India Heat Exchanger Market (2024-2030) | Size, Growth, Industry, Companies, Trends, Analysis, Value, Forecast, Revenue, Outlook & Share

Market Forecast By Material Types (Hastelloy, Steel, Titanium, Others (Graphite, Ceramic, Copper etc.)),By Product Types (Finned Tube Heat Exchanger/Air Cooler Heat Exchanger, Shell & Tube Heat Exchanger, Plate Heat Exchanger, Spiral Tube Heat Exchanger),By End Use Industries (Chemical, Oil and Gas, HVAC, Food and Beverages, Paper and Pulp, Power and Energy, Metal, Others (Cement, Marine etc.))And Competitive Landscape

| Product Code: ETC4378020 | Publication Date: Aug 2024 | Updated Date: Aug 2025 | Product Type: Report | |

| Publisher: 6Wresearch | Author: Ravi Bhandari | No. of Pages: 84 | No. of Figures: 27 | No. of Tables: 7 |

Topics Covered in India Heat Exchanger Market Report

India Heat Exchanger Market Report thoroughly covers the market by material types, product types and end use industries. India Heat Exchanger Market Outlook report provides an unbiased and detailed analysis of the ongoing India Heat Exchanger Market trends, opportunities/high growth areas, and market drivers. This would help stakeholders devise and align their market strategies according to the current and future market dynamics.

India Heat Exchanger Market Synopsis

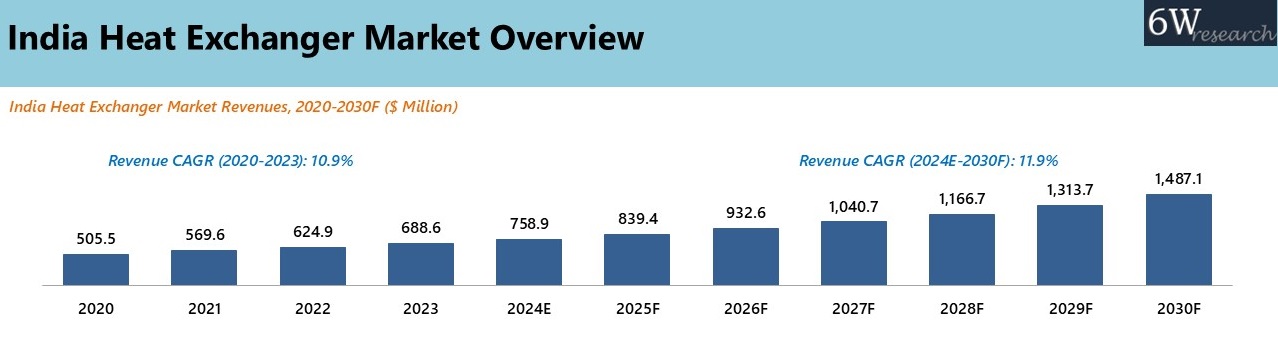

India heat exchanger market experienced rapid growth from 2020 to 2023, propelled by rising demand across key sectors such as oil and gas, and power and energy. This uptrend was underpinned by the ongoing expansion of the country's electricity generation capacity, which increased by 8% annually, with thermal power holding the largest share at 60%, complemented by renewables at 30% and hydroelectric power at 10%. Despite a downturn in early 2020 due to the COVID-19 pandemic-induced nationwide lockdown, the market swiftly rebounded post-lockdown. The revival of industrial operations nationwide, which saw a 12% increase in manufacturing output, played a crucial role in restoring the market's growth trajectory. Additionally, the chemical and pharmaceutical industries exhibited significant demand for heat exchangers, driven by a 25% surge in production and sales of COVID-19-related drugs and vaccines.

According to 6Wresearch, India Heat Exchanger Market size is projected to grow at a CAGR of 11.9% during 2024E-2030F. India heat exchanger market is poised for robust growth, fueled by various government initiatives and ambitious targets. At the COP26 event, the Government of India committed to achieving 500 GW of non-fossil fuel-based energy by 2030, underscoring its emphasis on renewable energy sources. This strategic commitment is expected to drive significant advancements in the energy sector, thereby creating a conducive environment for the heat exchanger market.

Additionally, the government has set forth plans to bolster domestic chemical sector output, aiming to reach $304 billion by 2025, up from $232.8 billion in 2022, and ultimately targeting $1000 billion by 2040. This projected expansion offers considerable opportunities for heat exchanger manufacturers, given the essential role of heat exchangers in the chemical industry. Moreover, the Indian pharmaceutical sector is anticipated to witness substantial growth, with a market size target of $130 billion by 2030. This ambitious growth trajectory will significantly drive the demand for heat exchangers within the pharmaceutical sector.

Market Segmentation by Material Types

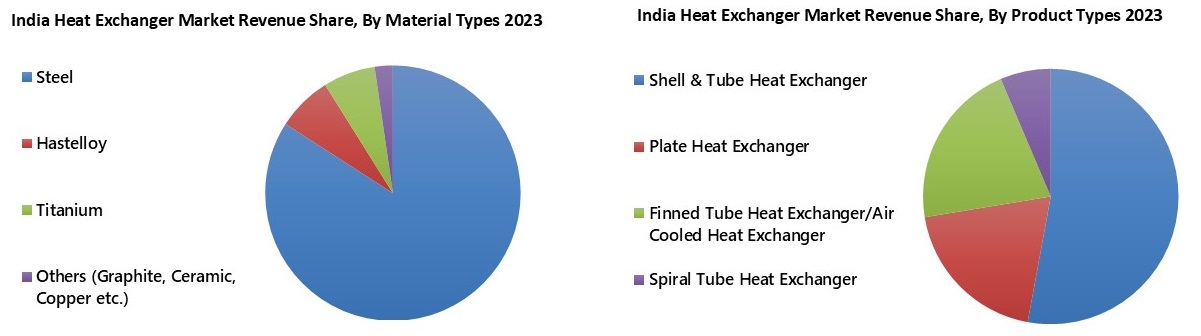

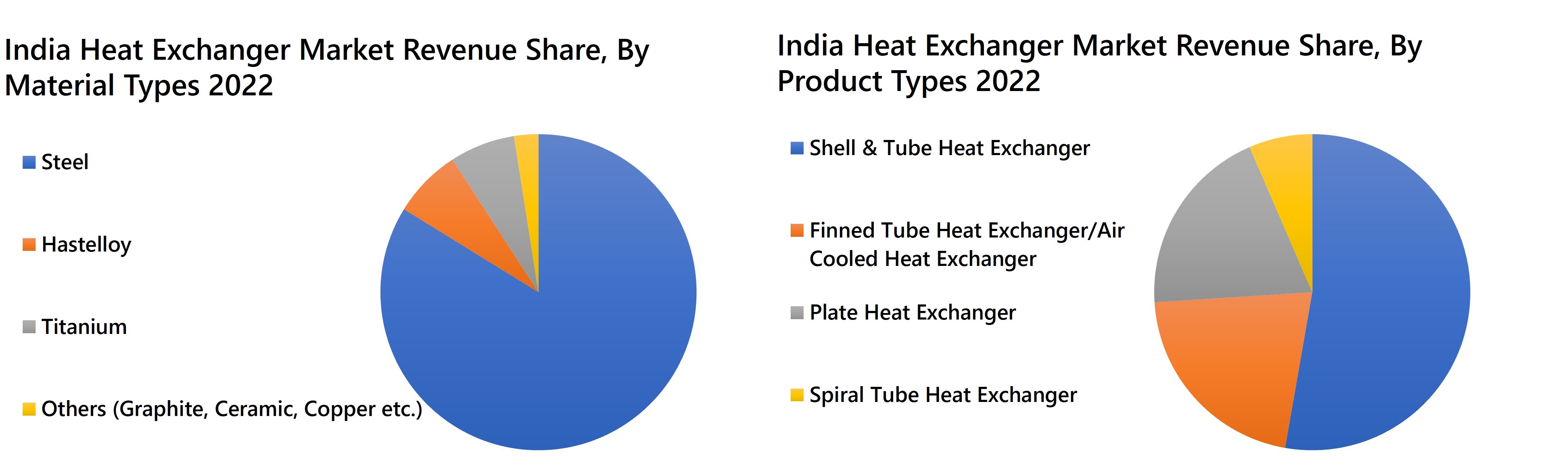

In the projected timeframe, steel heat exchangers are expected to show the highest growth due to their strength, durability, and corrosion resistance. Steel's availability and cost-effectiveness, along with its ability to be customized for specific industry needs, make it ideal for demanding industrial applications.

Market Segmentation by Product Types

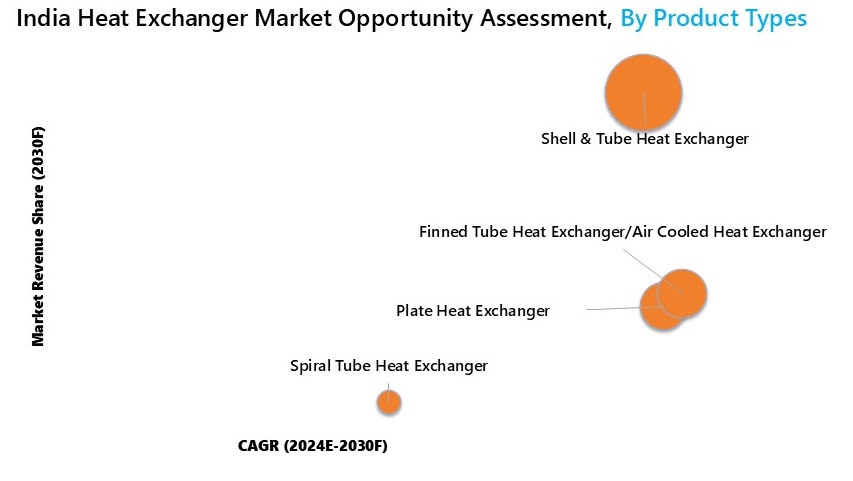

In forthcoming years, Finned Tube Heat Exchangers are set for rapid growth due to their efficiency, compact design, and versatility in HVAC, power, and chemical sectors. Their low maintenance and cost-effectiveness, along with rising demand in emerging markets, make them a top choice for efficient thermal management solutions.

Market Segmentation by End Use Industries

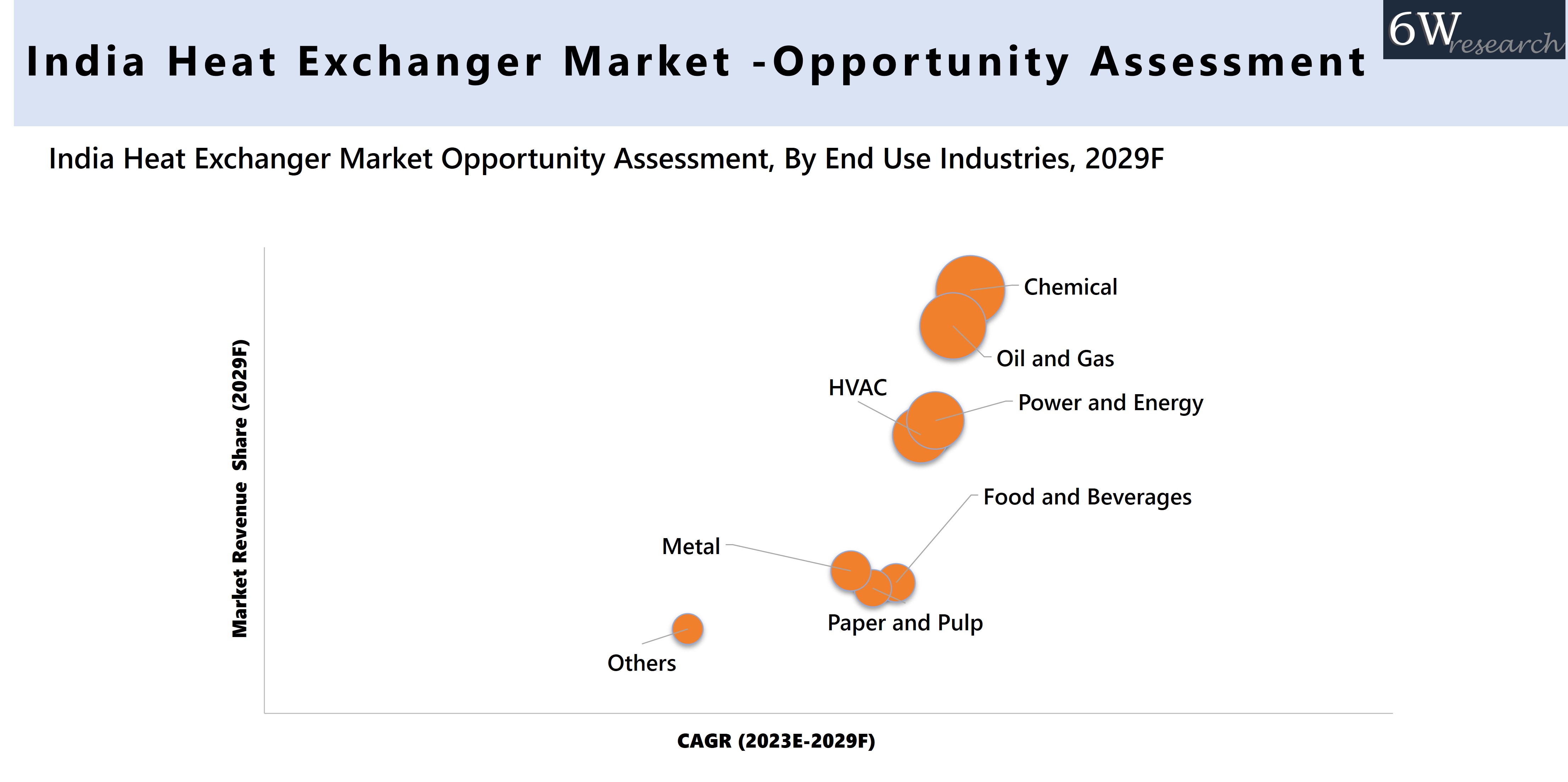

The chemical industry is expected to significantly boost the growth of India's heat exchanger market. Rising demand from sectors such as pharmaceuticals, petrochemicals, fertilizers, and specialty chemicals, coupled with factors like population growth, urbanization, and industrialization, presents substantial opportunities for OEMs to supply customized heat exchangers.

Key Attractiveness of the Report

- 10 Years Market Numbers.

- Historical Data Starting from 2020 to 2023.

- Base Year: 2023

- Forecast Data until 2030.

- Key Performance Indicators Impacting the Market.

- Major Upcoming Developments and Projects.

Key Highlights of the Report:

- India Heat Exchanger Market Overview

- India Heat Exchanger Market Outlook

- India Heat Exchanger Market Forecast

- Historical Data and Forecast of India Heat Exchanger Market Revenues, for the Period 2020-2030F

- Historical Data and Forecast of India Heat Exchanger Market Revenues, By Product Types, for the Period 2020-2030F

- Historical Data and Forecast of India Heat Exchanger Market Revenues, By Material Types, for the Period 2020-2030F

- Historical Data and Forecast of India Heat Exchanger Market Revenues, By End Use Industries, for the Period 2020-2030F

- India Heat Exchanger Market Revenue Share, By Companies

- India Heat Exchanger Market Drivers and Restraints

- India Heat Exchanger Market Trends

- India Heat Exchanger Market Porters Five Forces

- India Heat Exchanger Market Opportunity Assessment

- Company Profiles

- Key Strategic Recommendations

Market Scope and Segmentation

Thereportprovides a detailed analysis of the following market segments:

By Material Types

- Hastelloy

- Steel

- Titanium

- Others (Graphite, Ceramic, Copper etc.)

By Product Types

- Finned Tube Heat Exchanger/Air Cooler Heat Exchanger

- Shell & Tube Heat Exchanger

- Plate Heat Exchanger

- Spiral Tube Heat Exchanger

By End Use Industries

- Chemical

- Oil and Gas

- HVAC

- Food and Beverages

- Paper and Pulp

- Power and Energy

- Metal

- Others (Cement, Marine etc.)

India Heat Exchanger Market: FAQs

India heat exchangers market size is projected to grow at a CAGR of 11.9% during 2025-2031.

Government initiatives and advancements in the energy sector are the key drivers for market growth.

Steel heat exchangers accounted for the majority of revenue share in 2022 owing to their superior ability to handle high temperatures and resist corrosion compared to alternative materials like Hastelloy, Titanium, and others.

Segments that are covered in the market report are by material types, product types and end use industries.

| 1. Executive Summary |

| 2. Introduction |

| 2.1 Report Description |

| 2.2 Key Highlights of the Report |

| 2.3 Market Scope and Segmentation |

| 2.4 Research Methodology |

| 2.5 Assumptions |

| 3. India Heat Exchanger Market Overview |

| 3.1 India Heat Exchanger Market Revenues (2020-2030F) |

| 3.2 India Heat Exchanger Market Industry Life Cycle |

| 3.3 India Heat Exchanger Market Porter’s Five Forces Model |

| 4. India Heat Exchanger Market Dynamics |

| 4.1 Impact Analysis |

| 4.2 Market Drivers |

| 4.2.1 Increasing industrialization in India leading to higher demand for heat exchangers |

| 4.2.2 Growing investments in sectors like power generation, oil gas, and chemical industries |

| 4.2.3 Government initiatives focusing on energy efficiency and sustainability |

| 4.3 Market Restraints |

| 4.3.1 Fluctuating raw material prices impacting manufacturing costs |

| 4.3.2 Intense competition from international and domestic heat exchanger manufacturers |

| 4.3.3 Technological advancements leading to shorter product life cycles |

| 5. India Heat Exchanger Market Trends & Evolution |

| 6. India Heat Exchanger Market Overview, By Material Types |

| 6.1 India Heat Exchanger Market Revenue Share, By Material Types, 2023 & 2030F |

| 6.1.1 India Heat Exchanger Market Revenues, By Hastelloy (2020-2030F) |

| 6.1.2 India Heat Exchanger Market Revenues, By Steel (2020-2030F) |

| 6.1.3 India Heat Exchanger Market Revenues, By Titanium (2020-2030F) |

| 6.1.4 India Heat Exchanger Market Revenues, By Others (2020-2030F) |

| 7. India Heat Exchanger Market Overview, By Product Types |

| 7.1 India Heat Exchanger Market Revenue Share, By Product Types, 2023 & 2030F |

| 7.1.1 India Heat Exchanger Market Revenues, By Finned Tube Heat Exchanger/Air Cooler Heat Exchanger (2020-2030F) |

| 7.1.2 India Heat Exchanger Market Revenues, By Shell & Tube Heat Exchanger (2020-2030F) |

| 7.1.3 India Heat Exchanger Market Revenues, By Plate Heat Exchanger (2020-2030F) |

| 7.1.4 India Heat Exchanger Market Revenues, By Spiral Tube Heat Exchanger (2020-2030F) |

| 8. India Heat Exchanger Market Overview, By End Use Industries |

| 8.1 India Heat Exchanger Market Revenue Share, By End Use Industries, 2023 & 2030F |

| 8.1.1 India Heat Exchanger Market Revenues, By Chemical (2020-2030F) |

| 8.1.2 India Heat Exchanger Market Revenues, By Oil and Gas (2020-2030F) |

| 8.1.3 India Heat Exchanger Market Revenues, By HVAC (2020-2030F) |

| 8.1.4 India Heat Exchanger Market Revenues, By Food and Beverages (2020-2030F) |

| 8.1.5 India Heat Exchanger Market Revenues, By Paper and Pulp (2020-2030F) |

| 8.1.6 India Heat Exchanger Market Revenues, By Power and Energy (2020-2030F) |

| 8.1.7 India Heat Exchanger Market Revenues, By Metal (2020-2030F) |

| 8.1.8 India Heat Exchanger Market Revenues, By Others (2020-2030F) |

| 9. India Heat Exchanger Market - Key Performance Indicators |

| 9.1 Energy efficiency improvements in heat exchanger technology |

| 9.2 Adoption rate of heat exchangers in key industries |

| 9.3 Rate of investment in research and development for innovative heat exchanger solutions |

| 10. Key Advantages Analysis of Aluminium/Copper-Based Fins and Copper-Based Tubes |

| 11. Industry Wise Consumption Analysis of Heat Exchanger |

| 11.1 India Heat Exchanger Market - Industry Wise Consumption Analysis of Heat Exchanger (2023) |

| 11.2 India Heat Exchanger Market - Industry Wise Consumption Analysis of Heat Exchanger (2024E) |

| 12. India Heat Exchanger Market - Analysis of Government Standards, Regulations and Initiatives |

| 13. India Heat Exchanger Market - Opportunity Assessment |

| 13.1 India Heat Exchanger Market Revenues, By Material Types (2030F) |

| 13.2 India Heat Exchanger Market Revenues, By Product Types (2030F) |

| 13.3 India Heat Exchanger Market Revenues, By End Use Industries (2030F) |

| 14. India Heat Exchanger Market - Competitive Landscape |

| 14.1 India Heat Exchanger Market Revenue Share, By Companies (2023) |

| 15. Company Profiles |

| 15.1 Alfa Laval India Pvt. Ltd. |

| 15.2 REX Heat Exchanger Pvt. Ltd. |

| 15.3 HRS Process Systems Limited |

| 15.4 Danfoss Industries Pvt. Ltd. |

| 15.5 Kelvion India Pvt. Ltd. |

| 15.6 Kinam Engineering Industries |

| 15.7 Radiant Engineers |

| 15.8 Tranter |

| 15.9 Universal Heat Exchangers Ltd. |

| 15.10 KGC Engineering Projects Pvt. Ltd. |

| 15.11 ISGEC Heavy Engineering Ltd. |

| 15.12 Anup Engineering Limited |

| 15.13 Godrej & Boyce Mfg. Co. Ltd. |

| 15.14 L&T Heavy Engineering |

| 15.15 Thermax Group |

| 15.16 TEMA India |

| 15.17 BHEL |

| 16. Key Strategic Recommendations |

| 17. Disclaimer |

| List of Figures |

| 1. India Heat Exchanger Market Revenues, 2020-2030F ($ Million) |

| 2. India Current Investment Trends in Airport Infrastructure (INR Crore), 2020-2040F |

| 3. Major Petrochemical Products Production Share in FY22 |

| 4. India Major Petrochemical Production and Capacity (In 000’MT), FY22-FY26 |

| 5. Distribution of Greenhouse Emission In India 2022, By Sector |

| 6. Price Trend of Metals, Jan 2020- Jan 2023, ($/Ton) |

| 7. India Heat Exchanger Market Revenue Share, By Material Types, 2023 & 2030F |

| 8. India Heat Exchanger Market Revenue Share, By Product Types, 2023 & 2030F |

| 9. India Heat Exchanger Market Revenue Share, By End Use Industries, 2023 & 2030F |

| 10. Production & Consumption of Petroleum Products (MMT), 2019 -Nov 2022 |

| 11. Domestic Gas Production Plus Imports (BCM), 2016-2022 |

| 12. Total Power Generation in India (including renewable sources), 2011-2023 (Billion Units) |

| 13. India Chemical Industry Output ($ Billion), 2019-2025F |

| 14. India’s Major Chemical and Petrochemical Products Exports (US$ Billon), FY17-FY24 |

| 15. Imports and Exports of Chemicals (US$ Million), FY24 |

| 16. Drugs & Pharmaceuticals Exports from India (US$ Billion), FY16-FY24 |

| 17. Indian Pharmaceutical Market, 2019-2047F ($ Billion) |

| 18. R&D spending by top pharma companies in FY23 (US$ Million) |

| 19. India Heat Exchanger Market Opportunity Assessment, By Material Types, 2030F |

| 20. India Heat Exchanger Market Opportunity Assessment, By Product Types, 2030F |

| 21. India Heat Exchanger Market Opportunity Assessment, By End Use Industries, 2030F |

| 22. India Heat Exchanger Market Revenue Share, By Shell & Tube Heat Exchanger, 2023 |

| 23. India Heat Exchanger Market Revenue Share, By Finned Tube /Air Cooled Heat Exchanger Heat Exchanger, 2023 |

| 24. India Heat Exchanger Market Revenue Share, By Plate Heat Exchangers, 2023 |

| 25. India Heat Exchanger Market Revenue Share, By Spiral Tube Heat Exchanger, 2023 |

| 26. Indian Chemical Market, 2022-2040F ($ Billion) |

| 27. Indian Pharmaceutical Market, 2024-2047F ($ Billion) |

| List of Tables |

| 1. India Ongoing Office and Other Commercial Projects |

| 2. India Heat Exchanger Market Revenues, By Material Types, 2020-2030F ($ Million) |

| 3. India Heat Exchanger Market Revenues, By Product Types, 2020-2030F ($ Million) |

| 4. India Heat Exchanger Market Revenues, By End Use Industries, 2020-2030F ($ Million) |

| 5. India Heat Exchanger Market Revenues, By End Use Industries By Product Types, 2023 |

| 6. India Heat Exchanger Market Revenues, By End Use Industries By Product Types, 2024E |

| 7. Upcoming Projects for Chemical and Pharmaceutical Industries |

Market Forecast By Material Types (Hastelloy, Steel, Titanium, Others (Graphite, Ceramic, Copper etc.)), By Product Types (Finned Tube Heat Exchanger/Air Cooler Heat Exchanger, Shell & Tube Heat Exchanger, Plate Heat Exchanger, Spiral Tube Heat Exchanger), By End Use Industries (Chemical, Oil and Gas, HVAC, Food and Beverages, Paper and Pulp, Power and Energy, Metal, Others (Cement, Marine etc.)) And Competitive Landscape

| Product Code: ETC4378020 | Publication Date: Sep 2023 | Product Type: Report | |

| Publisher: 6Wresearch | No. of Pages: 84 | No. of Figures: 22 | No. of Tables: 14 |

India Heat Exchanger Market Synopsis

India heat exchanger market witnessed significant growth from 2019 to 2022, driven by the increasing demand in the oil and gas sector, as well as the power and energy sector. This growth was a result of the continuous expansion of electricity generation capacity in the country, with thermal power contributing the largest share, followed by renewables and hydroelectric power. Although the heat exchanger market experienced a decline during the first half of 2020 due to nationwide lockdown measures imposed during the COVID-19 pandemic, it regained momentum after the lifting of the lockdown. The resumption of industrial activities across the country supported the market's growth trajectory. Furthermore, the demand for heat exchangers witnessed notable growth in the chemical and pharmaceutical industries, fueled by the increased sales of COVID-19-related drugs and vaccines.

According to 6Wresearch, India heat exchangers market size is projected to grow at a CAGR of 11.6% during 2023-2029F. India heat exchanger industry is anticipated to witness substantial growth, driven by various government initiatives and ambitious targets. At the COP26 event, the Government of India announced its commitment to achieving 500 GW of non-fossil fuel-based energy by 2030, emphasizing its focus on renewable energy sources. This commitment sets the stage for significant advancements in the energy sector and creates a favorable environment for the heat exchanger market. Additionally, the government has outlined plans to enhance the domestic output of the chemical sector, with a target of reaching $304 billion by 2025, surpassing the $232.8 billion recorded in 2022, and eventually aiming for $1000 billion by 2040. This projected growth presents substantial opportunities for heat exchanger manufacturers, given the critical role of heat exchangers in the chemical industry. Furthermore, the pharmaceutical sector in India is expected to experience significant expansion, targeting a market size of $130 billion by 2030. This ambitious objective signifies substantial growth in pharmaceutical output, which will drive the demand for heat exchangers in the sector.

Market by Materials Types

Steel heat exchangers accounted for the majority of revenue share in 2022 owing to their superior ability to handle high temperatures and resist corrosion compared to alternative materials like Hastelloy, Titanium, and others. It is anticipated that steel heat exchangers will continue to dominate the market in the forthcoming years as they are known for their durability and long lifespan. Additionally, steel heat exchangers are affordable and have low installation costs compared to others.

Market by Product Types

Shell and tube Heat Exchangers accounted for the major chunk of revenue in 2022 on account of their extensive utilization in industries such as chemical, pharmaceutical, and oil and gas. Furthermore, Shell & Tube Heat Exchangers are expected to continue their dominance in upcoming years owing to their versatility in handling a wide range of fluid types, flow rates, and temperature ranges, making them suitable for diverse applications in industries such as oil and gas, chemical, power generation, and HVAC.

Market by End-Use Industries

In 2022, the chemical sector acquired a major portion of revenues in India heat exchanger market owing to the high demand for heat exchangers within the chemical industry as the chemical industry frequently involves processes that necessitate precise temperature control, efficient cooling, and heat transfer. Therefore, heat exchangers play a crucial role in facilitating these operations. In addition, after COVID-19, the chemical and pharmaceutical industry expanded significantly and are expected to follow the same trend in upcoming years. This expansion is likely to continue proliferating India heat exchanger market.

Key Attractiveness of the Report

- COVID-19 Impact on the Market.

- 11 Years Market Numbers.

- Historical Data Starting from 2019 to 2022.

- Base Year: 2022

- Forecast Data until 2029.

- Key Performance Indicators Impacting the Market.

- Major Upcoming Developments and Projects.

Key Highlights of the Report

- India Heat Exchanger Market Overview

- India Heat Exchanger Market Outlook

- India Heat Exchanger Market Forecast

- Historical Data and Forecast of India Heat Exchanger Market Revenues, for the Period 2019-2029F

- Historical Data and Forecast of India Heat Exchanger Market Revenues, By Product Types, for the Period 2019-2029F

- Historical Data and Forecast of India Heat Exchanger Market Revenues, By Material Types, for the Period 2019-2029F

- Historical Data and Forecast of India Heat Exchanger Market Revenues, By End Use Industries, for the Period 2019-2029F

- India Heat Exchanger Market Revenue Share, By Companies

- India Heat Exchanger Market Drivers and Restraints

- India Heat Exchanger Market Trends

- India Heat Exchanger Market Porters Five Forces

- India Heat Exchanger Market Opportunity Assessment

- Company Profiles

- Key Strategic Recommendations

Market Scope and Segmentation

The report provides a detailed analysis of the following market segments:

By Material Types

- Hastelloy

- Steel

- Titanium

- Others (Graphite, Ceramic, Copper etc.)

By Product Types

- Finned Tube Heat Exchanger/Air Cooler Heat Exchanger

- Shell & Tube Heat Exchanger

- Plate Heat Exchanger

- Spiral Tube Heat Exchanger

By End Use Industries

- Chemical

- Oil and Gas

- HVAC

- Food and Beverages

- Paper and Pulp

- Power and Energy

- Metal

- Others (Cement, Marine etc.)

Global Go To Market Strategy - 2030

Export potential enables firms to identify high-growth global markets with greater confidence by combining advanced trade intelligence with a structured quantitative methodology. The framework analyzes emerging demand trends and country-level import patterns while integrating macroeconomic and trade datasets such as GDP and population forecasts, bilateral import–export flows, tariff structures, elasticity differentials between developed and developing economies, geographic distance, and import demand projections. Using weighted trade values from 2020–2024 as the base period to project country-to-country export potential for 2030, these inputs are operationalized through calculated drivers such as gravity model parameters, tariff impact factors, and projected GDP per-capita growth. Through an analysis of hidden potentials, demand hotspots, and market conditions that are most favorable to success, this method enables firms to focus on target countries, maximize returns, and global expansion with data, backed by accuracy.

By factoring in the projected importer demand gap that is currently unmet and could be potential opportunity, it identifies the potential for the Exporter (Country) among 190 countries, against the general trade analysis, which identifies the biggest importer or exporter.

To discover high-growth global markets and optimize your business strategy:

Click Here

Pricing

- Single User License$ 1,995

- Department License$ 2,400

- Site License$ 3,120

- Global License$ 3,795

Leadership Perspectives from Industry Events

Search

Thought Leadership and Analyst Meet

Our Clients

6WResearch In News

- India Export Attractiveness Tracker 2026

- India Air Conditioner Market Set for Strong Rebound in 2026 After Weather-Led Correction and GST-Driven Recovery: 6Wresearch

- ADAS in India: How Automatic Emergency Braking, Blind Spot Detection & Driver Monitoring are Transforming Road Safety

- Doha a strategic location for EV manufacturing hub: IPA Qatar

- Demand for luxury TVs surging in the GCC, says Samsung

- Empowering Growth: The Thriving Journey of Bangladesh’s Cable Industry

Latest Reports

- Nicaragua RPG Gaming Market (2026-2032)

- New Zealand RPG Gaming Market (2026-2032)

- Netherlands RPG Gaming Market (2026-2032)

- Nauru RPG Gaming Market (2026-2032)

- Namibia RPG Gaming Market (2026-2032)

- Mozambique RPG Gaming Market (2026-2032)

- Montenegro RPG Gaming Market (2026-2032)

- Mongolia RPG Gaming Market (2026-2032)

- Monaco RPG Gaming Market (2026-2032)

- Micronesia RPG Gaming Market (2026-2032)

Industry Events and Analyst Meet

EV India Expo 2026

HIMTEX 2026

India Refining Summit 2026

India EV Show 2026

EV tech India Expo 2026

Whitepaper

- Middle East & Africa Commercial Security Market Click here to view more.

- Middle East & Africa Fire Safety Systems & Equipment Market Click here to view more.

- GCC Drone Market Click here to view more.

- Middle East Lighting Fixture Market Click here to view more.

- GCC Physical & Perimeter Security Market Click here to view more.