Tanzania Cheese Market (2025 - 2031) | Industry, Growth, Analysis, Companies, Trends, COVID-19 IMPACT, Forecast, Value, Size, Revenue & Share

Market Forecast By Type (Natural, Processed), By Product (Mozzarella, Cheddar, Feta, Parmesan, Roquefort, Others), By Source (Cow Milk, Sheep Milk, Goat Milk, Buffalo), By Distribution Channel (Hypermarkets, Supermarkets, Food Specialty Stores, Convenience Stores, Others) And Competitive Landscape

| Product Code: ETC180314 | Publication Date: Jan 2022 | Updated Date: Aug 2025 | Product Type: Market Research Report | |

| Publisher: 6Wresearch | Author: Shubham Deep | No. of Pages: 70 | No. of Figures: 35 | No. of Tables: 5 |

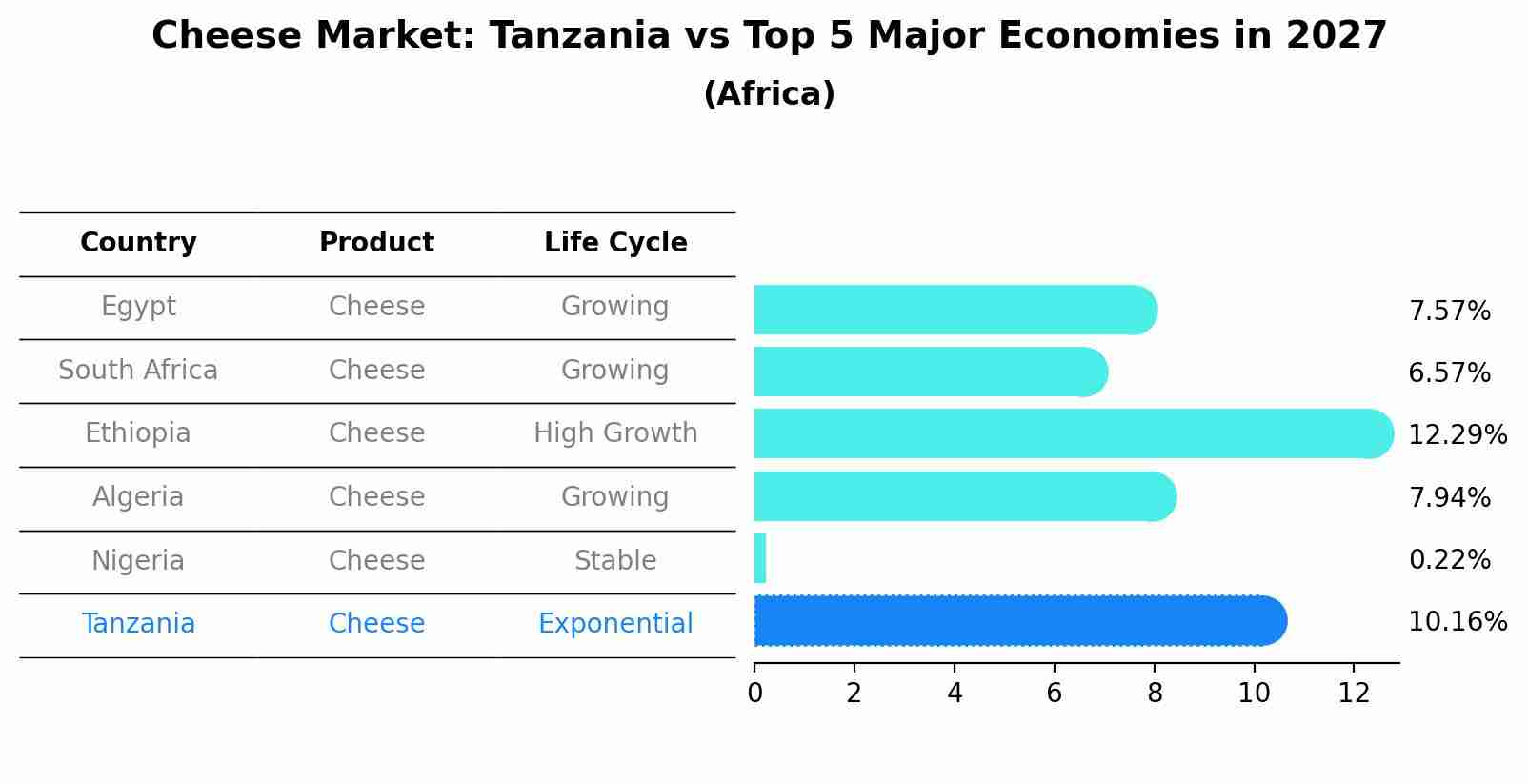

Cheese Market: Tanzania vs Top 5 Major Economies in 2027 (Africa)

By 2027, the Cheese market in Tanzania is anticipated to reach a growth rate of 10.16%, as part of an increasingly competitive Africa region, where Egypt remains at the forefront, supported by South Africa, Ethiopia, Algeria and Nigeria, driving innovations and market adoption across sectors.

Tanzania Cheese Market Overview

The Tanzania cheese market is experiencing steady growth driven by increasing consumer awareness and demand for dairy products. The market is primarily dominated by imported cheeses due to limited local production capacity and technology constraints. However, there is a growing trend towards artisanal and specialty cheeses, as well as an increasing focus on promoting domestic cheese production to reduce reliance on imports. Key players in the market are expanding their product offerings and distribution channels to cater to the evolving consumer preferences. The market is also witnessing a rise in health-conscious consumers opting for organic and natural cheese varieties. Overall, the Tanzania cheese market shows promise for further growth and diversification in the coming years, with opportunities for both local and international cheese producers to capitalize on the market potential.

Tanzania Cheese Market Trends

The Tanzania cheese market is experiencing steady growth, driven by increasing urbanization, rising disposable incomes, and changing consumer preferences towards Western-style cuisine. There is a growing demand for high-quality and diverse cheese products, particularly among the younger population and expatriates. Local dairy companies are expanding their cheese production capabilities and introducing new flavors and varieties to cater to this growing demand. The market is also seeing a rise in the availability of imported cheeses, offering consumers a wider selection to choose from. Health and wellness trends are influencing the market as well, with a preference for natural, organic, and lactose-free cheese options gaining traction among health-conscious consumers. Overall, the Tanzania cheese market is poised for further growth and innovation in the coming years.

Tanzania Cheese Market Challenges

In the Tanzania cheese market, some key challenges include limited awareness and consumption of cheese among the local population, a lack of production infrastructure and technology to meet growing demand, and competition from imported cheeses. Additionally, issues related to distribution and storage facilities, as well as inconsistent quality standards, pose obstacles to market growth. Furthermore, the relatively high cost of cheese compared to other dairy products may hinder widespread adoption, particularly among price-sensitive consumers. Addressing these challenges will require investments in marketing and education to increase cheese consumption, as well as improvements in production capabilities and supply chain efficiency to enhance competitiveness and meet evolving consumer preferences in the Tanzanian market.

Tanzania Cheese Market Investment Opportunities

The Tanzania cheese market presents promising investment opportunities due to increasing urbanization, rising disposable incomes, and changing dietary preferences towards Western foods. There is a growing demand for cheese products among the middle-class population, leading to an expanding market for both domestic and imported cheese varieties. Potential investment avenues include establishing dairy farms for cheese production, setting up cheese processing facilities, or importing high-quality cheese brands to cater to the growing consumer demand. Additionally, investing in marketing strategies to educate consumers about the nutritional benefits and versatility of cheese could further drive market growth. Overall, the Tanzania cheese market offers potential for investors to capitalize on the shifting consumer preferences and increasing demand for cheese products in the region.

Tanzania Cheese Market Government Policy

Government policies related to the Tanzania Cheese Market include regulations on food safety and quality standards enforced by the Tanzania Food and Drugs Authority (TFDA). Import tariffs and trade regulations also impact the market, with the government encouraging domestic production through incentives and tariffs on imported cheese products. Additionally, the government has initiatives to support the dairy industry, such as providing subsidies for dairy farmers and processors to enhance production and distribution capabilities. Overall, the government aims to promote the growth of the Tanzania Cheese Market while ensuring compliance with quality standards and supporting local production and employment opportunities within the dairy sector.

Tanzania Cheese Market Future Outlook

The Tanzania cheese market is poised for steady growth in the coming years, driven by factors such as increasing disposable income, changing dietary preferences, and a growing urban population with a taste for Western cuisine. The rising awareness of the nutritional benefits of cheese, coupled with a burgeoning foodservice industry and expanding retail sector, is expected to boost the demand for various types of cheese products in the country. Furthermore, the increasing investments in dairy farming and processing facilities are likely to improve the quality and availability of cheese products, thereby attracting more consumers. However, challenges such as price sensitivity, supply chain inefficiencies, and competition from other dairy products could impact the market growth to some extent. Overall, the Tanzania cheese market is anticipated to show promising opportunities for both domestic and international cheese manufacturers in the foreseeable future.

Key Highlights of the Report:

- Tanzania Cheese Market Outlook

- Market Size of Tanzania Cheese Market, 2024

- Forecast of Tanzania Cheese Market, 2031

- Historical Data and Forecast of Tanzania Cheese Revenues & Volume for the Period 2021 - 2031

- Tanzania Cheese Market Trend Evolution

- Tanzania Cheese Market Drivers and Challenges

- Tanzania Cheese Price Trends

- Tanzania Cheese Porter's Five Forces

- Tanzania Cheese Industry Life Cycle

- Historical Data and Forecast of Tanzania Cheese Market Revenues & Volume By Type for the Period 2021 - 2031

- Historical Data and Forecast of Tanzania Cheese Market Revenues & Volume By Natural for the Period 2021 - 2031

- Historical Data and Forecast of Tanzania Cheese Market Revenues & Volume By Processed for the Period 2021 - 2031

- Historical Data and Forecast of Tanzania Cheese Market Revenues & Volume By Product for the Period 2021 - 2031

- Historical Data and Forecast of Tanzania Cheese Market Revenues & Volume By Mozzarella for the Period 2021 - 2031

- Historical Data and Forecast of Tanzania Cheese Market Revenues & Volume By Cheddar for the Period 2021 - 2031

- Historical Data and Forecast of Tanzania Cheese Market Revenues & Volume By Feta for the Period 2021 - 2031

- Historical Data and Forecast of Tanzania Cheese Market Revenues & Volume By Parmesan for the Period 2021 - 2031

- Historical Data and Forecast of Tanzania Cheese Market Revenues & Volume By Roquefort for the Period 2021 - 2031

- Historical Data and Forecast of Tanzania Cheese Market Revenues & Volume By Others for the Period 2021 - 2031

- Historical Data and Forecast of Tanzania Cheese Market Revenues & Volume By Source for the Period 2021 - 2031

- Historical Data and Forecast of Tanzania Cheese Market Revenues & Volume By Cow Milk for the Period 2021 - 2031

- Historical Data and Forecast of Tanzania Cheese Market Revenues & Volume By Sheep Milk for the Period 2021 - 2031

- Historical Data and Forecast of Tanzania Cheese Market Revenues & Volume By Goat Milk for the Period 2021 - 2031

- Historical Data and Forecast of Tanzania Cheese Market Revenues & Volume By Buffalo for the Period 2021 - 2031

- Historical Data and Forecast of Tanzania Cheese Market Revenues & Volume By Distribution Channel for the Period 2021 - 2031

- Historical Data and Forecast of Tanzania Cheese Market Revenues & Volume By Hypermarkets for the Period 2021 - 2031

- Historical Data and Forecast of Tanzania Cheese Market Revenues & Volume By Supermarkets for the Period 2021 - 2031

- Historical Data and Forecast of Tanzania Cheese Market Revenues & Volume By Food Specialty Stores for the Period 2021 - 2031

- Historical Data and Forecast of Tanzania Cheese Market Revenues & Volume By Convenience Stores for the Period 2021 - 2031

- Historical Data and Forecast of Tanzania Cheese Market Revenues & Volume By Others for the Period 2021 - 2031

- Tanzania Cheese Import Export Trade Statistics

- Market Opportunity Assessment By Type

- Market Opportunity Assessment By Product

- Market Opportunity Assessment By Source

- Market Opportunity Assessment By Distribution Channel

- Tanzania Cheese Top Companies Market Share

- Tanzania Cheese Competitive Benchmarking By Technical and Operational Parameters

- Tanzania Cheese Company Profiles

- Tanzania Cheese Key Strategic Recommendations

Frequently Asked Questions About the Market Study (FAQs):

6Wresearch actively monitors the Tanzania Cheese Market and publishes its comprehensive annual report, highlighting emerging trends, growth drivers, revenue analysis, and forecast outlook. Our insights help businesses to make data-backed strategic decisions with ongoing market dynamics. Our analysts track relevent industries related to the Tanzania Cheese Market, allowing our clients with actionable intelligence and reliable forecasts tailored to emerging regional needs.

Yes, we provide customisation as per your requirements. To learn more, feel free to contact us on sales@6wresearch.com

1 Executive Summary |

2 Introduction |

2.1 Key Highlights of the Report |

2.2 Report Description |

2.3 Market Scope & Segmentation |

2.4 Research Methodology |

2.5 Assumptions |

3 Tanzania Cheese Market Overview |

3.1 Tanzania Country Macro Economic Indicators |

3.2 Tanzania Cheese Market Revenues & Volume, 2021 & 2031F |

3.3 Tanzania Cheese Market - Industry Life Cycle |

3.4 Tanzania Cheese Market - Porter's Five Forces |

3.5 Tanzania Cheese Market Revenues & Volume Share, By Type, 2021 & 2031F |

3.6 Tanzania Cheese Market Revenues & Volume Share, By Product, 2021 & 2031F |

3.7 Tanzania Cheese Market Revenues & Volume Share, By Source, 2021 & 2031F |

3.8 Tanzania Cheese Market Revenues & Volume Share, By Distribution Channel, 2021 & 2031F |

4 Tanzania Cheese Market Dynamics |

4.1 Impact Analysis |

4.2 Market Drivers |

4.2.1 Increasing disposable income leading to higher purchasing power |

4.2.2 Growing awareness and preference for dairy products |

4.2.3 Expansion of retail channels and distribution networks |

4.2.4 Shift towards westernized dietary habits and increasing demand for convenience foods |

4.3 Market Restraints |

4.3.1 Price volatility of raw materials impacting production costs |

4.3.2 Limited availability of skilled labor in the dairy industry |

4.3.3 Infrastructure challenges affecting transportation and storage of cheese products |

5 Tanzania Cheese Market Trends |

6 Tanzania Cheese Market, By Types |

6.1 Tanzania Cheese Market, By Type |

6.1.1 Overview and Analysis |

6.1.2 Tanzania Cheese Market Revenues & Volume, By Type, 2021 - 2031F |

6.1.3 Tanzania Cheese Market Revenues & Volume, By Natural, 2021 - 2031F |

6.1.4 Tanzania Cheese Market Revenues & Volume, By Processed, 2021 - 2031F |

6.2 Tanzania Cheese Market, By Product |

6.2.1 Overview and Analysis |

6.2.2 Tanzania Cheese Market Revenues & Volume, By Mozzarella, 2021 - 2031F |

6.2.3 Tanzania Cheese Market Revenues & Volume, By Cheddar, 2021 - 2031F |

6.2.4 Tanzania Cheese Market Revenues & Volume, By Feta, 2021 - 2031F |

6.2.5 Tanzania Cheese Market Revenues & Volume, By Parmesan, 2021 - 2031F |

6.2.6 Tanzania Cheese Market Revenues & Volume, By Roquefort, 2021 - 2031F |

6.2.7 Tanzania Cheese Market Revenues & Volume, By Others, 2021 - 2031F |

6.3 Tanzania Cheese Market, By Source |

6.3.1 Overview and Analysis |

6.3.2 Tanzania Cheese Market Revenues & Volume, By Cow Milk, 2021 - 2031F |

6.3.3 Tanzania Cheese Market Revenues & Volume, By Sheep Milk, 2021 - 2031F |

6.3.4 Tanzania Cheese Market Revenues & Volume, By Goat Milk, 2021 - 2031F |

6.3.5 Tanzania Cheese Market Revenues & Volume, By Buffalo, 2021 - 2031F |

6.4 Tanzania Cheese Market, By Distribution Channel |

6.4.1 Overview and Analysis |

6.4.2 Tanzania Cheese Market Revenues & Volume, By Hypermarkets, 2021 - 2031F |

6.4.3 Tanzania Cheese Market Revenues & Volume, By Supermarkets, 2021 - 2031F |

6.4.4 Tanzania Cheese Market Revenues & Volume, By Food Specialty Stores, 2021 - 2031F |

6.4.5 Tanzania Cheese Market Revenues & Volume, By Convenience Stores, 2021 - 2031F |

6.4.6 Tanzania Cheese Market Revenues & Volume, By Others, 2021 - 2031F |

7 Tanzania Cheese Market Import-Export Trade Statistics |

7.1 Tanzania Cheese Market Export to Major Countries |

7.2 Tanzania Cheese Market Imports from Major Countries |

8 Tanzania Cheese Market Key Performance Indicators |

8.1 Consumer preferences and trends in cheese varieties |

8.2 Percentage growth in per capita cheese consumption |

8.3 Number of new product launches and innovations in the cheese market |

8.4 Quality control measures and compliance with food safety regulations |

8.5 Investment in research and development for new cheese products |

9 Tanzania Cheese Market - Opportunity Assessment |

9.1 Tanzania Cheese Market Opportunity Assessment, By Type, 2021 & 2031F |

9.2 Tanzania Cheese Market Opportunity Assessment, By Product, 2021 & 2031F |

9.3 Tanzania Cheese Market Opportunity Assessment, By Source, 2021 & 2031F |

9.4 Tanzania Cheese Market Opportunity Assessment, By Distribution Channel, 2021 & 2031F |

10 Tanzania Cheese Market - Competitive Landscape |

10.1 Tanzania Cheese Market Revenue Share, By Companies, 2024 |

10.2 Tanzania Cheese Market Competitive Benchmarking, By Operating and Technical Parameters |

11 Company Profiles |

12 Recommendations |

13 Disclaimer |

Global Go To Market Strategy - 2030

Export potential enables firms to identify high-growth global markets with greater confidence by combining advanced trade intelligence with a structured quantitative methodology. The framework analyzes emerging demand trends and country-level import patterns while integrating macroeconomic and trade datasets such as GDP and population forecasts, bilateral import–export flows, tariff structures, elasticity differentials between developed and developing economies, geographic distance, and import demand projections. Using weighted trade values from 2020–2024 as the base period to project country-to-country export potential for 2030, these inputs are operationalized through calculated drivers such as gravity model parameters, tariff impact factors, and projected GDP per-capita growth. Through an analysis of hidden potentials, demand hotspots, and market conditions that are most favorable to success, this method enables firms to focus on target countries, maximize returns, and global expansion with data, backed by accuracy.

By factoring in the projected importer demand gap that is currently unmet and could be potential opportunity, it identifies the potential for the Exporter (Country) among 190 countries, against the general trade analysis, which identifies the biggest importer or exporter.

To discover high-growth global markets and optimize your business strategy:

Click Here

Pricing

- Single User License$ 1,995

- Department License$ 2,400

- Site License$ 3,120

- Global License$ 3,795

Leadership Perspectives from Industry Events

Search

Thought Leadership and Analyst Meet

Our Clients

6WResearch In News

- Doha a strategic location for EV manufacturing hub: IPA Qatar

- Demand for luxury TVs surging in the GCC, says Samsung

- Empowering Growth: The Thriving Journey of Bangladesh’s Cable Industry

- Demand for luxury TVs surging in the GCC, says Samsung

- Video call with a traditional healer? Once unthinkable, it’s now common in South Africa

- Intelligent Buildings To Smooth GCC’s Path To Net Zero

Latest Reports

- New Zealand Aseptic Manufacturing Market (2026-2032)

- Netherlands Aseptic Manufacturing Market (2026-2032)

- Nauru Aseptic Manufacturing Market (2026-2032)

- Namibia Aseptic Manufacturing Market (2026-2032)

- Mozambique Aseptic Manufacturing Market (2026-2032)

- Montenegro Aseptic Manufacturing Market (2026-2032)

- Mongolia Aseptic Manufacturing Market (2026-2032)

- Monaco Aseptic Manufacturing Market (2026-2032)

- Micronesia Aseptic Manufacturing Market (2026-2032)

- Mauritius Aseptic Manufacturing Market (2026-2032)

Industry Events and Analyst Meet

HIMTEX 2026

India Refining Summit 2026

India EV Show 2026

EV tech India Expo 2026

Auto Tech Asia 2026

Whitepaper

- Middle East & Africa Commercial Security Market Click here to view more.

- Middle East & Africa Fire Safety Systems & Equipment Market Click here to view more.

- GCC Drone Market Click here to view more.

- Middle East Lighting Fixture Market Click here to view more.

- GCC Physical & Perimeter Security Market Click here to view more.