China Lumber Market (2025-2029) | Forecast, Companies, Revenue, Trends, Value, Outlook, Growth, Industry, Size, Analysis & Share

Market Forecast By Types (Hardwood Lumber, Softwood Lumber), By Application (Construction, Furniture, Flooring, Moldings, Others) And Competitive Landscape

| Product Code: ETC036761 | Publication Date: Oct 2020 | Updated Date: Oct 2025 | Product Type: Report | |

| Publisher: 6Wresearch | Author: Ravi Bhandari | No. of Pages: 70 | No. of Figures: 35 | No. of Tables: 5 |

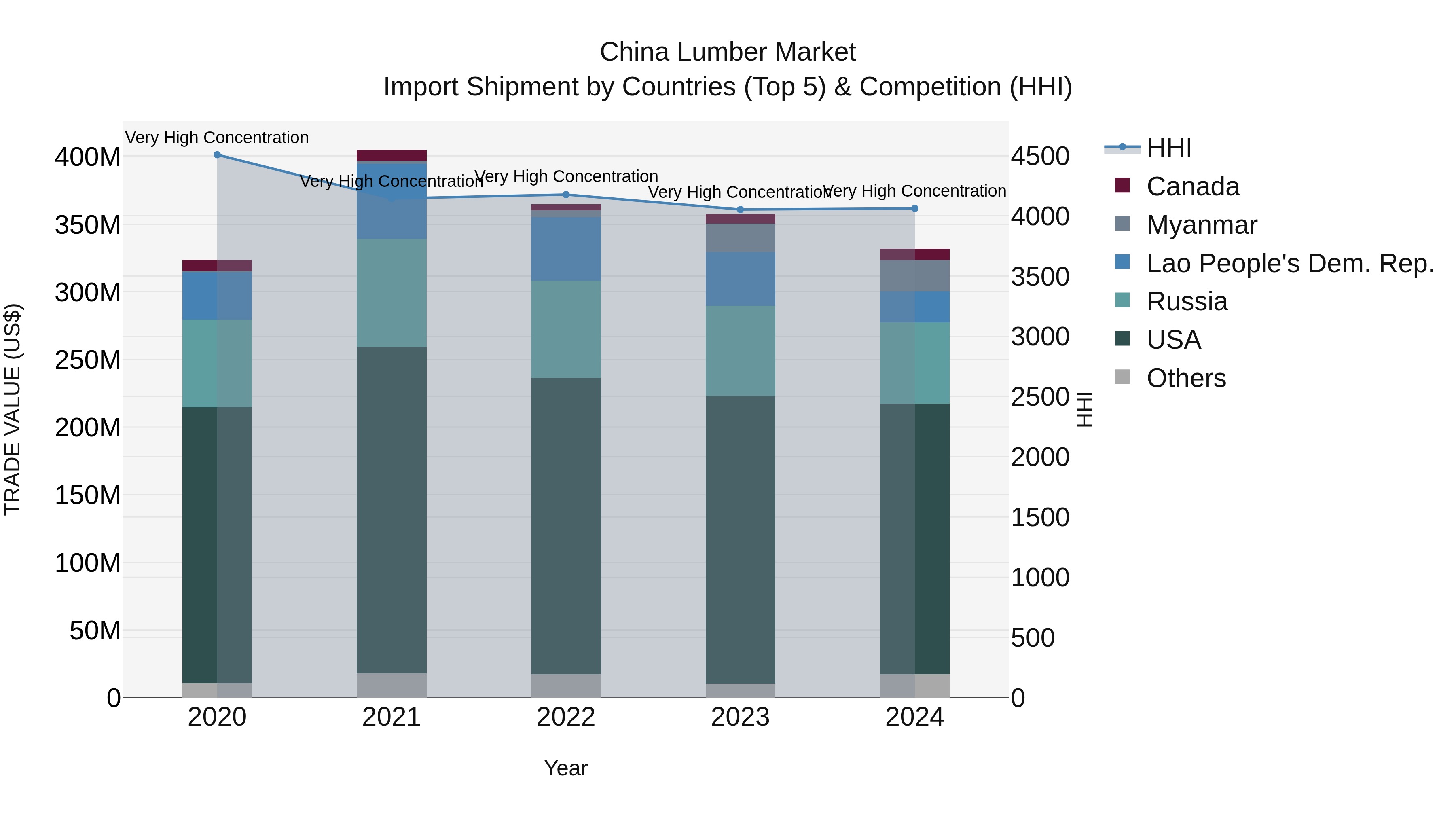

China Lumber Market Top 5 Importing Countries and Market Competition (HHI) Analysis

In 2024, China continued to rely heavily on lumber imports, with the USA, Russia, Myanmar, Lao People`s Dem. Rep., and Canada emerging as top exporting countries. Despite a modest Compound Annual Growth Rate (CAGR) of 0.64% from 2020 to 2024, the industry faced a downturn in 2024 with a negative growth rate of -7.13%. The High Herfindahl-Hirschman Index (HHI) indicates a market concentration, highlighting the dominance of key players. The market dynamics suggest a need for strategic planning and diversification to navigate challenges and capitalize on opportunities in the lumber import sector.

China Lumber Market Highlights

| Report Name | China Lumber Market |

| Forecast Period | 2025–2029 |

| CAGR | 5.33% |

| Growing Sector | Construction |

Topics Covered in the China Lumber Market Report

The China Lumber Market report thoroughly covers the market by types, and applications. The market report provides an unbiased and detailed analysis of ongoing market trends, opportunities/high growth areas, and market drivers, which would help stakeholders to devise and align their market strategies according to the current and future market dynamics.

China Lumber Market Synopsis

China Lumber Market is expected to attain major growth due to surging demand from construction, furniture, and flooring industries, supported by rapid urbanization and rising middle-class consumption. Lumber, sourced from both domestic forests and imports, is a critical raw material used across residential housing projects, commercial infrastructure, and high-quality furniture manufacturing. Furthermore, China growing exports of finished wood products and rising domestic demand for eco-friendly and certified lumber further strengthen market development.

Evaluation of Growth Drivers in the China Lumber Market

Below mentioned are some prominent drivers and their influence to the market dynamics:

| Driver | Primary Segments Affected | Why it Matters (Evidence) |

| Urbanization & Housing Demand | Construction, Flooring, Moldings | Large-scale residential and urban housing projects in China generate significant demand for lumber for structural and finishing purposes. |

| Furniture Industry Growth | Furniture, Hardwood Lumber | China is one of the largest furniture producers and exporters; demand for high-quality hardwood lumber continues to rise. |

| Infrastructure Expansion | Construction, Softwood Lumber | Mega infrastructure projects and commercial developments require cost-effective softwood lumber for scaffolding, formwork, and structural components. |

| Export Growth in Furniture & Panels | Furniture, Moldings | Increasing exports of furniture and plywood boost lumber demand in processing industries. |

| Eco-Friendly Preferences | Hardwood & Softwood Lumber | Rising consumer and regulatory demand for FSC-certified and sustainable wood promotes green lumber consumption. |

The China Lumber Market size is projected to grow at the CAGR of 5.33% during the forecast period of 2025–2029. The China Lumber Market is driven by accelerating urbanization, ongoing infrastructure projects, and increasing demand for furniture and flooring. Rising middle-class incomes and a preference for premium hardwood products further reinforce market growth. Furthermore, China Lumber Market Growth is fuelled by the booming furniture export industry, which increases the need for imported hardwoods like oak and walnut. Infrastructure growth, along with government policies supporting sustainable forestry and eco-friendly building materials, continues to drive demand. Collectively, these dynamics provide solid momentum for the expansion of the lumber industry.

Evaluation of Restraints in the China Lumber Market

Below mentioned are some major restraints and their influence to the market dynamics:

| Restraint | Primary Segments Affected | What this Means (Evidence) |

| Deforestation Concerns | Hardwood Lumber | Tight environmental policies limit excessive logging, reducing local hardwood availability. |

| Price Volatility of Imports | All types | Heavy import reliance exposes the industry to international market volatility. |

| Environmental Regulations | Construction & Furniture | Stricter standards on logging and processing increase compliance costs. |

| Substitution by Engineered Wood | Furniture, Flooring | Increasing use of MDF, plywood, and engineered wood cuts into natural lumber demand. |

| Transportation & Logistics Issues | Construction, Furniture | Extended transport distances increase costs and slow supply chain operations. |

China Lumber Market Challenges

Despite its growth, the China Lumber Industry is challenged by strict government forestry regulations that restrict overharvesting and reduce local hardwood supply. Reliance on imported wood creates exposure to volatile global pricing trends. Regulatory compliance adds to production costs, affecting profitability. Engineered wood alternatives such as MDF and plywood present stiff competition, lowering natural lumber market share. Furthermore, transportation bottlenecks and rising logistics costs contribute to inefficiencies in supply chains, making it difficult for producers to sustain margins.

China Lumber Market Trends

Several prominent trends reshaping the market growth include:

- Eco-Certified Construction Use: Builders go increasingly toward certified timber in order to comply with sustainable building codes.

- High-End Hardwood Imports: Walnut, oak, and maple imports go up with luxury furniture demand.

- Smart Sawmill Equipment: Modern machinery enhance output and reduce processing wastes.

- Global Certification Standards: FSC-and PEFC-certified wood is getting broader acceptance in trade.

- Furniture Style Shift: Demand for modern, tailor-made designs is increasing the demand for hardwood.

Investment Opportunities in the China Lumber Industry

There are some main areas of investment opportunity in the market which includes:

- Certified Eco-Lumber Production – Investment in FSC-certified supply chains to meet domestic and global green demand.

- Furniture Export-Oriented Mills – Set up lumber processing units targeting China massive furniture export market.

- Urban Construction Projects - Deliver softwood lumber for scaffolding needs, flooring, and city infrastructure works.

- Products of Innovative Engineered Lumber - Hybrid products combining natural lumber with engineered solutions are developed in terms of durability and cost-efficiency.

- Value-added finishing plants - Processing plants for kiln-dried, pre-cut, and treated lumber for premium applications.

Top 5 Leading Players in the China Lumber Market

Some leading players dominating the China Lumber Market Share include:

1. Sichuan Guodong Construction Co. Ltd.

| Company Name | Sichuan Guodong Construction Co. Ltd. |

| Establishment Year | 1989 |

| Headquarter | Chengdu, China |

| Official Website | Click here |

A diversified construction and materials company, heavily engaged in lumber distribution for housing and infrastructure projects.

2. Anxin Flooring Group

| Company Name | Anxin Flooring Group |

| Establishment Year | 1995 |

| Headquarter | Shanghai, China |

| Official Website | Click here |

A leading flooring solutions provider using both hardwood and softwood lumber, known for eco-friendly and design-driven products.

3. China Forestry Group Corporation (CFGC)

| Company Name | China Forestry Group Corporation (CFGC) |

| Establishment Year | 1984 |

| Headquarter | Beijing, China |

| Official Website | Click here |

A state-owned enterprise engaged in forestry, logging, and lumber imports, providing large-scale supply for domestic consumption.

4. Zhejiang Shiyou Timber Co. Ltd.

| Company Name | Zhejiang Shiyou Timber Co. Ltd. |

| Establishment Year | 2002 |

| Headquarter | Zhejiang, China |

| Official Website | Click here |

Specializes in hardwood imports and supply for furniture and construction industries.

5. Yihua Timber Industry Co. Ltd.

| Company Name | Yihua Timber Industry Co. Ltd. |

| Establishment Year | 1993 |

| Headquarter | Guangdong, China |

| Official Website | Click here |

A major player in furniture and lumber products, focusing on integrated supply chains from raw lumber to finished goods.

Government Regulations Introduced in the China Lumber Market

According to Chinese Government data, China government has implemented strict policies to regulate logging and promote sustainability. The government’s NFPP program bans logging in critical forest regions to protect ecosystems. The Green Building Action Plan, which drives certified eco-lumber use. Import restrictions on illegal timber and reforestation subsidies further secure domestic resources. These measures foster sustainable forestry while meeting growing demand.

Future Insights of the China Lumber Market

The China Lumber Market is projected to witness stable growth, supported by rising residential construction, expanding furniture production, and the rising use of certified timber. Rising domestic demand, along with growing furniture exports, is expected to drive steady market expansion. Advanced sawmill technology will further improve productivity and reduce waste. Furthermore, greater adoption of sustainable forestry practices will strengthen resource management, ensure environmental compliance, and enhance long-term competitiveness.

Market Segmentation Analysis

The report offers a comprehensive study of the subsequent market segments and their leading categories.

Hardwood Lumber to Dominate the Market – By Types

According to Ritika Kalra, Senior Research Analyst at 6Wresearch, the hardwood lumber category holds the largest market share in the China Lumber Market. Hardwood is highly preferred in furniture, flooring, and interior design applications due to its durability, aesthetic value, and suitability for high-end exports. Growing demand for oak, walnut, and mahogany in both domestic and international markets further cement its dominance.

Construction to Dominate the Market – By Applications

The construction sector dominates the China Lumber Industry, driven by large-scale housing, commercial complexes, and public infrastructure. Softwood lumber is widely used in scaffolding and structural applications, while hardwood is utilized for flooring, doors, and decorative interiors. With rapid urbanization and government initiatives promoting affordable housing, construction remains the largest application category.

Key Attractiveness of the Report

- 10 Years of Market Numbers.

- Historical Data Starting from 2021 to 2024.

- Base Year: 2024.

- Forecast Data until 2029.

- Key Performance Indicators Impacting the Market.

- Major Upcoming Developments and Projects.

Key Highlights of the Report:

- China Lumber Market Outlook

- Market Size of China Lumber Market, 2024

- Forecast of China Lumber Market, 2029

- Historical Data and Forecast of China Lumber Revenues & Volume for the Period 2019-2029

- China Lumber Market Trend Evolution

- China Lumber Market Drivers and Challenges

- China Lumber Price Trends

- China Lumber Porter's Five Forces

- China Lumber Industry Life Cycle

- Historical Data and Forecast of China Lumber Market Revenues & Volume By Types for the Period 2019-2029

- Historical Data and Forecast of China Lumber Market Revenues & Volume By Hardwood Lumber for the Period 2019-2029

- Historical Data and Forecast of China Lumber Market Revenues & Volume By Softwood Lumber for the Period 2019-2029

- Historical Data and Forecast of China Lumber Market Revenues & Volume By Application for the Period 2019-2029

- Historical Data and Forecast of China Lumber Market Revenues & Volume By Construction for the Period 2019-2029

- Historical Data and Forecast of China Lumber Market Revenues & Volume By Furniture for the Period 2019-2029

- Historical Data and Forecast of China Lumber Market Revenues & Volume By Flooring for the Period 2019-2029

- Historical Data and Forecast of China Lumber Market Revenues & Volume By Moldings for the Period 2019-2029

- Historical Data and Forecast of China Lumber Market Revenues & Volume By Others for the Period 2019-2029

- China Lumber Import Export Trade Statistics

- Market Opportunity Assessment By Types

- Market Opportunity Assessment By Application

- China Lumber Top Companies Market Share

- China Lumber Competitive Benchmarking By Technical and Operational Parameters

- China Lumber Company Profiles

- China Lumber Key Strategic Recommendations

Market Covered

The report offers a comprehensive study of the subsequent market segments:

By Types

- Hardwood Lumber

- Softwood Lumber

By Applications

- Construction

- Furniture

- Flooring

- Moldings

- Others

China Lumber Market (2025-2029): FAQs

The China Lumber Market is projected to grow at a CAGR of approximately 5.33% during the forecast period.

Key players include Sichuan Guodong Construction, Anxin Flooring, China Forestry Group, Zhejiang Shiyou Timber, and Yihua Timber Industry.

Trends include green building material adoption, imported hardwood preference, sawmill automation, sustainability certifications, and design-driven furniture growth.

Opportunities include eco-certified lumber production, export-oriented sawmills, urban construction supply, engineered hybrid lumber, and value-added finishing plants.

6Wresearch actively monitors the China Lumber Market and publishes its comprehensive annual report, highlighting emerging trends, growth drivers, revenue analysis, and forecast outlook. Our insights help businesses to make data-backed strategic decisions with ongoing market dynamics. Our analysts track relevent industries related to the China Lumber Market, allowing our clients with actionable intelligence and reliable forecasts tailored to emerging regional needs.

Yes, we provide customisation as per your requirements. To learn more, feel free to contact us on sales@6wresearch.com

| 1 Executive Summary |

| 2 Introduction |

| 2.1 Key Highlights of the Report |

| 2.2 Report Description |

| 2.3 Market Scope & Segmentation |

| 2.4 Research Methodology |

| 2.5 Assumptions |

| 3 China Lumber Market Overview |

| 3.1 China Country Macro Economic Indicators |

| 3.2 China Lumber Market Revenues & Volume, 2019 & 2029F |

| 3.3 China Lumber Market - Industry Life Cycle |

| 3.4 China Lumber Market - Porter's Five Forces |

| 3.5 China Lumber Market Revenues & Volume Share, By Types, 2019 & 2029F |

| 3.6 China Lumber Market Revenues & Volume Share, By Application, 2019 & 2029F |

| 4 China Lumber Market Dynamics |

| 4.1 Impact Analysis |

| 4.2 Market Drivers |

| 4.2.1 Increasing construction and infrastructure development projects in China |

| 4.2.2 Growing urbanization leading to higher demand for housing and commercial spaces |

| 4.2.3 Government initiatives promoting sustainable forestry practices and timber production |

| 4.3 Market Restraints |

| 4.3.1 Environmental concerns leading to stricter regulations on logging and deforestation |

| 4.3.2 Fluctuating global timber prices impacting import costs and competitiveness in the market |

| 5 China Lumber Market Trends |

| 6 China Lumber Market, By Types |

| 6.1 China Lumber Market, By Types |

| 6.1.1 Overview and Analysis |

| 6.1.2 China Lumber Market Revenues & Volume, By Types, 2019 - 2029F |

| 6.1.3 China Lumber Market Revenues & Volume, By Hardwood Lumber, 2019 - 2029F |

| 6.1.4 China Lumber Market Revenues & Volume, By Softwood Lumber, 2019 - 2029F |

| 6.2 China Lumber Market, By Application |

| 6.2.1 Overview and Analysis |

| 6.2.2 China Lumber Market Revenues & Volume, By Construction, 2019 - 2029F |

| 6.2.3 China Lumber Market Revenues & Volume, By Furniture, 2019 - 2029F |

| 6.2.4 China Lumber Market Revenues & Volume, By Flooring, 2019 - 2029F |

| 6.2.5 China Lumber Market Revenues & Volume, By Moldings, 2019 - 2029F |

| 6.2.6 China Lumber Market Revenues & Volume, By Others, 2019 - 2029F |

| 7 China Lumber Market Import-Export Trade Statistics |

| 7.1 China Lumber Market Export to Major Countries |

| 7.2 China Lumber Market Imports from Major Countries |

| 8 China Lumber Market Key Performance Indicators |

| 8.1 Forest certification rate in China |

| 8.2 Domestic timber production growth rate |

| 8.3 Export-to-import ratio of lumber in China |

| 9 China Lumber Market - Opportunity Assessment |

| 9.1 China Lumber Market Opportunity Assessment, By Types, 2019 & 2029F |

| 9.2 China Lumber Market Opportunity Assessment, By Application, 2019 & 2029F |

| 10 China Lumber Market - Competitive Landscape |

| 10.1 China Lumber Market Revenue Share, By Companies, 2024 |

| 10.2 China Lumber Market Competitive Benchmarking, By Operating and Technical Parameters |

| 11 Company Profiles |

| 12 Recommendations |

| 13 Disclaimer |

Global Go To Market Strategy - 2030

Export potential enables firms to identify high-growth global markets with greater confidence by combining advanced trade intelligence with a structured quantitative methodology. The framework analyzes emerging demand trends and country-level import patterns while integrating macroeconomic and trade datasets such as GDP and population forecasts, bilateral import–export flows, tariff structures, elasticity differentials between developed and developing economies, geographic distance, and import demand projections. Using weighted trade values from 2020–2024 as the base period to project country-to-country export potential for 2030, these inputs are operationalized through calculated drivers such as gravity model parameters, tariff impact factors, and projected GDP per-capita growth. Through an analysis of hidden potentials, demand hotspots, and market conditions that are most favorable to success, this method enables firms to focus on target countries, maximize returns, and global expansion with data, backed by accuracy.

By factoring in the projected importer demand gap that is currently unmet and could be potential opportunity, it identifies the potential for the Exporter (Country) among 190 countries, against the general trade analysis, which identifies the biggest importer or exporter.

To discover high-growth global markets and optimize your business strategy:

Click Here

Pricing

- Single User License$ 1,995

- Department License$ 2,400

- Site License$ 3,120

- Global License$ 3,795

Leadership Perspectives from Industry Events

Search

Thought Leadership and Analyst Meet

Our Clients

6WResearch In News

- Doha a strategic location for EV manufacturing hub: IPA Qatar

- Demand for luxury TVs surging in the GCC, says Samsung

- Empowering Growth: The Thriving Journey of Bangladesh’s Cable Industry

- Demand for luxury TVs surging in the GCC, says Samsung

- Video call with a traditional healer? Once unthinkable, it’s now common in South Africa

- Intelligent Buildings To Smooth GCC’s Path To Net Zero

Latest Reports

- Taiwan Airport Wireless Infrastructure Market (2026-2032)

- Vietnam Airport Wireless Infrastructure Market (2026-2032)

- Thailand Airport Wireless Infrastructure Market (2026-2032)

- South Korea Airport Wireless Infrastructure Market (2026-2032)

- Romania Airport Wireless Infrastructure Market (2026-2032)

- Qatar Airport Wireless Infrastructure Market (2026-2032)

- Philippines Airport Wireless Infrastructure Market (2026-2032)

- Japan Airport Wireless Infrastructure Market (2026-2032)

- Taiwan Airport Winter Services Market (2026-2032)

- Vietnam Airport Winter Services Market (2026-2032)

Industry Events and Analyst Meet

HIMTEX 2026

India Refining Summit 2026

India EV Show 2026

EV tech India Expo 2026

Auto Tech Asia 2026

Whitepaper

- Middle East & Africa Commercial Security Market Click here to view more.

- Middle East & Africa Fire Safety Systems & Equipment Market Click here to view more.

- GCC Drone Market Click here to view more.

- Middle East Lighting Fixture Market Click here to view more.

- GCC Physical & Perimeter Security Market Click here to view more.