US Lithography Systems Market (2025-2031) | Outlook, Industry, Revenue, Analysis, Share, Trends, Companies, Size, Growth, Value, Forecast

Market Forecast By Technology (ArF Immersion, KrF, i-line, ArF Dry, EUV), By Application (Foundry, Memory, Integrated Device) And Competitive Landscape

| Product Code: ETC234781 | Publication Date: Aug 2022 | Updated Date: Nov 2025 | Product Type: Market Research Report | |

| Publisher: 6Wresearch | Author: Ravi Bhandari | No. of Pages: 75 | No. of Figures: 35 | No. of Tables: 20 |

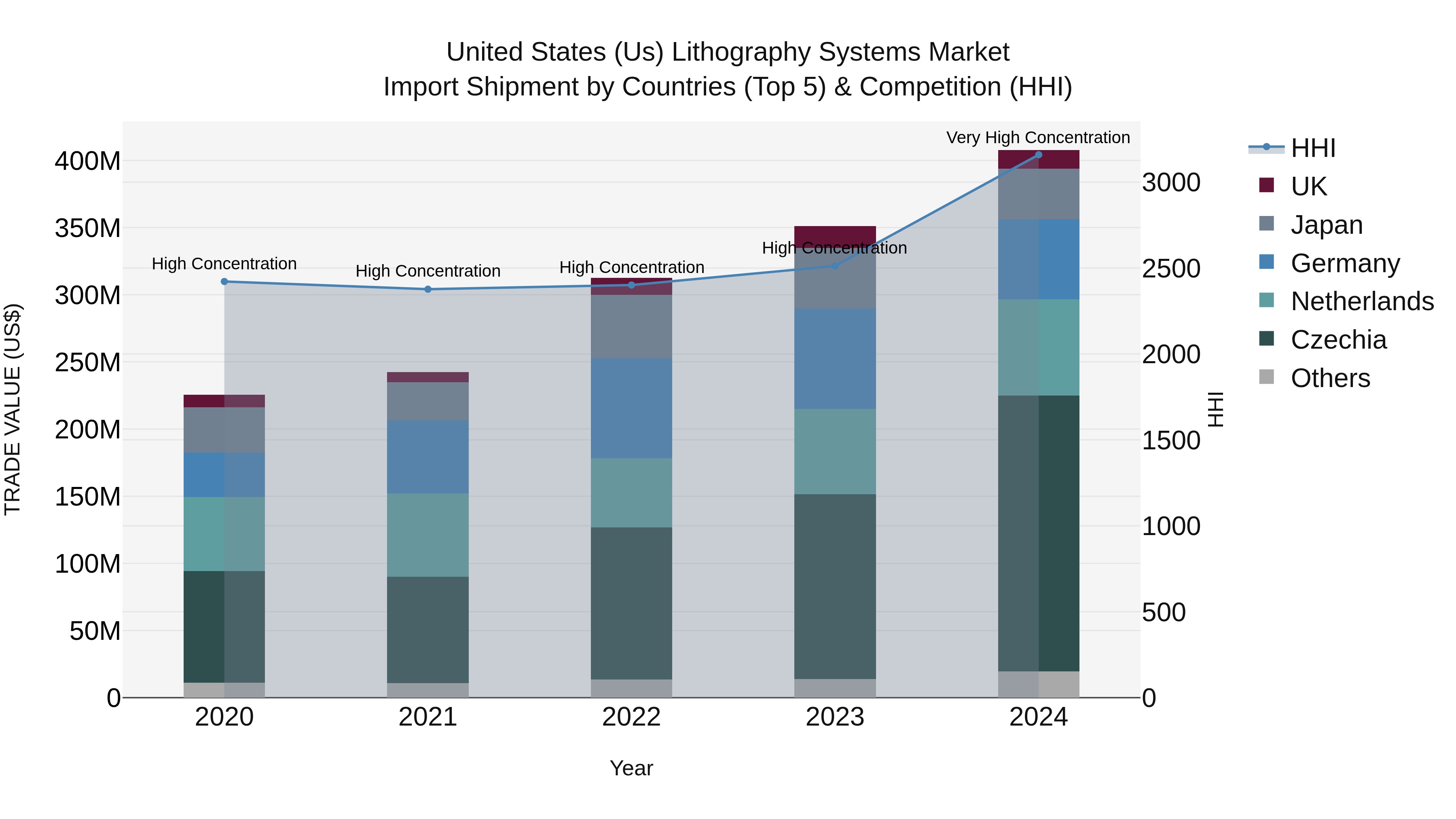

United States (US) Lithography Systems Market Top 5 Importing Countries and Market Competition (HHI) Analysis

The lithography systems import market in the United States experienced significant growth in 2024, with a high concentration of shipments coming from top exporting countries such as Czechia, Netherlands, Germany, Japan, and the UK. The Herfindahl-Hirschman Index (HHI) indicated a shift from high to very high concentration in 2024, reflecting a more consolidated market landscape. The impressive Compound Annual Growth Rate (CAGR) of 15.94% from 2020 to 2024 highlights the increasing demand for lithography systems in the US market. Moreover, the notable growth rate of 16.14% from 2023 to 2024 suggests ongoing momentum and opportunities for market expansion in the near future.

US Lithography Systems Market Highlights

| Report Name | US Lithography Systems Market |

| Forecast period | 2025-2031 |

| CAGR | 7.4% |

| Growing Sector | BFSI |

Topics Covered in the US Lithography Systems Market Report

The US Lithography Systems market report thoroughly covers the market by technology, by application and competitive Landscape. The report provides an unbiased and detailed analysis of the on-going market trends, opportunities/high growth areas, and market drivers which would help the stakeholders to devise and align their market strategies according to the current and future market dynamics.

US Lithography Systems Market Synopsis

The US lithography systems market has witnessed substantial growth due to the rising demand for semiconductor devices. Factors driving this demand include the continuous evolution of consumer electronics, the surge in automation across multiple industries, and the expanding scope of Internet of Things (IoT) applications. Lithography systems, crucial in the fabrication of semiconductors, have thus become key assets in meeting the intricate design and manufacturing requirements of modern electronic components. Additionally, among the emerging trends, the transition towards extreme ultraviolet (EUV) lithography stands out as a significant advancement. EUV lithography enables the production of semiconductors with much smaller feature sizes, crucial for the next generation of microprocessors and memory chips. Additionally, the integration of artificial intelligence (AI) and machine learning (ML) into lithography systems is revolutionizing the manufacturing process. These technological integrations facilitate greater precision, efficiency, and reduced error rates, essential for the highly competitive and fast-paced semiconductor industry. Furthermore, sustainability initiatives are also influencing market trends, with manufacturers increasingly focusing on reducing the environmental impact of lithography processes.

According to 6Wresearch, US Lithography Systems market size is projected to grow at a CAGR of 7.4% during 2025-2031. The growth of the US lithography systems market is primarily fueled by several key factors. Firstly, the relentless innovation and development within the tech industry necessitate the continual upgrade of semiconductor technology, driving the demand for advanced lithography systems. Secondly, the digital transformation of traditional industries has led to an increased need for sophisticated electronic components, further boosting the market. Additionally, the global push towards 5G technology and network infrastructure upgrades represents a significant growth driver, as it requires high-performance semiconductors produced using advanced lithography techniques. Lastly, government policies and investments aimed at bolstering domestic semiconductor manufacturing capacities are poised to further stimulate market growth by providing financial incentives and reducing dependency on foreign technology.

Government Initiatives Introduced in the US Lithography Systems Market

Government initiatives play a pivotal role in shaping the trajectory of the US lithography systems market. In response to global supply chain vulnerabilities exposed by recent events, federal and state governments are enacting policies aimed at strengthening domestic semiconductor production capabilities. Consistently, these actions have boosted the US Lithography Systems Market Share. Additionally, this involves significant investment in research and development programs, tax incentives for semiconductor manufacturing firms, and grants to support the construction of new fabrication plants. Such measures not only aim to invigorate the lithography systems market but also secure the nation's technological sovereignty and economic competitiveness on the global stage.

Key Players in the US Lithography Systems Market

Several key companies dominate the global lithography systems market, including ASML, Nikon, and Canon. ASML, a Dutch company, is renowned for its cutting-edge extreme ultraviolet (EUV) lithography machines, which are crucial for manufacturing the most advanced semiconductor chips. Nikon and Canon, both based in Japan, are also significant players, offering a range of photolithography equipment tailored to different steps of the semiconductor manufacturing process. In addition, the businesses’ grasp massive US Lithography Systems Market Revenues. Further, these companies play a pivotal role in driving technological advancements and competition within the industry, continually pushing the limits of what's possible in chip fabrication technology.

Future Insights of the US Lithography Systems Market

Looking ahead, the US lithography systems market is poised for further innovation and growth. Advances in lithography technology, particularly in extreme ultraviolet (EUV) and deep ultraviolet (DUV) systems, are expected to meet the increasing demands for smaller, more efficient semiconductor chips. The ongoing push towards miniaturization and the integration of semiconductors in a wider array of sectors, from automotive to IoT devices, signals robust future demand. In tandem, environmental sustainability and energy efficiency will become increasingly important, pushing companies to develop eco-friendlier manufacturing processes. Furthermore, as geopolitical tensions continue to influence global trade and technology exchange, securing a resilient and self-sufficient semiconductor supply chain will remain a top priority for the US. This landscape offers both challenges and opportunities for industry players, investors, and policymakers, underscoring the importance of innovation, collaboration, and strategic planning in securing the future of technology and manufacturing.

Market Analysis by Technology

According to Ravi Bhandari, Research Head, 6Wresearch, the semiconductor lithography process utilizes various types of technology, each suited to specific requirements of chip manufacturing. ArF Immersion technology, which uses argon fluoride lasers to create extremely small circuit patterns, is at the forefront for producing advanced semiconductor devices. KrF, or krypton fluoride technology, is utilized for slightly larger feature sizes and offers a balance between performance and cost-effectiveness. I-Line technology, working with a longer wavelength, is often employed for less critical layers where cost efficiency is paramount. Lastly, ArF Dry technology is used for applications where immersion is not feasible, providing a versatile solution for a range of manufacturing contexts. Each of these technologies plays a crucial role in the intricate process of semiconductor fabrication, enabling the production of chips that power the modern, digital world.

Market Analysis by Application

The variety of semiconductor technologies finds application in multiple fields, catering to diverse market needs. Foundries, serving as third-party manufacturers for chip design companies, greatly rely on the latest lithography techniques to produce chips with cutting-edge performance and efficiency. In the memory sector, both volatile RAM and non-volatile memory manufacturers leverage these technologies to increase storage capacity and speed, essential for the vast data requirements of today's digital age. Integrated Device Manufacturers (IDMs), which design, manufacture, and market their own semiconductor products, utilize these lithographic advancements to create more complex and integrated solutions, driving innovation across computing, consumer electronics, networking, and automotive industries.

Key Attractiveness of the Report

- 10 Years Market Numbers.

- Historical Data Starting from 2021 to 2024.

- Base Year: 2024.

- Forecast Data until 2031.

- Key Performance Indicators Impacting the Market.

- Major Upcoming Developments and Projects.

Key Highlights of the Report:

- US Lithography Systems Market Overview

- US Lithography Systems Market Outlook

- US Lithography Systems Market Forecast

- Market Size of US Lithography Systems Market, 2024

- Forecast of US Lithography Systems Market, 2031

- Historical Data and Forecast of US Lithography Systems Revenues & Volume for the Period 2021 - 2031

- US Lithography Systems Market Trend Evolution

- US Lithography Systems Market Drivers and Challenges

- US Lithography Systems Price Trends

- US Lithography Systems Porter's Five Forces

- US Lithography Systems Industry Life Cycle

- Historical Data and Forecast of US Lithography Systems Market Revenues & Volume By Technology for the Period 2021 - 2031

- Historical Data and Forecast of US Lithography Systems Market Revenues & Volume By ArF Immersion for the Period 2021 - 2031

- Historical Data and Forecast of US Lithography Systems Market Revenues & Volume By KrF for the Period 2021 - 2031

- Historical Data and Forecast of US Lithography Systems Market Revenues & Volume By i-line for the Period 2021 - 2031

- Historical Data and Forecast of US Lithography Systems Market Revenues & Volume By ArF Dry for the Period 2021 - 2031

- Historical Data and Forecast of US Lithography Systems Market Revenues & Volume By EUV for the Period 2021 - 2031

- Historical Data and Forecast of US Lithography Systems Market Revenues & Volume By Application for the Period 2021 - 2031

- Historical Data and Forecast of US Lithography Systems Market Revenues & Volume By Foundry for the Period 2021 - 2031

- Historical Data and Forecast of US Lithography Systems Market Revenues & Volume By Memory for the Period 2021 - 2031

- Historical Data and Forecast of US Lithography Systems Market Revenues & Volume, By Integrated Device for the Period 2021 - 2031

- US Lithography Systems Import Export Trade Statistics

- Market Opportunity Assessment, By Technology

- Market Opportunity Assessment, By Application

- US Lithography Systems Top Companies Market Share

- US Lithography Systems Competitive Benchmarking, By Technical and Operational Parameters

- US Lithography Systems Company Profiles

- US Lithography Systems Key Strategic Recommendations

Markets Covered

The US Lithography Systems market report provides a detailed analysis of the following market segments:

By Technology

- ArF Immersion

- KrF

- I-Line

- ArF Dry

- EUV

By Application

- Foundry

- Memory

- Integrated Device

US Lithography Systems Market (2025-2031): FAQs

The market growth is driven by the relentless innovation and development within the tech industry necessitate the continual upgrade of semiconductor technology.

The ArF Immersion technology is expected to register enormous growth over the years.

The integrated device application holds the highest market share.

ASML, Nikon, and Canon are some of the prominent players in the US Lithography Systems market.

6Wresearch actively monitors the US Lithography Systems Market and publishes its comprehensive annual report, highlighting emerging trends, growth drivers, revenue analysis, and forecast outlook. Our insights help businesses to make data-backed strategic decisions with ongoing market dynamics. Our analysts track relevent industries related to the US Lithography Systems Market, allowing our clients with actionable intelligence and reliable forecasts tailored to emerging regional needs.

Yes, we provide customisation as per your requirements. To learn more, feel free to contact us on sales@6wresearch.com

| 1 Executive Summary |

| 2 Introduction |

| 2.1 Key Highlights of the Report |

| 2.2 Report Description |

| 2.3 Market Scope & Segmentation |

| 2.4 Research Methodology |

| 2.5 Assumptions |

| 3 US Lithography Systems Market Overview |

| 3.1 US Country Macro Economic Indicators |

| 3.2 US Lithography Systems Market Revenues & Volume, 2021 & 2031F |

| 3.3 US Lithography Systems Market - Industry Life Cycle |

| 3.4 US Lithography Systems Market - Porter's Five Forces |

| 3.5 US Lithography Systems Market Revenues & Volume Share, By Technology, 2021 & 2031F |

| 3.6 US Lithography Systems Market Revenues & Volume Share, By Application, 2021 & 2031F |

| 4 US Lithography Systems Market Dynamics |

| 4.1 Impact Analysis |

| 4.2 Market Drivers |

| 4.2.1 Technological advancements in lithography systems |

| 4.2.2 Increasing demand for high-resolution imaging in industries such as semiconductor and electronics |

| 4.2.3 Growing investments in research and development in the field of lithography systems |

| 4.3 Market Restraints |

| 4.3.1 High initial investment required for lithography systems |

| 4.3.2 Limited availability of skilled professionals in the field of lithography |

| 4.3.3 Regulatory challenges related to environmental and safety standards |

| 5 US Lithography Systems Market Trends |

| 6 US Lithography Systems Market, By Types |

| 6.1 US Lithography Systems Market, By Technology |

| 6.1.1 Overview and Analysis |

| 6.1.2 US Lithography Systems Market Revenues & Volume, By Technology, 2021-2031F |

| 6.1.3 US Lithography Systems Market Revenues & Volume, By ArF Immersion, 2021-2031F |

| 6.1.4 US Lithography Systems Market Revenues & Volume, By KrF, 2021-2031F |

| 6.1.5 US Lithography Systems Market Revenues & Volume, By i-line, 2021-2031F |

| 6.1.6 US Lithography Systems Market Revenues & Volume, By ArF Dry, 2021-2031F |

| 6.1.7 US Lithography Systems Market Revenues & Volume, By EUV, 2021-2031F |

| 6.2 US Lithography Systems Market, By Application |

| 6.2.1 Overview and Analysis |

| 6.2.2 US Lithography Systems Market Revenues & Volume, By Foundry, 2021-2031F |

| 6.2.3 US Lithography Systems Market Revenues & Volume, By Memory, 2021-2031F |

| 6.2.4 US Lithography Systems Market Revenues & Volume, By Integrated Device, 2021-2031F |

| 7 US Lithography Systems Market Import-Export Trade Statistics |

| 7.1 US Lithography Systems Market Export to Major Countries |

| 7.2 US Lithography Systems Market Imports from Major Countries |

| 8 US Lithography Systems Market Key Performance Indicators |

| 8.1 Number of patents filed for lithography system technologies |

| 8.2 Adoption rate of next-generation lithography systems in the US market |

| 8.3 Percentage of research and development budget allocated to lithography system innovation |

| 9 US Lithography Systems Market - Opportunity Assessment |

| 9.1 US Lithography Systems Market Opportunity Assessment, By Technology, 2021 & 2031F |

| 9.2 US Lithography Systems Market Opportunity Assessment, By Application, 2021 & 2031F |

| 10 US Lithography Systems Market - Competitive Landscape |

| 10.1 US Lithography Systems Market Revenue Share, By Companies, 2024 |

| 10.2 US Lithography Systems Market Competitive Benchmarking, By Operating and Technical Parameters |

| 11 Company Profiles |

| 12 Recommendations |

| 13 Disclaimer |

Global Go To Market Strategy - 2030

Export potential enables firms to identify high-growth global markets with greater confidence by combining advanced trade intelligence with a structured quantitative methodology. The framework analyzes emerging demand trends and country-level import patterns while integrating macroeconomic and trade datasets such as GDP and population forecasts, bilateral import–export flows, tariff structures, elasticity differentials between developed and developing economies, geographic distance, and import demand projections. Using weighted trade values from 2020–2024 as the base period to project country-to-country export potential for 2030, these inputs are operationalized through calculated drivers such as gravity model parameters, tariff impact factors, and projected GDP per-capita growth. Through an analysis of hidden potentials, demand hotspots, and market conditions that are most favorable to success, this method enables firms to focus on target countries, maximize returns, and global expansion with data, backed by accuracy.

By factoring in the projected importer demand gap that is currently unmet and could be potential opportunity, it identifies the potential for the Exporter (Country) among 190 countries, against the general trade analysis, which identifies the biggest importer or exporter.

To discover high-growth global markets and optimize your business strategy:

Click Here

Pricing

- Single User License$ 1,995

- Department License$ 2,400

- Site License$ 3,120

- Global License$ 3,795

Leadership Perspectives from Industry Events

Search

Thought Leadership and Analyst Meet

Our Clients

6WResearch In News

- India Air Conditioner Market Set for Strong Rebound in 2026 After Weather-Led Correction and GST-Driven Recovery: 6Wresearch

- ADAS in India: How Automatic Emergency Braking, Blind Spot Detection & Driver Monitoring are Transforming Road Safety

- Doha a strategic location for EV manufacturing hub: IPA Qatar

- Demand for luxury TVs surging in the GCC, says Samsung

- Empowering Growth: The Thriving Journey of Bangladesh’s Cable Industry

- Demand for luxury TVs surging in the GCC, says Samsung

Latest Reports

- Poland Fire Protection Systems Market (2026-2032)

- Cape Verde Portable Hand-Thrown Extinguisher Market (2026-2032)

- Canada Portable Hand-Thrown Extinguisher Market (2026-2032)

- Cameroon Portable Hand-Thrown Extinguisher Market (2026-2032)

- Burundi Portable Hand-Thrown Extinguisher Market (2026-2032)

- Burkina Faso Portable Hand-Thrown Extinguisher Market (2026-2032)

- Bulgaria Portable Hand-Thrown Extinguisher Market (2026-2032)

- Brunei Portable Hand-Thrown Extinguisher Market (2026-2032)

- Botswana Portable Hand-Thrown Extinguisher Market (2026-2032)

- Bosnia and Herzegovina Portable Hand-Thrown Extinguisher Market (2026-2032)

Industry Events and Analyst Meet

HIMTEX 2026

India Refining Summit 2026

India EV Show 2026

EV tech India Expo 2026

Auto Tech Asia 2026

Whitepaper

- Middle East & Africa Commercial Security Market Click here to view more.

- Middle East & Africa Fire Safety Systems & Equipment Market Click here to view more.

- GCC Drone Market Click here to view more.

- Middle East Lighting Fixture Market Click here to view more.

- GCC Physical & Perimeter Security Market Click here to view more.