Brazil Carbon Market (2025-2031) | Forecast, Size, Analysis, Share, Trends, Outlook, Revenue, Industry, Growth, Value, Companies

Market Forecast By Product Types (Amorphous Carbon, Graphite, Diamond), By Applications (Automotive, Construction, Engineering Industries, Aerospace, Others) And Competitive Landscape

| Product Code: ETC004115 | Publication Date: Sep 2020 | Updated Date: Oct 2025 | Product Type: Report | |

| Publisher: 6Wresearch | Author: Ravi Bhandari | No. of Pages: 70 | No. of Figures: 35 | No. of Tables: 5 |

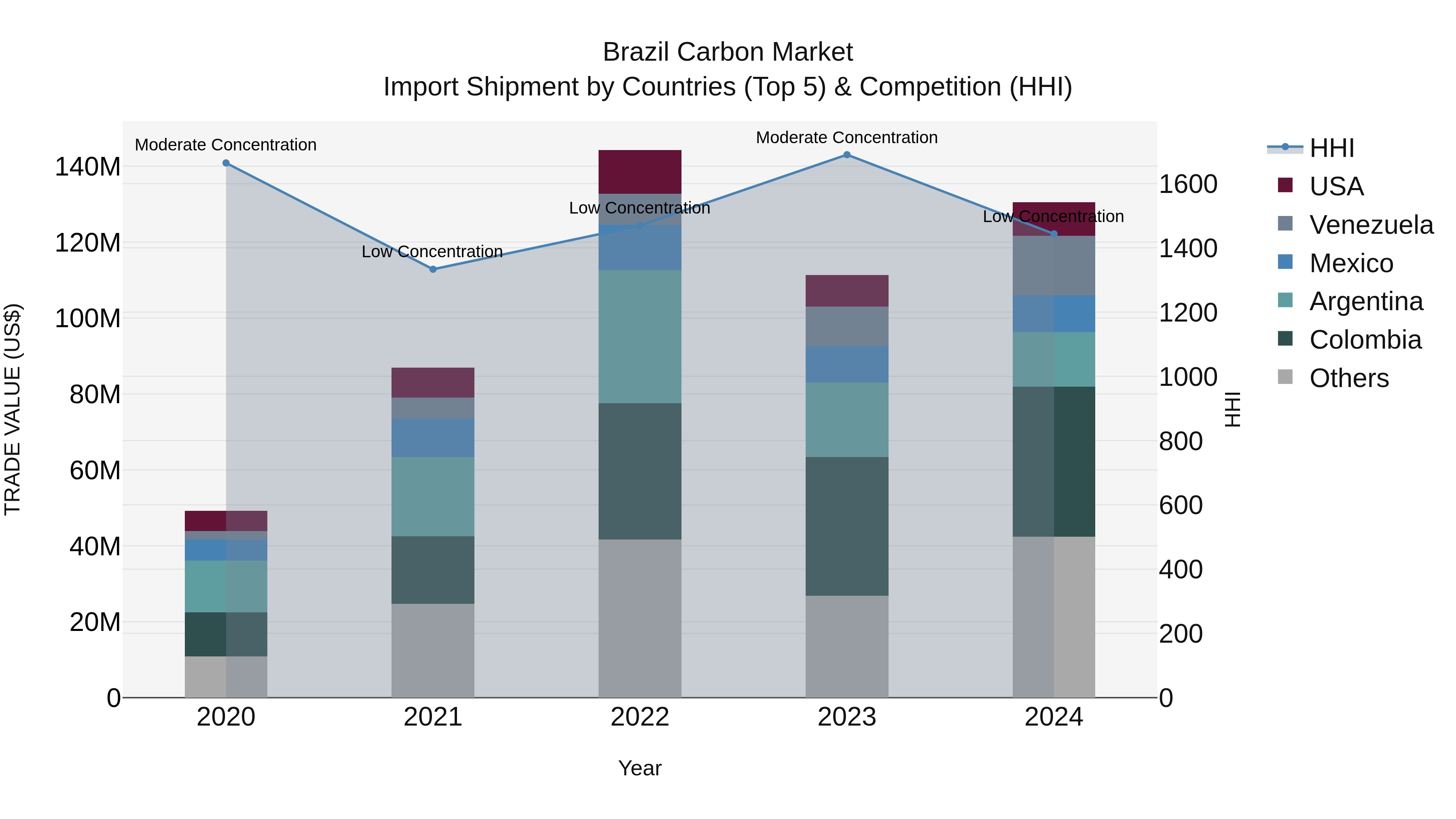

Brazil Carbon Market Top 5 Importing Countries and Market Competition (HHI) Analysis

The carbon import market in Brazil saw significant growth in 2024, with top exporting countries being Colombia, Venezuela, Argentina, Germany, and Mexico. The market concentration, as measured by the HHI, decreased from moderate to low in 2024, indicating a more competitive landscape. The impressive compound annual growth rate (CAGR) of 27.63% from 2020 to 2024 highlights the expanding demand for carbon imports in Brazil. Additionally, the growth rate of 17.18% from 2023 to 2024 suggests a strong momentum in the market, presenting opportunities for both importers and exporters to capitalize on this growing sector.

Brazil Carbon Market Growth Rate

According to 6Wresearch internal database and industry insights

Brazil Carbon Market Highlights

| Report Name | Brazil Carbon Market |

| Forecast period | 2025-2031 |

| CAGR | 6.7% |

| Growing Sector | Automotive & Engineering Industries |

Topics Covered in the Brazil Carbon Market Report

The Brazil Carbon Market report thoroughly covers the market by product types and applications. The market report provides an unbiased and detailed analysis of ongoing market trends, opportunities/high growth areas, and market drivers, which would help stakeholders to devise and align their market strategies according to the current and future market dynamics.

Brazil Carbon Market Synopsis

Brazil Carbon Market is likely to grow during the forecast period due to the ongoing deforestation, forest recovery projects, and the expansion of renewable energy projects across the country. Carbon is a versatile chemical element (symbol C) that exists in several forms, including graphite, carbon black, activated carbon, and diamond. The Brazil Carbon Market is poised for major development, bolstered by the Brazilian government's initiatives to battle deforestation and encourage sustainable development.

Evaluation of Growth Drivers in the Brazil Carbon Market

Below mentioned are some prominent drivers and their influence to the market dynamics:

|

Drivers |

Primary Segments Affected |

Why it Matters (Evidence) |

|

EV & Battery Supply Chain Localization |

Graphite; Automotive, Others (Energy Storage) |

OEM and cell manufacturing announcements bolster requirement for natural and synthetic graphite anodes, conductive additives. Also, specialty carbons as well to encourage domestic battery ecosystem buildout. |

|

Steel & Metallurgy Expansion |

Amorphous Carbon & Graphite; Engineering Industries |

Development in electric arc furnaces and alloy production increases usage of carbon electrodes, recarburizers, and refractories. |

|

Lightweighting in Mobility |

Graphite & Diamond (coatings/tools); Automotive, Aerospace |

Push to minimize vehicle weight boosts advanced carbon composites, friction materials, and diamond-coated tooling for precision machining. |

|

Thermal & Electrical Applications |

Graphite; Construction, Engineering Industries |

Electrification and industrial heat management boost the use of graphite sheets, gaskets, and conductive components in buildings and plants. |

|

Government Industrial Programs |

All product types; Automotive, Engineering Industries, Aerospace |

Policy encouragement for advanced manufacturing and local content promotes investment in carbon materials processing and high-performance applications. |

The Brazil Carbon Market size is projected to grow at the CAGR of 6.7% during the forecast period of 2025-2031. One of the leading drivers behind the Brazil Carbon Market is the country's progressive legal framework and regulatory environment that encourages sustainable development. Brazil's environmental regulations and policies have made it an attractive destination for investors looking for sustainable development opportunities.

Various companies are allocating money in renewable energy and forest conservation projects. Additionally, this helps the Brazil Carbon Industry to remain attractive to international investors wanting to offset their emissions and provide to mitigating climate change. Despite the challenges that the Brazilian government and market participants encounter, the long-term outlook for market growth remains promising.

Evaluation of Restraints in the Brazil Carbon Market

Below mentioned are some major restraints and their influence to the market dynamics:

|

Restraints |

Primary Segments Affected |

What this Means (Evidence) |

|

Price Volatility of Raw Materials |

Graphite & Amorphous Carbon; All applications |

Changes in coke/needle coke and natural flake graphite costs impact production planning and margins for electrode and anode manufacturers. |

|

Technology & Qualification Barriers |

Diamond & Advanced Graphite; Aerospace, Automotive |

Stringent qualification cycles and certification requirements increase time-to-market for high-spec carbon components. |

|

Environmental Compliance Costs |

New installs; all product types |

Emission controls, mining permits, and waste handling increase compliance prices, especially for processing and beneficiation resources. |

|

Import Dependence on Specialty Grades |

Graphite & Diamond; High-end applications |

Dependency on imported high-purity graphite and synthetic diamond tools forms supply-network vulnerabilities and longer lead times. |

|

Skilled Workforce Gaps |

All product types; Engineering Industries, Aerospace |

Insufficient pool of experienced composite technicians, coating specialists, and process engineers restricts increasing capacity scaling. |

Brazil Carbon Market Challenges

Despite the growing demand, the Brazil Carbon Market goes through numerous challenges. The Paris Climate Accord, which is a global treaty adopted in 2015 to limit global warming and reduce greenhouse gas emissions is creating challenges for the market such as insufficient environmental law enforcement, forest fires, and climate change scepticism among some political leaders have obstructed Brazil's anti-deforestation efforts. The complexity of the carbon market system and the lack of established methodologies to measure the environmental impact of carbon offset projects are also significant issues.

Brazil Carbon Market Trends

Several prominent trends reshaping the market landscape consist of:

Hybrid Carbon-Composite Systems: Increasing use of graphite, carbon fiber, and resin hybrids for automotive structures and aerospace interiors to balance stiffness, weight, and cost.

Battery-Grade Purification & Spheronization: Accelerated investment in midstream resources for purified, coated spherical graphite. They are customised for local cell makers.

IoT-Enabled Process Control: Broader adoption of smart kilns, furnaces, and coating lines with remote supervision to optimize yield, energy, and product consistency.

Diamond Coatings for Tool Life: Increasing deployment of CVD diamond and DLC coatings on cutting tools and molds. This is being done to expand life in machining lightweight alloys and composites.

Circularity & By-product Valorization: Advancement in electrode recycling, pitch/coke by-product recovery, and reprocessing scrap graphite into conductive additives.

Investment Opportunities in the Brazil Carbon Industry

Some prominent investment opportunities in the market consist of:

Anode-Grade Graphite Processing Hubs – Build purification, spheronization, and coating lines proximate to graphite deposits and port infrastructure. This can be done to serve to EV battery makers.

Refractories & Electrode Upgrades – Modernize EAF electrode and refractory plants with energy-efficient furnaces and advanced QC. Additionally it will help to cater expanding steel output.

Diamond Tooling & Coatings – Establish localized CVD/DLC coating services and precision tool manufacturing targeting automotive, aerospace, and die & mold clusters.

Thermal Management Solutions – Develop graphite films, gaskets, and heat spreaders for electronics, industrial HVAC, and high-temperature process industries.

Top 5 Leading Players in the Brazil Carbon Market

Some leading players operating in the market include:

Nacional de Grafite Ltda

Established Year: 1939

Headquarters: Itapecerica, Minas Gerais, Brazil

Official Website: https://www.grafite.com.br

A leading Brazilian producer of natural graphite, delivering various grades for refractories, lubricants, and battery-related applications with combined mining and processing.

SGL Carbon SE

Established Year: 1992

Headquarters: Wiesbaden, Germany

Official Website: https://www.sglcarbon.com

Worldwide supplier of graphite materials, carbon composites, and specialty graphites serving Brazil’s metallurgy, automotive, and industrial sectors.

GrafTech International

Established Year: 1886

Headquarters: Brooklyn Heights, Ohio, USA

Official Website: https://www.graftech.com

Leading producer of graphite electrodes and related products utilised in electric arc furnace steelmaking, supporting customers across Latin America including Brazil.

Petrobras

Established Year: 1953

Headquarters: Rio de Janeiro, Brazil

Official Website: https://petrobras.com.br

Integrated energy company offering key feedstocks (e.g., pitches, cokes) and partnering in industrial chains prevalent to carbon materials and electrodes.

Hexcel Corporation

Established Year: 1948

Headquarters: Stamford, Connecticut, USA

Official Website: https://www.hexcel.com

Developer of advanced carbon fiber composites and honeycombs used in aerospace and high-performance automotive, supporting Brazilian aerospace supply networks.

Government Regulations Introduced in the Brazil Carbon Market

According to Brazilian government data, several initiatives to increase the Brazil Carbon Market Growth have been implemented by Brazilian government. The government has made the Brazilian Carbon Credit Unit (CBio), a financial instrument that gives incentives for greenhouse gas emission minimization activities. In 2020, the Brazilian government also launched the Sustainable Agriculture Program. This programme has the objective to promote sustainable practices in agriculture.

Future Insights of the Brazil Carbon Market

The future of the Brazil Carbon Market looks promising, with more investors identifying the opportunities that await. The execution of a carbon tax may motivate domestic companies to minimize their emissions. Brazil’s large potential for bio-energy, renewable energy, and sustainable land use also gives a major opportunity for investors wanting to minimize carbon emissions. All these advancements point to continued overall growth, making the market a force to reckon with.

Market Segmentation Analysis

The report offers a comprehensive study of the subsequent market segments and their leading categories.

Graphite to Dominate the Market – By Product Types

According to Parth, Senior Research Analyst at 6Wresearch, the graphite category holds the largest Brazil carbon Market Share. The country’s sizable natural graphite resources, integrated with increasing requirement for EAF electrodes, refractories, and battery anodes, firmly position graphite ahead of amorphous carbon and diamond.

Automotive to Dominate the Market– By Applications

The Automotive segment dominates the Brazil Carbon Industry, proliferated by vehicle lightweighting, friction materials (brakes, clutches), thermal management components, and increasing localization of battery value networks.

Key Attractiveness of the Report

- 10 Years of Market Numbers.

- Historical Data Starting from 2021 to 2024.

- Base Year: 2024.

- Forecast Data until 2031.

- Key Performance Indicators Impacting the Market.

- Major Upcoming Developments and Projects.

Key Highlights of the Report:

- Brazil Carbon Market Overview

- Brazil Carbon Market Outlook

- Market Size of Brazil Carbon Market, 2024

- Forecast of Brazil Carbon Market, 2031

- Historical Data and Forecast of Brazil Carbon Revenues & Volume for the Period 2021-2031

- Brazil Carbon Market Trend Evolution

- Brazil Carbon Market Drivers and Challenges

- Brazil Carbon Price Trends

- Brazil Carbon Porter's Five Forces

- Brazil Carbon Industry Life Cycle

- Historical Data and Forecast of Brazil Carbon Market Revenues & Volume By Product Types for the Period 2021-2031

- Historical Data and Forecast of Brazil Carbon Market Revenues & Volume By Amorphous Carbon for the Period 2021-2031

- Historical Data and Forecast of Brazil Carbon Market Revenues & Volume By Graphite for the Period 2021-2031

- Historical Data and Forecast of Brazil Carbon Market Revenues & Volume By Diamond for the Period 2021-2031

- Historical Data and Forecast of Brazil Carbon Market Revenues & Volume By Applications for the Period 2021-2031

- Historical Data and Forecast of Brazil Carbon Market Revenues & Volume By Automotive for the Period 2021-2031

- Historical Data and Forecast of Brazil Carbon Market Revenues & Volume By Construction for the Period 2021-2031

- Historical Data and Forecast of Brazil Carbon Market Revenues & Volume By Engineering Industries for the Period 2021-2031

- Historical Data and Forecast of Brazil Carbon Market Revenues & Volume By Aerospace for the Period 2021-2031

- Historical Data and Forecast of Brazil Carbon Market Revenues & Volume By Others for the Period 2021-2031

- Brazil Carbon Import Export Trade Statistics

- Market Opportunity Assessment By Product Types

- Market Opportunity Assessment By Applications

- Brazil Carbon Top Companies Market Share

- Brazil Carbon Competitive Benchmarking By Technical and Operational ParametersBrazil Carbon Company Profiles

- Brazil Carbon Key Strategic Recommendations

Market Covered

The report offers a comprehensive study of the subsequent market segments:

By Product Types

- Amorphous Carbon

- Graphite

- Diamond

By Applications

- Automotive

- Construction

- Engineering Industries

- Aerospace

- Others

Brazil Carbon Market (2025-2031): FAQs

The Brazil Carbon Market is projected to grow at a CAGR of approximately 6.7% during the forecast period.

Major drivers consist of Brazil’s renewable energy expansion and corporate initiatives to meet net-zero targets.

Programs such as PNMC-aligned industrial measures, and financing from BNDES/Finep encourage efficiency, innovation, and capacity buildout in carbon processing and applications.

Challenges consist of insufficient of standardized regulations, changing carbon credit pricing, risks of greenwashing, and monitoring difficulties in forest-based projects.

6Wresearch actively monitors the Brazil Carbon Market and publishes its comprehensive annual report, highlighting emerging trends, growth drivers, revenue analysis, and forecast outlook. Our insights help businesses to make data-backed strategic decisions with ongoing market dynamics. Our analysts track relevent industries related to the Brazil Carbon Market, allowing our clients with actionable intelligence and reliable forecasts tailored to emerging regional needs.

Yes, we provide customisation as per your requirements. To learn more, feel free to contact us on sales@6wresearch.com

| Table of Contents |

| 1. Executive Summary |

| 2. Introduction |

| 2.1. Key Highlights of the Report |

| 2.2. Report Description |

| 2.3. Market Scope & Segmentation |

| 2.4. Research Methodology |

| 2.5. Assumptions |

| 3. Brazil Carbon Market Overview |

| 3.1. Brazil Country Macro Economic Indicators |

| 3.2. Brazil Carbon Market Revenues & Volume, 2021 & 2031F |

| 3.3. Brazil Carbon Market - Industry Life Cycle |

| 3.4. Brazil Carbon Market - Porter's Five Forces |

| 3.5. Brazil Carbon Market Revenues & Volume Share, By Product Types, 2021 & 2031F |

| 3.6. Brazil Carbon Market Revenues & Volume Share, By Applications, 2021 & 2031F |

| 4. Brazil Carbon Market Dynamics |

| 4.1. Impact Analysis |

| 4.2. Market Drivers |

| 4.2.1 Government initiatives and regulations promoting carbon reduction efforts |

| 4.2.2 Increasing awareness and concern about climate change among businesses and consumers |

| 4.2.3 Growing demand for renewable energy sources and sustainable practices in Brazil |

| 4.3. Market Restraints |

| 4.3.1 Challenges in implementing and enforcing carbon pricing mechanisms |

| 4.3.2 Lack of comprehensive data and monitoring systems for carbon emissions |

| 4.3.3 Economic uncertainty and fluctuations affecting investments in carbon reduction projects |

| 5. Brazil Carbon Market Trends |

| 6. Brazil Carbon Market, By Types |

| 6.1. Brazil Carbon Market, By Product Types |

| 6.1.1 Overview and Analysis |

| 6.1.2. Brazil Carbon Market Revenues & Volume, By Product Types, 2021-2031F |

| 6.1.3. Brazil Carbon Market Revenues & Volume, By Amorphous Carbon, 2021-2031F |

| 6.1.4. Brazil Carbon Market Revenues & Volume, By Graphite, 2021-2031F |

| 6.1.5. Brazil Carbon Market Revenues & Volume, By Diamond, 2021-2031F |

| 6.2. Brazil Carbon Market, By Applications |

| 6.2.1. Overview and Analysis |

| 6.2.2. Brazil Carbon Market Revenues & Volume, By Automotive, 2021-2031F |

| 6.2.3. Brazil Carbon Market Revenues & Volume, By Construction, 2021-2031F |

| 6.2.4. Brazil Carbon Market Revenues & Volume, By Engineering Industries, 2021-2031F |

| 6.2.5. Brazil Carbon Market Revenues & Volume, By Aerospace, 2021-2031F |

| 6.2.6. Brazil Carbon Market Revenues & Volume, By Others, 2021-2031F |

| 7. Brazil Carbon Market Import-Export Trade Statistics |

| 7.1 Brazil Carbon Market Export to Major Countries |

| 7.2. Brazil Carbon Market Imports from Major Countries |

| 8. Brazil Carbon Market Key Performance Indicators |

| 8.1 Carbon offset prices in the Brazilian market |

| 8.2 Number of companies participating in carbon trading schemes |

| 8.3 Investments in renewable energy projects in Brazil |

| 8.4 Carbon emissions reduction targets set by Brazilian companies |

| 8.5 Adoption rate of sustainable practices and technologies in key industries in Brazil |

| 9. Brazil Carbon Market - Opportunity Assessment |

| 9.1. Brazil Carbon Market Opportunity Assessment, By Product Types, 2021 & 2031F |

| 9.2. Brazil Carbon Market Opportunity Assessment, By Applications, 2021 & 2031F |

| 10. Brazil Carbon Market - Competitive Landscape |

| 10.1. Brazil Carbon Market Revenue Share, By Companies, 2024 |

| 10.2. Brazil Carbon Market Competitive Benchmarking, By Operating and Technical Parameters |

| 11. Company Profiles |

| 12. Recommendations |

| 13. Disclaimer |

Global Go To Market Strategy - 2030

Export potential enables firms to identify high-growth global markets with greater confidence by combining advanced trade intelligence with a structured quantitative methodology. The framework analyzes emerging demand trends and country-level import patterns while integrating macroeconomic and trade datasets such as GDP and population forecasts, bilateral import–export flows, tariff structures, elasticity differentials between developed and developing economies, geographic distance, and import demand projections. Using weighted trade values from 2020–2024 as the base period to project country-to-country export potential for 2030, these inputs are operationalized through calculated drivers such as gravity model parameters, tariff impact factors, and projected GDP per-capita growth. Through an analysis of hidden potentials, demand hotspots, and market conditions that are most favorable to success, this method enables firms to focus on target countries, maximize returns, and global expansion with data, backed by accuracy.

By factoring in the projected importer demand gap that is currently unmet and could be potential opportunity, it identifies the potential for the Exporter (Country) among 190 countries, against the general trade analysis, which identifies the biggest importer or exporter.

To discover high-growth global markets and optimize your business strategy:

Click Here

Pricing

- Single User License$ 1,995

- Department License$ 2,400

- Site License$ 3,120

- Global License$ 3,795

Leadership Perspectives from Industry Events

Search

6Wresearch in the News

Forbes

Forbes

Citing 6Wresearch analytics to map global infrastructure and pharmaceutical industry trajectories.

Bloomberg Law

Bloomberg Law

Direct syndication of 6Wresearch's macro data points, capturing complex supply chain shifts.

Reuters

Reuters

Tracking industrial manufacturing adjustments and electronic security ecosystem scaling.

Mint

Mint

Utilizing deep-tech sector market sizing to analyze global automation and robotics.

The Economic Times

The Economic Times

Anchoring features on industrial IoT growth metrics and connected smart-grid devices.

Business Standard

Business Standard

Featuring strategic evaluations of Advanced Driver Assistance Systems (ADAS) and AI road safety.

The Hindu

The Hindu

Spotlighting core commercial metrics ranging from unmanned aerial vehicles (UAVs) to consumer durables.

Financial Express

Financial Express

Anchoring quarterly reviews on cross-border real estate tech and structural hardware manufacturing.

Yahoo Finance

Yahoo Finance

Syndicating the tracker's $30.1 billion untapped-market findings, spotlighting Japan, the US and China as India's top new-potential importers.

India Today

India Today

Carrying the release on smartphones leading India's export potential to $94 billion by 2031, per 6WExportGTM data.

Dailyhunt

Dailyhunt

Distributing the tracker findings to its regional readership, framing India's export diversification into Japan and Mexico.

PR Newswire Original release

PR Newswire Original release

Publishing the full India Export Attractiveness Tracker 2026, detailing new trade corridors across iron ore, LCVs and pharmaceuticals.

The Industrial

The Industrial

Highlighting the tracker's read on India's semiconductor ambitions and long-term chip-assembly export potential.

PTI News

PTI News

Reporting on the $66.81 billion pharmaceuticals export opportunity flagged in the tracker, amid looming US generic-drug tariffs.

Tribune India

Tribune India

Covering the tracker's tariff-versus-regulation analysis across India's mature export markets in the US, China and UAE.

ANI News

ANI News

Amplifying the report's findings on polished diamonds, refined petroleum and medicines as India's core export engines.

International Business Magazine

International Business Magazine

Covering the report's insight into how AEB, blind spot detection, and driver monitoring are reshaping India's ADAS market.

Focus Gaming News

Focus Gaming News

Highlighting the research forecast for Egypt's gambling market, projecting steady growth through 2032.

Thought Leadership and Analyst Meet

Our Clients

Latest Reports

- Poland Engine Ignition Components Market (2026-2032)

- Peru Engine Ignition Components Market (2026-2032)

- Pakistan Engine Ignition Components Market (2026-2032)

- Oman Engine Ignition Components Market (2026-2032)

- Nigeria Engine Ignition Components Market (2026-2032)

- Nepal Engine Ignition Components Market (2026-2032)

- Myanmar Engine Ignition Components Market (2026-2032)

- Morocco Engine Ignition Components Market (2026-2032)

- Mexico Engine Ignition Components Market (2026-2032)

- Malaysia Engine Ignition Components Market (2026-2032)

Industry Events and Analyst Meet

EV India Expo 2026

HIMTEX 2026

India Refining Summit 2026

India EV Show 2026

EV tech India Expo 2026

Whitepaper

- Middle East & Africa Commercial Security Market Click here to view more.

- Middle East & Africa Fire Safety Systems & Equipment Market Click here to view more.

- GCC Drone Market Click here to view more.

- Middle East Lighting Fixture Market Click here to view more.

- GCC Physical & Perimeter Security Market Click here to view more.