Saudi Arabia Meat Substitutes Market (2026-2032) | Value, Share, Industry, Growth, Companies, Analysis, Trends, Size, Forecast & Revenue

Market Forecast By Product (Tofu, Tempeh, Textured Vegetable Protein, Seitan, Quorn , Other Product), By Source (Soy Protein, Wheat Protein, Pea Protein , Other Sources), By Types ( Concentrates, Isolates , Textured), By Form (Solid, Liquid) And Competitive Landscape

| Product Code: ETC4549300 | Publication Date: Jul 2023 | Updated Date: Nov 2025 | Product Type: Report | |

| Publisher: 6Wresearch | Author: Ravi Bhandari | No. of Pages: 85 | No. of Figures: 45 | No. of Tables: 25 |

Saudi Arabia Meat Substitutes Market Growth Rate

According to 6Wresearch internal database and industry insights,

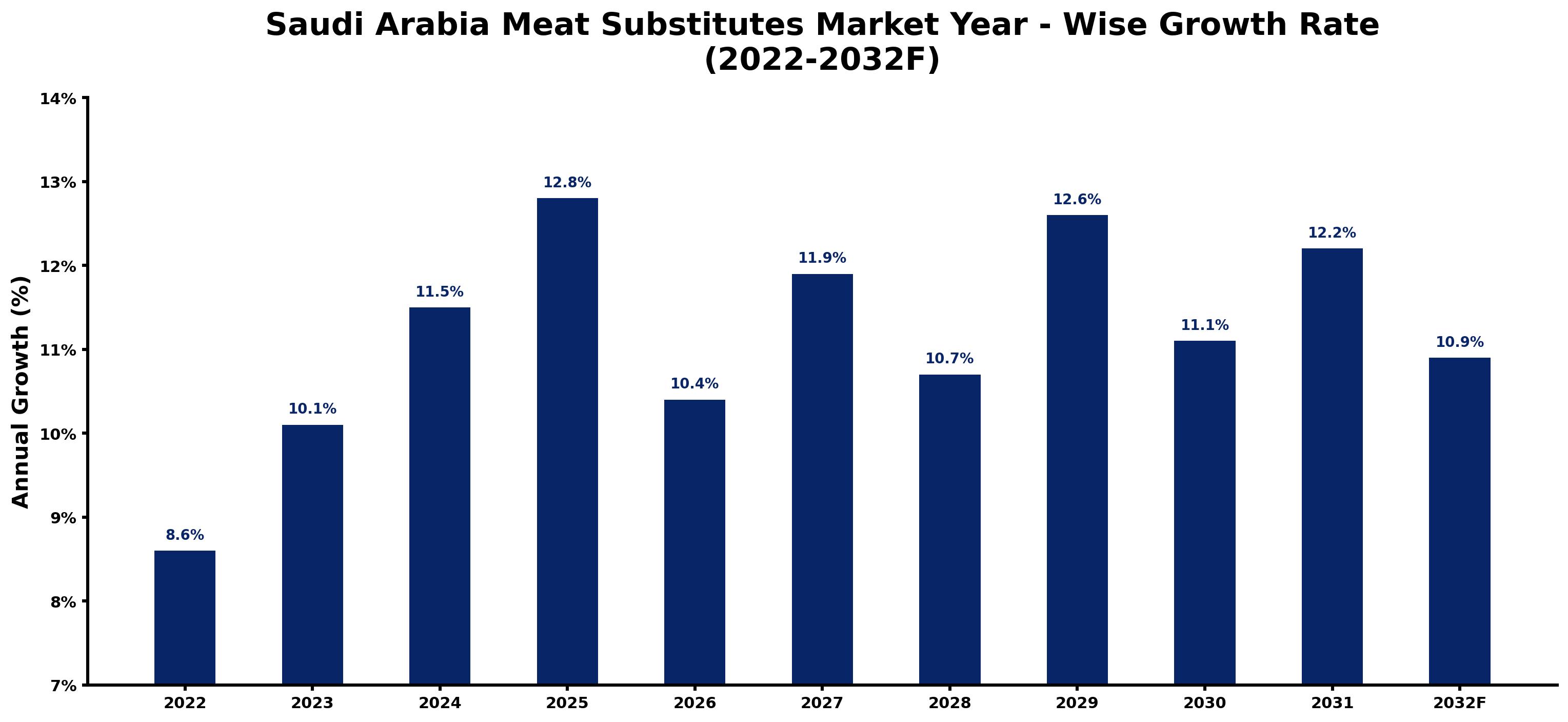

Saudi Arabia Meat Substitutes Market Year-wise Growth Rate and Key Drivers

This graph illustrates the annual growth rates of the Saudi Arabia Meat Substitutes Market from 2022 to 2032, highlighting stable industrial expansion, infrastructure-driven demand, and increasing adoption of precision finishing solutions.

The following table summarizes the historical and forecasted growth rates of the Saudi Arabia Meat Substitutes Market, along with the rationale behind each year’s performance.

| Year | Estimated Growth | Growth Drivers |

| 2022 | 8.6% | Growing awareness of plant-based nutrition, increased availability in premium supermarkets, and rising health-conscious consumer demand supported market expansion. |

| 2023 | 10.1% | International brands expanded their presence, while online grocery platforms and modern retail channels improved product accessibility across major cities. |

| 2024 | 11.5% | Rapid introduction of localized plant-based meat products, increasing foodservice adoption, and stronger marketing campaigns accelerated demand. |

| 2025 | 12.8% | Significant expansion by quick-service restaurants, higher disposable incomes, and broader product portfolios drove exceptional market growth. |

| 2026 | 10.4% | Inflationary pressures and premium product pricing moderated consumer spending despite continued retail expansion. |

| 2027 | 11.9% | Recovery in consumer purchasing power and increasing investments in alternative protein manufacturing strengthened market demand. |

| 2028 | 10.7% | Growth softened due to intensified competition from conventional meat and private-label products, while awareness continued to improve. |

| 2029 | 12.6% | Expansion into secondary cities, increasing institutional demand, and wider availability through hypermarkets boosted market performance. |

| 2030 | 11.1% | Product innovation in hybrid proteins and improved affordability maintained healthy market expansion despite gradual market maturation. |

| 2031 | 12.2% | Government sustainability initiatives, local manufacturing investments, and higher foodservice penetration accelerated market growth. |

| 2032 | 10.9% | Market maturity and price competition slightly moderated annual growth, although demand remained strong due to expanding consumer acceptance. |

Topics Covered in the Saudi Arabia Meat Substitutes Market Report

The Saudi Arabia Meat Substitutes Market report thoroughly covers the market by product, source, types and form. The report provides an unbiased and detailed analysis of ongoing market trends, opportunities/high-growth areas, and market drivers that will help stakeholders devise and align strategies according to current and future market dynamics.

Saudi Arabia Meat Substitutes Market Highlights

| Report Name | Saudi Arabia Meat Substitutes Market |

| Forecast period | 2026-2032 |

| CAGR | 11.4% |

| Growing Sector | Food & Beverage |

Saudi Arabia Meat Substitutes Market Synopsis

The Saudi Arabia Meat Substitutes Industry is witnessing a massive growth, driven by various factors, such as wellness-centric households and premium modern trade expansion. The localization of plant-based formats to traditional recipes (shish kebab, kofta, shawarma) is another major factor estimated to boost the growth of the market. Additionally, the meat substitute demand is on the rise due to the rapid expansion of modern retail and e‑commerce outlets is making plant‑based products more accessible.

Evaluation of Growth Drivers in the Saudi Arabia Meat Substitutes Market

Below mentioned are some prominent drivers and their influence on the Saudi Arabia Meat Substitutes Market dynamics:

| Drivers | Primary Segments Affected | Why it Matters (Evidence) |

| Health & Wellness Shift | Product; Source | Higher protein, lower fat and sodium attract fitness-conscious consumers. |

| Halal Assurance & Certification | Product; Form | Trusted halal certification builds confidence for global plant-based brands. |

| Retail & QSR Partnerships | Product; Types | Menu and private labels propel awareness, trial, and make them purchase again. |

| Localization of Flavors & Formats | Product | Arab-spiced patties, kofta, and shawarma strips boost relevance and usage. |

| Cold-chain & E-commerce Reach | Form | Strong logistics sustain product quality and broader availability. |

The Saudi Arabia Meat Substitutes Market is expected to grow steadily at a 11.4% CAGR between 2026 and 2032. The upward trajectory of the market is credited to expanding halal-certified assortments, strategic QSR tie-ups, and premium retail placement that normalize plant-based choices. Along with that, investments in recipe localization, protein fortification, and cleaner labels reinforce household penetration, while better price packs and promotions enhance affordability. Additionally, culinary education through influencer chefs and retailer demos is forming a new, sustained category adoption. Rising youth preference for sustainable diets and growing food-tech collaborations further strengthen market growth and innovation potential in Saudi Arabia.

Evaluation of Restraints in the Saudi Arabia Meat Substitutes Market

Below mentioned are some major restraints and their influence on the Saudi Arabia Meat Substitutes Market dynamics:

| Restraints | Primary Segments Affected | What this Means (Evidence) |

| Price Premium vs. Meat | Product; Types | Higher prices than conventional meat limit mass adoption; require affordable value packs. |

| Taste & Texture Expectations | Product | Sensory gaps versus fresh meat demand better formulations and chef-led education. |

| Cold-chain Dependence | Form | Breaks in frozen or chilled logistics put quality and customer dissatisfaction in a compromising position. |

| Label Clarity (Allergens/Protein) | Source | Transparency on soy/gluten and protein content is important for trust and compliance. |

| Limited Local Manufacturing | Types | Huge dependency on imports, increases costs and slows innovation cycles. |

Saudi Arabia Meat Substitutes Market Challenges

While the market is developing, challenges include narrowing the taste–texture gap, optimizing pricing to reduce premiums, and strengthening frozen distribution in secondary cities. Additionally, educating consumers, making sure of allergen clarity, and developing local co-manufacturing remain essential for repeat purchases. Furthermore, continued cold-chain investment and consistent marketing will help in gaining trust, accessibility, and long-term category growth in Saudi Arabia.

Saudi Arabia Meat Substitutes Market Trends

Several significant trends are impacting the Saudi Arabia Meat Substitutes Market

- High-Protein, Clean-Label Claims: Shorter labels with pea/soy proteins and reduced sodium attract gym and family buyers.

- Culinary Localization: Shawarma strips, kofta mince, and kebab skewers designed for regional cuisines drive everyday usage.

- Halal-Certified International Brands: Strong halal assurance and recognizable global names build trust and trial.

- Private Label & Value Packs: Retailer-owned brands and family packs lower entry price points and expand reach.

- Hybrid Blends & Functional Nutrition: Vegetable-forward blends with added fiber/omega fortification improve nutrition and acceptance.

Investment Opportunities in the Saudi Arabia Meat Substitutes Industry

Some of the notable investment opportunities are:

- Local Co-manufacturing & Co-packing: JV facilities for halal-certified patties, mince, and TVP to cut costs and speed innovation.

- Culinary R&D & Flavor Houses: Regional spice systems and fat-encapsulation tech to close sensory gaps.

- Cold-chain & Quick-commerce Enablement: Freezer capacity, route optimization, and dark-store partnerships for superior availability.

- HORECA Partnerships: Menu development with QSRs, cafés, and hotels for plant-based shawarma, burgers, and breakfast lines.

Top 5 Leading Players in the Saudi Arabia Meat Substitutes Market

Below is the list of prominent companies leading in the Saudi Arabia Meat Substitutes Market Share:

1. Quorn Foods

| Company Name | Quorn Foods |

| Established Year | 1985 |

| Headquarters |

Stokesley, United Kingdom |

| Official Website | Click Here |

Mycoprotein-based range (mince, fillets, nuggets) with halal-certified SKUs in GCC; strong culinary support and retail partnerships.

2. Beyond Meat (Saudi Distribution)

| Company Name | Beyond Meat (Saudi Distribution) |

| Established Year | 2009 |

| Headquarters |

El Segundo, California, USA |

| Official Website | Click Here |

Plant-based burgers, mince, and sausages distributed via modern trade and HORECA; focuses on high-protein, clean-label profiles.

3. IFFCO THRYVE Plant-Based

| Company Name | IFFCO THRYVE Plant-Based |

| Established Year | 1975 (Group legacy) |

| Headquarters |

Dubai, UAE |

| Official Website | Click Here |

Regional plant-based portfolio (patties, kofta, kebab) tailored for Middle Eastern flavors; halal-certified and expanding in KSA retail.

4. Al Islami Foods (Plant-Based Range)

| Company Name | Al Islami Foods (Plant-Based Range) |

| Established Year | 1981 |

| Headquarters |

Dubai, UAE |

| Official Website | Click Here |

Halal plant-based nuggets and patties; strong freezer presence in GCC hypermarkets with value-pack strategy.

5. Nestlé (Harvest Gourmet)

| Company Name | Nestlé (Harvest Gourmet) |

| Established Year | 1866 (Global legacy) |

| Headquarters |

Vevey, Switzerland |

| Official Website | Click Here |

Harvest Gourmet patties, mince, and schnitzel formats; leverages regional culinary R&D and retailer activations in KSA.

Government Regulations Introduced in the Saudi Arabia Meat Substitutes Market

According to Saudi government data, initiatives such as SFDA nutrition labeling needs, the Saudi Halal Center’s certification frameworks, and the Healthy Food Strategy encouraging reduced salt/fat intake support category credibility. Examples include front-of-pack energy disclosure on packaged foods, halal certification audits for imported plant-based products, school and workplace wellness guidance encouraging healthier menus, and Vision 2030 retail modernization that improves cold-chain infrastructure and product access.

Future Insights of the Saudi Arabia Meat Substitutes Market

The Saudi Arabia Meat Substitutes Industry will sustain its upward growth trajectory as brands localize flavors, expand halal-certified ranges, and scale retail/HORECA penetration. Private labels and co-manufacturing will compress price premiums, while sensory upgrades and chef partnerships foster repeat buying. Digital campaigns, freezer-door execution, and quick-commerce bundles will enhance visibility and frequency across family and youth cohorts, driving continued Saudi Arabia Meat Substitutes Market Growth and long-term consumer engagement.

Market Segmentation Analysis

The report offers a comprehensive study of the subsequent market segments and their leading categories.

By Product – Textured Vegetable Protein to Dominate the Market

According to Vanshika Arora, Senior Research Analyst, 6Wresearch, textured Vegetable Protein (TVP) is expected to dominate Saudi Arabia meat substitutes market size due to its affordability, versatility in local formats (kofta, kebab, keema/ mince), and strong suitability for both retail and foodservice.

By Source – Pea Protein to Lead the Market

Pea protein is projected to lead by source as it aligns with non-soy preferences, clean-label positioning, and allergen-conscious segments, while maintaining good texture in patties, mince, and shawarma strips.

By Types – Textured to Dominate the Market

Textured types are anticipated to dominate given their fibrous bite and culinary flexibility across kebabs, kofta, and shredded shawarma-style applications, enabling close meat mimicry in home and HORECA settings.

By Form – Solid to Dominate the Market

Solid formats (frozen patties, nuggets, mince, fillets, TVP granules) are set to dominate due to freezer-led retail, convenience, and better handling in foodservice. Liquid formats, including ready-to-cook sauces and protein bases for cloud kitchens, are emerging but smaller, used to speed preparation and standardize recipes.

Key attractiveness of the report

- 10 Years Market Numbers.

- Historical Data Starting from 2022 to 2025.

- Base Year: 2025

- Forecast Data until 2032.

- Key Performance Indicators Impacting the Market.

- Major Upcoming Developments and Projects.

Key Highlights of the Report:

- Saudi Arabia Meat Substitutes Market Outlook

- Market Size of Saudi Arabia Meat Substitutes Market, 2025

- Forecast of Saudi Arabia Meat Substitutes Market, 2032

- Historical Data and Forecast of Saudi Arabia Meat Substitutes Revenues & Volume for the Period 2022-2032

- Saudi Arabia Meat Substitutes Market Trend Evolution

- Saudi Arabia Meat Substitutes Market Drivers and Challenges

- Saudi Arabia Meat Substitutes Price Trends

- Saudi Arabia Meat Substitutes Porter's Five Forces

- Saudi Arabia Meat Substitutes Industry Life Cycle

- Historical Data and Forecast of Saudi Arabia Meat Substitutes Market Revenues & Volume By Product for the Period 2022-2032

- Historical Data and Forecast of Saudi Arabia Meat Substitutes Market Revenues & Volume By Tofu for the Period 2022-2032

- Historical Data and Forecast of Saudi Arabia Meat Substitutes Market Revenues & Volume By Tempeh for the Period 2022-2032

- Historical Data and Forecast of Saudi Arabia Meat Substitutes Market Revenues & Volume By Textured Vegetable Protein for the Period 2022-2032

- Historical Data and Forecast of Saudi Arabia Meat Substitutes Market Revenues & Volume By Seitan for the Period 2022-2032

- Historical Data and Forecast of Saudi Arabia Meat Substitutes Market Revenues & Volume By Quorn for the Period 2022-2032

- Historical Data and Forecast of Saudi Arabia Meat Substitutes Market Revenues & Volume By Other Product for the Period 2022-2032

- Historical Data and Forecast of Saudi Arabia Meat Substitutes Market Revenues & Volume By Source for the Period 2022-2032

- Historical Data and Forecast of Saudi Arabia Meat Substitutes Market Revenues & Volume By Soy Protein for the Period 2022-2032

- Historical Data and Forecast of Saudi Arabia Meat Substitutes Market Revenues & Volume By Wheat Protein for the Period 2022-2032

- Historical Data and Forecast of Saudi Arabia Meat Substitutes Market Revenues & Volume By Pea Protein for the Period 2022-2032

- Historical Data and Forecast of Saudi Arabia Meat Substitutes Market Revenues & Volume By Other Sources for the Period 2022-2032

- Historical Data and Forecast of Saudi Arabia Meat Substitutes Market Revenues & Volume By Types for the Period 2022-2032

- Historical Data and Forecast of Saudi Arabia Meat Substitutes Market Revenues & Volume By Concentrates for the Period 2022-2032

- Historical Data and Forecast of Saudi Arabia Meat Substitutes Market Revenues & Volume By Isolates for the Period 2022-2032

- Historical Data and Forecast of Saudi Arabia Meat Substitutes Market Revenues & Volume By Textured for the Period 2022-2032

- Historical Data and Forecast of Saudi Arabia Meat Substitutes Market Revenues & Volume By Form for the Period 2022-2032

- Historical Data and Forecast of Saudi Arabia Meat Substitutes Market Revenues & Volume By Solid for the Period 2022-2032

- Historical Data and Forecast of Saudi Arabia Meat Substitutes Market Revenues & Volume By Liquid for the Period 2022-2032

- Saudi Arabia Meat Substitutes Import Export Trade Statistics

- Market Opportunity Assessment By Product

- Market Opportunity Assessment By Source

- Market Opportunity Assessment By Types

- Market Opportunity Assessment By Form

- Saudi Arabia Meat Substitutes Top Companies Market Share

- Saudi Arabia Meat Substitutes Competitive Benchmarking By Technical and Operational Parameters

- Saudi Arabia Meat Substitutes Company Profiles

- Saudi Arabia Meat Substitutes Key Strategic Recommendations

Markets Covered

The Saudi Arabia meat substitutes market provides a detailed analysis of the following market segments:

By Product

- Tofu

- Tempeh

- Textured Vegetable Protein

- Seitan

- Quorn

- Other Product

By Source

- Soy Protein

- Wheat Protein

- Pea Protein

- Other Sources

By Types

- Concentrates

- Isolates

- Textured

By Form

- Solid

- Liquid

Saudi Arabia Meat Substitutes Market (2026-2032): FAQ's

The Saudi Arabia Meat Substitutes Market is projected to grow at a CAGR of 11.4% during the forecast period.

Textured Vegetable Protein (TVP) dominates due to affordability, versatility in kebab/kofta formats, and strong suitability for retail and HORECA.

Pea protein leads, driven by non-soy preferences, allergen considerations, and clean-label positioning with strong texture outcomes.

SFDA nutrition labeling, Saudi Halal Center certification, Healthy Food Strategy, and Vision 2030 retail modernization support quality, access, and consumer confidence.

6Wresearch actively monitors the Saudi Arabia Meat Substitutes Market and publishes its comprehensive annual report, highlighting emerging trends, growth drivers, revenue analysis, and forecast outlook. Our insights help businesses to make data-backed strategic decisions with ongoing market dynamics. Our analysts track relevent industries related to the Saudi Arabia Meat Substitutes Market, allowing our clients with actionable intelligence and reliable forecasts tailored to emerging regional needs.

Yes, we provide customisation as per your requirements. To learn more, feel free to contact us on sales@6wresearch.com

| 1 Executive Summary |

| 2 Introduction |

| 2.1 Key Highlights of the Report |

| 2.2 Report Description |

| 2.3 Market Scope & Segmentation |

| 2.4 Research Methodology |

| 2.5 Assumptions |

| 3 Saudi Arabia Meat Substitutes Market Overview |

| 3.1 Saudi Arabia Country Macro Economic Indicators |

| 3.2 Saudi Arabia Meat Substitutes Market Revenues & Volume, 2022 & 2032F |

| 3.3 Saudi Arabia Meat Substitutes Market - Industry Life Cycle |

| 3.4 Saudi Arabia Meat Substitutes Market - Porter's Five Forces |

| 3.5 Saudi Arabia Meat Substitutes Market Revenues & Volume Share, By Product, 2022 & 2032F |

| 3.6 Saudi Arabia Meat Substitutes Market Revenues & Volume Share, By Source, 2022 & 2032F |

| 3.7 Saudi Arabia Meat Substitutes Market Revenues & Volume Share, By Types, 2022 & 2032F |

| 3.8 Saudi Arabia Meat Substitutes Market Revenues & Volume Share, By Form, 2022 & 2032F |

| 4 Saudi Arabia Meat Substitutes Market Dynamics |

| 4.1 Impact Analysis |

| 4.2 Market Drivers |

| 4.2.1 Increasing health consciousness and dietary preferences towards plant-based diets |

| 4.2.2 Growing concerns over animal welfare and environmental sustainability |

| 4.2.3 Rising disposable income levels and changing lifestyles in Saudi Arabia |

| 4.3 Market Restraints |

| 4.3.1 Cultural and religious preferences for traditional meat-based diets |

| 4.3.2 Lack of awareness and education about meat substitutes |

| 4.3.3 High prices of meat substitute products compared to conventional meat products |

| 5 Saudi Arabia Meat Substitutes Market Trends |

| 6 Saudi Arabia Meat Substitutes Market, By Types |

| 6.1 Saudi Arabia Meat Substitutes Market, By Product |

| 6.1.1 Overview and Analysis |

| 6.1.2 Saudi Arabia Meat Substitutes Market Revenues & Volume, By Product, 2022-2032F |

| 6.1.3 Saudi Arabia Meat Substitutes Market Revenues & Volume, By Tofu, 2022-2032F |

| 6.1.4 Saudi Arabia Meat Substitutes Market Revenues & Volume, By Tempeh, 2022-2032F |

| 6.1.5 Saudi Arabia Meat Substitutes Market Revenues & Volume, By Textured Vegetable Protein, 2022-2032F |

| 6.1.6 Saudi Arabia Meat Substitutes Market Revenues & Volume, By Seitan, 2022-2032F |

| 6.1.7 Saudi Arabia Meat Substitutes Market Revenues & Volume, By Quorn , 2022-2032F |

| 6.1.8 Saudi Arabia Meat Substitutes Market Revenues & Volume, By Other Product, 2022-2032F |

| 6.2 Saudi Arabia Meat Substitutes Market, By Source |

| 6.2.1 Overview and Analysis |

| 6.2.2 Saudi Arabia Meat Substitutes Market Revenues & Volume, By Soy Protein, 2022-2032F |

| 6.2.3 Saudi Arabia Meat Substitutes Market Revenues & Volume, By Wheat Protein, 2022-2032F |

| 6.2.4 Saudi Arabia Meat Substitutes Market Revenues & Volume, By Pea Protein , 2022-2032F |

| 6.2.5 Saudi Arabia Meat Substitutes Market Revenues & Volume, By Other Sources, 2022-2032F |

| 6.3 Saudi Arabia Meat Substitutes Market, By Types |

| 6.3.1 Overview and Analysis |

| 6.3.2 Saudi Arabia Meat Substitutes Market Revenues & Volume, By Concentrates, 2022-2032F |

| 6.3.3 Saudi Arabia Meat Substitutes Market Revenues & Volume, By Isolates , 2022-2032F |

| 6.3.4 Saudi Arabia Meat Substitutes Market Revenues & Volume, By Textured, 2022-2032F |

| 6.4 Saudi Arabia Meat Substitutes Market, By Form |

| 6.4.1 Overview and Analysis |

| 6.4.2 Saudi Arabia Meat Substitutes Market Revenues & Volume, By Solid, 2022-2032F |

| 6.4.3 Saudi Arabia Meat Substitutes Market Revenues & Volume, By Liquid, 2022-2032F |

| 7 Saudi Arabia Meat Substitutes Market Import-Export Trade Statistics |

| 7.1 Saudi Arabia Meat Substitutes Market Export to Major Countries |

| 7.2 Saudi Arabia Meat Substitutes Market Imports from Major Countries |

| 8 Saudi Arabia Meat Substitutes Market Key Performance Indicators |

| 8.1 Consumer interest and engagement with meat substitute products through social media interactions |

| 8.2 Number of new product launches and innovations in the meat substitutes market |

| 8.3 Adoption rate of meat substitutes by restaurants and foodservice providers in Saudi Arabia |

| 9 Saudi Arabia Meat Substitutes Market - Opportunity Assessment |

| 9.1 Saudi Arabia Meat Substitutes Market Opportunity Assessment, By Product, 2022 & 2032F |

| 9.2 Saudi Arabia Meat Substitutes Market Opportunity Assessment, By Source, 2022 & 2032F |

| 9.3 Saudi Arabia Meat Substitutes Market Opportunity Assessment, By Types, 2022 & 2032F |

| 9.4 Saudi Arabia Meat Substitutes Market Opportunity Assessment, By Form, 2022 & 2032F |

| 10 Saudi Arabia Meat Substitutes Market - Competitive Landscape |

| 10.1 Saudi Arabia Meat Substitutes Market Revenue Share, By Companies, 2025 |

| 10.2 Saudi Arabia Meat Substitutes Market Competitive Benchmarking, By Operating and Technical Parameters |

| 11 Company Profiles |

| 12 Recommendations |

| 13 Disclaimer |

Global Go To Market Strategy - 2030

Export potential enables firms to identify high-growth global markets with greater confidence by combining advanced trade intelligence with a structured quantitative methodology. The framework analyzes emerging demand trends and country-level import patterns while integrating macroeconomic and trade datasets such as GDP and population forecasts, bilateral import–export flows, tariff structures, elasticity differentials between developed and developing economies, geographic distance, and import demand projections. Using weighted trade values from 2020–2024 as the base period to project country-to-country export potential for 2030, these inputs are operationalized through calculated drivers such as gravity model parameters, tariff impact factors, and projected GDP per-capita growth. Through an analysis of hidden potentials, demand hotspots, and market conditions that are most favorable to success, this method enables firms to focus on target countries, maximize returns, and global expansion with data, backed by accuracy.

By factoring in the projected importer demand gap that is currently unmet and could be potential opportunity, it identifies the potential for the Exporter (Country) among 190 countries, against the general trade analysis, which identifies the biggest importer or exporter.

To discover high-growth global markets and optimize your business strategy:

Click Here

Pricing

- Single User License$ 1,995

- Department License$ 2,400

- Site License$ 3,120

- Global License$ 3,795

Leadership Perspectives from Industry Events

Search

Thought Leadership and Analyst Meet

Our Clients

6WResearch In News

- India Export Attractiveness Tracker 2026

- India Air Conditioner Market Set for Strong Rebound in 2026 After Weather-Led Correction and GST-Driven Recovery: 6Wresearch

- ADAS in India: How Automatic Emergency Braking, Blind Spot Detection & Driver Monitoring are Transforming Road Safety

- Doha a strategic location for EV manufacturing hub: IPA Qatar

- Demand for luxury TVs surging in the GCC, says Samsung

- Empowering Growth: The Thriving Journey of Bangladesh’s Cable Industry

Latest Reports

- Nicaragua RPG Gaming Market (2026-2032)

- New Zealand RPG Gaming Market (2026-2032)

- Netherlands RPG Gaming Market (2026-2032)

- Nauru RPG Gaming Market (2026-2032)

- Namibia RPG Gaming Market (2026-2032)

- Mozambique RPG Gaming Market (2026-2032)

- Montenegro RPG Gaming Market (2026-2032)

- Mongolia RPG Gaming Market (2026-2032)

- Monaco RPG Gaming Market (2026-2032)

- Micronesia RPG Gaming Market (2026-2032)

Industry Events and Analyst Meet

EV India Expo 2026

HIMTEX 2026

India Refining Summit 2026

India EV Show 2026

EV tech India Expo 2026

Whitepaper

- Middle East & Africa Commercial Security Market Click here to view more.

- Middle East & Africa Fire Safety Systems & Equipment Market Click here to view more.

- GCC Drone Market Click here to view more.

- Middle East Lighting Fixture Market Click here to view more.

- GCC Physical & Perimeter Security Market Click here to view more.