Australia Organic Farming Market (2026-2032) | Competitive Landscape, Forecast, Industry, Value, Segmentation, Size & Revenue, Analysis, Share, Growth, Outlook, Trends, Companies

Market Forecast By Type (Pure Organic Farming, Integrated Organic Farming), By Product (Fruits, Vegetables, Cereals and Grains, Others), By Method (Crop Rotation, Polyculture, Mulching, Soil Management, Weed Management, Composting, Others), By End User (Agriculture Companies, Organic Farms) And Competitive Landscape

| Product Code: ETC6187083 | Publication Date: Sep 2024 | Updated Date: Mar 2026 | Product Type: Market Research Report | |

| Publisher: 6Wresearch | Author: Shubham Padhi | No. of Pages: 75 | No. of Figures: 35 | No. of Tables: 20 |

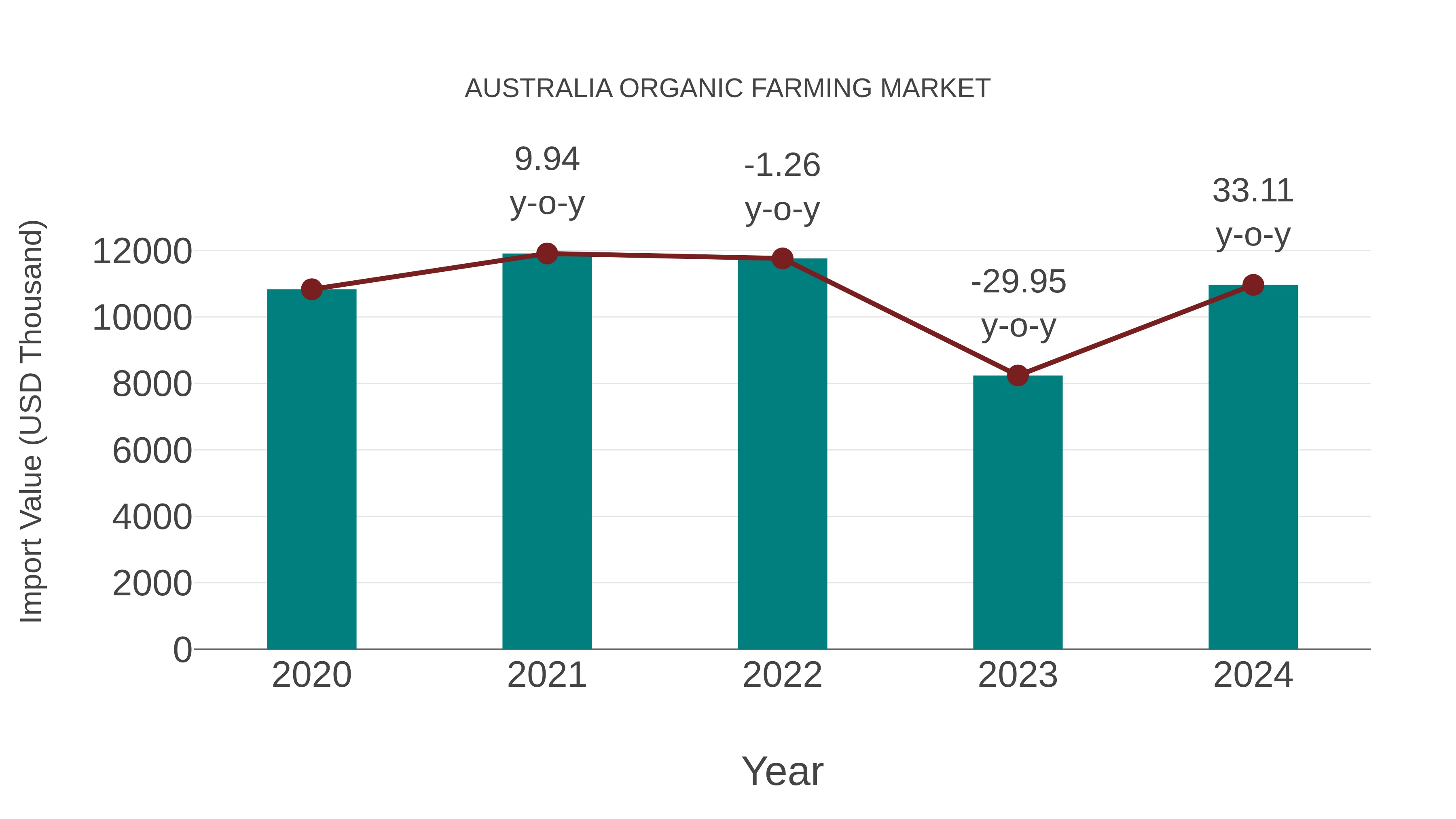

Australia Organic Farming Market: Import Trend Analysis

Australia`s import trend for the organic farming market experienced significant growth from 2023 to 2024, with a notable rate of 33.11%. The compound annual growth rate (CAGR) for the period of 2020 to 2024 stood at 0.3%. This growth can be attributed to a shift in consumer demand towards organic products, reflecting a changing preference for healthier and sustainable options in the market.

Australia Organic Farming Market Growth Rate

According to 6Wresearch internal database and industry insights, the Australia Organic Farming Market is anticipated to rise at a compound annual growth rate (CAGR) of 8.1% during the forecast period 2025 2031.

Five Year Growth Trajectory of the Australia Organic Farming Market with Core Drivers

Below is the evaluation of year wise growth rate along with key growth drivers:

| Year | Est. Annual Growth (%) | Growth Drivers |

| 2020 | 2.8% | There has been growing consumer demand for chemical‑free produce supported initial organic farm uptake. |

| 2021 | 3.7% | Massive expansion of organic retail offerings and improved access through online channels increased organic produce consumption. |

| 2022 | 5.1% | Widespread adoption of organic methods such as crop rotation and composting gained momentum as farmers sought sustainable practices. |

| 2023 | 6.54% | Enormous growth in export‑oriented organic produce and stronger certification frameworks improved market reliability. |

| 2024 | 6.9% | Government incentives and heightened environmental awareness accelerated the transition to organic farming practices. |

Australia Organic Farming Market Highlights

| Report Name | Australia Organic Farming Market |

| Forecast Period | 2025‑2031 |

| CAGR | 8.1% |

| Growing Segment | Agriculture |

Topics Covered in the Australia Organic Farming Market Report

Australia Organic Farming Market report thoroughly covers the market by product, type, method, and end-user. The report provides an unbiased and detailed analysis of ongoing market trends, opportunities/high growth areas, and market drivers, which would help stakeholders to devise and align their market strategies according to the current and future market dynamics.

Australia Organic Farming Market Synopsis

Australia Organic Farming Market is expected to experience significant growth in the forecast years due to increasing consumer demand for organic produce and products produced without synthetic chemicals or genetically modified organisms. Furthermore, more sustainable farming practices including crop rotation, mulching and soil management are leading to reduced chemical inputs, increased productivity, and environmental integrity positioning the market for sustained growth in the long-term.

Evaluation of Growth Drivers in the Australia Organic Farming Market

Below mentioned are some major growth factors and their impacts on the market dynamics:

| Drivers | Primary Segments Affected | Why it matters (evidence) |

| Consumer preference for clean‑label produce | By Product (Fruits, Vegetables) | Consumers who are more health‑conscious are actively favouring organic produce over conventional substitutes. |

| Expansion of export channels | By End User (Agriculture Companies) | Organic producers in the country are leveraging export demand to scale operations and increase profitability. |

| Emphasis on sustainable farming methods | By Method (Crop Rotation, Composting) | Organic farming methods improve soil health and resilience, aligning with environmental policies. |

| Certification & standards enforcement | By Type (Pure Organic Farming, Integrated Organic Farming) | Robust certification frameworks augment consumer trust and market access for organic farms. |

| Technological adoption in farming | By Method (Soil Management, Weed Management) | Use of ag tech highly supports higher yields and effective organic crop management. |

Australia Organic Farming Market is anticipated to grow at a CAGR of 8.1% during the forecast period of 2025 2031. Due to strong shift toward healthier and more environmentally responsible consumption patterns, the growth is expected to proliferate in the coming years. Furthermore, the growing adoption of sustainable and regenerative farming practices across the country is enhancing soil health, improving long-term productivity, and encouraging more farmers to transition to certified organic methods.

Evaluation of Restraints in the Australia Organic Farming Market

Below mentioned are some major restraints and their influence on the market dynamics:

| Restraints | Primary Segments Affected | What this means |

| High certification and transition costs | By Type (Pure Organic Farming) | Small‑scale farmers face financial burdens when converting to organic standards. |

| Lower yields compared with conventional farming | By Method (Polyculture, Mulching) | Yields may be suppressed in early stages of transition, affecting profitability. |

| Supply chain and market access limitations | By End User (Organic Farms) | Limited infrastructure in remote regions obstructs efficient distribution and export readiness. |

| Competition from imported ‘organic’ labels | By Product (Others) | Imported organic‑label products may undermine price competitiveness for local producers. |

| Climate and environmental variability | By Method (Soil Management, Weed Management) | Australia’s variable weather and extreme events pose risk to consistent organic output. |

Australia Organic Farming Market Challenges

Despite of growth outlook, the Australia Organic Farming Market is expected to witness key barriers such as the high cost and complexity of obtaining organic certification, particularly for small and medium scale farms. Transitioning to organic methods often results in initial yield reductions and increased labour demands. Apart from this, supply chain constraints and remote geographic locations affect distribution efficiency and export potential. Additionally, competition from lower cost imported organic products and exposure to climate variability create uncertainty for market participants.

Australia Organic Farming Market Trends

Below are the key trends shaping the Australia Organic Farming Industry:

- Expansion of Integrated Organic Farming: A growing number of Australian farmers are embracing integrated farming, which consists of crop, livestock, and aquaculture operations, often packaged as a certified organic system. This trend creates opportunities for diversified risk and improved resource efficiency.

- Increased Investments in Organic Certification and Traceability: Growing demand for transparency and confidence in organic claims has led to organic certification schemes, and systems for traceability developed through blockchain technology.

- Greater Focus on Soil Health and Regenerative Practices: More farmers are focusing on practices such as composting, cover cropping, and mulching aimed at rebuilding soil fertility and sustainability.

- Expansion of Premium Organic Fruit & Vegetable Exports: Australia's climate and strong reputation contribute to the expansion of high value organic fruit and vegetable exports to Asia and Europe.

Investment Opportunities in the Australia Organic Farming Market

Some of the potential investment prospects in the Australia Organic Farming Industry:

- Growth of Integrated Organic Farming Systems: The integration of livestock, aquaculture, and crops in one certified organic system presents opportunities overall for diversified income and improved resource efficiency.

- Technology Driven Organic Farming Solutions: Technology investment in precision agriculture, monitoring and automation can enhance efficiency, yield, and improved competitiveness of organic farms.

- Development of Organic Method Services and Inputs: Organic composts, biopesticides and mulching system producers are positioned to service the growing demand for certified organic inputs.

- Customization of Organic Farming for Niche Markets: Tailored organic produce for premium, health conscious domestic consumers and direct to consumer channels offers higher margins and brand differentiation.

Top 5 Leading Players in the Australia Organic Farming Market

There are some top companies dominating the Australia Organic Farming Industry, including:

Bellamy’s Organic

| Company Name | Bellamy’s Organic |

| Headquarters | Tasmania, Australia |

| Established | 2003 |

| Website | Click Here |

This company produces certified organic infant formula and packaged organic foods, catering to both domestic and export markets.

Barambah Organics

| Company Name | Barambah Organics |

| Headquarters | Queensland, Australia |

| Established | 2001 |

| Website | _ |

Known for organic meats and dairy, the company operates fully certified organic farms and supply chains.

Manna Farms

| Company Name | Manna Farms |

| Headquarters | Victoria, Australia |

| Established | 2008 |

| Website | Click Here |

Specialises in organic fruits and vegetables produced under regenerative practices, supplying retail and export channels.

Cleaver’s Organic

| Company Name | Cleaver’s Organic |

| Headquarters | New South Wales, Australia |

| Established | 2010 |

| Website | Click Here |

Provides organic grains and cereals, focusing on soil management and certified organic cropping systems.

Australian Organic Food Co.

| Company Name | Australian Organic Food Co. |

| Headquarters | 2012 |

| Established | Western Australia, Australia |

| Website | _ |

Government Regulations Introduced in the Australia Organic Farming Market

According to Australian Government Data, they have instituted regulations and programmes to support the organic agriculture sector by ensuring rigorous certification, facilitating exports, and promoting sustainable practices. In addition to this, there are certification standards administered by bodies such as Australian Organic Limited require strict compliance with chemical free production, soil conservation, and biodiversity. Also, there is ongoing land management and environmental programmes are encouraging adoption of regenerative organic farming practices nationwide, thereby reinforcing the integrity and credibility of the organic farming sector in Australia.

Future Insights of the Australia Organic Farming Market

The outlook for the Australia Organic Farming Market over the upcoming years is largely optimistic. The main factors affecting market growth include rising health consciousness, growing demand for sustainably produced food, and being favourably positioned for Australia’s exports. The most important consideration for future growth will be the evolution toward regenerative farming systems or integrated organic farming systems that are more resilient and productive, in addition to technology creating more efficient use of inputs and improving transparency. Increased use of technology in precision organic farming, alongside enhanced certification systems across supply chains is anticipated to further drive the Australia Organic Farming Market Growth outlook.

Market Segmentation Analysis

The report offers a comprehensive study of the following market segments and their leading categories:

By Type- Integrated Organic Farming to Dominate the Market

Integrated Organic Farming is the dominant segment as it combines multiple farming practices such as crop rotation, livestock management, and aquaculture under organic standards. This method allows farmers to diversify their income streams, improve resource use efficiency, and enhance sustainability, making it more attractive to large-scale agriculture companies. It also offers better risk mitigation through diversified production, leading to its dominance in the market.

By Method- Crop Rotation to Dominate the Market

According to Parth, Senior Research Analyst, 6Wresearch, Crop Rotation is the dominant method in organic farming due to its effectiveness in maintaining soil fertility and controlling pests naturally. It is a cornerstone of organic farming because it reduces the need for synthetic fertilizers and pesticides, making it essential for sustainable organic practices.

By End User- Agriculture Companies to Dominate the Market

Agriculture Companies are expected to lead the Australia Organic Farming Market as they have the resources to scale organic farming operations, navigate the complexities of organic certification, and manage logistics for both domestic and international markets. These companies typically operate at a larger scale, making them key players in driving the market growth.

Key Attractiveness of the Report

- 10 Years of Market Numbers

- Historical Data Starting from 2021 to 2024

- Base Year: 2024

- Forecast Data until 2031

- Key Performance Indicators Impacting the Market

- Major Upcoming Developments and Projects

Key Highlights of the Report:

- Australia Organic Farming Market Outlook

- Market Size of Australia Organic Farming Market, 2025

- Forecast of Australia Organic Farming Market, 2032

- Historical Data and Forecast of Australia Organic Farming Revenues & Volume for the Period 2022-2032F

- Australia Organic Farming Market Trend Evolution

- Australia Organic Farming Market Drivers and Challenges

- Australia Organic Farming Price Trends

- Australia Organic Farming Porter's Five Forces

- Australia Organic Farming Industry Life Cycle

- Historical Data and Forecast of Australia Organic Farming Market Revenues & Volume By Type for the Period 2022-2032F

- Historical Data and Forecast of Australia Organic Farming Market Revenues & Volume By Pure Organic Farming for the Period 2022-2032F

- Historical Data and Forecast of Australia Organic Farming Market Revenues & Volume By Integrated Organic Farming for the Period 2022-2032F

- Historical Data and Forecast of Australia Organic Farming Market Revenues & Volume By Product for the Period 2022-2032F

- Historical Data and Forecast of Australia Organic Farming Market Revenues & Volume By Fruits for the Period 2022-2032F

- Historical Data and Forecast of Australia Organic Farming Market Revenues & Volume By Vegetables for the Period 2022-2032F

- Historical Data and Forecast of Australia Organic Farming Market Revenues & Volume By Cereals and Grains for the Period 2022-2032F

- Historical Data and Forecast of Australia Organic Farming Market Revenues & Volume By Others for the Period 2022-2032F

- Historical Data and Forecast of Australia Organic Farming Market Revenues & Volume By Method for the Period 2022-2032F

- Historical Data and Forecast of Australia Organic Farming Market Revenues & Volume By Crop Rotation for the Period 2022-2032F

- Historical Data and Forecast of Australia Organic Farming Market Revenues & Volume By Polyculture for the Period 2022-2032F

- Historical Data and Forecast of Australia Organic Farming Market Revenues & Volume By Mulching for the Period 2022-2032F

- Historical Data and Forecast of Australia Organic Farming Market Revenues & Volume By Soil Management for the Period 2022-2032F

- Historical Data and Forecast of Australia Organic Farming Market Revenues & Volume By Weed Management for the Period 2022-2032F

- Historical Data and Forecast of Australia Organic Farming Market Revenues & Volume By Composting for the Period 2022-2032F

- Historical Data and Forecast of Australia Organic Farming Market Revenues & Volume By Others for the Period 2022-2032F

- Historical Data and Forecast of Australia Organic Farming Market Revenues & Volume By End User for the Period 2022-2032F

- Historical Data and Forecast of Australia Organic Farming Market Revenues & Volume By Agriculture Companies for the Period 2022-2032F

- Historical Data and Forecast of Australia Organic Farming Market Revenues & Volume By Organic Farms for the Period 2022-2032F

- Australia Organic Farming Import Export Trade Statistics

- Market Opportunity Assessment By Type

- Market Opportunity Assessment By Product

- Market Opportunity Assessment By Method

- Market Opportunity Assessment By End User

- Australia Organic Farming Top Companies Market Share

- Australia Organic Farming Competitive Benchmarking By Technical and Operational Parameters

- Australia Organic Farming Company Profiles

- Australia Organic Farming Key Strategic Recommendations

Market Covered

The report offers a comprehensive study of the subsequent market segments:

By Type

- Pure Organic Farming

- Integrated Organic Farming

- Others

By Product

- Fruits

- Vegetables

- Cereals and Grains

- Others

By Method

- Crop Rotation

- Polyculture

- Mulching

- Soil Management

- Weed Management

- Composting

- Others

By End User

- Agriculture Companies

- Organic Farms

Australia Organic Farming Market (2026-2032): FAQs

Australia organic farming market is expected to grow at a CAGR of 8.1% during the forecast period.

Growth is driven by environmental concerns and soil‑health awareness are pushing farmers to adopt organic practices; and government schemes are offering support for certified organic agriculture.

The main end-users are organic farms themselves and agriculture companies that purchase organic produce for retail, export, or processing into other organic products.

Prominent companies include Australian Organic Ltd., Sustainable Farming Solutions Pty Ltd., Bauer’s Organic Farm Pty Ltd., Eden Framer Organics, Totally Pure Fruits Pty Ltd. and Cleaver’s Organic.

6Wresearch actively monitors the Australia Organic Farming Market and publishes its comprehensive annual report, highlighting emerging trends, growth drivers, revenue analysis, and forecast outlook. Our insights help businesses to make data-backed strategic decisions with ongoing market dynamics. Our analysts track relevent industries related to the Australia Organic Farming Market, allowing our clients with actionable intelligence and reliable forecasts tailored to emerging regional needs.

Yes, we provide customisation as per your requirements. To learn more, feel free to contact us on sales@6wresearch.com

| 1 Executive Summary |

| 2 Introduction |

| 2.1 Key Highlights of the Report |

| 2.2 Report Description |

| 2.3 Market Scope & Segmentation |

| 2.4 Research Methodology |

| 2.5 Assumptions |

| 3 Australia Organic Farming Market Overview |

| 3.1 Australia Country Macro Economic Indicators |

| 3.2 Australia Organic Farming Market Revenues & Volume, 2022 & 2032F |

| 3.3 Australia Organic Farming Market - Industry Life Cycle |

| 3.4 Australia Organic Farming Market - Porter's Five Forces |

| 3.5 Australia Organic Farming Market Revenues & Volume Share, By Type, 2022 & 2032F |

| 3.6 Australia Organic Farming Market Revenues & Volume Share, By Product, 2022 & 2032F |

| 3.7 Australia Organic Farming Market Revenues & Volume Share, By Method, 2022 & 2032F |

| 3.8 Australia Organic Farming Market Revenues & Volume Share, By End User, 2022 & 2032F |

| 4 Australia Organic Farming Market Dynamics |

| 4.1 Impact Analysis |

| 4.2 Market Drivers |

| 4.2.1 Increasing consumer awareness and demand for organic products |

| 4.2.2 Growing concerns about health and sustainability |

| 4.2.3 Supportive government policies promoting organic farming practices |

| 4.3 Market Restraints |

| 4.3.1 Higher production costs compared to conventional farming |

| 4.3.2 Limited availability of organic farming inputs and resources |

| 4.3.3 Lack of standardized regulations and certifications in the organic farming industry |

| 5 Australia Organic Farming Market Trends |

| 6 Australia Organic Farming Market, By Types |

| 6.1 Australia Organic Farming Market, By Type |

| 6.1.1 Overview and Analysis |

| 6.1.2 Australia Organic Farming Market Revenues & Volume, By Type, 2021- 2031F |

| 6.1.3 Australia Organic Farming Market Revenues & Volume, By Pure Organic Farming, 2021- 2031F |

| 6.1.4 Australia Organic Farming Market Revenues & Volume, By Integrated Organic Farming, 2021- 2031F |

| 6.2 Australia Organic Farming Market, By Product |

| 6.2.1 Overview and Analysis |

| 6.2.2 Australia Organic Farming Market Revenues & Volume, By Fruits, 2021- 2031F |

| 6.2.3 Australia Organic Farming Market Revenues & Volume, By Vegetables, 2021- 2031F |

| 6.2.4 Australia Organic Farming Market Revenues & Volume, By Cereals and Grains, 2021- 2031F |

| 6.2.5 Australia Organic Farming Market Revenues & Volume, By Others, 2021- 2031F |

| 6.3 Australia Organic Farming Market, By Method |

| 6.3.1 Overview and Analysis |

| 6.3.2 Australia Organic Farming Market Revenues & Volume, By Crop Rotation, 2021- 2031F |

| 6.3.3 Australia Organic Farming Market Revenues & Volume, By Polyculture, 2021- 2031F |

| 6.3.4 Australia Organic Farming Market Revenues & Volume, By Mulching, 2021- 2031F |

| 6.3.5 Australia Organic Farming Market Revenues & Volume, By Soil Management, 2021- 2031F |

| 6.3.6 Australia Organic Farming Market Revenues & Volume, By Weed Management, 2021- 2031F |

| 6.3.7 Australia Organic Farming Market Revenues & Volume, By Composting, 2021- 2031F |

| 6.4 Australia Organic Farming Market, By End User |

| 6.4.1 Overview and Analysis |

| 6.4.2 Australia Organic Farming Market Revenues & Volume, By Agriculture Companies, 2021- 2031F |

| 6.4.3 Australia Organic Farming Market Revenues & Volume, By Organic Farms, 2021- 2031F |

| 7 Australia Organic Farming Market Import-Export Trade Statistics |

| 7.1 Australia Organic Farming Market Export to Major Countries |

| 7.2 Australia Organic Farming Market Imports from Major Countries |

| 8 Australia Organic Farming Market Key Performance Indicators |

| 8.1 Percentage increase in certified organic farmland in Australia |

| 8.2 Number of new organic farming operations established |

| 8.3 Adoption rate of organic farming practices by conventional farmers |

| 9 Australia Organic Farming Market - Opportunity Assessment |

| 9.1 Australia Organic Farming Market Opportunity Assessment, By Type, 2022 & 2032F |

| 9.2 Australia Organic Farming Market Opportunity Assessment, By Product, 2022 & 2032F |

| 9.3 Australia Organic Farming Market Opportunity Assessment, By Method, 2022 & 2032F |

| 9.4 Australia Organic Farming Market Opportunity Assessment, By End User, 2022 & 2032F |

| 10 Australia Organic Farming Market - Competitive Landscape |

| 10.1 Australia Organic Farming Market Revenue Share, By Companies, 2025 |

| 10.2 Australia Organic Farming Market Competitive Benchmarking, By Operating and Technical Parameters |

| 11 Company Profiles |

| 12 Recommendations |

| 13 Disclaimer |

Global Go To Market Strategy - 2030

Export potential enables firms to identify high-growth global markets with greater confidence by combining advanced trade intelligence with a structured quantitative methodology. The framework analyzes emerging demand trends and country-level import patterns while integrating macroeconomic and trade datasets such as GDP and population forecasts, bilateral import–export flows, tariff structures, elasticity differentials between developed and developing economies, geographic distance, and import demand projections. Using weighted trade values from 2020–2024 as the base period to project country-to-country export potential for 2030, these inputs are operationalized through calculated drivers such as gravity model parameters, tariff impact factors, and projected GDP per-capita growth. Through an analysis of hidden potentials, demand hotspots, and market conditions that are most favorable to success, this method enables firms to focus on target countries, maximize returns, and global expansion with data, backed by accuracy.

By factoring in the projected importer demand gap that is currently unmet and could be potential opportunity, it identifies the potential for the Exporter (Country) among 190 countries, against the general trade analysis, which identifies the biggest importer or exporter.

To discover high-growth global markets and optimize your business strategy:

Click Here

Pricing

- Single User License$ 1,995

- Department License$ 2,400

- Site License$ 3,120

- Global License$ 3,795

Leadership Perspectives from Industry Events

Search

Thought Leadership and Analyst Meet

Our Clients

6WResearch In News

- India Export Attractiveness Tracker 2026

- India Air Conditioner Market Set for Strong Rebound in 2026 After Weather-Led Correction and GST-Driven Recovery: 6Wresearch

- ADAS in India: How Automatic Emergency Braking, Blind Spot Detection & Driver Monitoring are Transforming Road Safety

- Doha a strategic location for EV manufacturing hub: IPA Qatar

- Demand for luxury TVs surging in the GCC, says Samsung

- Empowering Growth: The Thriving Journey of Bangladesh’s Cable Industry

Latest Reports

- Nicaragua RPG Gaming Market (2026-2032)

- New Zealand RPG Gaming Market (2026-2032)

- Netherlands RPG Gaming Market (2026-2032)

- Nauru RPG Gaming Market (2026-2032)

- Namibia RPG Gaming Market (2026-2032)

- Mozambique RPG Gaming Market (2026-2032)

- Montenegro RPG Gaming Market (2026-2032)

- Mongolia RPG Gaming Market (2026-2032)

- Monaco RPG Gaming Market (2026-2032)

- Micronesia RPG Gaming Market (2026-2032)

Industry Events and Analyst Meet

EV India Expo 2026

HIMTEX 2026

India Refining Summit 2026

India EV Show 2026

EV tech India Expo 2026

Whitepaper

- Middle East & Africa Commercial Security Market Click here to view more.

- Middle East & Africa Fire Safety Systems & Equipment Market Click here to view more.

- GCC Drone Market Click here to view more.

- Middle East Lighting Fixture Market Click here to view more.

- GCC Physical & Perimeter Security Market Click here to view more.