Pasig City, Philippines |

| Official Website | Click Here |

Known for diversification, they have expanded into the dairy sector, providing affordable cheese options that compete in the mass-market retail segment.

Government Regulations Introduced in the Philippines Cheese Market

According to Philippines’ government data, the Philippines has introduced many policies to support the dairy sector, such as the National Dairy Development Act, which aims to accelerate the growth of the local dairy industry through the National Dairy Authority (NDA). To boost milk production for cheese, the government offers local farmers high-quality livestock and technical assistance through the Dairy Multiplier Farm Program. Furthermore, all locally and imported cheese must adhere to stringent hygienic standards, as mandated by the Food Safety Act of 2013. To satisfy the local demand, the Bureau of Customs also oversees tariff quotas under various Free Trade Agreements (FTAs), which allow for the controlled importation of foreign cheese varieties.

Future Insights of the Philippines Cheese Market

The Philippines Cheese Market Share is expected to grow steadily in the future. The role of Technology will be crucial in cold-chain delivery, smart inventory systems, and digital ordering platforms, which help to enhance access and storage. Additionally, the shifting preference of consumers for more personalised and healthy cheese products will drive robust market growth. Moreover, eco-friendly and sustainable packaging is likely to become more common due to rising environmental concerns among people, also supporting the market growth in the coming years.

Market Segmentation Analysis

The report offers a comprehensive study of the subsequent market segments and their leading categories:

By Type - Processed Cheese to dominate the market

According to Ekta, Senior Research Analyst, 6Wresearch, Processed cheese is expected to dominate the market share due to its long shelf life, affordability, and high melting point, which makes it ideal for the tropical climate. It is a mainstay in Filipino households, used in traditional dishes such as "pancit" and "ensaymada," and remains the preferred choice for the huge network of local bakeries and sari-sari stores.

By Product - Cheddar to dominate the market

Cheddar cheese is the dominant product segment because it is the primary flavor profile preferred by Filipino consumers. Its versatility makes it suitable for a variety of dishes, including sandwiches and desserts. While Mozzarella is rapidly expanding due to the pizza sector, Cheddar established position in both processed and natural versions ensures market domination.

By Source - Cow Milk to dominate the market

Cow milk remains the primary source for cheese production in the Philippines due to the established worldwide supply network and the volume of imports from major dairy-producing countries.

By Distribution Channel - Hypermarkets/Supermarkets to dominate the market

Supermarkets and hypermarkets are the main distribution channels as they offer the cold chain infrastructure needed to showcase a large selection of both domestic and imported cheeses. Customers favor these stores as they allow them to shop in one place and the big dairy brands frequently run promotions there.

Key Attractiveness of the Report

- 10 Years of Market Numbers

- Historical Data Starting from 2022 to 2025

- Base Year: 2025

- Forecast Data until 2032

- Key Performance Indicators Impacting the Market

- Major Upcoming Developments and Projects

Key Highlights of the Report:

- Philippines Cheese Market Outlook

- Market Size of Philippines Cheese Market, 2025

- Forecast of Philippines Cheese Market, 2032

- Historical Data and Forecast of Philippines Cheese Revenues & Volume for the Period 2022-2032

- Philippines Cheese Market Trend Evolution

- Philippines Cheese Market Drivers and Challenges

- Philippines Cheese Price Trends

- Philippines Cheese Porter's Five Forces

- Philippines Cheese Industry Life Cycle

- Historical Data and Forecast of Philippines Cheese Market Revenues & Volume By Type for the Period 2022-2032

- Historical Data and Forecast of Philippines Cheese Market Revenues & Volume By Natural for the Period 2022-2032

- Historical Data and Forecast of Philippines Cheese Market Revenues & Volume By Processed for the Period 2022-2032

- Historical Data and Forecast of Philippines Cheese Market Revenues & Volume By Product for the Period 2022-2032

- Historical Data and Forecast of Philippines Cheese Market Revenues & Volume By Mozzarella for the Period 2022-2032

- Historical Data and Forecast of Philippines Cheese Market Revenues & Volume By Cheddar for the Period 2022-2032

- Historical Data and Forecast of Philippines Cheese Market Revenues & Volume By Feta for the Period 2022-2032

- Historical Data and Forecast of Philippines Cheese Market Revenues & Volume By Parmesan for the Period 2022-2032

- Historical Data and Forecast of Philippines Cheese Market Revenues & Volume By Roquefort for the Period 2022-2032

- Historical Data and Forecast of Philippines Cheese Market Revenues & Volume By Others for the Period 2022-2032

- Historical Data and Forecast of Philippines Cheese Market Revenues & Volume By Source for the Period 2022-2032

- Historical Data and Forecast of Philippines Cheese Market Revenues & Volume By Cow Milk for the Period 2022-2032

- Historical Data and Forecast of Philippines Cheese Market Revenues & Volume By Sheep Milk for the Period 2022-2032

- Historical Data and Forecast of Philippines Cheese Market Revenues & Volume By Goat Milk for the Period 2022-2032

- Historical Data and Forecast of Philippines Cheese Market Revenues & Volume By Buffalo for the Period 2022-2032

- Historical Data and Forecast of Philippines Cheese Market Revenues & Volume By Distribution Channel for the Period 2022-2032

- Historical Data and Forecast of Philippines Cheese Market Revenues & Volume By Hypermarkets for the Period 2022-2032

- Historical Data and Forecast of Philippines Cheese Market Revenues & Volume By Supermarkets for the Period 2022-2032

- Historical Data and Forecast of Philippines Cheese Market Revenues & Volume By Food Specialty Stores for the Period 2022-2032

- Historical Data and Forecast of Philippines Cheese Market Revenues & Volume By Convenience Stores for the Period 2022-2032

- Historical Data and Forecast of Philippines Cheese Market Revenues & Volume By Others for the Period 2022-2032

- Philippines Cheese Import Export Trade Statistics

- Market Opportunity Assessment By Type

- Market Opportunity Assessment By Product

- Market Opportunity Assessment By Source

- Market Opportunity Assessment By Distribution Channel

- Philippines Cheese Top Companies Market Share

- Philippines Cheese Competitive Benchmarking By Technical and Operational Parameters

- Philippines Cheese Company Profiles

- Philippines Cheese Key Strategic Recommendations

Market Covered

The report offers a comprehensive study of the following Philippines Cheese Market segments:

By Type

- Natural

- Processed

By Product

- Mozzarella

- Cheddar

- Feta

- Parmesan

- Roquefort

- Others

By Source

- Cow Milk

- Sheep Milk

- Goat Milk

- Buffalo

By Distribution Channel

- Hypermarkets

- Supermarkets

- Food Specialty Stores

- Convenience Stores

- Others

Philippines Cheese Market (2026-2032): FAQs

Philippines Cheese Market is expected to grow at a compound annual growth rate of 5.8% during the forecast period of 2026 to 2032.

Some main factors are the expansion of the fast-food industry, rising disposable incomes, and the growing popularity of international cuisines among the youth.

Major trends are the rise of plant-based cheese alternatives, the popularity of "cheese-heavy" Korean snacks, and an increasing interest in locally produced artisanal goat cheese.

Government incentives like technical training for dairy farmers and programs for livestock distribution help increase local milk supply, which is vital for the sustainable growth of the domestic cheese industry.

6Wresearch actively monitors the Philippines Cheese Market and publishes its comprehensive annual report, highlighting emerging trends, growth drivers, revenue analysis, and forecast outlook. Our insights help businesses to make data-backed strategic decisions with ongoing market dynamics. Our analysts track relevent industries related to the Philippines Cheese Market, allowing our clients with actionable intelligence and reliable forecasts tailored to emerging regional needs.

Yes, we provide customisation as per your requirements. To learn more, feel free to contact us on sales@6wresearch.com

| 1 Executive Summary |

| 2 Introduction |

| 2.1 Key Highlights of the Report |

| 2.2 Report Description |

| 2.3 Market Scope & Segmentation |

| 2.4 Research Methodology |

| 2.5 Assumptions |

| 3 Philippines Cheese Market Overview |

| 3.1 Philippines Country Macro Economic Indicators |

| 3.2 Philippines Cheese Market Revenues & Volume, 2022 & 2032F |

| 3.3 Philippines Cheese Market - Industry Life Cycle |

| 3.4 Philippines Cheese Market - Porter's Five Forces |

| 3.5 Philippines Cheese Market Revenues & Volume Share, By Type, 2022 & 2032F |

| 3.6 Philippines Cheese Market Revenues & Volume Share, By Product, 2022 & 2032F |

| 3.7 Philippines Cheese Market Revenues & Volume Share, By Source, 2022 & 2032F |

| 3.8 Philippines Cheese Market Revenues & Volume Share, By Distribution Channel, 2022 & 2032F |

| 4 Philippines Cheese Market Dynamics |

| 4.1 Impact Analysis |

| 4.2 Market Drivers |

| 4.2.1 Increasing disposable income of consumers in Philippines, leading to higher spending on premium cheese products. |

| 4.2.2 Growing awareness and adoption of Western cuisines in Philippines, driving demand for cheese as a key ingredient. |

| 4.2.3 Expansion of retail chains and supermarkets in urban areas, providing easier access to a variety of cheese products. |

| 4.3 Market Restraints |

| 4.3.1 High import tariffs on cheese products, increasing the final cost to consumers and affecting affordability. |

| 4.3.2 Limited domestic production of cheese in Philippines, leading to reliance on imports and potential supply chain disruptions. |

| 5 Philippines Cheese Market Trends |

| 6 Philippines Cheese Market, By Types |

| 6.1 Philippines Cheese Market, By Type |

| 6.1.1 Overview and Analysis |

| 6.1.2 Philippines Cheese Market Revenues & Volume, By Type, 2022 - 2032F |

| 6.1.3 Philippines Cheese Market Revenues & Volume, By Natural, 2022 - 2032F |

| 6.1.4 Philippines Cheese Market Revenues & Volume, By Processed, 2022 - 2032F |

| 6.2 Philippines Cheese Market, By Product |

| 6.2.1 Overview and Analysis |

| 6.2.2 Philippines Cheese Market Revenues & Volume, By Mozzarella, 2022 - 2032F |

| 6.2.3 Philippines Cheese Market Revenues & Volume, By Cheddar, 2022 - 2032F |

| 6.2.4 Philippines Cheese Market Revenues & Volume, By Feta, 2022 - 2032F |

| 6.2.5 Philippines Cheese Market Revenues & Volume, By Parmesan, 2022 - 2032F |

| 6.2.6 Philippines Cheese Market Revenues & Volume, By Roquefort, 2022 - 2032F |

| 6.2.7 Philippines Cheese Market Revenues & Volume, By Others, 2022 - 2032F |

| 6.3 Philippines Cheese Market, By Source |

| 6.3.1 Overview and Analysis |

| 6.3.2 Philippines Cheese Market Revenues & Volume, By Cow Milk, 2022 - 2032F |

| 6.3.3 Philippines Cheese Market Revenues & Volume, By Sheep Milk, 2022 - 2032F |

| 6.3.4 Philippines Cheese Market Revenues & Volume, By Goat Milk, 2022 - 2032F |

| 6.3.5 Philippines Cheese Market Revenues & Volume, By Buffalo, 2022 - 2032F |

| 6.4 Philippines Cheese Market, By Distribution Channel |

| 6.4.1 Overview and Analysis |

| 6.4.2 Philippines Cheese Market Revenues & Volume, By Hypermarkets, 2022 - 2032F |

| 6.4.3 Philippines Cheese Market Revenues & Volume, By Supermarkets, 2022 - 2032F |

| 6.4.4 Philippines Cheese Market Revenues & Volume, By Food Specialty Stores, 2022 - 2032F |

| 6.4.5 Philippines Cheese Market Revenues & Volume, By Convenience Stores, 2022 - 2032F |

| 6.4.6 Philippines Cheese Market Revenues & Volume, By Others, 2022 - 2032F |

| 7 Philippines Cheese Market Import-Export Trade Statistics |

| 7.1 Philippines Cheese Market Export to Major Countries |

| 7.2 Philippines Cheese Market Imports from Major Countries |

| 8 Philippines Cheese Market Key Performance Indicators |

| 8.1 Consumer preference for different types of cheese (e.g., mozzarella, cheddar, parmesan) in the Philippines market. |

| 8.2 Growth in the number of specialty cheese stores and sections within supermarkets. |

| 8.3 Frequency of cheese-related promotions and marketing campaigns by retailers and brands in Philippines. |

| 9 Philippines Cheese Market - Opportunity Assessment |

| 9.1 Philippines Cheese Market Opportunity Assessment, By Type, 2022 & 2032F |

| 9.2 Philippines Cheese Market Opportunity Assessment, By Product, 2022 & 2032F |

| 9.3 Philippines Cheese Market Opportunity Assessment, By Source, 2022 & 2032F |

| 9.4 Philippines Cheese Market Opportunity Assessment, By Distribution Channel, 2022 & 2032F |

| 10 Philippines Cheese Market - Competitive Landscape |

| 10.1 Philippines Cheese Market Revenue Share, By Companies, 2025 |

| 10.2 Philippines Cheese Market Competitive Benchmarking, By Operating and Technical Parameters |

| 11 Company Profiles |

| 12 Recommendations |

| 13 Disclaimer |

Global Go To Market Strategy - 2030

Export potential enables firms to identify high-growth global markets with greater confidence by combining advanced trade intelligence with a structured quantitative methodology. The framework analyzes emerging demand trends and country-level import patterns while integrating macroeconomic and trade datasets such as GDP and population forecasts, bilateral import–export flows, tariff structures, elasticity differentials between developed and developing economies, geographic distance, and import demand projections. Using weighted trade values from 2020–2024 as the base period to project country-to-country export potential for 2030, these inputs are operationalized through calculated drivers such as gravity model parameters, tariff impact factors, and projected GDP per-capita growth. Through an analysis of hidden potentials, demand hotspots, and market conditions that are most favorable to success, this method enables firms to focus on target countries, maximize returns, and global expansion with data, backed by accuracy.

By factoring in the projected importer demand gap that is currently unmet and could be potential opportunity, it identifies the potential for the Exporter (Country) among 190 countries, against the general trade analysis, which identifies the biggest importer or exporter.

To discover high-growth global markets and optimize your business strategy:

Click Here

Pricing

- Single User License$ 1,995

- Department License$ 2,400

- Site License$ 3,120

- Global License$ 3,795

Leadership Perspectives from Industry Events

Search

Thought Leadership and Analyst Meet

Our Clients

6WResearch In News

- India Export Attractiveness Tracker 2026

- India Air Conditioner Market Set for Strong Rebound in 2026 After Weather-Led Correction and GST-Driven Recovery: 6Wresearch

- ADAS in India: How Automatic Emergency Braking, Blind Spot Detection & Driver Monitoring are Transforming Road Safety

- Doha a strategic location for EV manufacturing hub: IPA Qatar

- Demand for luxury TVs surging in the GCC, says Samsung

- Empowering Growth: The Thriving Journey of Bangladesh’s Cable Industry

Latest Reports

- Nicaragua RPG Gaming Market (2026-2032)

- New Zealand RPG Gaming Market (2026-2032)

- Netherlands RPG Gaming Market (2026-2032)

- Nauru RPG Gaming Market (2026-2032)

- Namibia RPG Gaming Market (2026-2032)

- Mozambique RPG Gaming Market (2026-2032)

- Montenegro RPG Gaming Market (2026-2032)

- Mongolia RPG Gaming Market (2026-2032)

- Monaco RPG Gaming Market (2026-2032)

- Micronesia RPG Gaming Market (2026-2032)

Industry Events and Analyst Meet

EV India Expo 2026

HIMTEX 2026

India Refining Summit 2026

India EV Show 2026

EV tech India Expo 2026

Whitepaper

- Middle East & Africa Commercial Security Market Click here to view more.

- Middle East & Africa Fire Safety Systems & Equipment Market Click here to view more.

- GCC Drone Market Click here to view more.

- Middle East Lighting Fixture Market Click here to view more.

- GCC Physical & Perimeter Security Market Click here to view more.