Ethiopia Edible Oil Market (2026-2032) | Companies, Share, Outlook, Growth, Forecast, Size, Revenue, Industry, Analysis, Trends, Value & Segmentation

Market Forecast By Type (Palm Oil, Soybean Oil, Mustard Oil, Sunflower Oil, Others, ), By Packaging Type (Pouches, Jars, Cans, Bottles, ), By Pack Size (Less than 1 Litres, 1 Litres, 1 Litres - 5 litres, 5 Litres - 10 Litres, 10 Litres and Above, ), By Packaging Material (Metal, Plastic, Paper, Others), By Application (HoReCa, Home Users, Food Processing Industry, ), By Distribution Channel (Direct/Institutional Sales, Supermarkets and Hypermarkets, Convenience Stores, Online, Others) And Competitive Landscape

| Product Code: ETC5013867 | Publication Date: Nov 2023 | Updated Date: Jun 2026 | Product Type: Market Research Report | |

| Publisher: 6Wresearch | Author: Ravi Bhandari | No. of Pages: 70 | No. of Figures: 35 | No. of Tables: 5 |

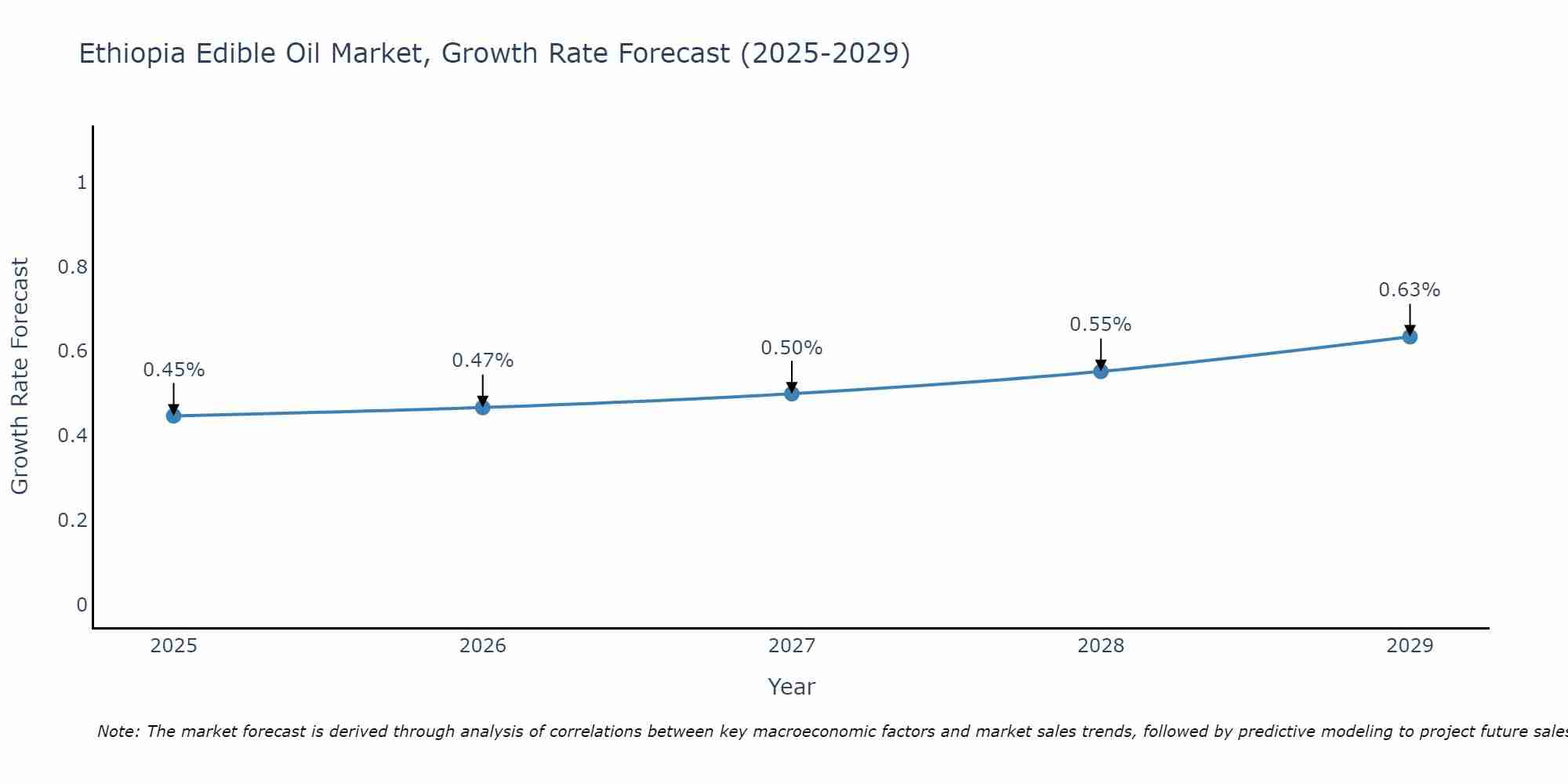

Ethiopia Edible Oil Market Size Growth Rate

The Ethiopia Edible Oil Market is likely to experience consistent growth rate gains over the period 2025 to 2029. From 0.45% in 2025, the growth rate steadily ascends to 0.63% in 2029.

Ethiopia Edible Oil Market Growth Rate

According to 6Wresearch internal database and industry insights, the Ethiopia Edible Oil Market is growing at a compound annual growth rate (CAGR) of 7.4% during the forecast period (2026–2032).

Five-Years Growth Trajectory of the Ethiopia Edible Oil Market with Core Drivers

Below mentioned are the evaluation of year-wise growth rate along with key drivers:

| Years | Est. Annual Growth in % | Growth Drivers |

| 2021 | 4.8% | Increasing population and rising household consumption of edible oils. |

| 2022 | 5.3% | Expansion of domestic oilseed crushing facilities and processing plants. |

| 2023 | 6% | Government initiatives promoting local edible oil production. |

| 2024 | 6.6% | Rising demand from restaurants, food processors, and urban households. |

| 2025 | 7% | Growth in packaged edible oils and improved retail distribution networks |

Topics Covered in the Ethiopia Edible Oil Market Report

Ethiopia Edible Oil Market report thoroughly covers the market by type, packaging type, pack size, packaging material, application, and distribution channel. The market report provides an unbiased and detailed analysis of ongoing market trends, opportunities/high growth areas, and market drivers, which would help stakeholders devise and align their market strategies according to the current and future market dynamics.

Ethiopia Edible Oil Market Highlights

| Report Name |

Ethiopia Edible Oil Market |

| Forecast period | 2026-2032 |

| CAGR | 7.4% |

| Market Size |

Residential |

Ethiopia Edible Oil Market Synopsis

The Ethiopia Edible Oil Market is expected to experience strong growth driven by increasing population, urbanization, and growing demand for packaged cooking oils. People consume more edible oil as there are more food service businesses and they use it for home cooking purpose also. The market growth is supported by government programs which promote domestic edible oil processing and funding for refinery basis. The edible oil industry in Ethiopia experiences continuous growth as of better retail distribution systems, cheap packaging options, and increased consumer product knowledge.

Evaluation of Growth Drivers in the Ethiopia Edible Oil Market

Below mentioned some growth drivers and their impact on market dynamics:

| Drivers | Primary Segments Affected | Why It Matters |

| Growing Population & Urbanization | Application, Distribution Channel | Increases overall edible oil demand. |

| Government Support for Oilseed Processing | Type, Food Processing Industry | Encourages local edible oil production. |

| Rising Packaged Oil Consumption | Packaging Type, Pack Size | Makes more demand for safe packaged oils. |

| Expansion of Retail Infrastructure | Distribution Channel | Improves product availability nationwide. |

| Food Processing Industry Growth | Application | Raises bulk edible oil consumption. |

The Ethiopia Edible Oil Market is projected to grow significantly, with a CAGR of 7.4% during the forecast period of 2026-2032. The Ethiopia Edible Oil Market experiences growth as more people in the country increase their need for cooking oils from their homes. The market expansion receives support from rising demand which the food processing sector needs to support bakeries and packaged food manufacturing companies. The government supports local production through its programs which promote domestic oilseed farming of sesame sunflower and soybean. The establishment of edible oil refining plants and the development of better distribution systems work together to decrease the need for imported products. The increasing urban population together with the shift in eating patterns drives higher demand for packaged edible oil products used in both home kitchens and commercial food service operations.

Evaluation of Restraints in the Ethiopia Edible Oil Market

Below mentioned are some major restraints and their influence on market dynamics:

| Restraints | Primary Segments Affected | What This Means |

| Dependence on Edible Oil Imports | Type, Food Processing Industry | Creates supply vulnerability and increases reliance on foreign markets. |

| Price Volatility of Oilseeds | All Segments | Leads to fluctuating edible oil prices and uncertainty for producers and consumers. |

| Limited Refining Capacity | Type, Packaging | Restricts domestic production and limits the availability of refined edible oils. |

| Logistics & Infrastructure Challenges | Distribution Channel | Causes delays in transportation and reduces distribution efficiency across regions. |

| Competition from Informal Oil Producers | Packaged Oils | Low-cost informal oils reduce demand for branded and packaged edible oil products |

Ethiopia Edible Oil Market Challenges

The Ethiopia Edible Oil Market faces challenges as the country lacks sufficient domestic oilseed processing facilities and relies on imported crude edible oils for its operations. Ethiopia edible oil price changes directly impact both production expenses and retail price determination. The rural areas of the country experience distribution problems as businesses lack proper transportation systems to deliver packaged oils effectively. Informal small-scale oil processors create competition for branded products while manufacturers struggle to maintain product quality standards throughout their production processes.

Ethiopia Edible Oil Market Trends

Some major trends contributing to the Ethiopia Edible Oil Market Growth are:

- Growing Demand for Packaged Edible Oils: There is an increasing demand among consumers for packaged products due to its hygiene and quality assurance claims and longer shelf life.

- Expansion of Domestic Oilseed Processing: The import dependency is being getting reduced due to more and more investment in the soybean and sunflower crushing plants.

- Rising Urban Consumption: A growing demand can be seen by urban consumers for edible oil due to the expansion of restaurants, street food vendors, and processed food manufacturers.

Investment Opportunities in the Ethiopia Edible Oil Market

Here are some investment opportunities in the Ethiopia Edible Oil Industry:

- Oilseed Farming Expansion: Investing in large-scale soybean and sunflower farming can strengthen the raw material supply chain for edible oil producers.

- Modern Oil Refining Facilities: The new technological advancement are encouraging the market expansion by provides modern refining plants that improve the quality and lower import reliance.

- Affordable Packaged Oil Products: Developing cost-effective packaging formats such as pouches can target price-sensitive consumers and rural markets.

Top 5 Leading Players in the Ethiopia Edible Oil Market

Here are some top companies contributing to Ethiopia Edible Oil Market Share:

1. East African Trading House PLC

| Company Name | East African Trading House PLC |

|---|---|

| Established Year | 2006 |

| Headquarters | Addis Ababa, Ethiopia |

| Official Website | Click Here |

East African Trading House PLC is one of the largest edible oil producers in Ethiopia. The company operates modern oil processing facilities producing sunflower oil, palm oil blends, and other cooking oils. It focuses on improving domestic edible oil production and reducing reliance on imports.

2. Al Impex PLC

| Company Name | Al Impex PLC |

|---|---|

| Established Year | 1994 |

| Headquarters | Addis Ababa, Ethiopia |

| Official Website | Click Here |

Al Impex PLC is a major importer and distributor of edible oils in Ethiopia. The company supplies palm oil and blended cooking oils to wholesalers, retailers, and institutional buyers across the country.

3. Holland Dairy Ethiopia PLC

| Company Name | Holland Dairy Ethiopia PLC |

|---|---|

| Established Year | 2014 |

| Headquarters | Bishoftu, Ethiopia |

| Official Website | Click Here |

Holland Dairy Ethiopia is involved in the production and distribution of food products including edible oils. The company is recognized for maintaining high-quality food processing standards and expanding distribution channels.

4. Shemu Group

| Company Name | Shemu Group |

|---|---|

| Established Year | 1993 |

| Headquarters | Addis Ababa, Ethiopia |

| Official Website | Click Here |

Shemu Group operates in food processing and distribution, including edible oil imports and packaging. The company focuses on improving product availability across supermarkets and convenience stores.

5. WA Oil Factory PLC

| Company Name | WA Oil Factory PLC |

|---|---|

| Established Year | 2010 |

| Headquarters | Addis Ababa, Ethiopia |

| Official Website | Click Here |

WA Oil Factory PLC specializes in producing and refining edible oils derived from oilseeds such as soybean and sunflower. The company focuses on expanding local refining capacity and supporting Ethiopia’s edible oil supply chain.

Government Regulations Introduced in the Ethiopia Edible Oil Market

According to Ethiopian government data, the development of the Ethiopia Edible Oil Market is well regulated by various government policies. The Ministry of Trade and Regional Integration regulates edible oil imports while promoting local production through investment incentives. The government has launched the Edible Oil Development Program to increase domestic oilseed farming and processing capacity. The Integrated Agro-Industrial Parks (IAIPs) project provides infrastructure and tax advantages to food processing industries which helps support edible oil production. The domestic supply strengthening policies work to decrease dependency on imported goods.

Future Insights of the Ethiopia Edible Oil Market

The Ethiopia Edible Oil Market maintains its positive outlook as of increasing population growth and higher urban food consumption patterns and the rising agricultural sector investment. The domestic production of oilseeds will increase as the edible oil supply chain relies on soybean and sunflower farming. The growth of retail distribution networks together with the development of contemporary packaging solutions will enhance product distribution to both urban centers and rural regions. Government policies which support food processing industries and agricultural development will drive market expansion throughout the upcoming years.

Market Segmentation Analysis

The report offers a comprehensive study of the subsequent market segments and their leading categories.

Palm Oil to Dominate the Market – By Type

According to Guneet Kaur, Senior Research Analyst, 6Wresearch, palm oil dominates the Ethiopia Edible Oil Market due to its affordability and wide availability. It is extensively used for cooking, frying, and food processing applications because of its stable shelf life and cost-effectiveness.

Pouches to Dominate the Market – By Packaging Type

Pouches are leading the market by packaging type segment. As they are affordable and convenient for daily household usage. Mainly these packaging formats are lightweight and suitable for price-sensitive consumers. Also, edible oil brands prefer pouches as they have fewer packaging costs and allow producers to offer competitive pricing.

1 Litres – 5 Litres to Dominate the Market – By Pack Size

The 1 litre – 5 litres pack size is leading the Ethiopia Edible Oil Market. As they provide with an ideal balance between affordability and consumption needs of the households. Moreover, this pack size is commonly used by families for regular cooking and offers better value compared to smaller packs.

Plastic to Dominate the Market – By Packaging Material

Plastic is leading the market by packaging type. Mainly due to its durability and lightweight properties. Also, plastic bottles and containers are popularly used by consumers for their edible oils as they protect the product from leakage and contamination.

Home Users to Dominate the Market – By Application

Home users are leading the market by application segment in the Ethiopia Edible Oil Market. Mainly due to the high reliance on home-cooked meals across the country. Edible oils are very important ingredients in traditional Ethiopian dishes, which drives consistent household consumption.

Convenience Stores to Dominate the Market – By Distribution Channel

Convenience stores is leading the market by distribution channel segment. As they are widely accessible across urban and rural areas. Also, consumers frequently purchase edible oils during routine grocery shopping from nearby small retailers.

Key attractiveness of the report

- 10 Years Market Numbers.

- Historical Data Starting from 2022 to 2025.

- Base Year: 2025

- Forecast Data until 2032.

- Key Performance Indicators Impacting the Market.

- Major Upcoming Developments and Projects.

Key Highlights of the Report:

- Ethiopia Edible Oil Market Outlook

- Market Size of Ethiopia Edible Oil Market, 2025

- Forecast of Ethiopia Edible Oil Market, 2032

- Historical Data and Forecast of Ethiopia Edible Oil Revenues & Volume for the Period 2022-3032

- Ethiopia Edible Oil Market Trend Evolution

- Ethiopia Edible Oil Market Drivers and Challenges

- Ethiopia Edible Oil Price Trends

- Ethiopia Edible Oil Porter`s Five Forces

- Ethiopia Edible Oil Industry Life Cycle

- Historical Data and Forecast of Ethiopia Edible Oil Market Revenues & Volume By Type for the Period 2022-3032

- Historical Data and Forecast of Ethiopia Edible Oil Market Revenues & Volume By Palm Oil for the Period 2022-3032

- Historical Data and Forecast of Ethiopia Edible Oil Market Revenues & Volume By Soybean Oil for the Period 2022-3032

- Historical Data and Forecast of Ethiopia Edible Oil Market Revenues & Volume By Mustard Oil for the Period 2022-3032

- Historical Data and Forecast of Ethiopia Edible Oil Market Revenues & Volume By Sunflower Oil for the Period 2022-3032

- Historical Data and Forecast of Ethiopia Edible Oil Market Revenues & Volume By Others for the Period 2022-3032

- Historical Data and Forecast of Ethiopia Edible Oil Market Revenues & Volume By for the Period 2022-3032

- Historical Data and Forecast of Ethiopia Edible Oil Market Revenues & Volume By Packaging Type for the Period 2022-3032

- Historical Data and Forecast of Ethiopia Edible Oil Market Revenues & Volume By Pouches for the Period 2022-3032

- Historical Data and Forecast of Ethiopia Edible Oil Market Revenues & Volume By Jars for the Period 2022-3032

- Historical Data and Forecast of Ethiopia Edible Oil Market Revenues & Volume By Cans for the Period 2022-3032

- Historical Data and Forecast of Ethiopia Edible Oil Market Revenues & Volume By Bottles for the Period 2022-3032

- Historical Data and Forecast of Ethiopia Edible Oil Market Revenues & Volume By for the Period 2022-3032

- Historical Data and Forecast of Ethiopia Edible Oil Market Revenues & Volume By Pack Size for the Period 2022-3032

- Historical Data and Forecast of Ethiopia Edible Oil Market Revenues & Volume By Less than 1 Litres for the Period 2022-3032

- Historical Data and Forecast of Ethiopia Edible Oil Market Revenues & Volume By 1 Litres for the Period 2022-3032

- Historical Data and Forecast of Ethiopia Edible Oil Market Revenues & Volume By 1 Litres - 5 litres for the Period 2022-3032

- Historical Data and Forecast of Ethiopia Edible Oil Market Revenues & Volume By 5 Litres - 10 Litres for the Period 2022-3032

- Historical Data and Forecast of Ethiopia Edible Oil Market Revenues & Volume By 10 Litres and Above for the Period 2022-3032

- Historical Data and Forecast of Ethiopia Edible Oil Market Revenues & Volume By for the Period 2022-3032

- Historical Data and Forecast of Ethiopia Edible Oil Market Revenues & Volume By Packaging Material for the Period 2022-3032

- Historical Data and Forecast of Ethiopia Edible Oil Market Revenues & Volume By Metal for the Period 2022-3032

- Historical Data and Forecast of Ethiopia Edible Oil Market Revenues & Volume By Plastic for the Period 2022-3032

- Historical Data and Forecast of Ethiopia Edible Oil Market Revenues & Volume By Paper for the Period 2022-3032

- Historical Data and Forecast of Ethiopia Edible Oil Market Revenues & Volume By Others for the Period 2022-3032

- Historical Data and Forecast of Ethiopia Edible Oil Market Revenues & Volume By Application for the Period 2022-3032

- Historical Data and Forecast of Ethiopia Edible Oil Market Revenues & Volume By HoReCa for the Period 2022-3032

- Historical Data and Forecast of Ethiopia Edible Oil Market Revenues & Volume By Home Users for the Period 2022-3032

- Historical Data and Forecast of Ethiopia Edible Oil Market Revenues & Volume By Food Processing Industry for the Period 2022-3032

- Historical Data and Forecast of Ethiopia Edible Oil Market Revenues & Volume By for the Period 2022-3032

- Historical Data and Forecast of Ethiopia Edible Oil Market Revenues & Volume By Distribution Channel for the Period 2022-3032

- Historical Data and Forecast of Ethiopia Edible Oil Market Revenues & Volume By Direct/Institutional Sales for the Period 2022-3032

- Historical Data and Forecast of Ethiopia Edible Oil Market Revenues & Volume By Supermarkets and Hypermarkets for the Period 2022-3032

- Historical Data and Forecast of Ethiopia Edible Oil Market Revenues & Volume By Convenience Stores for the Period 2022-3032

- Historical Data and Forecast of Ethiopia Edible Oil Market Revenues & Volume By Online for the Period 2022-3032

- Historical Data and Forecast of Ethiopia Edible Oil Market Revenues & Volume By Others for the Period 2022-3032

- Ethiopia Edible Oil Import Export Trade Statistics

- Market Opportunity Assessment By Type

- Market Opportunity Assessment By Packaging Type

- Market Opportunity Assessment By Pack Size

- Market Opportunity Assessment By Packaging Material

- Market Opportunity Assessment By Application

- Market Opportunity Assessment By Distribution Channel

- Ethiopia Edible Oil Top Companies Market Share

- Ethiopia Edible Oil Competitive Benchmarking By Technical and Operational Parameters

- Ethiopia Edible Oil Company Profiles

- Ethiopia Edible Oil Key Strategic Recommendations

Market covered

The report subsequently covers the market by following segments and subsegments.

By Type

- Palm Oil

- Soybean Oil

- Mustard Oil

- Sunflower Oil

- Others

By Packaging Type

- Pouches

- Jars

- Cans

- Bottles

By Pack Size

- Less than 1 Litres

- 1 Litres

- 1 Litres – 5 litres

- 5 Litres – 10 Litres

- 10 Litres and Above

By Packaging Material

- Metal

- Plastic

- Paper

- Others

By Application

- HoReCa

- Home Users

- Food Processing Industry

By Distribution Channel

- Direct/Institutional Sales

- Supermarkets and Hypermarkets

- Convenience Stores

- Online

- Others

Ethiopia Edible Oil Market (2026-2032): FAQs

The Ethiopia Edible Oil Market is projected to grow at a CAGR of 7.4% during the forecast period.

Programs such as the Edible Oil Development Program and Integrated Agro-Industrial Parks support oilseed cultivation and processing investments.

The palm oil remains the most widely consumed due to affordability and wide supply.

The limited refining capacity and oilseed price volatility impact the Ethiopia Edible Oil Market.

6Wresearch actively monitors the Ethiopia Edible Oil Market and publishes its comprehensive annual report, highlighting emerging trends, growth drivers, revenue analysis, and forecast outlook. Our insights help businesses to make data-backed strategic decisions with ongoing market dynamics. Our analysts track relevent industries related to the Ethiopia Edible Oil Market, allowing our clients with actionable intelligence and reliable forecasts tailored to emerging regional needs.

Yes, we provide customisation as per your requirements. To learn more, feel free to contact us on sales@6wresearch.com

| 1 Executive Summary |

| 2 Introduction |

| 2.1 Key Highlights of the Report |

| 2.2 Report Description |

| 2.3 Market Scope & Segmentation |

| 2.4 Research Methodology |

| 2.5 Assumptions |

| 3 Ethiopia Edible Oil Market Overview |

| 3.1 Ethiopia Country Macro Economic Indicators |

| 3.2 Ethiopia Edible Oil Market Revenues & Volume, 2022 & 2032F |

| 3.3 Ethiopia Edible Oil Market - Industry Life Cycle |

| 3.4 Ethiopia Edible Oil Market - Porter's Five Forces |

| 3.5 Ethiopia Edible Oil Market Revenues & Volume Share, By Type, 2022 & 2032F |

| 3.6 Ethiopia Edible Oil Market Revenues & Volume Share, By Packaging Type, 2022 & 2032F |

| 3.7 Ethiopia Edible Oil Market Revenues & Volume Share, By Pack Size, 2022 & 2032F |

| 3.8 Ethiopia Edible Oil Market Revenues & Volume Share, By Packaging Material, 2022 & 2032F |

| 3.9 Ethiopia Edible Oil Market Revenues & Volume Share, By Application, 2022 & 2032F |

| 3.10 Ethiopia Edible Oil Market Revenues & Volume Share, By Distribution Channel, 2022 & 2032F |

| 4 Ethiopia Edible Oil Market Dynamics |

| 4.1 Impact Analysis |

| 4.2 Market Drivers |

| 4.2.1 Increasing population leading to higher demand for edible oil |

| 4.2.2 Rising disposable income and changing dietary habits favoring consumption of edible oils |

| 4.2.3 Government initiatives promoting domestic production of edible oils |

| 4.3 Market Restraints |

| 4.3.1 Fluctuating prices of raw materials impacting production costs |

| 4.3.2 Dependency on imports for certain types of edible oils leading to supply chain disruptions |

| 5 Ethiopia Edible Oil Market Trends |

| 6 Ethiopia Edible Oil Market Segmentations |

| 6.1 Ethiopia Edible Oil Market, By Type |

| 6.1.1 Overview and Analysis |

| 6.1.2 Ethiopia Edible Oil Market Revenues & Volume, By Palm Oil, 2022-2032F |

| 6.1.3 Ethiopia Edible Oil Market Revenues & Volume, By Soybean Oil, 2022-2032F |

| 6.1.4 Ethiopia Edible Oil Market Revenues & Volume, By Mustard Oil, 2022-2032F |

| 6.1.5 Ethiopia Edible Oil Market Revenues & Volume, By Sunflower Oil, 2022-2032F |

| 6.1.6 Ethiopia Edible Oil Market Revenues & Volume, By Others, 2022-2032F |

| 6.1.7 Ethiopia Edible Oil Market Revenues & Volume, By , 2022-2032F |

| 6.2 Ethiopia Edible Oil Market, By Packaging Type |

| 6.2.1 Overview and Analysis |

| 6.2.2 Ethiopia Edible Oil Market Revenues & Volume, By Pouches, 2022-2032F |

| 6.2.3 Ethiopia Edible Oil Market Revenues & Volume, By Jars, 2022-2032F |

| 6.2.4 Ethiopia Edible Oil Market Revenues & Volume, By Cans, 2022-2032F |

| 6.2.5 Ethiopia Edible Oil Market Revenues & Volume, By Bottles, 2022-2032F |

| 6.2.6 Ethiopia Edible Oil Market Revenues & Volume, By , 2022-2032F |

| 6.3 Ethiopia Edible Oil Market, By Pack Size |

| 6.3.1 Overview and Analysis |

| 6.3.2 Ethiopia Edible Oil Market Revenues & Volume, By Less than 1 Litres, 2022-2032F |

| 6.3.3 Ethiopia Edible Oil Market Revenues & Volume, By 1 Litres, 2022-2032F |

| 6.3.4 Ethiopia Edible Oil Market Revenues & Volume, By 1 Litres - 5 litres, 2022-2032F |

| 6.3.5 Ethiopia Edible Oil Market Revenues & Volume, By 5 Litres - 10 Litres, 2022-2032F |

| 6.3.6 Ethiopia Edible Oil Market Revenues & Volume, By 10 Litres and Above, 2022-2032F |

| 6.3.7 Ethiopia Edible Oil Market Revenues & Volume, By , 2022-2032F |

| 6.4 Ethiopia Edible Oil Market, By Packaging Material |

| 6.4.1 Overview and Analysis |

| 6.4.2 Ethiopia Edible Oil Market Revenues & Volume, By Metal, 2022-2032F |

| 6.4.3 Ethiopia Edible Oil Market Revenues & Volume, By Plastic, 2022-2032F |

| 6.4.4 Ethiopia Edible Oil Market Revenues & Volume, By Paper, 2022-2032F |

| 6.4.5 Ethiopia Edible Oil Market Revenues & Volume, By Others, 2022-2032F |

| 6.5 Ethiopia Edible Oil Market, By Application |

| 6.5.1 Overview and Analysis |

| 6.5.2 Ethiopia Edible Oil Market Revenues & Volume, By HoReCa, 2022-2032F |

| 6.5.3 Ethiopia Edible Oil Market Revenues & Volume, By Home Users, 2022-2032F |

| 6.5.4 Ethiopia Edible Oil Market Revenues & Volume, By Food Processing Industry, 2022-2032F |

| 6.5.5 Ethiopia Edible Oil Market Revenues & Volume, By , 2022-2032F |

| 6.6 Ethiopia Edible Oil Market, By Distribution Channel |

| 6.6.1 Overview and Analysis |

| 6.6.2 Ethiopia Edible Oil Market Revenues & Volume, By Direct/Institutional Sales, 2022-2032F |

| 6.6.3 Ethiopia Edible Oil Market Revenues & Volume, By Supermarkets and Hypermarkets, 2022-2032F |

| 6.6.4 Ethiopia Edible Oil Market Revenues & Volume, By Convenience Stores, 2022-2032F |

| 6.6.5 Ethiopia Edible Oil Market Revenues & Volume, By Online, 2022-2032F |

| 6.6.6 Ethiopia Edible Oil Market Revenues & Volume, By Others, 2022-2032F |

| 7 Ethiopia Edible Oil Market Import-Export Trade Statistics |

| 7.1 Ethiopia Edible Oil Market Export to Major Countries |

| 7.2 Ethiopia Edible Oil Market Imports from Major Countries |

| 8 Ethiopia Edible Oil Market Key Performance Indicators |

| 8.1 Average per capita consumption of edible oil |

| 8.2 Number of domestic edible oil production facilities |

| 8.3 Percentage of edible oil imports compared to domestic production |

| 9 Ethiopia Edible Oil Market - Opportunity Assessment |

| 9.1 Ethiopia Edible Oil Market Opportunity Assessment, By Type, 2022 & 2032F |

| 9.2 Ethiopia Edible Oil Market Opportunity Assessment, By Packaging Type, 2022 & 2032F |

| 9.3 Ethiopia Edible Oil Market Opportunity Assessment, By Pack Size, 2022 & 2032F |

| 9.4 Ethiopia Edible Oil Market Opportunity Assessment, By Packaging Material, 2022 & 2032F |

| 9.5 Ethiopia Edible Oil Market Opportunity Assessment, By Application, 2022 & 2032F |

| 9.6 Ethiopia Edible Oil Market Opportunity Assessment, By Distribution Channel, 2022 & 2032F |

| 10 Ethiopia Edible Oil Market - Competitive Landscape |

| 10.1 Ethiopia Edible Oil Market Revenue Share, By Companies, 2025 |

| 10.2 Ethiopia Edible Oil Market Competitive Benchmarking, By Operating and Technical Parameters |

| 11 Company Profiles |

| 12 Recommendations |

| 13 Disclaimer |

Global Go To Market Strategy - 2030

Export potential enables firms to identify high-growth global markets with greater confidence by combining advanced trade intelligence with a structured quantitative methodology. The framework analyzes emerging demand trends and country-level import patterns while integrating macroeconomic and trade datasets such as GDP and population forecasts, bilateral import–export flows, tariff structures, elasticity differentials between developed and developing economies, geographic distance, and import demand projections. Using weighted trade values from 2020–2024 as the base period to project country-to-country export potential for 2030, these inputs are operationalized through calculated drivers such as gravity model parameters, tariff impact factors, and projected GDP per-capita growth. Through an analysis of hidden potentials, demand hotspots, and market conditions that are most favorable to success, this method enables firms to focus on target countries, maximize returns, and global expansion with data, backed by accuracy.

By factoring in the projected importer demand gap that is currently unmet and could be potential opportunity, it identifies the potential for the Exporter (Country) among 190 countries, against the general trade analysis, which identifies the biggest importer or exporter.

To discover high-growth global markets and optimize your business strategy:

Click Here

Pricing

- Single User License$ 1,995

- Department License$ 2,400

- Site License$ 3,120

- Global License$ 3,795

Leadership Perspectives from Industry Events

Search

Thought Leadership and Analyst Meet

Our Clients

6WResearch In News

- India Air Conditioner Market Set for Strong Rebound in 2026 After Weather-Led Correction and GST-Driven Recovery: 6Wresearch

- ADAS in India: How Automatic Emergency Braking, Blind Spot Detection & Driver Monitoring are Transforming Road Safety

- Doha a strategic location for EV manufacturing hub: IPA Qatar

- Demand for luxury TVs surging in the GCC, says Samsung

- Empowering Growth: The Thriving Journey of Bangladesh’s Cable Industry

- Demand for luxury TVs surging in the GCC, says Samsung

Latest Reports

- Nicaragua RPG Gaming Market (2026-2032)

- New Zealand RPG Gaming Market (2026-2032)

- Netherlands RPG Gaming Market (2026-2032)

- Nauru RPG Gaming Market (2026-2032)

- Namibia RPG Gaming Market (2026-2032)

- Mozambique RPG Gaming Market (2026-2032)

- Montenegro RPG Gaming Market (2026-2032)

- Mongolia RPG Gaming Market (2026-2032)

- Monaco RPG Gaming Market (2026-2032)

- Micronesia RPG Gaming Market (2026-2032)

Industry Events and Analyst Meet

EV India Expo 2026

HIMTEX 2026

India Refining Summit 2026

India EV Show 2026

EV tech India Expo 2026

Whitepaper

- Middle East & Africa Commercial Security Market Click here to view more.

- Middle East & Africa Fire Safety Systems & Equipment Market Click here to view more.

- GCC Drone Market Click here to view more.

- Middle East Lighting Fixture Market Click here to view more.

- GCC Physical & Perimeter Security Market Click here to view more.