Bulgaria Gas Market (2025-2031) | Industry, Companies, Share, Segmentation, Value, Size & Revenue, Analysis, Outlook, Growth, Trends, Forecast, Competitive Landscape

Market Forecast By Application (Utilities, Industrial, Commercial) And Competitive Landscape

| Product Code: ETC6549200 | Publication Date: Sep 2024 | Updated Date: Oct 2025 | Product Type: Market Research Report | |

| Publisher: 6Wresearch | Author: Dhaval Chaurasia | No. of Pages: 75 | No. of Figures: 35 | No. of Tables: 20 |

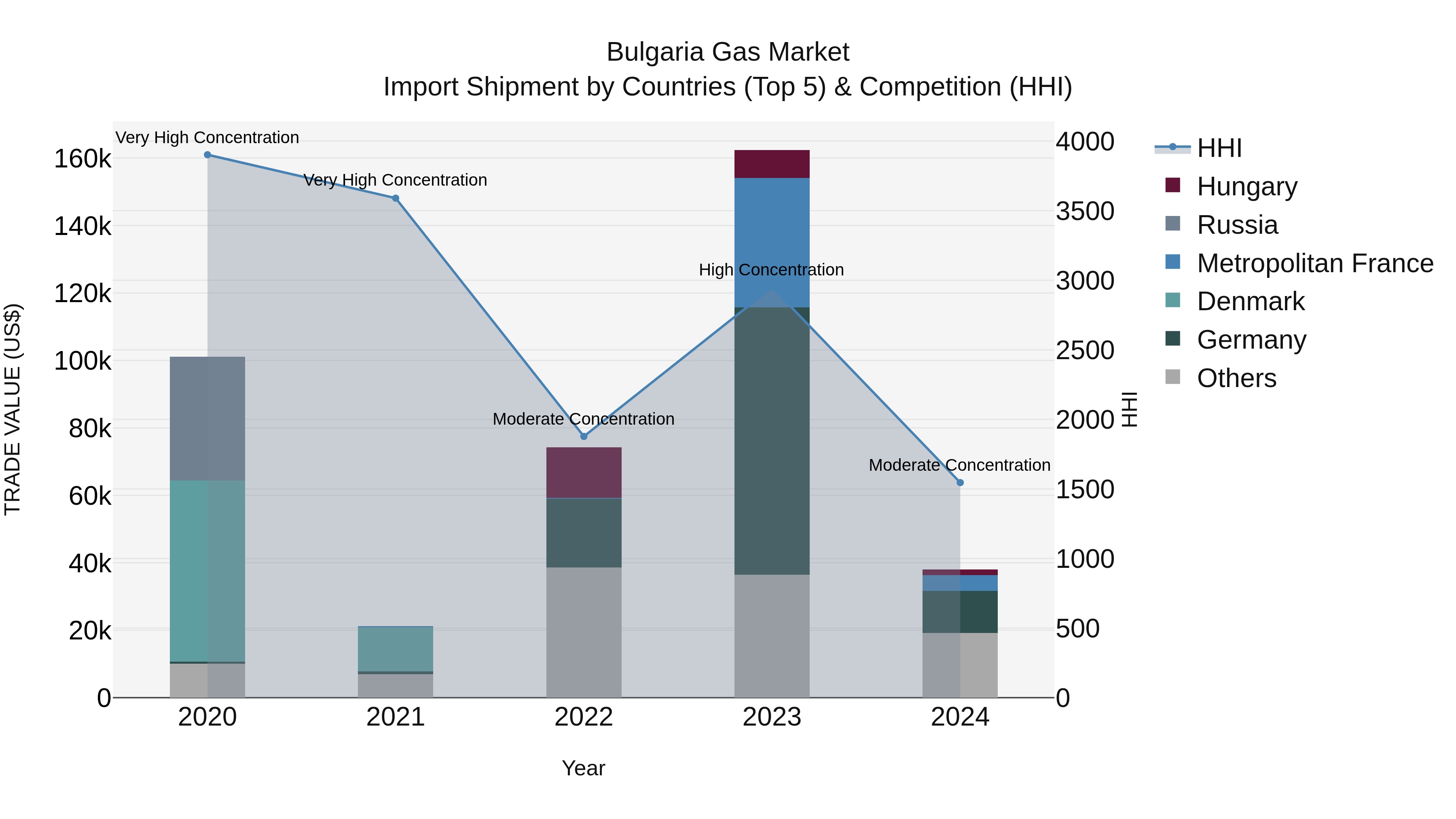

Bulgaria Gas Market Top 5 Importing Countries and Market Competition (HHI) Analysis

Bulgaria`s gas import shipments in 2024 showed diversification with top exporting countries being Germany, Austria, Metropolitan France, Italy, and Romania. The Herfindahl-Hirschman Index (HHI) indicated a shift from very high concentration in 2023 to a more moderate level in 2024, reflecting a more balanced Market Top 5 Importing Countries and Market Competition (HHI) Analysis . The compound annual growth rate (CAGR) for gas imports from 2020 to 2024 was -21.65%, while the growth rate in 2024 experienced a significant decline of -76.55%. These trends suggest a changing landscape in Bulgaria`s gas import Market Top 5 Importing Countries and Market Competition (HHI) Analysis with implications for future strategies and partnerships.

Bulgaria Gas Market Synopsis

The Bulgaria Gas Market is characterized by a mix of domestic production, imports, and consumption. The country produces natural gas from its own reserves but heavily relies on imports from Russia, with Gazprom being a major supplier. The market is dominated by state-owned companies, with Bulgargaz holding a monopoly on gas imports and distribution. Recent efforts have been made to diversify gas sources and improve infrastructure to enhance security of supply and promote competition. Bulgaria is also investing in interconnectors with neighboring countries to further diversify its gas supply routes. The market is regulated by the State Energy and Water Regulatory Commission (SEWRC) to ensure fair competition and consumer protection. Overall, the Bulgaria Gas Market is in a phase of transition towards a more competitive and secure energy landscape.

Bulgaria Gas Market Trends

The Bulgaria Gas Market is currently experiencing a shift towards greater diversification and integration with the European energy market. The country is investing in infrastructure development to enhance its gas storage capacity and interconnections with neighboring countries, such as Greece and Romania. With the increasing focus on sustainability and renewable energy sources, there are opportunities for the expansion of natural gas as a cleaner alternative to coal in Bulgaria`s energy mix. Furthermore, the liberalization of the gas market is creating opportunities for new players to enter and compete, leading to greater market efficiency and potentially lower prices for consumers. Overall, the Bulgaria Gas Market presents opportunities for investment in infrastructure, innovation in cleaner energy solutions, and increased competition in a maturing market.

Bulgaria Gas Market Challenges

The Bulgaria Gas Market faces several challenges, including dependence on imports from Russia, lack of infrastructure for gas storage and transmission, regulatory uncertainties, and limited competition in the market. The heavy reliance on Russian gas exposes the market to geopolitical risks and pricing fluctuations. The insufficient infrastructure hinders the diversification of gas sources and limits the market`s flexibility to respond to supply disruptions. Regulatory uncertainties create barriers to investment in the sector, while the lack of competition results in higher prices and reduced incentives for innovation. Addressing these challenges will be crucial for the Bulgaria Gas Market to enhance security of supply, promote competition, and achieve sustainability in the long term.

Bulgaria Gas Market Investment Opportunities

The Bulgaria Gas Market is primarily driven by factors such as increasing energy demand, economic growth, government policies promoting gas as a cleaner alternative to coal, and the country`s strategic location as a key transit hub for natural gas in Southeast Europe. Additionally, the diversification of gas supply sources, including the development of liquefied natural gas (LNG) terminals and interconnectors with neighboring countries, plays a significant role in driving market growth. The implementation of infrastructure projects, such as the Balkan Gas Hub and the Greece-Bulgaria Interconnector, further contribute to the expansion and integration of the Bulgaria Gas Market within the broader European gas market landscape. Overall, these drivers are expected to continue shaping the future development and competitiveness of the Bulgarian gas sector.

Bulgaria Gas Market Government Polices

Government policies related to the Bulgaria Gas Market focus on increasing competition, enhancing security of supply, and ensuring regulatory oversight. The government has implemented measures to promote market liberalization, encourage investment in infrastructure, and diversify gas sources to reduce dependency on single suppliers. Bulgaria has committed to aligning its gas market regulations with EU directives to foster a more transparent and efficient market structure. Additionally, the government has adopted initiatives to improve energy efficiency, promote renewable energy sources, and advance towards decarbonization goals. Regulatory bodies such as the Energy and Water Regulatory Commission (EWRC) oversee the implementation and enforcement of these policies to ensure fair competition and consumer protection in the gas market.

Bulgaria Gas Market Future Outlook

The Bulgaria Gas Market is expected to experience steady growth in the coming years, driven by factors such as increasing demand for natural gas in industries, households, and power generation. The country`s strategic location as a key transit hub for gas supplies in Southeast Europe further enhances its position in the market. Investments in infrastructure projects, such as the construction of interconnectors and LNG terminals, will also contribute to the market`s development. Additionally, Bulgaria`s efforts to diversify its gas supply sources and reduce its dependence on a single supplier will play a crucial role in shaping the future of the market. Overall, the Bulgaria Gas Market is forecasted to remain resilient and continue its upward trajectory in terms of consumption, infrastructure development, and market competitiveness.

Key Highlights of the Report:

- Bulgaria Gas Market Outlook

- Market Size of Bulgaria Gas Market, 2024

- Forecast of Bulgaria Gas Market, 2031

- Historical Data and Forecast of Bulgaria Gas Revenues & Volume for the Period 2021- 2031

- Bulgaria Gas Market Trend Evolution

- Bulgaria Gas Market Drivers and Challenges

- Bulgaria Gas Price Trends

- Bulgaria Gas Porter's Five Forces

- Bulgaria Gas Industry Life Cycle

- Historical Data and Forecast of Bulgaria Gas Market Revenues & Volume By Application for the Period 2021- 2031

- Historical Data and Forecast of Bulgaria Gas Market Revenues & Volume By Utilities for the Period 2021- 2031

- Historical Data and Forecast of Bulgaria Gas Market Revenues & Volume By Industrial for the Period 2021- 2031

- Historical Data and Forecast of Bulgaria Gas Market Revenues & Volume By Commercial for the Period 2021- 2031

- Bulgaria Gas Import Export Trade Statistics

- Market Opportunity Assessment By Application

- Bulgaria Gas Top Companies Market Share

- Bulgaria Gas Competitive Benchmarking By Technical and Operational Parameters

- Bulgaria Gas Company Profiles

- Bulgaria Gas Key Strategic Recommendations

Frequently Asked Questions About the Market Study (FAQs):

6Wresearch actively monitors the Bulgaria Gas Market and publishes its comprehensive annual report, highlighting emerging trends, growth drivers, revenue analysis, and forecast outlook. Our insights help businesses to make data-backed strategic decisions with ongoing market dynamics. Our analysts track relevent industries related to the Bulgaria Gas Market, allowing our clients with actionable intelligence and reliable forecasts tailored to emerging regional needs.

Yes, we provide customisation as per your requirements. To learn more, feel free to contact us on sales@6wresearch.com

1 Executive Summary |

2 Introduction |

2.1 Key Highlights of the Report |

2.2 Report Description |

2.3 Market Scope & Segmentation |

2.4 Research Methodology |

2.5 Assumptions |

3 Bulgaria Gas Market Overview |

3.1 Bulgaria Country Macro Economic Indicators |

3.2 Bulgaria Gas Market Revenues & Volume, 2021 & 2031F |

3.3 Bulgaria Gas Market - Industry Life Cycle |

3.4 Bulgaria Gas Market - Porter's Five Forces |

3.5 Bulgaria Gas Market Revenues & Volume Share, By Application, 2021 & 2031F |

4 Bulgaria Gas Market Dynamics |

4.1 Impact Analysis |

4.2 Market Drivers |

4.2.1 Increasing demand for natural gas in Bulgaria due to economic growth and industrial development. |

4.2.2 Government initiatives to promote cleaner energy sources, including natural gas, to reduce carbon emissions. |

4.2.3 Infrastructure development projects to improve gas distribution networks and storage facilities in Bulgaria. |

4.3 Market Restraints |

4.3.1 Price volatility of natural gas in the global market impacting the cost of imports in Bulgaria. |

4.3.2 Regulatory challenges and uncertainties in the energy sector affecting investment decisions. |

4.3.3 Competition from alternative energy sources such as renewable energy impacting the market share of natural gas. |

5 Bulgaria Gas Market Trends |

6 Bulgaria Gas Market, By Types |

6.1 Bulgaria Gas Market, By Application |

6.1.1 Overview and Analysis |

6.1.2 Bulgaria Gas Market Revenues & Volume, By Application, 2021- 2031F |

6.1.3 Bulgaria Gas Market Revenues & Volume, By Utilities, 2021- 2031F |

6.1.4 Bulgaria Gas Market Revenues & Volume, By Industrial, 2021- 2031F |

6.1.5 Bulgaria Gas Market Revenues & Volume, By Commercial, 2021- 2031F |

7 Bulgaria Gas Market Import-Export Trade Statistics |

7.1 Bulgaria Gas Market Export to Major Countries |

7.2 Bulgaria Gas Market Imports from Major Countries |

8 Bulgaria Gas Market Key Performance Indicators |

8.1 Number of new gas connections installed in residential, commercial, and industrial sectors. |

8.2 Percentage increase in natural gas consumption in Bulgaria annually. |

8.3 Investment in infrastructure projects for gas distribution and storage capacity expansion. |

8.4 Number of regulatory approvals and policy changes impacting the gas market. |

8.5 Average price of natural gas in Bulgaria compared to global market trends. |

9 Bulgaria Gas Market - Opportunity Assessment |

9.1 Bulgaria Gas Market Opportunity Assessment, By Application, 2021 & 2031F |

10 Bulgaria Gas Market - Competitive Landscape |

10.1 Bulgaria Gas Market Revenue Share, By Companies, 2024 |

10.2 Bulgaria Gas Market Competitive Benchmarking, By Operating and Technical Parameters |

11 Company Profiles |

12 Recommendations |

13 Disclaimer |

Export potential assessment - trade Analytics for 2030

Export potential enables firms to identify high-growth global markets with greater confidence by combining advanced trade intelligence with a structured quantitative methodology. The framework analyzes emerging demand trends and country-level import patterns while integrating macroeconomic and trade datasets such as GDP and population forecasts, bilateral import–export flows, tariff structures, elasticity differentials between developed and developing economies, geographic distance, and import demand projections. Using weighted trade values from 2020–2024 as the base period to project country-to-country export potential for 2030, these inputs are operationalized through calculated drivers such as gravity model parameters, tariff impact factors, and projected GDP per-capita growth. Through an analysis of hidden potentials, demand hotspots, and market conditions that are most favorable to success, this method enables firms to focus on target countries, maximize returns, and global expansion with data, backed by accuracy.

By factoring in the projected importer demand gap that is currently unmet and could be potential opportunity, it identifies the potential for the Exporter (Country) among 190 countries, against the general trade analysis, which identifies the biggest importer or exporter.

To discover high-growth global markets and optimize your business strategy:

Click Here

Pricing

- Single User License$ 1,995

- Department License$ 2,400

- Site License$ 3,120

- Global License$ 3,795

Search

Thought Leadership and Analyst Meet

Our Clients

Latest Reports

- Canada Cloud CFD Market (2026-2032) | Size & Revenue, Industry, Growth, Competitive Landscape, Forecast, Segmentation, Value, Outlook, Trends, Share, Analysis, Companies

- Taiwan Food Delivery Platform Market (2026-2032) | Companies, Outlook, Analysis, Trends, Value, Revenue, Segmentation, Share, Forecast, Competitive Landscape, Growth, Size & Forecast

- United Kingdom (UK) Long-term Care Insurance Market (2026-2032) | Growth, Share, Consumer Insights, Drivers, Opportunities, Competition, Pricing Analysis, Segments, Restraints, Companies, Competitive, Value, Outlook, Size, Demand, Analysis, Challenges, Strategic Insights, Investment Trends, Revenue, Trends, Supply, Forecast

- United Kingdom (UK) Long Term Care Market (2026-2032) | Companies, Outlook, Analysis, Trends, Value, Revenue, Segmentation, Share, Forecast, Competitive Landscape, Growth, Size & Forecast

- Iraq Insulation and Waterproofing Market (2026-2032) | Outlook, Drivers, Growth, Size, Share, Industry, Revenue, Trends, Demand, Competitive, Strategic Insights, Opportunities, Segments, Companies, Challenges, Strategy, Consumer Insights, Analysis, Investment Trends, Value, Segmentation, Forecast, Restraints

- India Switchgear Market Outlook (2026-2032) | Size, Share, Trends, Growth, Revenue, Forecast, Analysis, Value, Outlook

- Pakistan Contraceptive Implants Market (2025-2031) | Demand, Growth, Size, Share, Industry, Pricing Analysis, Competitive, Strategic Insights, Strategy, Consumer Insights, Analysis, Investment Trends, Opportunities, Revenue, Segments, Value, Segmentation, Supply, Forecast, Restraints, Outlook, Competition, Drivers, Trends, Companies, Challenges

- Sri Lanka Packaging Market (2026-2032) | Outlook, Competition, Drivers, Trends, Demand, Pricing Analysis, Competitive, Strategic Insights, Companies, Challenges, Strategy, Consumer Insights, Analysis, Investment Trends, Opportunities, Growth, Size, Share, Industry, Revenue, Segments, Value, Segmentation, Supply, Forecast, Restraints

- India Kids Watches Market (2026-2032) | Strategy, Consumer Insights, Analysis, Investment Trends, Opportunities, Growth, Size, Share, Industry, Revenue, Segments, Value, Segmentation, Supply, Forecast, Restraints, Outlook, Competition, Drivers, Trends, Demand, Pricing Analysis, Competitive, Strategic Insights, Companies, Challenges

- Saudi Arabia Core Assurance Service Market (2025-2031) | Strategy, Consumer Insights, Analysis, Investment Trends, Opportunities, Growth, Size, Share, Industry, Revenue, Segments, Value, Segmentation, Supply, Forecast, Restraints, Outlook, Competition, Drivers, Trends, Demand, Pricing Analysis, Competitive, Strategic Insights, Companies, Challenges

Industry Events and Analyst Meet

India EV Show 2026

EV tech India Expo 2026

Auto Tech Asia 2026

Battery Tech India 2026

Smart Production Solutions Guangzhou 2026

Whitepaper

- Middle East & Africa Commercial Security Market Click here to view more.

- Middle East & Africa Fire Safety Systems & Equipment Market Click here to view more.

- GCC Drone Market Click here to view more.

- Middle East Lighting Fixture Market Click here to view more.

- GCC Physical & Perimeter Security Market Click here to view more.

6WResearch In News

- Doha a strategic location for EV manufacturing hub: IPA Qatar

- Demand for luxury TVs surging in the GCC, says Samsung

- Empowering Growth: The Thriving Journey of Bangladesh’s Cable Industry

- Demand for luxury TVs surging in the GCC, says Samsung

- Video call with a traditional healer? Once unthinkable, it’s now common in South Africa

- Intelligent Buildings To Smooth GCC’s Path To Net Zero