China Beer Market (2025-2029) | Revenue, Value, Companies, Share, Outlook, Size, Trends, Analysis, Growth, Industry & Forecast

Market Forecast By Type (Lager, Ale, Stout & Porter, Malt, Others), By Category (Popular Price, Premium, Super Premium), By Packaging (Glass, PET Bottle, Metal Can, Others), By Production (Macro-brewery, Micro-brewery, Craft Brewery, Others) And Competitive Landscape

| Product Code: ETC048301 | Publication Date: Jan 2021 | Updated Date: Oct 2025 | Product Type: Report | |

| Publisher: 6Wresearch | Author: Ravi Bhandari | No. of Pages: 70 | No. of Figures: 35 | No. of Tables: 5 |

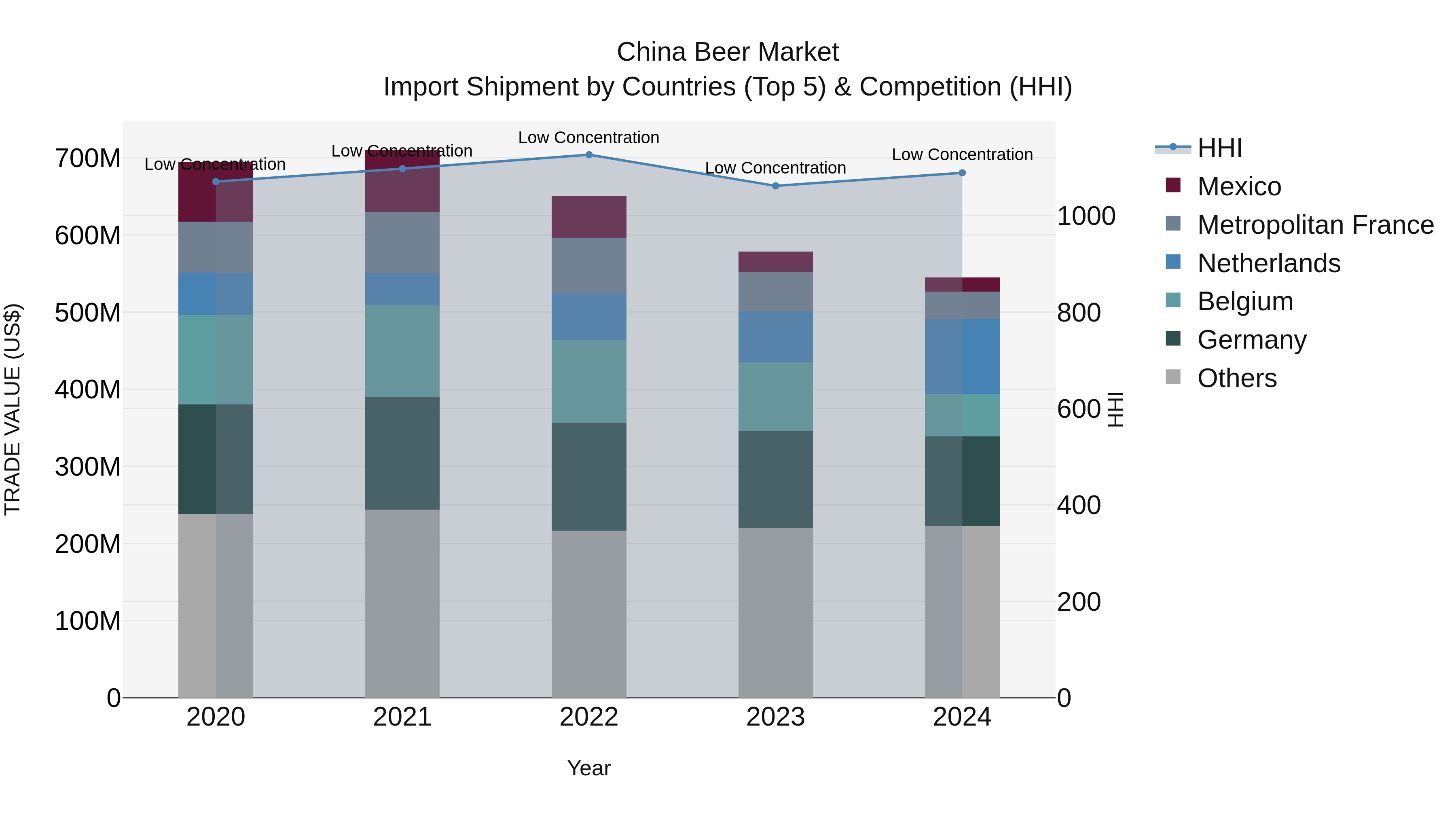

China Beer Market Top 5 Importing Countries and Market Competition (HHI) Analysis

Despite a negative CAGR and growth rate in 2024, China beer import market continues to be diversified, with top exporters including Germany, Netherlands, Belgium, Spain, and Metropolitan France. The low concentration level of the Herfindahl-Hirschman Index (HHI) indicates a competitive market environment, offering opportunities for various players to enter and compete. Continued interest from these key exporting countries suggests a stable demand for imported beers in China, with potential for further growth and product diversification in the future.

China Beer Market Highlights

| Report Name | China Beer Market |

| Forecast period | 2025-2029 |

| CAGR | 7.13% |

| Growing Sector | Premium Beer |

opics Covered in the China Beer Market Report

The China Beer Market report thoroughly covers the market by type, category, packaging, and by production. The market report provides an unbiased and detailed analysis of ongoing market trends, opportunities/high growth areas, and market drivers, to help stakeholders devise and align their market strategies according to current and future market dynamics.

China Beer Market Synopsis

The China Beer Market is projected to experience steady growth with increasing disposable incomes, a growing preference for premiumization (consumers willing to pay more for better quality or imported/brand name beers), expansion in craft and niche brewing, and increasing consumption in on trade channels (bars, restaurants). Domestic macro brewers still lead in volume, but smaller craft and premium brands are increasing their market share. The market also faces challenges from changing consumer tastes, regulatory/tax environments, and competition from other alcoholic beverages.

Evaluation of Growth Drivers in the China Beer Market

Below mentioned are some prominent drivers and their influence on the market dynamics:

| Driver | Primary Segments Affected | Why it matters (evidence) |

| Rising Middle‑Income Households & Premiumization | By Category: Premium & Super Premium; By Type: Lager, Imported / Specialty | As incomes grow, more consumers are trading up from standard / popular price beer to premium / super premium varieties. Budweiser APAC estimates that only ~17% of beer consumption is currently premium or above, but expects strong increase. |

| Growth of Craft & Micro‑breweries | Production: Craft Brewery, Micro‑brewery; By Type: Ale, Specialty | The craft segment is growing: over 10,000 craft breweries with annual production under 100,000 metric tons; craft beer holds about 8% of the domestic market. |

| Younger Consumer Preferences & Urbanization | By Category & Type; On‑trade channels | Younger consumers in cities are more experimental: demand for imported beers, seasonal / flavored / speciality beers, more frequent consumption out of home. |

| Packaging Efficiency & Sustainability | Packaging: Glass, Metal Can, Others | Brewers are optimizing packaging (light glass, increased recycled material, cans), to reduce cost and carbon footprint. CR Beer and others investing in lightweight glass bottle R&D and recycled aluminium cans. |

China beer market is projected to grow rapidly, growing at a growth rate of (CAGR) of 7.13% during the forecast period 2025–2029. The main drivers of the China beer market consist of rising disposable incomes, increasing demand for premium and craft beer, and evolving consumer preferences toward quality and unique flavors. Urbanization and a growing young adult population stimulate on-premise consumption. Government aid through relaxed microbrewery rules, tourism-based beer festivals, and domestic brand promotion further support China Beer Market Growth. Health-conscious trends also encourage the rise of low-alcohol and flavored beer options.

Evaluation of Restraints in the China Beer Market

Below mentioned are some major restraints and their influence on the market dynamics:

| Restraint | Primary Segments Affected | What this means (evidence) |

| Slowing Volume Growth & Saturation in Some Regions | Macro‑breweries, Popular Price Category | After years of expansion, volume consumption has stagnated or slightly declined in certain provinces/cities; population aging, lower growth in per capita consumption. |

| High Taxation & Regulatory Controls | Import / Super Premium Beers; Foreign Brands | Import duties, excise taxes, licensing, distribution regulations make it harder / more costly for foreign premium/super premium beers. |

| Health, Social, and Cultural Shifts | All Categories | Increasing awareness of health, moderate drinking, preference for lower‑alcohol or non‑alcoholic alternatives; competition from wine, spirits, RTDs etc. |

| Cost Inflation of Raw Materials & Packaging | All Producers, especially Craft | Rising costs of barley, hops, packaging material (glass, aluminium), energy etc., plus environmental regulation adding cost. |

China Beer Market Challenges

Although strong growth drivers exist, the China Beer Industry encounters notable challenges. Macro brewers suffer from overcapacity, while growing competition from imported beers and alternative beverages adds pressure. Environmental regulations, rising production costs, and evolving tax policies further burden operations. Craft breweries, while increasing in popularity, frequently face challenges in distribution, scalability, quality consistency, and licensing that can restrict their expansion and long-term sustainability in the market.

China Beer Market Trends

Several prominent trends reshaping the market growth include:

- Premiumization – more consumers are upgrading from standard/popular beers to premium and super premium brands. Producers are launching higher priced offerings, limited editions, imported beers, and gift packaging.

- Expansion of Craft & Microbreweries – more small scale breweries, offering niche/flavoured ales, seasonal beers; innovation in flavour, ingredients, style.

- Packaging Innovation & Sustainability – lighter glass bottles, cans, recycled materials, shifts from glass to aluminium / metal cans to reduce costs and environmental impact.

- On Trade Recovery & Experience Marketing – bars, pubs, restaurants regaining importance; themed bars, beer festivals; consumption in hospitality channels is driving demand for better quality.

- E commerce & Online Sales Channels – increased penetration of online sales, gift box packs, digital marketing, direct to consumer subscription or limited edition purchases.

Investment Opportunities in the China Beer Market

Several prominent opportunities reshaping the market growth include:

- Premium & Super Premium Brand Expansion – invest in brands that can command higher margins; imported or specialty beers; use limited editions and luxury packaging.

- Craft Brewery Growth & Acquisition – consolidate or invest in microbreweries; niche brands that appeal to younger / urban consumers.

- Sustainable Packaging & Supply Chain Innovation – develop lighter / recycled packaging; invest in processes that reduce carbon emissions, energy consumption.

- On Trade and Experiential Venues – create beer bars, brewpubs, taprooms, beer festivals; experiential marketing for premium and specialty consumption.

- Digital & Online Platform Growth – leveraging e commerce, social media, digital marketplaces; limited edition drops; home delivery; subscription models.

Top 5 Leading Players of the China Beer Market

Following leading players significantly contribute to China beer market share are:

1. China Resources Snow Breweries (CR Snow)

| Company Name | China Resources Snow Breweries (CR Snow) |

|---|---|

| Established Year | 1993 |

| Headquarters | Beijing, China |

| Official Website | Click Here |

China Resources Snow Breweries is the largest beer company in China by sales volume. The company is best known for its flagship brand, Snow Beer, and serves a wide consumer base through its extensive distribution network across the country.

2. Tsingtao Brewery Co., Ltd.

| Company Name | Tsingtao Brewery Co., Ltd. |

|---|---|

| Established Year | 1903 |

| Headquarters | Qingdao, Shandong, China |

| Official Website | Click Here |

Tsingtao Brewery is one of the oldest and most internationally recognized Chinese beer brands. It combines German brewing techniques with local craftsmanship and exports to over 100 countries worldwide.

3. Budweiser Brewing Company APAC (Anheuser-Busch InBev)

| Company Name | Budweiser Brewing Company APAC (AB InBev) |

|---|---|

| Established Year | – |

| Headquarters | Shanghai, China |

| Official Website | Click Here |

A subsidiary of global giant AB InBev, Budweiser APAC focuses on the premium and super-premium segments in China. Its portfolio includes Budweiser, Stella Artois, and Corona, targeting younger and affluent consumers.

4. Beijing Yanjing Brewery Co., Ltd.

| Company Name | Beijing Yanjing Brewery Co., Ltd. |

|---|---|

| Established Year | 1980 |

| Headquarters | Beijing, China |

| Official Website | Click Here |

Yanjing Brewery is one of the major state-owned breweries in China, widely popular in northern regions. It produces a variety of beer products and is known for its competitive pricing and mass-market appeal.

5. Carlsberg China

| Company Name | Carlsberg China |

|---|---|

| Established Year | – |

| Headquarters | Kunming, Yunnan, China |

| Official Website | Click Here |

Carlsberg China, a subsidiary of Carlsberg Group, has grown significantly through regional acquisitions. It focuses on premiumization and local brand integration, with a strong presence in western and southwestern China.

Government Initiatives Introduced in the China Beer Market

According to Chinese Government Data, Local governments in China are relaxing licensing rules for microbreweries in areas such as Beijing and Shanghai to accommodate the increasing demand of craft beer. Concurrently, environmental rules are compelling breweries like CR Beer to implement sustainable packaging utilizing recycled materials and bottle return initiatives. Authorities are promoting domestic premium brands through festivals and trade events, while differential taxes and import levies affect the pricing competitiveness of local and imported beer products.

Future Insights of the China Beer Market

The China Beer Market Share is estimated to increase in coming years, particularly for premium & super premium categories, craft & microbreweries, metal can package, and e commerce/digital channels. The macro breweries will continue to supply popular price beer, but their growth in volume may be slower while value growth emerges in premium segments. Increasing consumer interest in flavor, quality, sustainable packaging, and experience will drive innovation. Also, imported beers will continue expanding in select urban markets. However, regulatory scrutiny, taxation, and competition from non beer alcoholic / non alcoholic alternatives may shape outcomes.

Market Segmentation Analysis

The report offers a comprehensive study of the subsequent market segments and their leading categories.

Lager to Dominate the Market– By Type

According to Guneet Kaur, Senior Research Analyst, 6Wresearch, “Lager is witnessing swift growth owing to its light, crisp flavor and high consumer preference in urban regions. Its widespread availability and suitability for various occasions make it a popular choice among young adults.”

Super Premium to Dominate the Market– By Category

Rising consumer interest in high-quality and exclusive beer options is driving the demand for super premium products. With increasing disposable incomes and exposure to global beer trends, consumers are shifting towards sophisticated tastes and unique brewing techniques in this segment.

Metal Can to Dominate the Market – By Packaging

Metal cans are gaining rapid traction due to their convenience, portability, and better preservation qualities. They offer longer shelf life, ease of recycling, and are favored for outdoor consumption, which aligns with the evolving lifestyles of modern beer consumers.

Craft Brewery to Dominate the Market – By Production

Craft breweries are rapidly expanding due to growing demand for artisanal and locally brewed beers. Consumers are increasingly drawn to unique flavors, small-batch quality, and brand authenticity, which gives this segment a distinct edge in the evolving beer market.

Key Attractiveness of the Report

- 10 Years of Market Numbers.

- Historical Data Starting from 2021 to 2024.

- Base Year: 2024.

- Forecast Data until 2029

- Key Performance Indicators Impacting the Market.

- Major Upcoming Developments and Projects.

Key Highlights of the Report:

- China Beer Market Outlook

- Market Size of China Beer Market, 2024

- Forecast of China Beer Market, 2029

- Historical Data and Forecast of China Beer Revenues & Volume for the Period 2019-2029

- China Beer Market Trend Evolution

- China Beer Market Drivers and Challenges

- China Beer Price Trends

- China Beer Porter's Five Forces

- China Beer Industry Life Cycle

- Historical Data and Forecast of China Beer Market Revenues & Volume By Type for the Period 2019-2029

- Historical Data and Forecast of China Beer Market Revenues & Volume By Lager for the Period 2019-2029

- Historical Data and Forecast of China Beer Market Revenues & Volume By Ale for the Period 2019-2029

- Historical Data and Forecast of China Beer Market Revenues & Volume By Stout & Porter for the Period 2019-2029

- Historical Data and Forecast of China Beer Market Revenues & Volume By Malt for the Period 2019-2029

- Historical Data and Forecast of China Beer Market Revenues & Volume By Others for the Period 2019-2029

- Historical Data and Forecast of China Beer Market Revenues & Volume By Category for the Period 2019-2029

- Historical Data and Forecast of China Beer Market Revenues & Volume By Popular Price for the Period 2019-2029

- Historical Data and Forecast of China Beer Market Revenues & Volume By Premium for the Period 2019-2029

- Historical Data and Forecast of China Beer Market Revenues & Volume By Super Premium for the Period 2019-2029

- Historical Data and Forecast of China Beer Market Revenues & Volume By Packaging for the Period 2019-2029

- Historical Data and Forecast of China Beer Market Revenues & Volume By Glass for the Period 2019-2029

- Historical Data and Forecast of China Beer Market Revenues & Volume By PET Bottle for the Period 2019-2029

- Historical Data and Forecast of China Beer Market Revenues & Volume By Metal Can for the Period 2019-2029

- Historical Data and Forecast of China Beer Market Revenues & Volume By Others for the Period 2019-2029

- Historical Data and Forecast of China Beer Market Revenues & Volume By Production for the Period 2019-2029

- Historical Data and Forecast of China Beer Market Revenues & Volume By Macro-brewery for the Period 2019-2029

- Historical Data and Forecast of China Beer Market Revenues & Volume By Micro-brewery for the Period 2019-2029

- Historical Data and Forecast of China Beer Market Revenues & Volume By Craft Brewery for the Period 2019-2029

- Historical Data and Forecast of China Beer Market Revenues & Volume By Others for the Period 2019-2029

- China Beer Import Export Trade Statistics

- Market Opportunity Assessment By Type

- Market Opportunity Assessment By Category

- Market Opportunity Assessment By Packaging

- Market Opportunity Assessment By Production

- China Beer Top Companies Market Share

- China Beer Competitive Benchmarking By Technical and Operational Parameters

- China Beer Company Profiles

- China Beer Key Strategic Recommendations

Market Covered

The report offers a comprehensive study of the subsequent market segments:

By Type

- Lager

- Ale

- Stout & Porter

- Malt

- Others

By Category

- Popular Price

- Premium

- Super Premium

By Packaging

- Glass

- PET Bottle

- Metal Can

- Others

By Production

- Macro Brewery

- Micro Brewery

- Craft Brewery

- Others

China Beer Market (2025-2029) : FAQ's

The China Beer Market is projected to grow at a CAGR of approximately 7.13%

during the forecast period 2025 2029

Lager dominates both in revenue and volume; it is also expected to register the fastest growth among types during the forecast period.

Glass bottles currently generate the most revenue; Metal cans are the fastest growing packaging segment owing to cost, recyclability, and convenience.

Macro breweries dominate in terms of production volume and reach; Craft Brewery / Micro breweries are growing fastest in niche, urban, and premium portfolios.

6Wresearch actively monitors the China Beer Market and publishes its comprehensive annual report, highlighting emerging trends, growth drivers, revenue analysis, and forecast outlook. Our insights help businesses to make data-backed strategic decisions with ongoing market dynamics. Our analysts track relevent industries related to the China Beer Market, allowing our clients with actionable intelligence and reliable forecasts tailored to emerging regional needs.

Yes, we provide customisation as per your requirements. To learn more, feel free to contact us on sales@6wresearch.com

| 1 Executive Summary |

| 2 Introduction |

| 2.1 Key Highlights of the Report |

| 2.2 Report Description |

| 2.3 Market Scope & Segmentation |

| 2.4 Research Methodology |

| 2.5 Assumptions |

| 3 China Beer Market Overview |

| 3.1 China Country Macro Economic Indicators |

| 3.2 China Beer Market Revenues & Volume, 2019 & 2029F |

| 3.3 China Beer Market - Industry Life Cycle |

| 3.4 China Beer Market - Porter's Five Forces |

| 3.5 China Beer Market Revenues & Volume Share, By Type, 2019 & 2029F |

| 3.6 China Beer Market Revenues & Volume Share, By Category, 2019 & 2029F |

| 3.7 China Beer Market Revenues & Volume Share, By Packaging, 2019 & 2029F |

| 3.8 China Beer Market Revenues & Volume Share, By Production, 2019 & 2029F |

| 4 China Beer Market Dynamics |

| 4.1 Impact Analysis |

| 4.2 Market Drivers |

| 4.2.1 Increasing disposable income of Chinese consumers leading to higher spending on beer. |

| 4.2.2 Growing popularity of craft and premium beers among Chinese consumers. |

| 4.2.3 Rising urbanization and changing lifestyles driving demand for beer consumption. |

| 4.3 Market Restraints |

| 4.3.1 Stringent government regulations and policies related to alcohol consumption in China. |

| 4.3.2 Competition from other alcoholic beverages like wine and spirits affecting beer sales. |

| 4.3.3 Health concerns and increased awareness about the negative effects of excessive alcohol consumption. |

| 5 China Beer Market Trends |

| 6 China Beer Market, By Types |

| 6.1 China Beer Market, By Type |

| 6.1.1 Overview and Analysis |

| 6.1.2 China Beer Market Revenues & Volume, By Type, 2019 - 2029F |

| 6.1.3 China Beer Market Revenues & Volume, By Lager, 2019 - 2029F |

| 6.1.4 China Beer Market Revenues & Volume, By Ale, 2019 - 2029F |

| 6.1.5 China Beer Market Revenues & Volume, By Stout & Porter, 2019 - 2029F |

| 6.1.6 China Beer Market Revenues & Volume, By Malt, 2019 - 2029F |

| 6.1.7 China Beer Market Revenues & Volume, By Others, 2019 - 2029F |

| 6.2 China Beer Market, By Category |

| 6.2.1 Overview and Analysis |

| 6.2.2 China Beer Market Revenues & Volume, By Popular Price, 2019 - 2029F |

| 6.2.3 China Beer Market Revenues & Volume, By Premium, 2019 - 2029F |

| 6.2.4 China Beer Market Revenues & Volume, By Super Premium, 2019 - 2029F |

| 6.3 China Beer Market, By Packaging |

| 6.3.1 Overview and Analysis |

| 6.3.2 China Beer Market Revenues & Volume, By Glass, 2019 - 2029F |

| 6.3.3 China Beer Market Revenues & Volume, By PET Bottle, 2019 - 2029F |

| 6.3.4 China Beer Market Revenues & Volume, By Metal Can, 2019 - 2029F |

| 6.3.5 China Beer Market Revenues & Volume, By Others, 2019 - 2029F |

| 6.4 China Beer Market, By Production |

| 6.4.1 Overview and Analysis |

| 6.4.2 China Beer Market Revenues & Volume, By Macro-brewery, 2019 - 2029F |

| 6.4.3 China Beer Market Revenues & Volume, By Micro-brewery, 2019 - 2029F |

| 6.4.4 China Beer Market Revenues & Volume, By Craft Brewery, 2019 - 2029F |

| 6.4.5 China Beer Market Revenues & Volume, By Others, 2019 - 2029F |

| 7 China Beer Market Import-Export Trade Statistics |

| 7.1 China Beer Market Export to Major Countries |

| 7.2 China Beer Market Imports from Major Countries |

| 8 China Beer Market Key Performance Indicators |

| 8.1 Consumer demand for craft and premium beer brands. |

| 8.2 Number of breweries and beer brands entering the Chinese market. |

| 8.3 Growth in beer consumption during festivals and events in China. |

| 8.4 Investments in marketing and brand promotions by beer companies. |

| 8.5 Adoption of innovative packaging and brewing techniques in the Chinese beer market. |

| 9 China Beer Market - Opportunity Assessment |

| 9.1 China Beer Market Opportunity Assessment, By Type, 2019 & 2029F |

| 9.2 China Beer Market Opportunity Assessment, By Category, 2019 & 2029F |

| 9.3 China Beer Market Opportunity Assessment, By Packaging, 2019 & 2029F |

| 9.4 China Beer Market Opportunity Assessment, By Production, 2019 & 2029F |

| 10 China Beer Market - Competitive Landscape |

| 10.1 China Beer Market Revenue Share, By Companies, 2024 |

| 10.2 China Beer Market Competitive Benchmarking, By Operating and Technical Parameters |

| 11 Company Profiles |

| 12 Recommendations |

| 13 Disclaimer |

Export potential assessment - trade Analytics for 2030

Export potential enables firms to identify high-growth global markets with greater confidence by combining advanced trade intelligence with a structured quantitative methodology. The framework analyzes emerging demand trends and country-level import patterns while integrating macroeconomic and trade datasets such as GDP and population forecasts, bilateral import–export flows, tariff structures, elasticity differentials between developed and developing economies, geographic distance, and import demand projections. Using weighted trade values from 2020–2024 as the base period to project country-to-country export potential for 2030, these inputs are operationalized through calculated drivers such as gravity model parameters, tariff impact factors, and projected GDP per-capita growth. Through an analysis of hidden potentials, demand hotspots, and market conditions that are most favorable to success, this method enables firms to focus on target countries, maximize returns, and global expansion with data, backed by accuracy.

By factoring in the projected importer demand gap that is currently unmet and could be potential opportunity, it identifies the potential for the Exporter (Country) among 190 countries, against the general trade analysis, which identifies the biggest importer or exporter.

To discover high-growth global markets and optimize your business strategy:

Click Here

Pricing

- Single User License$ 1,995

- Department License$ 2,400

- Site License$ 3,120

- Global License$ 3,795

Search

Thought Leadership and Analyst Meet

Our Clients

Latest Reports

- Philippines Polyhydroxybutyrate-co-Hydroxyvalerate Market (2026-2032) | Trends, Insights, Challenges, Restraints, Competition, Size, Value, Forecast, Pricing, Share, Outlook, Revenue, Investment Opportunities, Strategy, Drivers, Demand, Growth, segmentation, Analysis, Companies

- Peru Polyhydroxybutyrate-co-Hydroxyvalerate Market (2026-2032) | Growth, Demand, Challenges, Share, Trends, Analysis, Pricing, Investment Opportunities, Drivers, Value, Forecast, Competition, Size, Companies, Insights, Outlook, Restraints, segmentation, Revenue, Strategy

- Pakistan Polyhydroxybutyrate-co-Hydroxyvalerate Market (2026-2032) | Restraints, segmentation, Pricing, Forecast, Share, Strategy, Competition, Trends, Insights, Drivers, Challenges, Growth, Revenue, Outlook, Value, Investment Opportunities, Companies, Size, Analysis, Demand

- Oman Polyhydroxybutyrate-co-Hydroxyvalerate Market (2026-2032) | Drivers, segmentation, Insights, Competition, Pricing, Outlook, Size, Revenue, Challenges, Forecast, Analysis, Growth, Value, Share, Trends, Investment Opportunities, Strategy, Restraints, Companies, Demand

- Nigeria Polyhydroxybutyrate-co-Hydroxyvalerate Market (2026-2032) | Value, Investment Opportunities, Analysis, Revenue, Restraints, Pricing, Outlook, Competition, Demand, Growth, Forecast, Companies, Trends, Challenges, segmentation, Drivers, Insights, Share, Size, Strategy

- Nepal Polyhydroxybutyrate-co-Hydroxyvalerate Market (2026-2032) | Insights, Analysis, Drivers, Share, Revenue, Demand, segmentation, Investment Opportunities, Competition, Forecast, Growth, Pricing, Companies, Strategy, Trends, Restraints, Challenges, Outlook, Size, Value

- Myanmar Polyhydroxybutyrate-co-Hydroxyvalerate Market (2026-2032) | Outlook, Revenue, Strategy, Restraints, Drivers, segmentation, Share, Forecast, Competition, Insights, Growth, Pricing, Size, Demand, Value, Companies, Trends, Challenges, Investment Opportunities, Analysis

- Morocco Polyhydroxybutyrate-co-Hydroxyvalerate Market (2026-2032) | Outlook, Investment Opportunities, Restraints, Strategy, Forecast, Challenges, Drivers, Growth, Companies, segmentation, Trends, Size, Competition, Revenue, Demand, Insights, Share, Analysis, Value, Pricing

- Mexico Polyhydroxybutyrate-co-Hydroxyvalerate Market (2026-2032) | Size, Drivers, Outlook, Share, Strategy, Growth, Pricing, Challenges, Companies, Demand, Value, Investment Opportunities, Restraints, Trends, Forecast, segmentation, Analysis, Insights, Competition, Revenue

- Malaysia Polyhydroxybutyrate-co-Hydroxyvalerate Market (2026-2032) | Share, segmentation, Size, Companies, Analysis, Insights, Forecast, Value, Revenue, Drivers, Restraints, Challenges, Investment Opportunities, Trends, Competition, Strategy, Demand, Growth, Outlook, Pricing

Industry Events and Analyst Meet

HIMTEX 2026

India Refining Summit 2026

India EV Show 2026

EV tech India Expo 2026

Auto Tech Asia 2026

Whitepaper

- Middle East & Africa Commercial Security Market Click here to view more.

- Middle East & Africa Fire Safety Systems & Equipment Market Click here to view more.

- GCC Drone Market Click here to view more.

- Middle East Lighting Fixture Market Click here to view more.

- GCC Physical & Perimeter Security Market Click here to view more.

6WResearch In News

- Doha a strategic location for EV manufacturing hub: IPA Qatar

- Demand for luxury TVs surging in the GCC, says Samsung

- Empowering Growth: The Thriving Journey of Bangladesh’s Cable Industry

- Demand for luxury TVs surging in the GCC, says Samsung

- Video call with a traditional healer? Once unthinkable, it’s now common in South Africa

- Intelligent Buildings To Smooth GCC’s Path To Net Zero