Singapore Lead Market (2024-2030) | Trends, Industry, Growth, Analysis, Companies, Forecast, Outlook, Size, Revenue, Value & Share

Market Forecast By Isotopes (Lead-204, Lead-207, Lead-206, Lead-208), By Applications (Batteries, Cable sheaths, Shipbuilding, Light industry, Others), By End-users (Mechanical Industry, Construction Industry, Defense, Electronics, Others) And Competitive Landscape

| Product Code: ETC009047 | Publication Date: Jul 2023 | Updated Date: Feb 2026 | Product Type: Report | |

| Publisher: 6Wresearch | Author: Ravi Bhandari | No. of Pages: 70 | No. of Figures: 35 | No. of Tables: 5 |

Singapore Lead Market: Import Trend Analysis

Singapore`s import trend in the lead market exhibited significant growth from 2023 to 2024, with a remarkable increase of 351.15%. The compound annual growth rate (CAGR) for the period 2020-2024 stood at 2.86%. This surge in import momentum can be attributed to evolving demand dynamics or shifts in trade policies during this period.

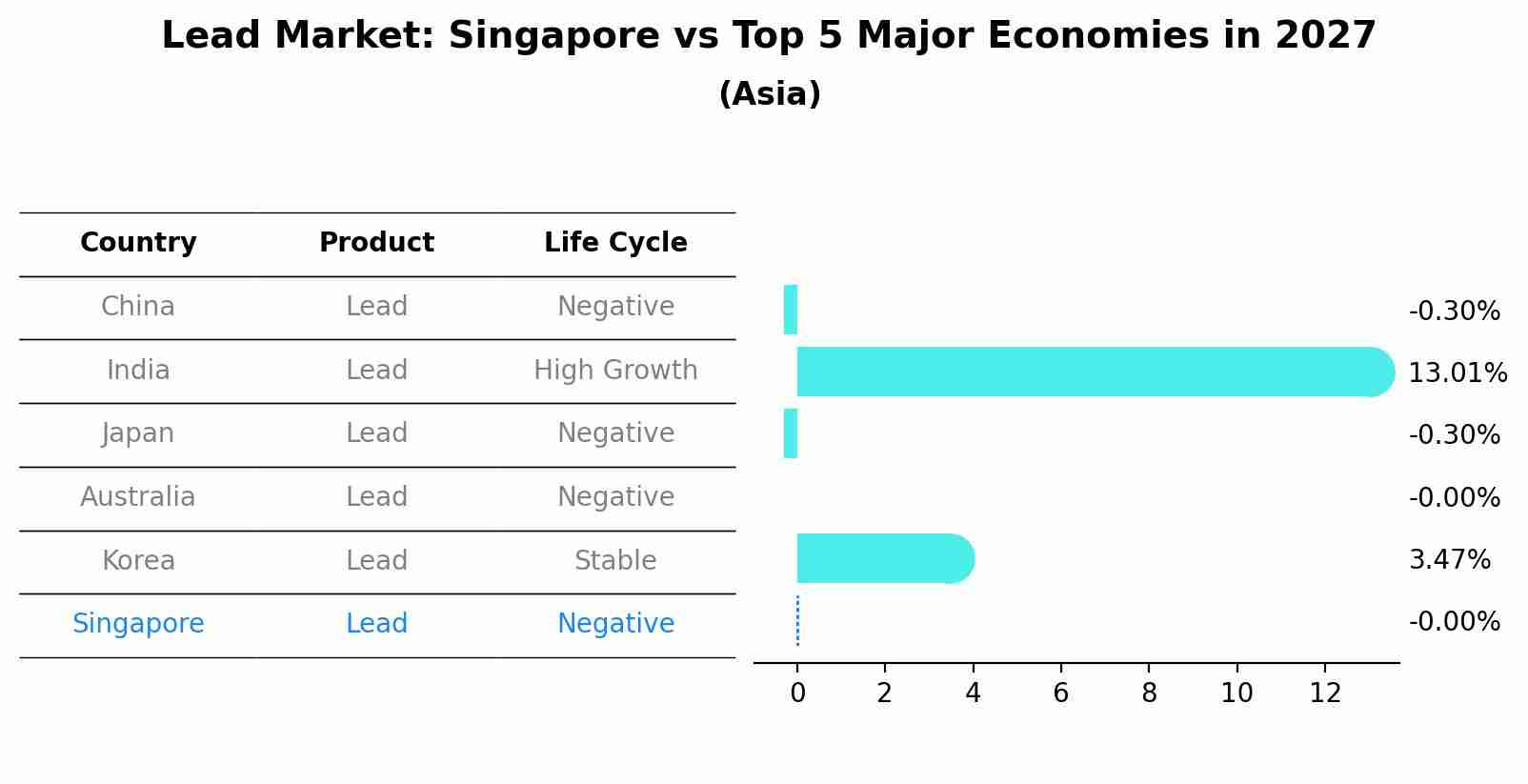

Lead Market: Singapore vs Top 5 Major Economies in 2027 (Asia)

By 2027, the Lead market in Singapore is anticipated to reach a growth rate of -0.00%, as part of an increasingly competitive Asia region, where China remains at the forefront, supported by India, Japan, Australia and South Korea, driving innovations and market adoption across sectors.

Singapore Lead Market Synopsis

Singapore is an attractive market for lead, as it has a booming economy and is a major financial hub in the region. The Singapore government has also taken significant steps to promote sustainability and green initiatives, leading to increased demand for recycled lead from various industries. Additionally, it boasts of strong infrastructure that supports the efficient transportation of lead around the country.

Market Drivers

The main driver behind increasing lead production in Singapore is its robust economic growth over the past few years which has bolstered industrial activity across many sectors including energy, transport and metalworking. In addition to this, there are numerous incentives offered by the government such as tax exemptions or subsidies on purchasing equipment used in manufacturing activities which have further boosted local demand for lead products. Furthermore, stringent environmental regulations implemented by authorities have encouraged companies to recycle old materials like lead instead of producing new ones from scratch thus driving up consumption rates in this sector even higher.

Market challenges

Lead contamination can pose serious health risks if not handled correctly so meeting safety standards set out by regulatory bodies can be complicated and costly for producers operating within Singapore borders. Moreover since most of its resources come from overseas suppliers they may face fluctuations in prices depending on global trends affecting supply chains at any given time due to issues like political instability or natural disasters.

Key players

Some key players active within Singapore Lead Market include GMG Corporation Ltd., Umicore Precious Metals Asia Pte Ltd., Yieh Corp Metal One Co Ltd., Primetal Technologies (S) Pte Ltd., Thakur International Pvt Ltd., Hyundai Steel Co; Mitsubishi Materials Corporation; Nippon Steel Corp.; Rio Tinto Minerals; Hitachi Metals America LLC; Guangdong Yuegang Nonferrous Metals Group Co.; China Metallurgical Group Corp.; Jiangxi Copper Company Limited; Jinzhou New Era Nonferrous Metal Products Co.; Wuhan Iron & Steel (Group) Corporation ETC

Covid-19 Impact

Due to restrictions imposed during COVID-19 pandemic global trade has been severely affected resulting in delays or disruption of supplies that could affect production operations negatively going forward until normalcy returns sometime later 2021 onwards.On top of this, closure/reduction hours at retail stores & construction sites also dampen consumer spending power hence putting more strain onto businesses already struggling with thin profit margins.

Key Highlights of the Report:

- Singapore Lead Market Outlook

- Market Size of Singapore Lead Market, 2023

- Forecast of Singapore Lead Market, 2030

- Historical Data and Forecast of Singapore Lead Revenues & Volume for the Period 2020-2030

- Singapore Lead Market Trend Evolution

- Singapore Lead Market Drivers and Challenges

- Singapore Lead Price Trends

- Singapore Lead Porter's Five Forces

- Singapore Lead Industry Life Cycle

- Historical Data and Forecast of Singapore Lead Market Revenues & Volume By Isotopes for the Period 2020-2030

- Historical Data and Forecast of Singapore Lead Market Revenues & Volume By Lead-204 for the Period 2020-2030

- Historical Data and Forecast of Singapore Lead Market Revenues & Volume By Lead-207 for the Period 2020-2030

- Historical Data and Forecast of Singapore Lead Market Revenues & Volume By Lead-206 for the Period 2020-2030

- Historical Data and Forecast of Singapore Lead Market Revenues & Volume By Lead-208 for the Period 2020-2030

- Historical Data and Forecast of Singapore Lead Market Revenues & Volume By Applications for the Period 2020-2030

- Historical Data and Forecast of Singapore Lead Market Revenues & Volume By Batteries for the Period 2020-2030

- Historical Data and Forecast of Singapore Lead Market Revenues & Volume By Cable sheaths for the Period 2020-2030

- Historical Data and Forecast of Singapore Lead Market Revenues & Volume By Shipbuilding for the Period 2020-2030

- Historical Data and Forecast of Singapore Lead Market Revenues & Volume By Light industry for the Period 2020-2030

- Historical Data and Forecast of Singapore Lead Market Revenues & Volume By Others for the Period 2020-2030

- Historical Data and Forecast of Singapore Lead Market Revenues & Volume By End-users for the Period 2020-2030

- Historical Data and Forecast of Singapore Lead Market Revenues & Volume By Mechanical Industry for the Period 2020-2030

- Historical Data and Forecast of Singapore Lead Market Revenues & Volume By Construction Industry for the Period 2020-2030

- Historical Data and Forecast of Singapore Lead Market Revenues & Volume By Defense for the Period 2020-2030

- Historical Data and Forecast of Singapore Lead Market Revenues & Volume By Electronics for the Period 2020-2030

- Historical Data and Forecast of Singapore Lead Market Revenues & Volume By Others for the Period 2020-2030

- Singapore Lead Import Export Trade Statistics

- Market Opportunity Assessment By Isotopes

- Market Opportunity Assessment By Applications

- Market Opportunity Assessment By End-users

- Singapore Lead Top Companies Market Share

- Singapore Lead Competitive Benchmarking By Technical and Operational Parameters

- Singapore Lead Company Profiles

- Singapore Lead Key Strategic Recommendations

Frequently Asked Questions About the Market Study (FAQs):

6Wresearch actively monitors the Singapore Lead Market and publishes its comprehensive annual report, highlighting emerging trends, growth drivers, revenue analysis, and forecast outlook. Our insights help businesses to make data-backed strategic decisions with ongoing market dynamics. Our analysts track relevent industries related to the Singapore Lead Market, allowing our clients with actionable intelligence and reliable forecasts tailored to emerging regional needs.

Yes, we provide customisation as per your requirements. To learn more, feel free to contact us on sales@6wresearch.com

1 Executive Summary |

2 Introduction |

2.1 Key Highlights of the Report |

2.2 Report Description |

2.3 Market Scope & Segmentation |

2.4 Research Methodology |

2.5 Assumptions |

3 Singapore Lead Market Overview |

3.1 Singapore Country Macro Economic Indicators |

3.2 Singapore Lead Market Revenues & Volume, 2020 & 2030F |

3.3 Singapore Lead Market - Industry Life Cycle |

3.4 Singapore Lead Market - Porter's Five Forces |

3.5 Singapore Lead Market Revenues & Volume Share, By Isotopes , 2020 & 2030F |

3.6 Singapore Lead Market Revenues & Volume Share, By Applications, 2020 & 2030F |

3.7 Singapore Lead Market Revenues & Volume Share, By End-users, 2020 & 2030F |

4 Singapore Lead Market Dynamics |

4.1 Impact Analysis |

4.2 Market Drivers |

4.3 Market Restraints |

5 Singapore Lead Market Trends |

6 Singapore Lead Market, By Types |

6.1 Singapore Lead Market, By Isotopes |

6.1.1 Overview and Analysis |

6.1.2 Singapore Lead Market Revenues & Volume, By Isotopes , 2020-2030F |

6.1.3 Singapore Lead Market Revenues & Volume, By Lead-204, 2020-2030F |

6.1.4 Singapore Lead Market Revenues & Volume, By Lead-207, 2020-2030F |

6.1.5 Singapore Lead Market Revenues & Volume, By Lead-206, 2020-2030F |

6.1.6 Singapore Lead Market Revenues & Volume, By Lead-208, 2020-2030F |

6.2 Singapore Lead Market, By Applications |

6.2.1 Overview and Analysis |

6.2.2 Singapore Lead Market Revenues & Volume, By Batteries, 2020-2030F |

6.2.3 Singapore Lead Market Revenues & Volume, By Cable sheaths, 2020-2030F |

6.2.4 Singapore Lead Market Revenues & Volume, By Shipbuilding, 2020-2030F |

6.2.5 Singapore Lead Market Revenues & Volume, By Light industry, 2020-2030F |

6.2.6 Singapore Lead Market Revenues & Volume, By Others, 2020-2030F |

6.3 Singapore Lead Market, By End-users |

6.3.1 Overview and Analysis |

6.3.2 Singapore Lead Market Revenues & Volume, By Mechanical Industry, 2020-2030F |

6.3.3 Singapore Lead Market Revenues & Volume, By Construction Industry, 2020-2030F |

6.3.4 Singapore Lead Market Revenues & Volume, By Defense, 2020-2030F |

6.3.5 Singapore Lead Market Revenues & Volume, By Electronics, 2020-2030F |

6.3.6 Singapore Lead Market Revenues & Volume, By Others, 2020-2030F |

7 Singapore Lead Market Import-Export Trade Statistics |

7.1 Singapore Lead Market Export to Major Countries |

7.2 Singapore Lead Market Imports from Major Countries |

8 Singapore Lead Market Key Performance Indicators |

9 Singapore Lead Market - Opportunity Assessment |

9.1 Singapore Lead Market Opportunity Assessment, By Isotopes , 2020 & 2030F |

9.2 Singapore Lead Market Opportunity Assessment, By Applications, 2020 & 2030F |

9.3 Singapore Lead Market Opportunity Assessment, By End-users, 2020 & 2030F |

10 Singapore Lead Market - Competitive Landscape |

10.1 Singapore Lead Market Revenue Share, By Companies, 2023 |

10.2 Singapore Lead Market Competitive Benchmarking, By Operating and Technical Parameters |

11 Company Profiles |

12 Recommendations |

13 Disclaimer |

Global Go To Market Strategy - 2030

Export potential enables firms to identify high-growth global markets with greater confidence by combining advanced trade intelligence with a structured quantitative methodology. The framework analyzes emerging demand trends and country-level import patterns while integrating macroeconomic and trade datasets such as GDP and population forecasts, bilateral import–export flows, tariff structures, elasticity differentials between developed and developing economies, geographic distance, and import demand projections. Using weighted trade values from 2020–2024 as the base period to project country-to-country export potential for 2030, these inputs are operationalized through calculated drivers such as gravity model parameters, tariff impact factors, and projected GDP per-capita growth. Through an analysis of hidden potentials, demand hotspots, and market conditions that are most favorable to success, this method enables firms to focus on target countries, maximize returns, and global expansion with data, backed by accuracy.

By factoring in the projected importer demand gap that is currently unmet and could be potential opportunity, it identifies the potential for the Exporter (Country) among 190 countries, against the general trade analysis, which identifies the biggest importer or exporter.

To discover high-growth global markets and optimize your business strategy:

Click Here

Pricing

- Single User License$ 1,995

- Department License$ 2,400

- Site License$ 3,120

- Global License$ 3,795

Leadership Perspectives from Industry Events

Search

Thought Leadership and Analyst Meet

Our Clients

6WResearch In News

- India Air Conditioner Market Set for Strong Rebound in 2026 After Weather-Led Correction and GST-Driven Recovery: 6Wresearch

- ADAS in India: How Automatic Emergency Braking, Blind Spot Detection & Driver Monitoring are Transforming Road Safety

- Doha a strategic location for EV manufacturing hub: IPA Qatar

- Demand for luxury TVs surging in the GCC, says Samsung

- Empowering Growth: The Thriving Journey of Bangladesh’s Cable Industry

- Demand for luxury TVs surging in the GCC, says Samsung

Latest Reports

- Poland Fire Protection Systems Market (2026-2032)

- Cape Verde Portable Hand-Thrown Extinguisher Market (2026-2032)

- Canada Portable Hand-Thrown Extinguisher Market (2026-2032)

- Cameroon Portable Hand-Thrown Extinguisher Market (2026-2032)

- Burundi Portable Hand-Thrown Extinguisher Market (2026-2032)

- Burkina Faso Portable Hand-Thrown Extinguisher Market (2026-2032)

- Bulgaria Portable Hand-Thrown Extinguisher Market (2026-2032)

- Brunei Portable Hand-Thrown Extinguisher Market (2026-2032)

- Botswana Portable Hand-Thrown Extinguisher Market (2026-2032)

- Bosnia and Herzegovina Portable Hand-Thrown Extinguisher Market (2026-2032)

Industry Events and Analyst Meet

HIMTEX 2026

India Refining Summit 2026

India EV Show 2026

EV tech India Expo 2026

Auto Tech Asia 2026

Whitepaper

- Middle East & Africa Commercial Security Market Click here to view more.

- Middle East & Africa Fire Safety Systems & Equipment Market Click here to view more.

- GCC Drone Market Click here to view more.

- Middle East Lighting Fixture Market Click here to view more.

- GCC Physical & Perimeter Security Market Click here to view more.