China Lithium Ion Battery Market (2025 - 2029) | Outlook , Share, Size, Growth, Value, Analysis, Trends, Revenue, Companies, Industry & Forecast

Market Forecast By Type (Lithium Nickel Magnesium Cobalt (LI-NMC), Lithium Ferro Phosphate (LFP), Lithium Cobalt Oxide (LCO), Lithium Titanate Oxide (LTO), Lithium Manganese Oxide (LMO), Lithium Nickel Cobalt Aluminum Oxide (NCA)), By Power Capacity (0-300 mAH, 3,000-10,000 mAH, 10,000-60,000 mAH, More than 60,000 mAH), By Application (Consumer Electronics OEMs, Automotive OEMs, Energy Storage, Industrial OEMs, Other OEMs, Aftermarket), By Form (Pouch, Cylindrical, Elliptical, Prismatic, Custom Design) And Competitive Landscape

| Product Code: ETC266421 | Publication Date: Aug 2022 | Updated Date: Oct 2025 | Product Type: Market Research Report | |

| Publisher: 6Wresearch | Author: Sachin Kumar Rai | No. of Pages: 75 | No. of Figures: 35 | No. of Tables: 20 |

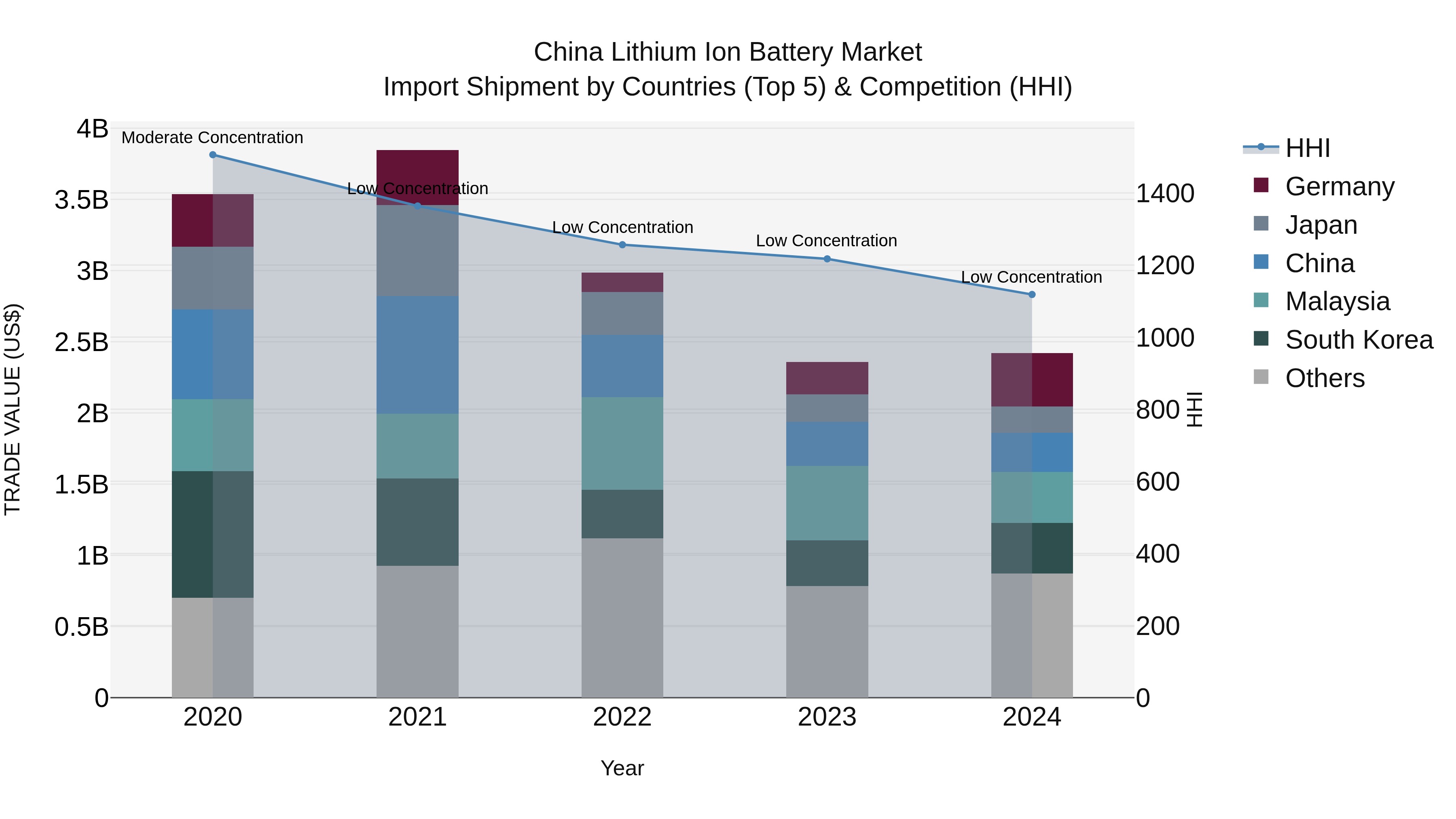

China Lithium Ion Battery Market Top 5 Importing Countries and Market Competition (HHI) Analysis

China lithium ion battery import shipments in 2024 were primarily sourced from top exporting countries such as Germany, Malaysia, South Korea, China, and Poland. Despite the negative CAGR of -9.05% from 2020 to 2024, there was a slight improvement in growth rate in 2024 at 2.67%. The Herfindahl-Hirschman Index (HHI) indicated low concentration in the market, reflecting a diverse import landscape for lithium ion batteries in China. This data suggests a mix of both challenges and opportunities for stakeholders in the global lithium ion battery market.

China Lithium-Ion Battery Market Highlights

| Report Name | China Lithium-Ion Battery Market |

| Forecast Period | 2025-2029 |

| CAGR | 1.18% |

| Growing Sector | Energy Storage and Power |

Topics Covered in the China Lithium-Ion Battery Market Report

The China Lithium-Ion Battery Market report thoroughly covers the market by type, power capacity, applications, and forms. The market report provides an unbiased and detailed analysis of ongoing market trends, opportunities/high growth areas, and market drivers, which would help stakeholders to devise and align their market strategies according to the current and future market dynamics.

China Lithium-Ion Battery Market Synopsis

China Lithium-Ion Battery Market is expected to achieve major growth owing to the rising adoption of New Energy Vehicles (NEVs), expansion of stationary energy storage systems, and sustained demand from consumer and industrial electronics. China leverages a complete supply chain, from cathodes and anodes to separators and electrolytes, to maintain competitive costs and stable access to key materials. Cutting-edge developments like cell-to-pack design and prismatic blade cells are lifting energy density, while scale economies in manufacturing are making lithium-ion batteries more affordable for electric vehicles, grid storage, and electronics.

Evaluation of Growth Drivers in the China Lithium-Ion Battery Market

Below mentioned are some prominent drivers and their influence to the market dynamics:

| Driver | Primary Segments Affected | Why it matters (evidence) |

| NEV Expansion | LFP, NMC; Automotive OEMs | Surging electric vehicle production in China requires durable and high-capacity traction batteries with strong safety profiles. |

| Energy Storage Growth | LFP; Energy Storage | Renewable integration and grid balancing are driving multi-MWh deployments, fueling demand for LFP chemistries. |

| Localized Manufacturing | All Types; All Forms | Integrated supply chains and large-scale capacity cut costs, secure supply, and boost international competitiveness. |

| Consumer Electronics Penetration | LCO, NMC; Consumer OEMs | Smartphones, laptops, and wearables demand compact, high-energy-density batteries. |

| Recycling & Policy Support | All Types; Aftermarket | Government recycling mandates and circular economy initiatives reduce raw material risk and environmental footprint. |

The China Lithium-Ion Battery Market size is projected to grow at the CAGR of 1.18% during the forecast period of 2025-2029. The China Lithium-Ion Battery Industry is being strongly driven by the rapid growth of New Energy Vehicles (NEVs). Expanding EV production, supported by government subsidies, tax incentives, and credit policies, is generating enormous demand for high-capacity and long-life batteries. Lithium Ferro Phosphate (LFP) and Nickel Manganese Cobalt (NMC) chemistry are favored for their safety and performance in electric mobility. This surge in adoption across passenger cars, buses, and commercial fleets makes automotive OEMs the single largest driver of market expansion.

Evaluation of Restraints in the China Lithium-Ion Battery Market

Below mentioned are some major restraints and their influence to the market dynamics:

| Restraint | Primary Segments Affected | What this means (evidence) |

| Raw Material Price Volatility | NMC, NCA; Automotive/Industrial OEMs | Fluctuations in lithium, nickel, and cobalt prices put pressure on margins and production costs. |

| Thermal Safety Concerns | All Types; Consumer & Automotive OEMs | High energy density requires sophisticated BMS and safety measures, raising costs. |

| Grid Integration Barriers | Energy Storage | Delays in grid connection and regulatory approvals slow ESS deployment timelines. |

| Technology Transition Risk | LCO, LMO legacy; Aftermarket | Legacy chemistries face substitution by LFP and NMC, affecting older devices and retrofit economics. |

| Trade Regulations | Prismatic, Custom Design | Export tariffs and compliance demands may limit overseas sales and supply chain efficiency. |

China Lithium-Ion Battery Market Challenges

Despite China Lithium-Ion Battery Market Growth potential, the market faces several challenges such as volatility in raw material supply chains, particularly lithium, nickel, and cobalt. Ensuring battery safety and managing thermal runaway risks are important as energy density increases. Export-oriented suppliers must comply with evolving international trade and certification standards, which may raise costs. Energy storage developers encounter project delays due to grid interconnection rules. Additionally, legacy chemistries like LCO and LMO face diminishing demand, pushing manufacturers to constantly adapt product portfolios.

China Lithium-Ion Battery Market Trends

Key developments influencing the growth of the market are:

- Cell-to-Pack (CTP) and Blade Configurations - Enhanced economics through improved energy density, cost savings, and thermal safety due to simpler pack architecture.

- LFP Scaling in EVs and ESS (Energy Storage Systems) - The safe, cost effective performance of lithium iron phosphate (LFP) batteries has facilitated adoption in leading EVs and stationary storage applications.

- High-Nickel Cathodes - While NMC and NCA continue to be depended upon for their superior energy density for premium EVs and industrial markets.

- AI Enabled BMS - Intelligent battery management systems for predictive maintenance, charge optimization, and increasing battery lifecycle.

- Recycling and Second Life Uses - The emergence of hydrometallurgical recycling and repurposing old EV packs for stationary storage systems.

Investment Opportunities in the China Lithium-Ion Battery Industry

There are some main areas of investment opportunity in the market which includes:

- Utility-Scale Storage Projects – A rising need for large-scale energy storage systems paired with renewable energy.

- LFP Cathode Manufacturing – An increase of capital investment in phosphate cathode manufacturing to fulfill increasing demands in EVs and ESSs.

- Battery Management and Thermal Systems - The creation of next level software and thermal management systems for even more safety and efficiency.

- Recycling & Circular Economy - The establishment of large-scale recycling facilities to recover lithium, nickel, and cobalt and provide supply security.

Top 5 Leading Players in the China Lithium-Ion Battery Market

Some leading players dominating the China Lithium-Ion Battery Market Share include:

1. Contemporary Amperex Technology Co., Limited (CATL)

| Company Name | Contemporary Amperex Technology Co., Limited (CATL) |

| Establishment Year | 2011 |

| Headquarter | Ningde, Fujian, China |

| Official Website | Click here |

CATL is a global leader in EV and energy storage batteries, providing LFP and high-nickel solutions with innovations in CTP architecture and fast charging.

2. BYD Company Limited

| Company Name | BYD Company Limited |

| Establishment Year | 1995 |

| Headquarter | Shenzhen, China |

| Official Website | Click here |

BYD produces LFP blade batteries with high safety and long cycle life, supplying its automotive and energy businesses.

3. CALB Co., Ltd. (China Aviation Lithium Battery)

| Company Name | CALB Co., Ltd. (China Aviation Lithium Battery) |

| Establishment Year | 2007 |

| Headquarter | Changzhou, Jiangsu, China |

| Official Website | Click here |

CALB manufactures prismatic LFP and NMC batteries with applications in passenger vehicles, commercial fleets, and energy storage.

4. EVE Energy Co., Ltd.

| Company Name | EVE Energy Co., Ltd. |

| Establishment Year | 2001 |

| Headquarter | Huizhou, Guangdong, China |

| Official Website | Click here |

EVE Energy develops cylindrical, prismatic, and pouch cells for EVs, IoT, and industrial devices, focusing on innovation and durability.

5. Gotion High-Tech Co., Ltd.

| Company Name | Gotion High-Tech Co., Ltd. |

| Establishment Year | 2006 |

| Headquarter | Hefei, Anhui, China |

| Official Website | Click here |

Gotion provides LFP and NMC solutions for EVs and energy storage, expanding into overseas markets with localized production bases.

Government Regulations Introduced in the China Lithium-Ion Battery Market

According to Chinese Government data, the Chinese government has launched multiple policies to support the battery industry. Purchase tax exemptions and credit quotas under NEV policies incentivize electric vehicle adoption. The National Energy Administration has rolled out pilot programs for grid-scale storage deployment. The Ministry of Industry and Information Technology (MIIT) implements standards for traceability as a condition for recycling batteries and outlines closed-loop systems for material recovery. However, programs developed through Made in China 2025 seek to upgrade battery production facilities and support global competitiveness.

Future Insights of the China Lithium-Ion Battery Market

It is anticipated that the China Lithium-Ion Battery Market will grow rapidly in the coming years. Several factors driving growth for the market include the increased adoption of electric vehicles, greater use of renewable resources, and growth in demand for large scale stationary storage. Drivers of sustainability through technology are increasing with prismatic and pouch battery designs, AI-enabled battery management systems, and enhanced recycling efforts. Furthermore, export opportunities are likely to rise along with global demand for electric vehicles and energy storage, which allows Chinese manufacturers to take advantage of their economies of scale, cost competitiveness, and variety of products.

Market Segmentation Analysis

The report offers a comprehensive study of the subsequent market segments and their leading categories.

Lithium Ferro Phosphate (LFP) to Dominate the Market – By Type

According to Ritika Kalra, Senior Research Analyst at 6Wresearch, the Lithium Ferro Phosphate (LFP) category holds the largest market share in the China Lithium-Ion Battery Market. Its safety, cost-effectiveness, and long cycle life make it the preferred choice for mainstream EVs and grid storage, particularly as automakers and utilities prioritize durability and affordability over maximum energy density.

More than 60,000 mAH to Dominate the Market – By Power Capacity

The More than 60,000 mAH category dominates the market due to growing deployment in electric vehicles, buses, and large stationary storage projects. These high-capacity batteries are critical for providing the extended range and multi-MWh storage solutions needed in both automotive and utility-scale applications.

Automotive OEMs to Dominate the Market – By Application

The Automotive OEMs segment leads the China Lithium-Ion Battery Market. The rapid expansion of China’s NEV industry, supported by subsidies, credits, and growing consumer adoption, has positioned EV batteries as the largest demand source, with applications in passenger cars, commercial vehicles, and public transport fleets.

Prismatic to Dominate the Market – By Form

Among forms, the Prismatic segment dominates the China Lithium-Ion Battery Market. Prismatic cells are widely used in EVs and energy storage systems due to their higher packing efficiency, better thermal management, and compatibility with advanced pack designs such as cell-to-pack and blade architectures.

Key Attractiveness of the Report

- 10 Years of Market Numbers.

- Historical Data Starting from 2021 to 2024.

- Base Year: 2024.

- Forecast Data until 2029.

- Key Performance Indicators Impacting the Market.

- Major Upcoming Developments and Projects.

Key Highlights of the Report:

- China Lithium Ion Battery Market Outlook

- Market Size of China Lithium Ion Battery Market, 2024

- Forecast of China Lithium Ion Battery Market, 2029

- Historical Data and Forecast of China Lithium Ion Battery Revenues & Volume for the Period 2019 - 2029

- China Lithium Ion Battery Market Trend Evolution

- China Lithium Ion Battery Market Drivers and Challenges

- China Lithium Ion Battery Price Trends

- China Lithium Ion Battery Porter's Five Forces

- China Lithium Ion Battery Industry Life Cycle

- Historical Data and Forecast of China Lithium Ion Battery Market Revenues & Volume By Type for the Period 2019 - 2029

- Historical Data and Forecast of China Lithium Ion Battery Market Revenues & Volume By Lithium Nickel Magnesium Cobalt (LI-NMC) for the Period 2019 - 2029

- Historical Data and Forecast of China Lithium Ion Battery Market Revenues & Volume By Lithium Ferro Phosphate (LFP) for the Period 2019 - 2029

- Historical Data and Forecast of China Lithium Ion Battery Market Revenues & Volume By Lithium Cobalt Oxide (LCO) for the Period 2019 - 2029

- Historical Data and Forecast of China Lithium Ion Battery Market Revenues & Volume By Lithium Titanate Oxide (LTO) for the Period 2019 - 2029

- Historical Data and Forecast of China Lithium Ion Battery Market Revenues & Volume By Lithium Manganese Oxide (LMO) for the Period 2019 - 2029

- Historical Data and Forecast of China Lithium Ion Battery Market Revenues & Volume By Lithium Nickel Cobalt Aluminum Oxide (NCA) for the Period 2019 - 2029

- Historical Data and Forecast of China Lithium Ion Battery Market Revenues & Volume By Power Capacity for the Period 2019 - 2029

- Historical Data and Forecast of China Lithium Ion Battery Market Revenues & Volume By 0-300 mAH for the Period 2019 - 2029

- Historical Data and Forecast of China Lithium Ion Battery Market Revenues & Volume By 3,000-10,000 mAH for the Period 2019 - 2029

- Historical Data and Forecast of China Lithium Ion Battery Market Revenues & Volume By 10,000-60,000 mAH for the Period 2019 - 2029

- Historical Data and Forecast of China Lithium Ion Battery Market Revenues & Volume By More than 60,000 mAH for the Period 2019 - 2029

- Historical Data and Forecast of China Lithium Ion Battery Market Revenues & Volume By Application for the Period 2019 - 2029

- Historical Data and Forecast of China Lithium Ion Battery Market Revenues & Volume By Consumer Electronics OEMs for the Period 2019 - 2029

- Historical Data and Forecast of China Lithium Ion Battery Market Revenues & Volume By Automotive OEMs for the Period 2019 - 2029

- Historical Data and Forecast of China Lithium Ion Battery Market Revenues & Volume By Energy Storage for the Period 2019 - 2029

- Historical Data and Forecast of China Lithium Ion Battery Market Revenues & Volume By Industrial OEMs for the Period 2019 - 2029

- Historical Data and Forecast of China Lithium Ion Battery Market Revenues & Volume By Other OEMs for the Period 2019 - 2029

- Historical Data and Forecast of China Lithium Ion Battery Market Revenues & Volume By Aftermarket for the Period 2019 - 2029

- Historical Data and Forecast of China Lithium Ion Battery Market Revenues & Volume By Form for the Period 2019 - 2029

- Historical Data and Forecast of China Lithium Ion Battery Market Revenues & Volume By Pouch for the Period 2019 - 2029

- Historical Data and Forecast of China Lithium Ion Battery Market Revenues & Volume By Cylindrical for the Period 2019 - 2029

- Historical Data and Forecast of China Lithium Ion Battery Market Revenues & Volume By Elliptical for the Period 2019 - 2029

- Historical Data and Forecast of China Lithium Ion Battery Market Revenues & Volume By Prismatic for the Period 2019 - 2029

- Historical Data and Forecast of China Lithium Ion Battery Market Revenues & Volume By Custom Design for the Period 2019 - 2029

- China Lithium Ion Battery Import Export Trade Statistics

- Market Opportunity Assessment By Type

- Market Opportunity Assessment By Power Capacity

- Market Opportunity Assessment By Application

- Market Opportunity Assessment By Form

- China Lithium Ion Battery Top Companies Market Share

- China Lithium Ion Battery Competitive Benchmarking By Technical and Operational Parameters

- China Lithium Ion Battery Company Profiles

- China Lithium Ion Battery Key Strategic Recommendations

Market Covered

The report offers a comprehensive study of the subsequent market segments:

By Type

- Lithium Nickel Magnesium Cobalt (LI-NMC)

- Lithium Ferro Phosphate (LFP)

- Lithium Cobalt Oxide (LCO)

- Lithium Titanate Oxide (LTO)

- Lithium Manganese Oxide (LMO)

- Lithium Nickel Cobalt Aluminum Oxide (NCA)

By Power Capacity

- 0-300 mAH

- 3,000-10,000 mAH

- 10,000-60,000 mAH

- More than 60,000 mAH

By Application

- Consumer Electronics OEMs

- Automotive OEMs

- Energy Storage

- Industrial OEMs

- Other OEMs

- Aftermarket

By Form

- Pouch

- Cylindrical

- Elliptical

- Prismatic

- Custom Design

China Lithium Ion Battery Market (2025 - 2029): FAQs

The China Lithium-Ion Battery Market is projected to grow at a CAGR of approximately 1.18% during the forecast period.

Trends include rising EV adoption, renewable energy integration, solid-state battery research, and recycling initiatives.

Opportunities exist in EV battery manufacturing, energy storage systems, battery recycling, and next-generation solid-state technologies.

Key players include CATL, BYD, CALB, EVE Energy, and Gotion High-Tech.

6Wresearch actively monitors the China Lithium Ion Battery Market and publishes its comprehensive annual report, highlighting emerging trends, growth drivers, revenue analysis, and forecast outlook. Our insights help businesses to make data-backed strategic decisions with ongoing market dynamics. Our analysts track relevent industries related to the China Lithium Ion Battery Market, allowing our clients with actionable intelligence and reliable forecasts tailored to emerging regional needs.

Yes, we provide customisation as per your requirements. To learn more, feel free to contact us on sales@6wresearch.com

| 1 Executive Summary |

| 2 Introduction |

| 2.1 Key Highlights of the Report |

| 2.2 Report Description |

| 2.3 Market Scope & Segmentation |

| 2.4 Research Methodology |

| 2.5 Assumptions |

| 3 China Lithium Ion Battery Market Overview |

| 3.1 China Country Macro Economic Indicators |

| 3.2 China Lithium Ion Battery Market Revenues & Volume, 2019 & 2029F |

| 3.3 China Lithium Ion Battery Market - Industry Life Cycle |

| 3.4 China Lithium Ion Battery Market - Porter's Five Forces |

| 3.5 China Lithium Ion Battery Market Revenues & Volume Share, By Type, 2019 & 2029F |

| 3.6 China Lithium Ion Battery Market Revenues & Volume Share, By Power Capacity, 2019 & 2029F |

| 3.7 China Lithium Ion Battery Market Revenues & Volume Share, By Application, 2019 & 2029F |

| 3.8 China Lithium Ion Battery Market Revenues & Volume Share, By Form, 2019 & 2029F |

| 4 China Lithium Ion Battery Market Dynamics |

| 4.1 Impact Analysis |

| 4.2 Market Drivers |

| 4.2.1 Increasing demand for electric vehicles in China, leading to higher adoption of lithium-ion batteries. |

| 4.2.2 Government initiatives and policies promoting the use of renewable energy sources, driving the growth of the lithium-ion battery market. |

| 4.2.3 Technological advancements in lithium-ion battery manufacturing, leading to improved efficiency and performance. |

| 4.3 Market Restraints |

| 4.3.1 Fluctuating prices of raw materials like lithium and cobalt impacting the overall cost of lithium-ion batteries. |

| 4.3.2 Concerns regarding the safety and environmental impact of lithium-ion batteries, leading to regulatory scrutiny and potential restrictions. |

| 5 China Lithium Ion Battery Market Trends |

| 6 China Lithium Ion Battery Market, By Types |

| 6.1 China Lithium Ion Battery Market, By Type |

| 6.1.1 Overview and Analysis |

| 6.1.2 China Lithium Ion Battery Market Revenues & Volume, By Type, 2019 - 2029F |

| 6.1.3 China Lithium Ion Battery Market Revenues & Volume, By Lithium Nickel Magnesium Cobalt (LI-NMC), 2019 - 2029F |

| 6.1.4 China Lithium Ion Battery Market Revenues & Volume, By Lithium Ferro Phosphate (LFP), 2019 - 2029F |

| 6.1.5 China Lithium Ion Battery Market Revenues & Volume, By Lithium Cobalt Oxide (LCO), 2019 - 2029F |

| 6.1.6 China Lithium Ion Battery Market Revenues & Volume, By Lithium Titanate Oxide (LTO), 2019 - 2029F |

| 6.1.7 China Lithium Ion Battery Market Revenues & Volume, By Lithium Manganese Oxide (LMO), 2019 - 2029F |

| 6.1.8 China Lithium Ion Battery Market Revenues & Volume, By Lithium Nickel Cobalt Aluminum Oxide (NCA), 2019 - 2029F |

| 6.2 China Lithium Ion Battery Market, By Power Capacity |

| 6.2.1 Overview and Analysis |

| 6.2.2 China Lithium Ion Battery Market Revenues & Volume, By 0-300 mAH, 2019 - 2029F |

| 6.2.3 China Lithium Ion Battery Market Revenues & Volume, By 3,000-10,000 mAH, 2019 - 2029F |

| 6.2.4 China Lithium Ion Battery Market Revenues & Volume, By 10,000-60,000 mAH, 2019 - 2029F |

| 6.2.5 China Lithium Ion Battery Market Revenues & Volume, By More than 60,000 mAH, 2019 - 2029F |

| 6.3 China Lithium Ion Battery Market, By Application |

| 6.3.1 Overview and Analysis |

| 6.3.2 China Lithium Ion Battery Market Revenues & Volume, By Consumer Electronics OEMs, 2019 - 2029F |

| 6.3.3 China Lithium Ion Battery Market Revenues & Volume, By Automotive OEMs, 2019 - 2029F |

| 6.3.4 China Lithium Ion Battery Market Revenues & Volume, By Energy Storage, 2019 - 2029F |

| 6.3.5 China Lithium Ion Battery Market Revenues & Volume, By Industrial OEMs, 2019 - 2029F |

| 6.3.6 China Lithium Ion Battery Market Revenues & Volume, By Other OEMs, 2019 - 2029F |

| 6.3.7 China Lithium Ion Battery Market Revenues & Volume, By Aftermarket, 2019 - 2029F |

| 6.4 China Lithium Ion Battery Market, By Form |

| 6.4.1 Overview and Analysis |

| 6.4.2 China Lithium Ion Battery Market Revenues & Volume, By Pouch, 2019 - 2029F |

Global Go To Market Strategy - 2030

Export potential enables firms to identify high-growth global markets with greater confidence by combining advanced trade intelligence with a structured quantitative methodology. The framework analyzes emerging demand trends and country-level import patterns while integrating macroeconomic and trade datasets such as GDP and population forecasts, bilateral import–export flows, tariff structures, elasticity differentials between developed and developing economies, geographic distance, and import demand projections. Using weighted trade values from 2020–2024 as the base period to project country-to-country export potential for 2030, these inputs are operationalized through calculated drivers such as gravity model parameters, tariff impact factors, and projected GDP per-capita growth. Through an analysis of hidden potentials, demand hotspots, and market conditions that are most favorable to success, this method enables firms to focus on target countries, maximize returns, and global expansion with data, backed by accuracy.

By factoring in the projected importer demand gap that is currently unmet and could be potential opportunity, it identifies the potential for the Exporter (Country) among 190 countries, against the general trade analysis, which identifies the biggest importer or exporter.

To discover high-growth global markets and optimize your business strategy:

Click Here

Pricing

- Single User License$ 1,995

- Department License$ 2,400

- Site License$ 3,120

- Global License$ 3,795

Leadership Perspectives from Industry Events

Search

Thought Leadership and Analyst Meet

Our Clients

6WResearch In News

- India Export Attractiveness Tracker 2026

- India Air Conditioner Market Set for Strong Rebound in 2026 After Weather-Led Correction and GST-Driven Recovery: 6Wresearch

- ADAS in India: How Automatic Emergency Braking, Blind Spot Detection & Driver Monitoring are Transforming Road Safety

- Doha a strategic location for EV manufacturing hub: IPA Qatar

- Demand for luxury TVs surging in the GCC, says Samsung

- Empowering Growth: The Thriving Journey of Bangladesh’s Cable Industry

Latest Reports

- Nicaragua RPG Gaming Market (2026-2032)

- New Zealand RPG Gaming Market (2026-2032)

- Netherlands RPG Gaming Market (2026-2032)

- Nauru RPG Gaming Market (2026-2032)

- Namibia RPG Gaming Market (2026-2032)

- Mozambique RPG Gaming Market (2026-2032)

- Montenegro RPG Gaming Market (2026-2032)

- Mongolia RPG Gaming Market (2026-2032)

- Monaco RPG Gaming Market (2026-2032)

- Micronesia RPG Gaming Market (2026-2032)

Industry Events and Analyst Meet

EV India Expo 2026

HIMTEX 2026

India Refining Summit 2026

India EV Show 2026

EV tech India Expo 2026

Whitepaper

- Middle East & Africa Commercial Security Market Click here to view more.

- Middle East & Africa Fire Safety Systems & Equipment Market Click here to view more.

- GCC Drone Market Click here to view more.

- Middle East Lighting Fixture Market Click here to view more.

- GCC Physical & Perimeter Security Market Click here to view more.