China Clay Market (2025-2029) | Trends, Revenue, Companies, Share, Forecast, Size, Value, Growth, Analysis, Outlook & Industry

Market Forecast By Application (Tableware, Sanitary ware, Medical applications), By End Use (Ceramic and, Non-ceramic) And Competitive Landscape

| Product Code: ETC318981 | Publication Date: Aug 2022 | Updated Date: Oct 2025 | Product Type: Market Research Report | |

| Publisher: 6Wresearch | Author: Shubham Padhi | No. of Pages: 75 | No. of Figures: 35 | No. of Tables: 20 |

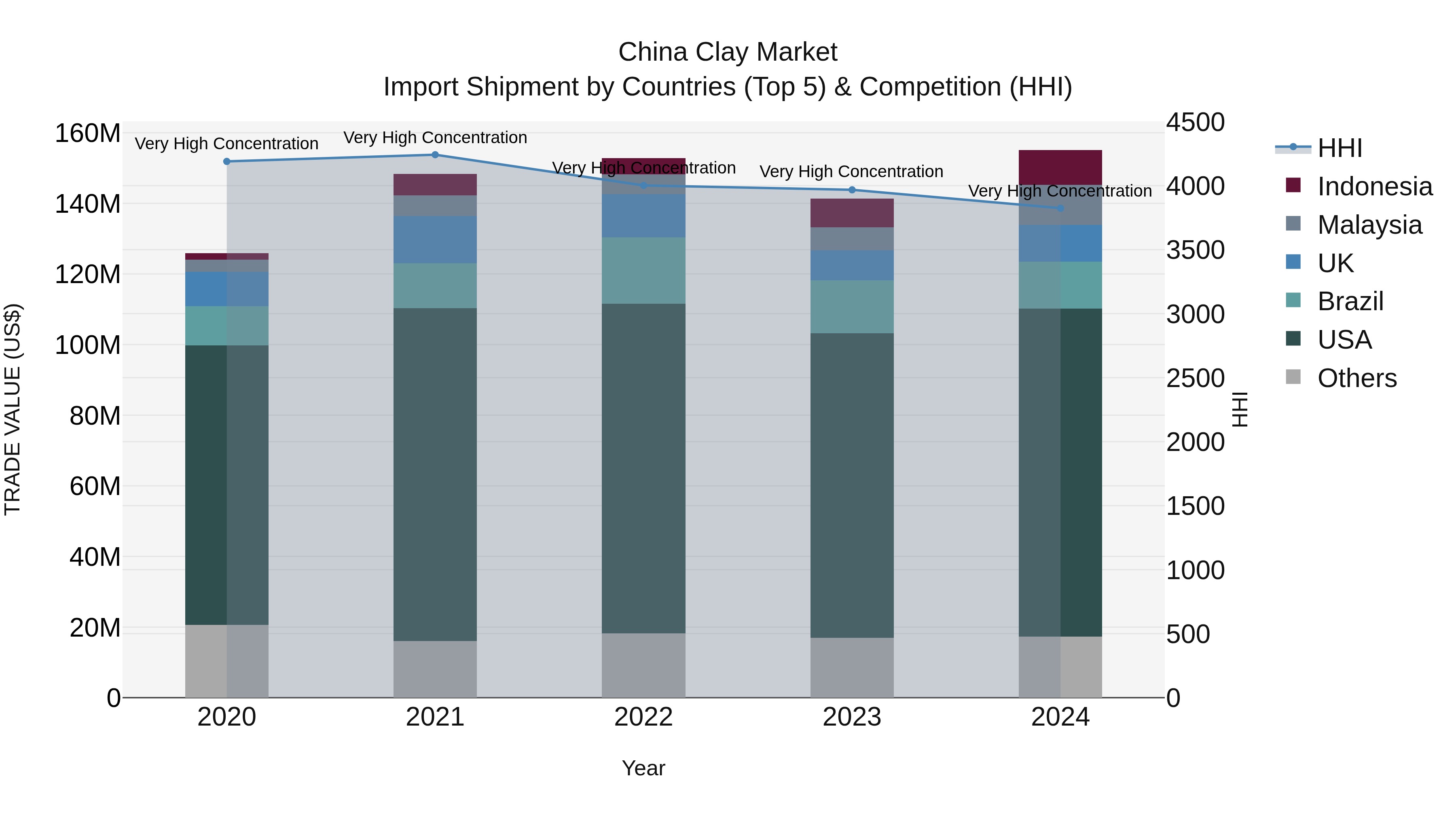

China Clay Market Top 5 Importing Countries and Market Competition (HHI) Analysis

China import shipments of china clay in 2024 continued to showcase strong growth, with top exporting countries including the USA, Brazil, Malaysia, UK, and Indonesia. The market remained highly concentrated with a high Herfindahl-Hirschman Index (HHI) in 2024. The compound annual growth rate (CAGR) from 2020 to 2024 stood at a healthy 5.34%, indicating sustained expansion. Furthermore, the growth rate from 2023 to 2024 surged to an impressive 9.7%, reflecting a robust upward trajectory in China china clay import market.

China Clay Market Highlights

| Report Name | China Clay Market |

| Forecast period | 2025-2029 |

| CAGR | 6.24% |

| Growing Sector | Ceramics & Porcelain |

Topics Covered in the China Clay Market Report

The China Clay Market report thoroughly covers the market by application, and end use. The market report provides an unbiased and detailed analysis of the ongoing market trends, opportunities/high growth areas, and market drivers which would help stakeholders to devise and align their market strategies according to the current and future market dynamics.

China Clay Market Synopsis

The China Clay Market is steadily gaining momentum with increasing demand from ceramic sectors and broader applications in construction and industrial manufacturing. Expansion in the global ceramic tiles industry leads to large kaolin requirements for surface finishing and aesthetics. Moreover, rising demand for premium sanitary ware and growth in the medical porcelain sector continue to fuel strong expansion of the China Clay Market, establishing it as an essential material across various industries.

China Clay Market is projected to grow steadily, growing at a compound annual growth rate (CAGR) of 6.24% during the forecast period 2025-2029. Market growth is driven by rising construction activities, increasing ceramic exports, and strong adoption in paints and coatings. The paper industry’s change toward kaolin as a filler and coating agent also raises demand. Expanded mining activities and advances in clay processing technology are increasing production capacity. Strategic investments by multinational ceramic companies across Asia-Pacific and Europe further enhance the market outlook. These factors collectively support the steady global expansion of the China clay market.

China Clay Market Challenges

Although demand remains steady, the China Clay Industry struggles with strict environmental mining regulations, fluctuating clay prices worldwide, and restricted availability of high-purity kaolin. Competition from synthetic alternatives and growing interest in bio-based fillers also reduce market share. Logistics challenges in distant mining sites and water-intensive production processes further hinder operational efficiency. Import-export restrictions and geopolitical tensions across supplier nations may disrupt long-term raw material availability.

China Clay Market Trends

The market is experiencing trends such as increasing use of ultrafine kaolin in cosmetics and pharmaceuticals, growing application in rubber reinforcement, and higher demand in high-end paper coating. Automated processing systems and AI-driven quality grading are improving supply chain management. There is rising interest in calcined kaolin as a replacement for titanium dioxide in industrial coatings. Export-driven production hubs in Asia-Pacific are focusing on expanding into Europe and Middle Eastern construction sectors.

Investment Opportunities in the China Clay Market

The China Clay Market Growth offers compelling investment prospects in establishing environmentally sustainable clay processing facilities, advancing clay purification technology, and constructing export-oriented infrastructure. Investment in research and development for specialty kaolin grades utilized in medical and high-temperature ceramic applications is increasing. Resource-rich regions, including India and Brazil, are soliciting foreign investments to enhance mining and processing capacities. Government-supported industrial mineral zones and measures to facilitate company operations further promote future growth.

Leading Players of the China Clay Market

The China Clay Market Share is dominated by companies leveraging integrated supply chains, automated processing plants, and regional expansion strategies. Leading companies include Imerys S.A., Ashapura Group, EICL Ltd., KaMin LLC, and BASF SE. These firms are focusing on high-performance clay variants and energy-efficient production processes. Emerging players in Asia-Pacific and Africa are disrupting traditional market structures through low-cost mining operations and fast regional delivery logistics.

Government Regulations Introduced in the China Clay Market

According to Chinese government data, several governments are introducing strict regulations regarding sustainable clay mining and industrial mineral usage. For example, India’s Ministry of Mines initiated the Sustainable Development Framework for Non-Coal Minerals, improving kaolin mining governance. Brazil’s ANM (Agência Nacional de Mineração) implemented real-time tracking of clay mining output to ensure transparency. In the EU, REACH regulations make sure that clay used in manufacturing is chemically compliant, mainly for applications involving consumer exposure.

Future Insights of the China Clay Market

The China Clay Market is estimated to see robust long-term growth as industries increasingly require fine-grade kaolin for technological applications. AI-integrated sorting systems and robotic handling are revolutionizing clay mining and refining. The expansion of solar panel manufacturing may introduce new avenues for kaolin usage in specialty glass coatings. Circular economy practices and clay recycling innovations are emerging. As the paper and ceramics industries digitalize, real-time demand tracking and B2B e-commerce platforms will enhance distribution.

Market Segmentation Analysis

The report offers a comprehensive study of the subsequent market segments and their leading categories.

Tableware to Dominate the Market – By Application

According to Guneet Kaur, Senior Research Analyst, 6Wresearch, Tableware is anticipated to dominate the market by application due to the rising demand for aesthetically pleasing, durable, and heat-resistant ceramic products. China clay’s whiteness and plasticity make it the preferred raw material in fine china and porcelain dishes. With global restaurant chains expanding and household dining preferences evolving, manufacturers are turning to kaolin-based materials for glossy finishes and microwave-safe utility. Increasing urban middle-class populations across Asia and Europe are further propelling tableware demand.

Ceramic to Dominate the Market – By End Use

Ceramic end-use is the leading segment in the China Clay Market as it serves diverse industries including tiles, sanitary ware, and medical-grade ceramics. The unique thermal and structural properties of china clay make it indispensable in high-temperature applications. Technological advancements have enabled enhanced sintering processes using kaolin, thus reducing energy consumption. With smart housing, real estate booms, and hospital infrastructure growth, ceramic applications of china clay continue to expand across developed and emerging markets.

Key Attractiveness of the Report

- 10 Years of Market Numbers.

- Historical Data Starting from 2021 to 2024.

- Base Year: 2024.

- Forecast Data until 2029

- Key Performance Indicators Impacting the Market.

- Major Upcoming Developments and Projects.

Key Highlights of the Report:

- China Clay Market Outlook

- Market Size of China Clay Market, 2024

- Forecast of China Clay Market, 2029

- Historical Data and Forecast of China Clay Revenues & Volume for the Period 2019-2029

- China Clay Market Trend Evolution

- China Clay Market Drivers and Challenges

- China Clay Price Trends

- China Clay Porter's Five Forces

- China Clay Industry Life Cycle

- Historical Data and Forecast of China Clay Market Revenues & Volume By Application for the Period 2019-2029

- Historical Data and Forecast of China Clay Market Revenues & Volume By Tableware for the Period 2019-2029

- Historical Data and Forecast of China Clay Market Revenues & Volume By Sanitary ware for the Period 2019-2029

- Historical Data and Forecast of China Clay Market Revenues & Volume By Medical applications for the Period 2019-2029

- Historical Data and Forecast of China Clay Market Revenues & Volume By End Use for the Period 2019-2029

- Historical Data and Forecast of China Clay Market Revenues & Volume By Ceramic and for the Period 2019-2029

- Historical Data and Forecast of China Clay Market Revenues & Volume By Non-ceramic for the Period 2019-2029

- China Clay Import Export Trade Statistics

- Market Opportunity Assessment By Application

- Market Opportunity Assessment By End Use

- China Clay Top Companies Market Share

- China Clay Competitive Benchmarking By Technical and Operational Parameters

- China Clay Company Profiles

- China Clay Key Strategic Recommendations

Market Covered

The market report provides a detailed analysis of the following market segments:

By Application

- Tableware

- Sanitary Ware

- Medical Applications

- Others

By End Use

- Ceramic

- Non-Ceramic

China Clay Market (2025-2029) : FAQ's

China Clay Market is projected to grow at a CAGR of approximately 6.24% during the forecast period.

Growth is influenced by expanding ceramic and construction industries, increasing export of kaolin-based products, and rising demand for high-quality sanitary ware and medical ceramics.

Major applications include fine porcelain tableware, durable sanitary ware, heat-resistant ceramics, industrial coatings, and paper filling materials.

China Clay Market trends include rising demand in ceramics, paints, eco-friendly mining, tech advances, and growth in pharma and cosmetics applications.

6Wresearch actively monitors the China Clay Market and publishes its comprehensive annual report, highlighting emerging trends, growth drivers, revenue analysis, and forecast outlook. Our insights help businesses to make data-backed strategic decisions with ongoing market dynamics. Our analysts track relevent industries related to the China Clay Market, allowing our clients with actionable intelligence and reliable forecasts tailored to emerging regional needs.

Yes, we provide customisation as per your requirements. To learn more, feel free to contact us on sales@6wresearch.com

| 1 Executive Summary |

| 2 Introduction |

| 2.1 Key Highlights of the Report |

| 2.2 Report Description |

| 2.3 Market Scope & Segmentation |

| 2.4 Research Methodology |

| 2.5 Assumptions |

| 3 China Clay Market Overview |

| 3.1 China Country Macro Economic Indicators |

| 3.2 China Clay Market Revenues & Volume, 2019 & 2029F |

| 3.3 China Clay Market - Industry Life Cycle |

| 3.4 China Clay Market - Porter's Five Forces |

| 3.5 China Clay Market Revenues & Volume Share, By Application, 2019 & 2029F |

| 3.6 China Clay Market Revenues & Volume Share, By End Use, 2019 & 2029F |

| 4 China Clay Market Dynamics |

| 4.1 Impact Analysis |

| 4.2 Market Drivers |

| 4.2.1 Increasing demand for china clay in various end-use industries such as ceramics, paper, paints, and polymers |

| 4.2.2 Growing construction activities and infrastructure development projects driving the demand for china clay in the manufacturing of tiles, sanitary ware, and other construction materials |

| 4.3 Market Restraints |

| 4.3.1 Fluctuating raw material prices affecting the overall production cost and profitability of china clay manufacturers |

| 4.3.2 Environmental regulations and concerns regarding the mining and processing of china clay leading to operational challenges and compliance costs |

| 5 China Clay Market Trends |

| 6 China Clay Market, By Types |

| 6.1 China Clay Market, By Application |

| 6.1.1 Overview and Analysis |

| 6.1.2 China Clay Market Revenues & Volume, By Application, 2019-2029F |

| 6.1.3 China Clay Market Revenues & Volume, By Tableware, 2019-2029F |

| 6.1.4 China Clay Market Revenues & Volume, By Sanitary ware, 2019-2029F |

| 6.1.5 China Clay Market Revenues & Volume, By Medical applications, 2019-2029F |

| 6.2 China Clay Market, By End Use |

| 6.2.1 Overview and Analysis |

| 6.2.2 China Clay Market Revenues & Volume, By Ceramic and, 2019-2029F |

| 6.2.3 China Clay Market Revenues & Volume, By Non-ceramic, 2019-2029F |

| 7 China Clay Market Import-Export Trade Statistics |

| 7.1 China Clay Market Export to Major Countries |

| 7.2 China Clay Market Imports from Major Countries |

| 8 China Clay Market Key Performance Indicators |

| 8.1 Average selling price of china clay in key markets |

| 8.2 Production capacity utilization rate of china clay manufacturers |

| 8.3 Research and development investment in new applications and technologies for china clay |

| 8.4 Environmental sustainability initiatives and certifications in the china clay industry |

| 9 China Clay Market - Opportunity Assessment |

| 9.1 China Clay Market Opportunity Assessment, By Application, 2019 & 2029F |

| 9.2 China Clay Market Opportunity Assessment, By End Use, 2019 & 2029F |

| 10 China Clay Market - Competitive Landscape |

| 10.1 China Clay Market Revenue Share, By Companies, 2024 |

| 10.2 China Clay Market Competitive Benchmarking, By Operating and Technical Parameters |

| 11 Company Profiles |

| 12 Recommendations |

| 13 Disclaimer |

Global Go To Market Strategy - 2030

Export potential enables firms to identify high-growth global markets with greater confidence by combining advanced trade intelligence with a structured quantitative methodology. The framework analyzes emerging demand trends and country-level import patterns while integrating macroeconomic and trade datasets such as GDP and population forecasts, bilateral import–export flows, tariff structures, elasticity differentials between developed and developing economies, geographic distance, and import demand projections. Using weighted trade values from 2020–2024 as the base period to project country-to-country export potential for 2030, these inputs are operationalized through calculated drivers such as gravity model parameters, tariff impact factors, and projected GDP per-capita growth. Through an analysis of hidden potentials, demand hotspots, and market conditions that are most favorable to success, this method enables firms to focus on target countries, maximize returns, and global expansion with data, backed by accuracy.

By factoring in the projected importer demand gap that is currently unmet and could be potential opportunity, it identifies the potential for the Exporter (Country) among 190 countries, against the general trade analysis, which identifies the biggest importer or exporter.

To discover high-growth global markets and optimize your business strategy:

Click Here

Pricing

- Single User License$ 1,995

- Department License$ 2,400

- Site License$ 3,120

- Global License$ 3,795

Leadership Perspectives from Industry Events

Search

Thought Leadership and Analyst Meet

Our Clients

6WResearch In News

- India Air Conditioner Market Set for Strong Rebound in 2026 After Weather-Led Correction and GST-Driven Recovery: 6Wresearch

- ADAS in India: How Automatic Emergency Braking, Blind Spot Detection & Driver Monitoring are Transforming Road Safety

- Doha a strategic location for EV manufacturing hub: IPA Qatar

- Demand for luxury TVs surging in the GCC, says Samsung

- Empowering Growth: The Thriving Journey of Bangladesh’s Cable Industry

- Demand for luxury TVs surging in the GCC, says Samsung

Latest Reports

- Nicaragua RPG Gaming Market (2026-2032)

- New Zealand RPG Gaming Market (2026-2032)

- Netherlands RPG Gaming Market (2026-2032)

- Nauru RPG Gaming Market (2026-2032)

- Namibia RPG Gaming Market (2026-2032)

- Mozambique RPG Gaming Market (2026-2032)

- Montenegro RPG Gaming Market (2026-2032)

- Mongolia RPG Gaming Market (2026-2032)

- Monaco RPG Gaming Market (2026-2032)

- Micronesia RPG Gaming Market (2026-2032)

Industry Events and Analyst Meet

EV India Expo 2026

HIMTEX 2026

India Refining Summit 2026

India EV Show 2026

EV tech India Expo 2026

Whitepaper

- Middle East & Africa Commercial Security Market Click here to view more.

- Middle East & Africa Fire Safety Systems & Equipment Market Click here to view more.

- GCC Drone Market Click here to view more.

- Middle East Lighting Fixture Market Click here to view more.

- GCC Physical & Perimeter Security Market Click here to view more.