India Automotive Glass Market (2026-2032) | Outlook, Revenue, Forecast, Growth, Industry, Companies, Trends, Analysis, Share, Size & Value

Market Forecast By Type (Laminated, Tempered), By Application (Windshield, Sidelite & Backlite, Side & Rearview Mirror), By Smart Glass (Technology, Application), By Vehicle Type (Passenger Car, Light Commercial Vehicles, Heavy Commercial Vehicles, Electric Vehicles) And Competitive Landscape

| Product Code: ETC4565485 | Publication Date: Jul 2023 | Updated Date: Nov 2025 | Product Type: Report | |

| Publisher: 6Wresearch | Author: Ravi Bhandari | No. of Pages: 70 | No. of Figures: 35 | No. of Tables: 5 |

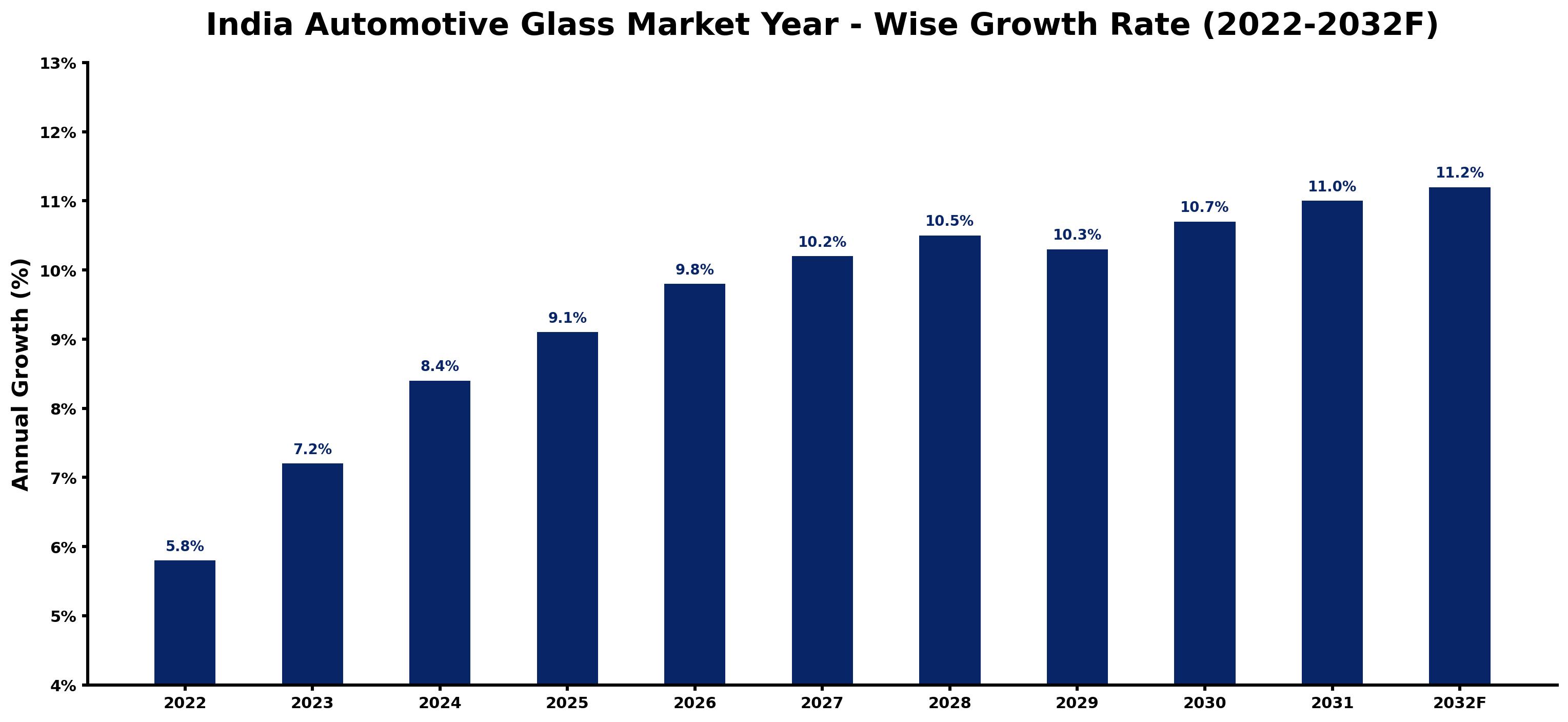

India Automotive Glass Market Growth Rate

According to 6Wresearch internal database and industry insights, the India Automotive Glass Market is projected to grow at a compound annual growth rate (CAGR) of 9.1% during the forecast period (2026-2032).

India Automotive Glass Market Year-wise Growth Rate and Key Drivers

This graph illustrates the annual growth rates of the India Automotive Glass Market from 2022 to 2032, highlighting stable industrial expansion, infrastructure-driven demand, and increasing adoption of precision finishing solutions.

The following table summarizes the historical and forecasted growth rates of the India Automotive Glass Market, along with the rationale behind each year’s performance.

| Year | Estimated Growth (%) | Market Rationale |

| 2022 | 5.8% | Recovery in passenger vehicle production and aftermarket demand following pandemic disruptions. |

| 2023 | 7.2% | Strong growth in passenger cars and SUVs, supported by improving supply chains and higher vehicle sales. |

| 2024 | 8.4% | Rising adoption of laminated and tempered safety glass, along with increasing vehicle production and exports. |

| 2025 | 9.1% | Growing demand for premium vehicles, sunroofs, and advanced automotive glazing technologies. |

| 2026 | 9.8% | Expansion of EV manufacturing, increasing OEM investments, and higher demand for lightweight automotive glass. |

| 2027 | 10.2% | Rising integration of acoustic, solar-control, and smart glass technologies in new vehicle models. |

| 2028 | 10.5% | Growth driven by premiumization, replacement demand, and increasing production capacity across India. |

| 2029 | 10.3% | Stable expansion supported by sustained automotive manufacturing and growing exports despite moderate economic normalization. |

| 2030 | 10.7% | Higher penetration of connected and electric vehicles requiring advanced glazing solutions. |

| 2031 | 11% | Strong demand for value-added automotive glass, supported by stricter safety regulations and technology upgrades. |

| 2032 | 11.2% | Market reaches maturity with continued innovation in smart glass, lightweight materials, and increasing replacement demand. |

Topics Covered in the India Automotive Glass Market Report

The India Automotive Glass Market report thoroughly covers the market by type, application, smart glass, and vehicle type. The report provides an unbiased and detailed analysis of ongoing market trends, opportunities/high-growth areas, and market drivers that will help stakeholders devise and align strategies according to current and future market dynamics.

India Automotive Glass Market Highlights

| Report Name | India Automotive Glass Market |

| Forecast period | 2026-2032 |

| CAGR | 9.1% |

| Growing Sector | Automotive Components and Materials |

India Automotive Glass Market Synopsis

The India Automotive Glass Industry is set to expand on the back of rising passenger car sales, growing SUV preference, and higher safety content per vehicle. Laminated windshields are standard, while laminated sidelights are entering upper trims to improve safety and cabin quietness. Sunroof penetration, panoramic roof designs, and head-up display (HUD) readiness are increasing the demand for specialty interlayers and coatings. The replacement market remains healthy due to a growing vehicle parc and insurance-supported repairs.

Evaluation of Growth Drivers in the India Automotive Glass Market

Below mentioned are some prominent drivers and their influence on the India Automotive Glass Market dynamics:

| Drivers | Main Segments Affected | Why It Matters |

| Safety Rules and Ratings | Type; Application | New safety rules and stronger crash tests are increasing the use of thicker laminated windshields and safer glass. |

| SUV and Sunroof Demand | Application; Type | The growth of mid-size cars and SUVs with sunroofs create the need for panoramic and soundproof glass. |

| Electric Vehicles and Smart Features | Application; Smart Glass | Smart and electric cars require special windshields that reduce noise and carry cameras and sensors. |

| Local Production and Cost Control | Type; Vehicle Type | More local factories for glass cutting and processing help reduce import costs and improve supply to automakers. |

| Aftermarket and Insurance Support | Vehicle Type; Application | Growing number of vehicles and easy insurance claims are driving steady demand for replacement windshields. |

The India Automotive Glass Market is expected to grow steadily at a 9.1% CAGR between 2026 and 2032. The upward growth of the market is driven by higher safety standards, more premium features such as sunroofs and advanced windshields, and a strong shift toward SUVs and electric vehicles. Raising domestic production capacity, better supply of interlayer materials, and wider dealer-led replacement services are improving affordability and availability. The market also gains advantage from the growing use of acoustic and solar-control glass. Increasing investments, local manufacturing, and technology upgrades, further enhance industry competitiveness and India Automotive Glass Market Growth.

Evaluation of Restraints in the India Automotive Glass Market

Below mentioned are some major restraints and their influence on the India Automotive Glass Market dynamics:

| Restraints | Main Segments Affected | What This Means |

| High Prices in Mass Market | Type; Vehicle Type | Advanced laminated and coated glass increases overall cost, so affordable local production is needed. |

| Complex Installation and Calibration | Application | It takes longer and costs more to service to recalibrate cameras and sensors after refurbishing a windshield. |

| Limited Supply of Special Materials | Smart Glass; Type | Large dependency on imported interlayers and coatings, delay manufacture and raises delivery time. |

| Risk of Damage During Transport | Type; Application | Handling big roofs or panoramic glass panels can cause breakage due to weak logistics and packaging. |

| Shortage of Skilled Technicians | Application | Insufficient number of trained professionals can lead to weak fitting, noise, leakage, and sensor issues after fixing. |

India Automotive Glass Market Challenges

Despite the growth there are challenges that the market faces. Major challenges include increasing use of scaling laminated sidelites without steep cost, expanding ADAS calibration capabilities across major cities, ensuring steady supply of specialty interlayers and coatings, and reducing handling losses for large sunroof or panoramic modules. Giving technicians the right skills, standardizing repair protocols, and developing insurance tie-ups remain significant for consistent service quality and customer confidence. Constant upgradations and domestic R&D generate long-term market stability.

India Automotive Glass Market Trends

Several significant trends are impacting the India Automotive Glass Market:

- High-Acoustic Laminates: PVB/acoustic interlayers reduce cabin noise, supporting premiumization in compact SUVs and sedans.

- Panoramic Roof Adoption: Larger roof modules drive specialized tempered/laminated assemblies and tighter dimensional controls.

- Solar & IR Control Coatings: Better thermal comfort and energy efficiency aid EV range and HVAC load reduction.

- HUD-Ready Windshields: Low-iron and wedge-controlled laminates improve projection clarity for ADAS information.

Investment Opportunities in the India Automotive Glass Industry

Some of the notable investment opportunities are:

- Interlayer & Coating Localization: Setting up PVB/acoustic interlayer and IR/UV coating lines to derisk imports and lower costs.

- ADAS Calibration Networks: Regional calibration centers bundled with windshield replacement to capture high-value services.

- Sunroof & Panoramic Modules: Local module manufacturing and bonded-glass assembly capabilities for SUVs.

- Recycling & Circular Glass: Scrap cullet recovery and reuse programs to improve yield and sustainability metrics.

Top 5 Leading Players in the India Automotive Glass Market

Below is the list of prominent companies leading in the India Automotive Glass Market Share:

1. Asahi India Glass Ltd. (AIS)

| Company Name | Asahi India Glass Ltd. (AIS) |

| Established Year | 1984 |

| Headquarters | Gurugram, India |

| Official Website | Click Here |

India’s largest automotive glass supplier with comprehensive laminated and tempered portfolio; strong OEM partnerships and nationwide replacement network.

2. Saint-Gobain Sekurit India

| Company Name | Saint-Gobain Sekurit India |

| Established Year | 1665 (Group legacy) |

| Headquarters | Paris, France; India operations in multiple locations |

| Official Website | Click Here |

Supplies laminated/tempered glazing, sunroof glass, and value-added coatings; focuses on acoustic, solar-control, and HUD-ready solutions for leading OEMs.

3. Gold Plus Glass Industry (Automotive)

| Company Name | Gold Plus Glass Industry (Automotive) |

| Established Year | 1985 |

| Headquarters | Delhi NCR, India |

| Official Website | Click Here |

Indian float and processed glass manufacturer expanding automotive lines; competitive offerings for windshields and sidelites with growing OEM linkages.

4. Guardian (Gujarat Guardian)

| Company Name | Guardian (Gujarat Guardian) |

| Established Year | 1932 |

| Headquarters | Auburn Hills, USA; India JV in Gujarat |

| Official Website | Click Here |

Provides float substrates and specialty coated glass supporting local processors; strengthens raw glass availability for automotive applications.

5. Fuyao Group (India Supply)

| Company Name | Fuyao Group (India Supply) |

| Established Year | 1987 |

| Headquarters | Fuzhou, China |

| Official Website | Click Here |

Global automotive glass major supplying select models and premium replacements; known for high precision laminated and panoramic units.

Government Regulations Introduced in the India Automotive Glass Market

According to Indian government data, initiatives such as AIS-037/IS glazing standards for safety glass, Bharat NCAP (BNCAP) star-rating adoption, and the Production Linked Incentive (PLI) scheme for Advanced Automotive Technology support category quality and localization. Examples include mandatory safety glazing compliance for windscreens and windows, higher star-rating targets encouraging laminated sidelites and better roof integrity, PLI incentives for value-added auto components like coated and acoustic glass, the Vehicle Scrappage Policy improving new vehicle sales mix.

Future Insights of the India Automotive Glass Market

The India Automotive Glass Industry will maintain strong growth as SUVs and EVs scale up, panoramic modules proliferate, and HUD/ADAS features become common. Localization of interlayers and coatings will reduce costs and lead times, while standardized calibration services and technician training will drive consistent customer experience. With OEM feature upgrades and a rising replacement market, the industry is poised for steady value addition and wider adoption of advanced glazing nationwide.

Market Segmentation Analysis

The report offers a comprehensive study of the subsequent market segments and their leading categories.

By Type – Laminated to Dominate the Market

According to Vartika, Senior Research Analyst, 6Wresearch, Laminated glass is expected to dominate India automotive glass market size due to mandatory use in windshields, rising adoption in sidelites for safety and NVH gains, and its compatibility with HUD projection and acoustic interlayers.

By Application – Windshield to Lead the Market

Windshield applications lead as every vehicle requires a laminated windshield, and this area concentrates the highest technology content: acoustic PVB, IR-control coatings, camera brackets for ADAS, rain/light sensors, and HUD readiness.

By Smart Glass – Technology and Application

By Technology, Polymer Dispersed Liquid Crystal (PDLC) is set to dominate early smart-glass deployments in India due to relative cost-effectiveness and suitability for sunshade/roof privacy, with electrochromic gaining in high-end imports.

By Vehicle Type – Passenger Car to Dominate the Market

Passenger cars dominate driven by strong compact and mid-size SUV sales and higher feature content per vehicle (sunroofs, acoustic laminates, HUD). Light commercial vehicles adopt advanced glazing more selectively; heavy commercial vehicles focus on durable tempered solutions and electric vehicles.

Key Attractiveness of the Report

- 10 Years of Market Numbers

- Historical Data Starting from 2022 to 2025

- Base Year: 2025

- Forecast Data until 2032

- Key Performance Indicators Impacting the Market

- Major Upcoming Developments and Projects

Key Highlights of the Report:

- India Automotive Glass Market Outlook

- Market Size of India Automotive Glass Market, 2025

- Forecast of India Automotive Glass Market, 2032

- Historical Data and Forecast of India Automotive Glass Revenues & Volume for the Period 2022-2032

- India Automotive Glass Market Trend Evolution

- India Automotive Glass Market Drivers and Challenges

- India Automotive Glass Price Trends

- India Automotive Glass Porter's Five Forces

- India Automotive Glass Industry Life Cycle

- Historical Data and Forecast of India Automotive Glass Market Revenues & Volume By Type for the Period 2022-2032

- Historical Data and Forecast of India Automotive Glass Market Revenues & Volume By Laminated for the Period 2022-2032

- Historical Data and Forecast of India Automotive Glass Market Revenues & Volume By Tempered for the Period 2022-2032

- Historical Data and Forecast of India Automotive Glass Market Revenues & Volume By Application for the Period 2022-2032

- Historical Data and Forecast of India Automotive Glass Market Revenues & Volume By Windshield for the Period 2022-2032

- Historical Data and Forecast of India Automotive Glass Market Revenues & Volume By Sidelite & Backlite for the Period 2022-2032

- Historical Data and Forecast of India Automotive Glass Market Revenues & Volume By Side & Rearview Mirror for the Period 2022-2032

- Historical Data and Forecast of India Automotive Glass Market Revenues & Volume By Smart Glass for the Period 2022-2032

- Historical Data and Forecast of India Automotive Glass Market Revenues & Volume By Technology for the Period 2022-2032

- Historical Data and Forecast of India Automotive Glass Market Revenues & Volume By Application for the Period 2022-2032

- Historical Data and Forecast of India Automotive Glass Market Revenues & Volume By Vehicle Type for the Period 2022-2032

- Historical Data and Forecast of India Automotive Glass Market Revenues & Volume By Passenger Car for the Period 2022-2032

- Historical Data and Forecast of India Automotive Glass Market Revenues & Volume By Light Commercial Vehicles for the Period 2022-2032

- Historical Data and Forecast of India Automotive Glass Market Revenues & Volume By Heavy Commercial Vehicles for the Period 2022-2032

- Historical Data and Forecast of India Automotive Glass Market Revenues & Volume By Electric Vehicles for the Period 2022-2032

- India Automotive Glass Import Export Trade Statistics

- Market Opportunity Assessment By Type

- Market Opportunity Assessment By Application

- Market Opportunity Assessment By Smart Glass

- Market Opportunity Assessment By Vehicle Type

- India Automotive Glass Top Companies Market Share

- India Automotive Glass Competitive Benchmarking By Technical and Operational Parameters

- India Automotive Glass Company Profiles

- India Automotive Glass Key Strategic Recommendations

Markets Covered

The India automotive glass market provides a detailed analysis of the following market segments:

By Type

- Laminated

- Tempered

By Application

- Windshield

- Sidelite & Backlite

- Side & Rearview Mirror

By Smart Glass

- Technology (Electrochromic, PDLC, SPD, Thermochromic)

- Application (Sunroof, Windshield/HUD, Sidelite Privacy)

By Vehicle Type

- Passenger Car

- Light Commercial Vehicles

- Heavy Commercial Vehicles

- Electric Vehicles

India Automotive Glass Market (2026-2032): FAQs

The India Automotive Glass Market is projected to grow at a CAGR of 9.1% during the forecast period.

Laminated glass dominates owing to mandatory windshields, growing sidelites adoption for safety and noise control, and HUD compatibility.

AIS glazing standards, BNVSAP/BNCAP safety emphasis, PLI for advanced auto components and FAME-driven EV acceleration support quality, localization, and demand.

Asahi India Glass Ltd. (AIS), Saint-Gobain Sekurit India, and Gold Plus Glass Industry (Automotive).

6Wresearch actively monitors the India Automotive Glass Market and publishes its comprehensive annual report, highlighting emerging trends, growth drivers, revenue analysis, and forecast outlook. Our insights help businesses to make data-backed strategic decisions with ongoing market dynamics. Our analysts track relevent industries related to the India Automotive Glass Market, allowing our clients with actionable intelligence and reliable forecasts tailored to emerging regional needs.

Yes, we provide customisation as per your requirements. To learn more, feel free to contact us on sales@6wresearch.com

| 1 Executive Summary |

| 2 Introduction |

| 2.1 Key Highlights of the Report |

| 2.2 Report Description |

| 2.3 Market Scope & Segmentation |

| 2.4 Research Methodology |

| 2.5 Assumptions |

| 3 India Automotive Glass Market Overview |

| 3.1 India Country Macro Economic Indicators |

| 3.2 India Automotive Glass Market Revenues & Volume, 2022 & 2032F |

| 3.3 India Automotive Glass Market - Industry Life Cycle |

| 3.4 India Automotive Glass Market - Porter's Five Forces |

| 3.5 India Automotive Glass Market Revenues & Volume Share, By Type, 2022 & 2032F |

| 3.6 India Automotive Glass Market Revenues & Volume Share, By Application, 2022 & 2032F |

| 3.7 India Automotive Glass Market Revenues & Volume Share, By Smart Glass, 2022 & 2032F |

| 3.8 India Automotive Glass Market Revenues & Volume Share, By Vehicle Type, 2022 & 2032F |

| 4 India Automotive Glass Market Dynamics |

| 4.1 Impact Analysis |

| 4.2 Market Drivers |

| 4.2.1 Increasing demand for passenger and commercial vehicles in India |

| 4.2.2 Growth in the automotive industry leading to higher production of vehicles |

| 4.2.3 Rising focus on safety features in vehicles driving the demand for advanced automotive glass technologies |

| 4.3 Market Restraints |

| 4.3.1 Fluctuating raw material prices affecting the manufacturing cost of automotive glass |

| 4.3.2 Intense competition among key players leading to pricing pressures |

| 4.3.3 Regulatory challenges related to automotive safety standards impacting the market |

| 5 India Automotive Glass Market Trends |

| 6 India Automotive Glass Market, By Types |

| 6.1 India Automotive Glass Market, By Type |

| 6.1.1 Overview and Analysis |

| 6.1.2 India Automotive Glass Market Revenues & Volume, By Type, 2022-2032F |

| 6.1.3 India Automotive Glass Market Revenues & Volume, By Laminated, 2022-2032F |

| 6.1.4 India Automotive Glass Market Revenues & Volume, By Tempered, 2022-2032F |

| 6.2 India Automotive Glass Market, By Application |

| 6.2.1 Overview and Analysis |

| 6.2.2 India Automotive Glass Market Revenues & Volume, By Windshield, 2022-2032F |

| 6.2.3 India Automotive Glass Market Revenues & Volume, By Sidelite & Backlite, 2022-2032F |

| 6.2.4 India Automotive Glass Market Revenues & Volume, By Side & Rearview Mirror, 2022-2032F |

| 6.3 India Automotive Glass Market, By Smart Glass |

| 6.3.1 Overview and Analysis |

| 6.3.2 India Automotive Glass Market Revenues & Volume, By Technology, 2022-2032F |

| 6.3.3 India Automotive Glass Market Revenues & Volume, By Application, 2022-2032F |

| 6.4 India Automotive Glass Market, By Vehicle Type |

| 6.4.1 Overview and Analysis |

| 6.4.2 India Automotive Glass Market Revenues & Volume, By Passenger Car, 2022-2032F |

| 6.4.3 India Automotive Glass Market Revenues & Volume, By Light Commercial Vehicles, 2022-2032F |

| 6.4.4 India Automotive Glass Market Revenues & Volume, By Heavy Commercial Vehicles, 2022-2032F |

| 6.4.5 India Automotive Glass Market Revenues & Volume, By Electric Vehicles, 2022-2032F |

| 7 India Automotive Glass Market Import-Export Trade Statistics |

| 7.1 India Automotive Glass Market Export to Major Countries |

| 7.2 India Automotive Glass Market Imports from Major Countries |

| 8 India Automotive Glass Market Key Performance Indicators |

| 8.1 Average selling price of automotive glass products |

| 8.2 Adoption rate of advanced automotive glass technologies |

| 8.3 Number of new vehicle models incorporating advanced glass features |

| 8.4 Investment in research and development for innovative automotive glass solutions |

| 8.5 Adoption rate of automotive safety regulations by manufacturers |

| 9 India Automotive Glass Market - Opportunity Assessment |

| 9.1 India Automotive Glass Market Opportunity Assessment, By Type, 2022 & 2032F |

| 9.2 India Automotive Glass Market Opportunity Assessment, By Application, 2022 & 2032F |

| 9.3 India Automotive Glass Market Opportunity Assessment, By Smart Glass, 2022 & 2032F |

| 9.4 India Automotive Glass Market Opportunity Assessment, By Vehicle Type, 2022 & 2032F |

| 10 India Automotive Glass Market - Competitive Landscape |

| 10.1 India Automotive Glass Market Revenue Share, By Companies, 2025 |

| 10.2 India Automotive Glass Market Competitive Benchmarking, By Operating and Technical Parameters |

| 11 Company Profiles |

| 12 Recommendations |

| 13 Disclaimer |

Global Go To Market Strategy - 2030

Export potential enables firms to identify high-growth global markets with greater confidence by combining advanced trade intelligence with a structured quantitative methodology. The framework analyzes emerging demand trends and country-level import patterns while integrating macroeconomic and trade datasets such as GDP and population forecasts, bilateral import–export flows, tariff structures, elasticity differentials between developed and developing economies, geographic distance, and import demand projections. Using weighted trade values from 2020–2024 as the base period to project country-to-country export potential for 2030, these inputs are operationalized through calculated drivers such as gravity model parameters, tariff impact factors, and projected GDP per-capita growth. Through an analysis of hidden potentials, demand hotspots, and market conditions that are most favorable to success, this method enables firms to focus on target countries, maximize returns, and global expansion with data, backed by accuracy.

By factoring in the projected importer demand gap that is currently unmet and could be potential opportunity, it identifies the potential for the Exporter (Country) among 190 countries, against the general trade analysis, which identifies the biggest importer or exporter.

To discover high-growth global markets and optimize your business strategy:

Click Here

Pricing

- Single User License$ 1,995

- Department License$ 2,400

- Site License$ 3,120

- Global License$ 3,795

Leadership Perspectives from Industry Events

Search

Thought Leadership and Analyst Meet

Our Clients

6WResearch In News

- India Export Attractiveness Tracker 2026

- India Air Conditioner Market Set for Strong Rebound in 2026 After Weather-Led Correction and GST-Driven Recovery: 6Wresearch

- ADAS in India: How Automatic Emergency Braking, Blind Spot Detection & Driver Monitoring are Transforming Road Safety

- Doha a strategic location for EV manufacturing hub: IPA Qatar

- Demand for luxury TVs surging in the GCC, says Samsung

- Empowering Growth: The Thriving Journey of Bangladesh’s Cable Industry

Latest Reports

- Nicaragua RPG Gaming Market (2026-2032)

- New Zealand RPG Gaming Market (2026-2032)

- Netherlands RPG Gaming Market (2026-2032)

- Nauru RPG Gaming Market (2026-2032)

- Namibia RPG Gaming Market (2026-2032)

- Mozambique RPG Gaming Market (2026-2032)

- Montenegro RPG Gaming Market (2026-2032)

- Mongolia RPG Gaming Market (2026-2032)

- Monaco RPG Gaming Market (2026-2032)

- Micronesia RPG Gaming Market (2026-2032)

Industry Events and Analyst Meet

EV India Expo 2026

HIMTEX 2026

India Refining Summit 2026

India EV Show 2026

EV tech India Expo 2026

Whitepaper

- Middle East & Africa Commercial Security Market Click here to view more.

- Middle East & Africa Fire Safety Systems & Equipment Market Click here to view more.

- GCC Drone Market Click here to view more.

- Middle East Lighting Fixture Market Click here to view more.

- GCC Physical & Perimeter Security Market Click here to view more.