Bangladesh Ethanol Market (2025-2029) | Trends, Value, Size, Revenue, Share, Forecast, Analysis, Outlook, Industry, Segmentation

MarketForecastBy Purity (Denatured, Non-Denatured), By Sources (Sugar & Molasses Based, Grained Based, Second Generation) By Application (Industrial Solvent, Fuel & Fuel Additives, Beverages, Disinfectant, Personal Care, Others) And Competitive Landscape

| Product Code: ETC003114 | Publication Date: Jul 2020 | Updated Date: Aug 2025 | Product Type: Report | |

| Publisher: 6Wresearch | Author: Ravi Bhandari | No. of Pages: 70 | No. of Figures: 35 | No. of Tables: 5 |

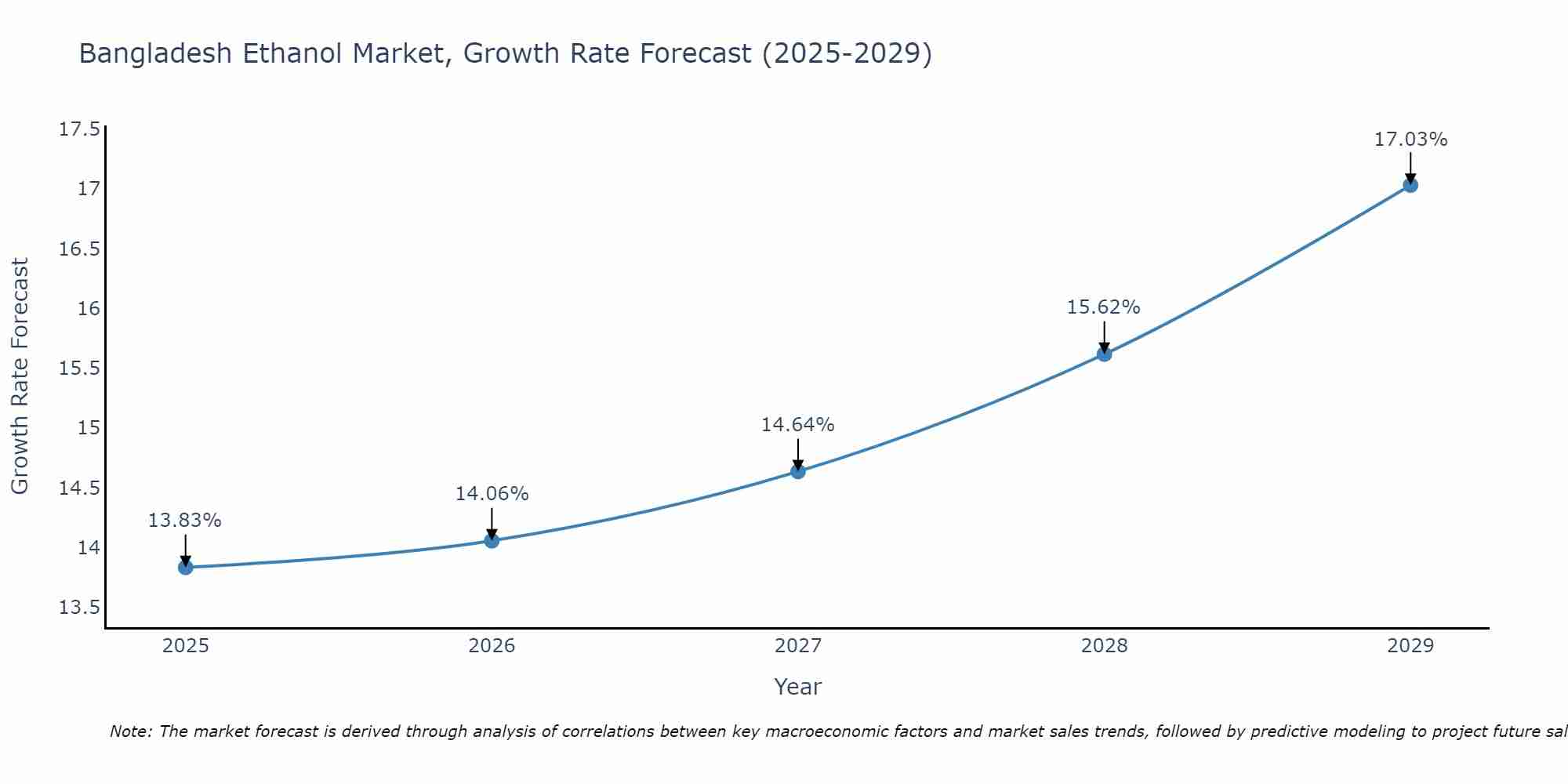

Bangladesh Ethanol Market Size Growth Rate

The Bangladesh Ethanol Market is likely to experience consistent growth rate gains over the period 2025 to 2029. The growth rate starts at 13.83% in 2025 and reaches 17.03% by 2029.

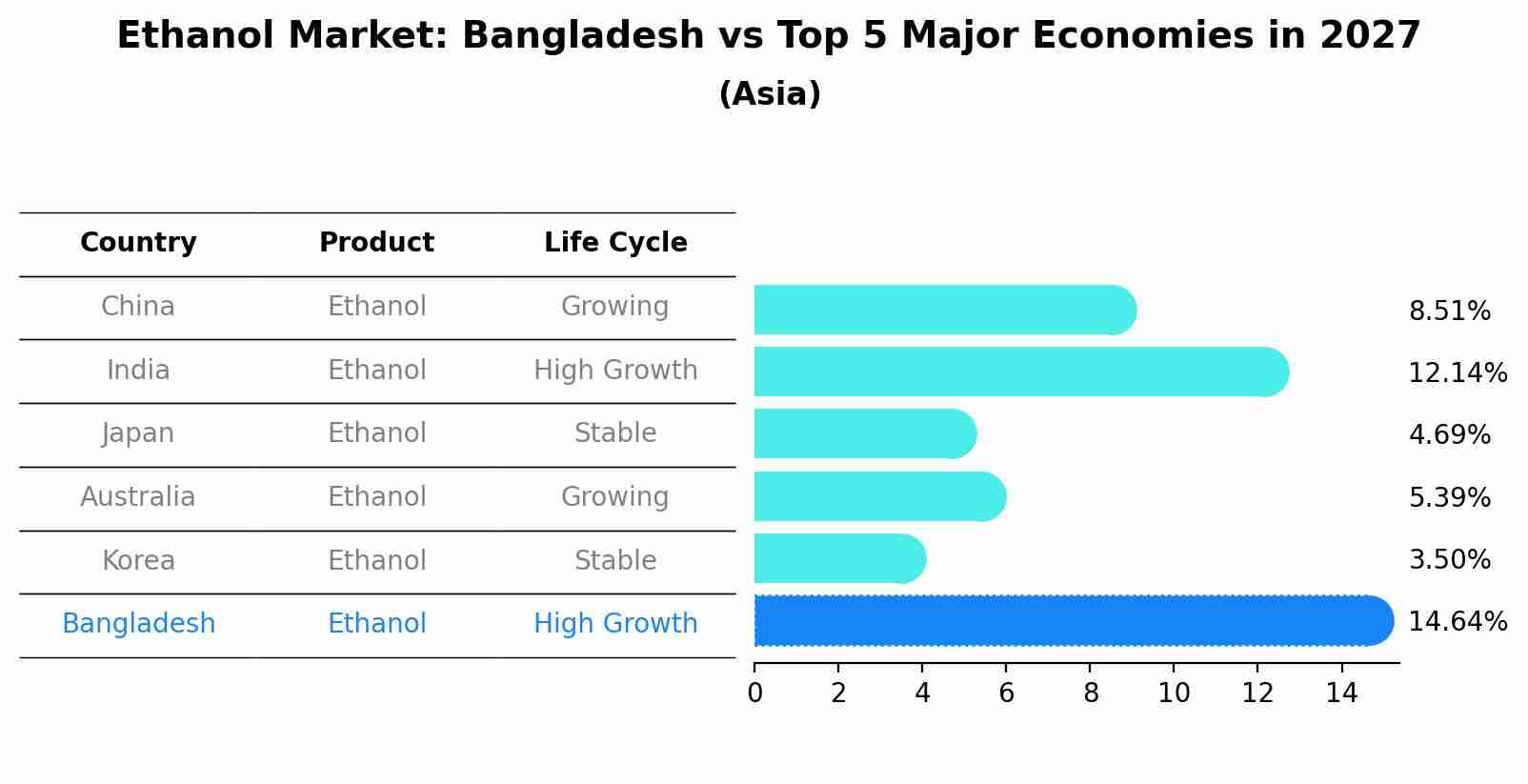

Ethanol Market: Bangladesh vs Top 5 Major Economies in 2027 (Asia)

By 2027, Bangladesh's Ethanol market is forecasted to achieve a high growth rate of 14.64%, with China leading the Asia region, followed by India, Japan, Australia and South Korea.

Bangladesh Ethanol Market Highlights

| Report Name | Bangladesh Ethanol Market |

| Forecast Period | 2025-2029 |

| CAGR | 17.03% |

| Growing Sector | Transportation |

Topics Covered in the Bangladesh Ethanol Market Report

The Bangladesh Ethanol Market report thoroughly covers the market by purity, sources and application. The report provides an unbiased and detailed analysis of the ongoing market trends, opportunities/high-growth areas, and market drivers to help stakeholders align their strategies with current and future market dynamics.

Bangladesh Ethanol Market Synopsis

The Bangladesh ethanol market is gaining popularity as policymakers seek substitute energy avenues to lower the reliance on imported fossil fuels and improve national energy flexibility. Momentum stems from the availability of agricultural residues, national biofuel policy support, and stakeholder interest across public and private sectors. Pilot ventures and small-scale production efforts are emerging in rural and peri-urban regions, reflecting measured adoption. Policymakers are balancing energy purposes with rural livelihoods, food security, and community well-being widely.

The Bangladesh Ethanol Market is anticipated to grow at a CAGR of 17.03% during the forecast period 2025-2029. Major drivers of the Bangladesh ethanol market include plentiful agricultural byproducts suitable for conversion, national biofuel policy endorsement, and growing energy demand that encourages variation away from imported fuels. Environmental issues and commitments to reduce greenhouse gas emissions push stakeholders to consider bioethanol as part of a low-carbon mix. Private sector interest in feedstock value addition and technology providers presenting conversion solutions further drives momentum. Trade dialogues and regional collaborations support tactical planning and investment confidence.

Bangladesh Ethanol Market Challenges

Challenges that hinder the growth of Bangladesh ethanol market include competition between using crops for food and diverting feedstock to boost manufacturing, which raises social and policy worries. Underdeveloped logistics and restrained industrial scale processing capacity increase costs and limit reliable supply chains. Financial obstacles and volatile long-term incentives make venture financing complex, while technical limitations in large-scale conversion capacity obstruct commercialization. Building distribution networks and guaranteeing stable fuel quality remain critical to gaining consumer and industry confidence and governance reforms.

Bangladesh Ethanol Market Trends

Recent trends include growing interest in enhanced ethanol technologies that use processing waste and agricultural residues, supporting circular economy principles. Pilot demonstrations facilitate modular production units that can be located near feedstock sources to minimize food competition and reduce transport. Research collaborations with universities emphasizing enhancing conversion efficiency and cost reduction. Dialogue on regional trade and potential import partnerships informs tactical selections. Traceability and sustainable certification are gaining popularity among consumers and policymakers widely.

Investment Opportunities in the Bangladesh Ethanol Market

Investment prospects lie in establishing conversion plants that process local residues into ethanol while adding value in rural economies. Storage facilities, building logistics hubs, and quality testing laboratories enhance supply trustworthiness. There is a possibility for engineering services, technology licensing, and financing structures that support demonstration ventures and risk sharing. Partnerships that fuse smallholders into feedstock supply chains and that allow co-products for agricultural inputs can improve returns while enhancing resilience and sustainable rural development.

Leading Players in the Bangladesh Ethanol Market

Prominent companies in the Bangladesh ethanol market include established industrial alcohol manufacturers such as Deshbandhu Group, PRAN-RFL Group, and Mymensingh Agro Limited, which tap into processing capabilities and strong fermentation. Emerging residue-to-ethanol technology firms and trading companies support supply flexibility. These stakeholders focus on scaling capacity, securing feedstock, and exploring fuel blending opportunities to meet growing domestic and potential export demand.

Government Regulations in the Bangladesh Ethanol Market

According to Bangladeshi government data, regulatory provisions address licensing for ethanol production, fuel quality standards for blending, environmental safeguards at production sites, and oversight mechanisms for power alcohol operations. Historic ordinances provide legal tools to govern production and feedstock selection to mitigate food security impacts. Coordination across energy, agriculture, and trade ministries guides pilot blending initiatives and import rules. Compliance requirements aim to ensure safety, traceability, and alignment with national energy and agricultural priorities and oversight.

Future Insights of the Bangladesh Ethanol Market

The Bangladesh ethanol market is poised for significant growth in the coming years, driven by increasing demand for renewable energy sources and the implementation of government-backed policies encouraging sustainable fuel alternatives. With a growing focus on reducing carbon emissions, ethanol has emerged as a viable solution for blending with conventional fuels, aiding in the transition towards greener energy practices. Additionally, the country's expanding agro-based economy provides ample raw materials, such as sugarcane and molasses, to support ethanol production.

Market Segmentation Analysis

The report offers a comprehensive study of the following market segments and their leading categories:

Fuel-grade ethanol to Dominate the Market – By Purity

According to Adammya, Senior Research Analyst at 6Wresearch, Fuel-grade ethanol is expected to dominate the Bangladesh ethanol market, driven by government interest in blending mandates to reduce fossil fuel dependence. Its production aligns with energy diversification goals, using cost-effective processes and local feedstock.

Molasses-based ethanol to Dominate the Market – By Sources

Molasses-based ethanol is anticipated to lead due to Bangladesh’s strong sugarcane production, providing a consistent and readily available feedstock. Established distilleries already integrated with sugar mills make molasses a cost-effective and scalable source.

Transportation Fuel segment to Dominate the Market – By Application

The transportation fuel segment is set to dominate, supported by policy interest in ethanol blending to lower greenhouse gas emissions and reduce fuel imports. Ethanol’s role in enhancing octane levels and improving combustion efficiency makes it attractive for the automotive sector.

Key Attractiveness of the Report

- 10 Years of Market Numbers.

- Historical Data Starting from 2021 to 2024.

- Base Year: 2024

- Forecast Data until 2029.

- Key Performance Indicators Impacting the Market.

- Major Upcoming Developments and Projects.

Key Highlights of the Report:

- Bangladesh Ethanol Market Overview

- Bangladesh Ethanol Market Outlook

- Bangladesh Ethanol Market Forecast

- Historical Data of Bangladesh Ethanol Market Revenues and Volumes, for the Period 2019-2029

- Market Size & Forecast of Bangladesh Ethanol Market Revenues and Volumes, until 2029

- Historical Data of Bangladesh Ethanol Market Revenues and Volumes, by purity, for the Period 2019-2029

- Market Size & Forecast of Bangladesh Ethanol Market Revenues and Volumes, by purity, until 2029

- Historical Data of Bangladesh Ethanol Market Revenues and Volumes, by Source, for the Period 2019-2029

- Market Size & Forecast of Bangladesh Ethanol Market Revenues and Volumes, by source, until 2029

- Historical Data of Bangladesh Ethanol Market Revenues and Volumes, by application, for the Period 2019-2029

- Market Size & Forecast of Bangladesh Ethanol Market Revenues and Volumes, by application, until 2029

- Market Drivers and Restraints

- Bangladesh Ethanol Market Price Trends

- Bangladesh Ethanol Market Trends and Industry Life Cycle

- Porter’s Five Force Analysis

- Market Opportunity Assessment

- Bangladesh Ethanol Market Share, By Players

- Bangladesh Ethanol Market Overview on Competitive Benchmarking

- Company Profiles

- Key Strategic Recommendations

Market Covered

This report extensively examines the following market segments:

By Purity

- Denatured

- Non-Denatured

By Sources

- Sugar & Molasses Based

- Grained Based

- Second Generation

By Application

- Industrial Solvent

- Fuel & Fuel Additives

- Beverages

- Disinfectant

- Personal Care

- Others

Bangladesh Ethanol Market (2025-2029) : FAQs

The Bangladesh Ethanol market is expected to grow at a CAGR of approximately 17.03% between 2025 and 2029.

The Bangladesh Ethanol market is driven by rising energy demand that motivates diversification away from imported fuels.

Leading players in the Bangladesh ethanol market include established industrial alcohol producers such as PRAN-RFL Group, Deshbandhu Group, and Mymensingh Agro Limited.

Trends show increasing interest in advanced ethanol technologies that utilise agricultural residues and processing waste, aligning with circular economy principles.

6Wresearch actively monitors the Bangladesh Ethanol Market and publishes its comprehensive annual report, highlighting emerging trends, growth drivers, revenue analysis, and forecast outlook. Our insights help businesses to make data-backed strategic decisions with ongoing market dynamics. Our analysts track relevent industries related to the Bangladesh Ethanol Market, allowing our clients with actionable intelligence and reliable forecasts tailored to emerging regional needs.

Yes, we provide customisation as per your requirements. To learn more, feel free to contact us on sales@6wresearch.com

| 1. Executive Summary |

| 2. Introduction |

| 2.1 Report Description |

| 2.2 Key Highlights |

| 2.3 Market Scope & Segmentation |

| 2.4 Research Methodology |

| 2.5 Assumptions |

| 3. Bangladesh Ethanol Market Overview |

| 3.1 Bangladesh Ethanol Market Revenues and Volume, 2019-2029F |

| 3.2 Bangladesh Ethanol Market Revenue Share, By Purity, 2019 & 2029F |

| 3.3 Bangladesh Ethanol Market Revenue Share, By Source, 2019 & 2029F |

| 3.4 Bangladesh Ethanol Market Revenue Share, By Application, 2019 & 2029F |

| 3.5 Bangladesh Ethanol Market - Industry Life Cycle |

| 3.6 Bangladesh Ethanol Market - Porter’s Five Forces |

| 4. Bangladesh Ethanol Market Dynamics |

| 4.1 Impact Analysis |

| 4.2 Market Drivers |

| 4.3 Market Restraints |

| 5. Bangladesh Ethanol Market Trends |

| 6. Bangladesh Ethanol Market Overview, by Source |

| 6.1 Bangladesh Sugar & Molasses Based Ethanol Market Revenues and Volume, 2019-2029F |

| 6.2 Bangladesh Grained Based Ethanol Market Revenues and Volume, 2019-2029F |

| 6.3 Bangladesh Second Generation Ethanol Market Revenues and Volume, 2019-2029F |

| 7. Bangladesh Ethanol Market Overview, by Purity |

| 7.1 Bangladesh Ethanol Market Revenue and Volumes, By Denatured, 2019-2029F |

| 7.2 Bangladesh Ethanol Market Revenue and Volumes, By Non-Denatured, 2019-2029F |

| 8. Bangladesh Ethanol Market Overview, by Application |

| 8.1 Bangladesh Ethanol Market Revenue and Volumes, By Industrial Solvent, 2019-2029F |

| 8.2 Bangladesh Ethanol Market Revenue and Volumes, By Fuel & Fuel Additives, 2019-2029F |

| 8.3 Bangladesh Ethanol Market Revenue and Volumes, By Beverages, 2019-2029F |

| 8.4 Bangladesh Ethanol Market Revenue and Volumes, By Disinfectant, 2019-2029F |

| 8.5 Bangladesh Ethanol Market Revenue and Volumes, By Personal Care, 2019-2029F |

| 8.6 Bangladesh Ethanol Market Revenue and Volumes, By Others, 2019-2029F |

| 9. Bangladesh Ethanol Market Key Performance Indicators |

| 10. Bangladesh Ethanol Market Opportunity Assessment |

| 10.1 Bangladesh Ethanol Market Opportunity Assessment, By Purity, 2029F |

| 10.2 Bangladesh Ethanol Market Opportunity Assessment, By Source, 2029F |

| 10.3 Bangladesh Ethanol Market Opportunity Assessment, By Application, 2029F |

| 11. Bangladesh Ethanol Market Competitive Landscape |

| 11.1 Bangladesh Ethanol Market By Companies, 2024 |

| 11.2 Bangladesh Ethanol Market Competitive Benchmarking, By Operating Parameters |

| 12. Company Profiles |

| 13. Key Strategic Recommendations |

| 14. Disclaimer |

Global Go To Market Strategy - 2030

Export potential enables firms to identify high-growth global markets with greater confidence by combining advanced trade intelligence with a structured quantitative methodology. The framework analyzes emerging demand trends and country-level import patterns while integrating macroeconomic and trade datasets such as GDP and population forecasts, bilateral import–export flows, tariff structures, elasticity differentials between developed and developing economies, geographic distance, and import demand projections. Using weighted trade values from 2020–2024 as the base period to project country-to-country export potential for 2030, these inputs are operationalized through calculated drivers such as gravity model parameters, tariff impact factors, and projected GDP per-capita growth. Through an analysis of hidden potentials, demand hotspots, and market conditions that are most favorable to success, this method enables firms to focus on target countries, maximize returns, and global expansion with data, backed by accuracy.

By factoring in the projected importer demand gap that is currently unmet and could be potential opportunity, it identifies the potential for the Exporter (Country) among 190 countries, against the general trade analysis, which identifies the biggest importer or exporter.

To discover high-growth global markets and optimize your business strategy:

Click Here

Pricing

- Single User License$ 1,995

- Department License$ 2,400

- Site License$ 3,120

- Global License$ 3,795

Leadership Perspectives from Industry Events

Search

Thought Leadership and Analyst Meet

Our Clients

6WResearch In News

- India Air Conditioner Market Set for Strong Rebound in 2026 After Weather-Led Correction and GST-Driven Recovery: 6Wresearch

- ADAS in India: How Automatic Emergency Braking, Blind Spot Detection & Driver Monitoring are Transforming Road Safety

- Doha a strategic location for EV manufacturing hub: IPA Qatar

- Demand for luxury TVs surging in the GCC, says Samsung

- Empowering Growth: The Thriving Journey of Bangladesh’s Cable Industry

- Demand for luxury TVs surging in the GCC, says Samsung

Latest Reports

- Nicaragua RPG Gaming Market (2026-2032)

- New Zealand RPG Gaming Market (2026-2032)

- Netherlands RPG Gaming Market (2026-2032)

- Nauru RPG Gaming Market (2026-2032)

- Namibia RPG Gaming Market (2026-2032)

- Mozambique RPG Gaming Market (2026-2032)

- Montenegro RPG Gaming Market (2026-2032)

- Mongolia RPG Gaming Market (2026-2032)

- Monaco RPG Gaming Market (2026-2032)

- Micronesia RPG Gaming Market (2026-2032)

Industry Events and Analyst Meet

HIMTEX 2026

India Refining Summit 2026

India EV Show 2026

EV tech India Expo 2026

Auto Tech Asia 2026

Whitepaper

- Middle East & Africa Commercial Security Market Click here to view more.

- Middle East & Africa Fire Safety Systems & Equipment Market Click here to view more.

- GCC Drone Market Click here to view more.

- Middle East Lighting Fixture Market Click here to view more.

- GCC Physical & Perimeter Security Market Click here to view more.