Indonesia Spine Devices Market (2026-2032) | Restraints, Technological Advancements, Market Penetration, Forecast, Supply, Share, Consumer Insights, Analysis, Demand, Innovation, Segmentation, Competitive Landscape, Size, Investment Trends, Regulations, Revenue, Landscape, Strategic Insights, Opportunities, Competition, Trends, Pricing Analysis, Future Prospects, Strategy, Value, Segments, Companies, Outlook, Challenges, Growth, Industry, Drivers

Market Forecast By Product Type (Spinal Fusion Devices, Non-Fusion Devices, Motion Preservation Devices, Vertebral Compression Fracture Devices, Others), By Material Used (Metal Alloys, Polymer, Ceramic, Biodegradable, Others), By Application (Degenerative Disc Disease, Spinal Stenosis, Herniated Disc, Spinal Deformities, Others), By End User (Hospitals, Clinics, Ambulatory Centers, Research Institutes, Others) And Competitive Landscape

| Product Code: ETC10739983 | Publication Date: Apr 2025 | Updated Date: Mar 2026 | Product Type: Market Research Report | |

| Publisher: 6Wresearch | Author: Sachin Kumar Rai | No. of Pages: 65 | No. of Figures: 34 | No. of Tables: 19 |

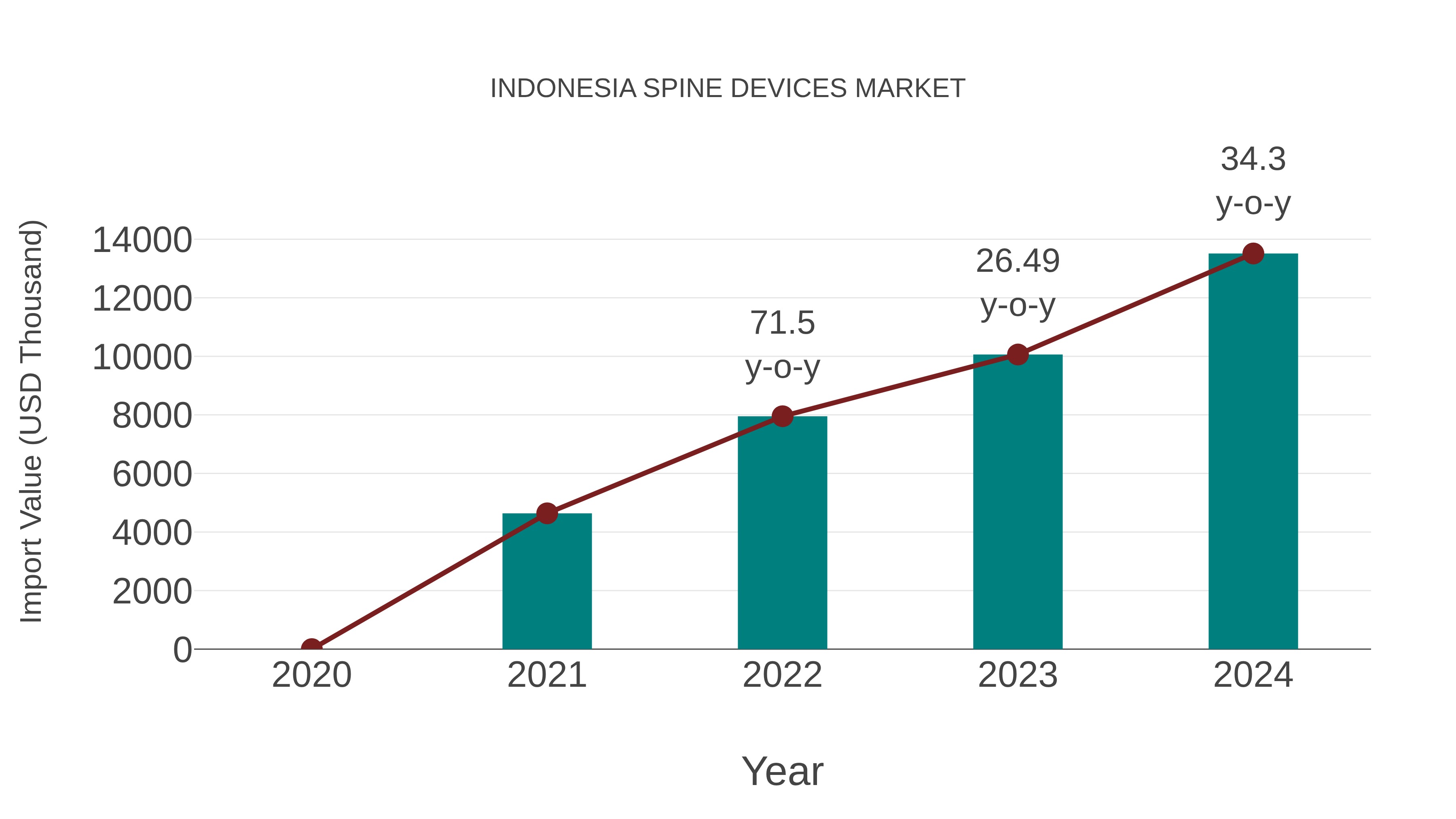

Indonesia Spine Devices Market: Import Trend Analysis

In the Indonesia spine devices market, the import trend exhibited a notable growth trajectory, with a 34.3% increase from 2023 to 2024. The compound annual growth rate (CAGR) for imports from 2020 to 2024 stood at 42.82%. This surge in imports can be attributed to a rising demand for advanced medical technologies in Indonesia`s healthcare sector, indicating a positive market momentum and increased reliance on imported spine devices to meet domestic needs.

Indonesia Spine Devices Market Overview

The Indonesia Spine Devices Market is experiencing robust growth, driven by an increasing prevalence of spinal disorders, an aging population, and rising healthcare awareness. The market encompasses a wide range of products, including fusion devices, non-fusion devices, spinal bone stimulators, and fixation systems. Urbanization and improving healthcare infrastructure have facilitated greater access to advanced spinal treatments, while government initiatives are enhancing medical device regulation and reimbursement policies. International players dominate the market, yet local manufacturers are emerging due to favorable investment climates. However, high device costs, limited skilled professionals, and uneven healthcare distribution pose challenges. Technological advancementsâsuch as minimally invasive surgical techniques and novel biomaterialsâare further propelling market expansion. Overall, the Indonesia Spine Devices Market is poised for steady growth, supported by demographic trends and ongoing healthcare modernization.

Trends of the Market

The Indonesia Spine Devices Market is experiencing robust growth, driven by rising incidences of spinal disorders, an aging population, and increasing awareness of advanced treatment options. Minimally invasive surgical procedures are gaining traction due to reduced recovery times and lower complication risks. The market is witnessing greater adoption of technologically advanced products such as motion preservation devices, 3D-printed implants, and navigation-assisted surgical systems. Local manufacturing and partnerships with international players are expanding, helping to improve product availability and affordability. Government investments in healthcare infrastructure and a growing number of specialized spine care centers further stimulate market expansion. However, high device costs and limited skilled professionals remain challenges. Overall, the market is poised for continued growth, with a focus on innovation and accessibility.

Challenges of the Market

The Indonesia Spine Devices Market faces several challenges that hinder its growth and development. Limited access to advanced healthcare infrastructure in rural and remote regions restricts patient reach and adoption of innovative spine devices. High costs associated with spine surgeries and devices, coupled with low insurance coverage, make these treatments unaffordable for a significant portion of the population. Additionally, there is a shortage of trained spine surgeons and healthcare professionals, resulting in delayed or suboptimal treatment. Regulatory hurdles and lengthy approval processes for new devices further impede market entry for international manufacturers. Moreover, low awareness about spinal disorders and available treatment options among both patients and healthcare providers adds to the challenge. Intense competition from cheaper, low-quality alternatives also poses a risk to established brands striving to maintain quality and safety standards in the market.

Investment Opportunities of the market

The Indonesia Spine Devices Market offers attractive investment opportunities driven by a growing aging population, increased prevalence of spinal disorders, and rising healthcare expenditures. The government`s commitment to healthcare infrastructure development and the expansion of private hospitals further stimulate demand for advanced spinal implants, minimally invasive surgery devices, and diagnostic equipment. Market penetration remains moderate, indicating potential for international manufacturers and local distributors to introduce innovative products and technologies. Strategic partnerships with local healthcare providers and investment in physician education can accelerate product adoption. Additionally, the emergence of value-based healthcare and rising medical tourism position Indonesia as a promising hub for both domestic and foreign investors seeking long-term growth in the spine devices sector.

Government Policy of the market

The Indonesian government has implemented several policies to enhance the healthcare sector, indirectly supporting the spine devices market. Through the National Health Insurance program (JKN), access to medical treatments, including spinal procedures, has expanded, driving demand for advanced medical devices. The Ministry of Health regulates medical devices via the Indonesian Food and Drug Authority (BPOM), mandating strict registration and quality standards for imported and locally manufactured spine devices. The government has also prioritized domestic medical device production, offering incentives to local manufacturers and requiring a certain percentage of local content in medical equipment. Additionally, import tariffs and licensing requirements are enforced to balance foreign and domestic products. These policies aim to improve healthcare quality, encourage local industry growth, and ensure patient safety in the spine devices segment.

Future Outlook of the market

The future outlook for the Indonesia Spine Devices Market is promising, driven by a growing aging population, rising prevalence of spinal disorders, and increasing awareness of advanced treatment options. Improvements in healthcare infrastructure, government initiatives to expand healthcare access, and the adoption of minimally invasive surgical techniques are expected to further boost market growth. Additionally, the market will benefit from increased investments by local and international manufacturers, as well as the introduction of innovative spine devices tailored to Indonesiaâs demographic needs. However, challenges such as high procedure costs, limited skilled professionals, and uneven access in rural areas may temper growth. Overall, the market is projected to experience steady expansion through 2030, supported by both public and private sector efforts to enhance spine care services.

Key Highlights of the Report:

- Indonesia Spine Devices Market Outlook

- Market Size of Indonesia Spine Devices Market,2025

- Forecast of Indonesia Spine Devices Market, 2032

- Historical Data and Forecast of Indonesia Spine Devices Revenues & Volume for the Period 2022-2032F

- Indonesia Spine Devices Market Trend Evolution

- Indonesia Spine Devices Market Drivers and Challenges

- Indonesia Spine Devices Price Trends

- Indonesia Spine Devices Porter's Five Forces

- Indonesia Spine Devices Industry Life Cycle

- Historical Data and Forecast of Indonesia Spine Devices Market Revenues & Volume By Product Type for the Period 2022-2032F

- Historical Data and Forecast of Indonesia Spine Devices Market Revenues & Volume By Spinal Fusion Devices for the Period 2022-2032F

- Historical Data and Forecast of Indonesia Spine Devices Market Revenues & Volume By Non-Fusion Devices for the Period 2022-2032F

- Historical Data and Forecast of Indonesia Spine Devices Market Revenues & Volume By Motion Preservation Devices for the Period 2022-2032F

- Historical Data and Forecast of Indonesia Spine Devices Market Revenues & Volume By Vertebral Compression Fracture Devices for the Period 2022-2032F

- Historical Data and Forecast of Indonesia Spine Devices Market Revenues & Volume By Others for the Period 2022-2032F

- Historical Data and Forecast of Indonesia Spine Devices Market Revenues & Volume By Material Used for the Period 2022-2032F

- Historical Data and Forecast of Indonesia Spine Devices Market Revenues & Volume By Metal Alloys for the Period 2022-2032F

- Historical Data and Forecast of Indonesia Spine Devices Market Revenues & Volume By Polymer for the Period 2022-2032F

- Historical Data and Forecast of Indonesia Spine Devices Market Revenues & Volume By Ceramic for the Period 2022-2032F

- Historical Data and Forecast of Indonesia Spine Devices Market Revenues & Volume By Biodegradable for the Period 2022-2032F

- Historical Data and Forecast of Indonesia Spine Devices Market Revenues & Volume By Others for the Period 2022-2032F

- Historical Data and Forecast of Indonesia Spine Devices Market Revenues & Volume By Application for the Period 2022-2032F

- Historical Data and Forecast of Indonesia Spine Devices Market Revenues & Volume By Degenerative Disc Disease for the Period 2022-2032F

- Historical Data and Forecast of Indonesia Spine Devices Market Revenues & Volume By Spinal Stenosis for the Period 2022-2032F

- Historical Data and Forecast of Indonesia Spine Devices Market Revenues & Volume By Herniated Disc for the Period 2022-2032F

- Historical Data and Forecast of Indonesia Spine Devices Market Revenues & Volume By Spinal Deformities for the Period 2022-2032F

- Historical Data and Forecast of Indonesia Spine Devices Market Revenues & Volume By Others for the Period 2022-2032F

- Historical Data and Forecast of Indonesia Spine Devices Market Revenues & Volume By End User for the Period 2022-2032F

- Historical Data and Forecast of Indonesia Spine Devices Market Revenues & Volume By Hospitals for the Period 2022-2032F

- Historical Data and Forecast of Indonesia Spine Devices Market Revenues & Volume By Clinics for the Period 2022-2032F

- Historical Data and Forecast of Indonesia Spine Devices Market Revenues & Volume By Ambulatory Centers for the Period 2022-2032F

- Historical Data and Forecast of Indonesia Spine Devices Market Revenues & Volume By Research Institutes for the Period 2022-2032F

- Historical Data and Forecast of Indonesia Spine Devices Market Revenues & Volume By Others for the Period 2022-2032F

- Indonesia Spine Devices Import Export Trade Statistics

- Market Opportunity Assessment By Product Type

- Market Opportunity Assessment By Material Used

- Market Opportunity Assessment By Application

- Market Opportunity Assessment By End User

- Indonesia Spine Devices Top Companies Market Share

- Indonesia Spine Devices Competitive Benchmarking By Technical and Operational Parameters

- Indonesia Spine Devices Company Profiles

- Indonesia Spine Devices Key Strategic Recommendations

Indonesia Spine Devices Market (2026-2032): FAQs

6Wresearch actively monitors the Indonesia Spine Devices Market and publishes its comprehensive annual report, highlighting emerging trends, growth drivers, revenue analysis, and forecast outlook. Our insights help businesses to make data-backed strategic decisions with ongoing market dynamics. Our analysts track relevent industries related to the Indonesia Spine Devices Market, allowing our clients with actionable intelligence and reliable forecasts tailored to emerging regional needs.

Yes, we provide customisation as per your requirements. To learn more, feel free to contact us on sales@6wresearch.com

1 Executive Summary |

2 Introduction |

2.1 Key Highlights of the Report |

2.2 Report Description |

2.3 Market Scope & Segmentation |

2.4 Research Methodology |

2.5 Assumptions |

3 Indonesia Spine Devices Market Overview |

3.1 Indonesia Country Macro Economic Indicators |

3.2 Indonesia Spine Devices Market Revenues & Volume, 2022 & 2032F |

3.3 Indonesia Spine Devices Market - Industry Life Cycle |

3.4 Indonesia Spine Devices Market - Porter's Five Forces |

3.5 Indonesia Spine Devices Market Revenues & Volume Share, By Product Type, 2022 & 2032F |

3.6 Indonesia Spine Devices Market Revenues & Volume Share, By Material Used, 2022 & 2032F |

3.7 Indonesia Spine Devices Market Revenues & Volume Share, By Application, 2022 & 2032F |

3.8 Indonesia Spine Devices Market Revenues & Volume Share, By End User, 2022 & 2032F |

4 Indonesia Spine Devices Market Dynamics |

4.1 Impact Analysis |

4.2 Market Drivers |

4.3 Market Restraints |

5 Indonesia Spine Devices Market Trends |

6 Indonesia Spine Devices Market, By Types |

6.1 Indonesia Spine Devices Market, By Product Type |

6.1.1 Overview and Analysis |

6.1.2 Indonesia Spine Devices Market Revenues & Volume, By Product Type, 2022 - 2032F |

6.1.3 Indonesia Spine Devices Market Revenues & Volume, By Spinal Fusion Devices, 2022 - 2032F |

6.1.4 Indonesia Spine Devices Market Revenues & Volume, By Non-Fusion Devices, 2022 - 2032F |

6.1.5 Indonesia Spine Devices Market Revenues & Volume, By Motion Preservation Devices, 2022 - 2032F |

6.1.6 Indonesia Spine Devices Market Revenues & Volume, By Vertebral Compression Fracture Devices, 2022 - 2032F |

6.1.7 Indonesia Spine Devices Market Revenues & Volume, By Others, 2022 - 2032F |

6.2 Indonesia Spine Devices Market, By Material Used |

6.2.1 Overview and Analysis |

6.2.2 Indonesia Spine Devices Market Revenues & Volume, By Metal Alloys, 2022 - 2032F |

6.2.3 Indonesia Spine Devices Market Revenues & Volume, By Polymer, 2022 - 2032F |

6.2.4 Indonesia Spine Devices Market Revenues & Volume, By Ceramic, 2022 - 2032F |

6.2.5 Indonesia Spine Devices Market Revenues & Volume, By Biodegradable, 2022 - 2032F |

6.2.6 Indonesia Spine Devices Market Revenues & Volume, By Others, 2022 - 2032F |

6.3 Indonesia Spine Devices Market, By Application |

6.3.1 Overview and Analysis |

6.3.2 Indonesia Spine Devices Market Revenues & Volume, By Degenerative Disc Disease, 2022 - 2032F |

6.3.3 Indonesia Spine Devices Market Revenues & Volume, By Spinal Stenosis, 2022 - 2032F |

6.3.4 Indonesia Spine Devices Market Revenues & Volume, By Herniated Disc, 2022 - 2032F |

6.3.5 Indonesia Spine Devices Market Revenues & Volume, By Spinal Deformities, 2022 - 2032F |

6.3.6 Indonesia Spine Devices Market Revenues & Volume, By Others, 2022 - 2032F |

6.4 Indonesia Spine Devices Market, By End User |

6.4.1 Overview and Analysis |

6.4.2 Indonesia Spine Devices Market Revenues & Volume, By Hospitals, 2022 - 2032F |

6.4.3 Indonesia Spine Devices Market Revenues & Volume, By Clinics, 2022 - 2032F |

6.4.4 Indonesia Spine Devices Market Revenues & Volume, By Ambulatory Centers, 2022 - 2032F |

6.4.5 Indonesia Spine Devices Market Revenues & Volume, By Research Institutes, 2022 - 2032F |

6.4.6 Indonesia Spine Devices Market Revenues & Volume, By Others, 2022 - 2032F |

7 Indonesia Spine Devices Market Import-Export Trade Statistics |

7.1 Indonesia Spine Devices Market Export to Major Countries |

7.2 Indonesia Spine Devices Market Imports from Major Countries |

8 Indonesia Spine Devices Market Key Performance Indicators |

9 Indonesia Spine Devices Market - Opportunity Assessment |

9.1 Indonesia Spine Devices Market Opportunity Assessment, By Product Type, 2022 & 2032F |

9.2 Indonesia Spine Devices Market Opportunity Assessment, By Material Used, 2022 & 2032F |

9.3 Indonesia Spine Devices Market Opportunity Assessment, By Application, 2022 & 2032F |

9.4 Indonesia Spine Devices Market Opportunity Assessment, By End User, 2022 & 2032F |

10 Indonesia Spine Devices Market - Competitive Landscape |

10.1 Indonesia Spine Devices Market Revenue Share, By Companies, 2025 |

10.2 Indonesia Spine Devices Market Competitive Benchmarking, By Operating and Technical Parameters |

11 Company Profiles |

12 Recommendations |

13 Disclaimer |

Export potential assessment - trade Analytics for 2030

Export potential enables firms to identify high-growth global markets with greater confidence by combining advanced trade intelligence with a structured quantitative methodology. The framework analyzes emerging demand trends and country-level import patterns while integrating macroeconomic and trade datasets such as GDP and population forecasts, bilateral import–export flows, tariff structures, elasticity differentials between developed and developing economies, geographic distance, and import demand projections. Using weighted trade values from 2020–2024 as the base period to project country-to-country export potential for 2030, these inputs are operationalized through calculated drivers such as gravity model parameters, tariff impact factors, and projected GDP per-capita growth. Through an analysis of hidden potentials, demand hotspots, and market conditions that are most favorable to success, this method enables firms to focus on target countries, maximize returns, and global expansion with data, backed by accuracy.

By factoring in the projected importer demand gap that is currently unmet and could be potential opportunity, it identifies the potential for the Exporter (Country) among 190 countries, against the general trade analysis, which identifies the biggest importer or exporter.

To discover high-growth global markets and optimize your business strategy:

Click Here

Pricing

- Single User License$ 1,995

- Department License$ 2,400

- Site License$ 3,120

- Global License$ 3,795

Search

Thought Leadership and Analyst Meet

Our Clients

Latest Reports

- Canada Cloud CFD Market (2026-2032) | Size & Revenue, Industry, Growth, Competitive Landscape, Forecast, Segmentation, Value, Outlook, Trends, Share, Analysis, Companies

- Taiwan Food Delivery Platform Market (2026-2032) | Companies, Outlook, Analysis, Trends, Value, Revenue, Segmentation, Share, Forecast, Competitive Landscape, Growth, Size & Forecast

- United Kingdom (UK) Long-term Care Insurance Market (2026-2032) | Growth, Share, Consumer Insights, Drivers, Opportunities, Competition, Pricing Analysis, Segments, Restraints, Companies, Competitive, Value, Outlook, Size, Demand, Analysis, Challenges, Strategic Insights, Investment Trends, Revenue, Trends, Supply, Forecast

- United Kingdom (UK) Long Term Care Market (2026-2032) | Companies, Outlook, Analysis, Trends, Value, Revenue, Segmentation, Share, Forecast, Competitive Landscape, Growth, Size & Forecast

- Iraq Insulation and Waterproofing Market (2026-2032) | Outlook, Drivers, Growth, Size, Share, Industry, Revenue, Trends, Demand, Competitive, Strategic Insights, Opportunities, Segments, Companies, Challenges, Strategy, Consumer Insights, Analysis, Investment Trends, Value, Segmentation, Forecast, Restraints

- India Switchgear Market Outlook (2026-2032) | Size, Share, Trends, Growth, Revenue, Forecast, Analysis, Value, Outlook

- Pakistan Contraceptive Implants Market (2025-2031) | Demand, Growth, Size, Share, Industry, Pricing Analysis, Competitive, Strategic Insights, Strategy, Consumer Insights, Analysis, Investment Trends, Opportunities, Revenue, Segments, Value, Segmentation, Supply, Forecast, Restraints, Outlook, Competition, Drivers, Trends, Companies, Challenges

- Sri Lanka Packaging Market (2026-2032) | Outlook, Competition, Drivers, Trends, Demand, Pricing Analysis, Competitive, Strategic Insights, Companies, Challenges, Strategy, Consumer Insights, Analysis, Investment Trends, Opportunities, Growth, Size, Share, Industry, Revenue, Segments, Value, Segmentation, Supply, Forecast, Restraints

- India Kids Watches Market (2026-2032) | Strategy, Consumer Insights, Analysis, Investment Trends, Opportunities, Growth, Size, Share, Industry, Revenue, Segments, Value, Segmentation, Supply, Forecast, Restraints, Outlook, Competition, Drivers, Trends, Demand, Pricing Analysis, Competitive, Strategic Insights, Companies, Challenges

- Saudi Arabia Core Assurance Service Market (2025-2031) | Strategy, Consumer Insights, Analysis, Investment Trends, Opportunities, Growth, Size, Share, Industry, Revenue, Segments, Value, Segmentation, Supply, Forecast, Restraints, Outlook, Competition, Drivers, Trends, Demand, Pricing Analysis, Competitive, Strategic Insights, Companies, Challenges

Industry Events and Analyst Meet

India EV Show 2026

EV tech India Expo 2026

Auto Tech Asia 2026

Battery Tech India 2026

Smart Production Solutions Guangzhou 2026

Whitepaper

- Middle East & Africa Commercial Security Market Click here to view more.

- Middle East & Africa Fire Safety Systems & Equipment Market Click here to view more.

- GCC Drone Market Click here to view more.

- Middle East Lighting Fixture Market Click here to view more.

- GCC Physical & Perimeter Security Market Click here to view more.

6WResearch In News

- Doha a strategic location for EV manufacturing hub: IPA Qatar

- Demand for luxury TVs surging in the GCC, says Samsung

- Empowering Growth: The Thriving Journey of Bangladesh’s Cable Industry

- Demand for luxury TVs surging in the GCC, says Samsung

- Video call with a traditional healer? Once unthinkable, it’s now common in South Africa

- Intelligent Buildings To Smooth GCC’s Path To Net Zero