Japan Structural Adhesives Market (2026-2032) | Industry, Forecast, Outlook, Growth, Value, Trends, Analysis, Competitive Landscape, Size & Revenue, Segmentation, Share, Companies

Market Forecast By Product Type (Epoxy, Acrylic, Urethanes, Cyanoacrylate, Others), By End- use (Automotive, Aerospace, Marine, Building & Construction, Wind Energy, Others) And Competitive Landscape

| Product Code: ETC7749417 | Publication Date: Sep 2024 | Updated Date: Mar 2026 | Product Type: Market Research Report | |

| Publisher: 6Wresearch | Author: Summon Dutta | No. of Pages: 75 | No. of Figures: 35 | No. of Tables: 20 |

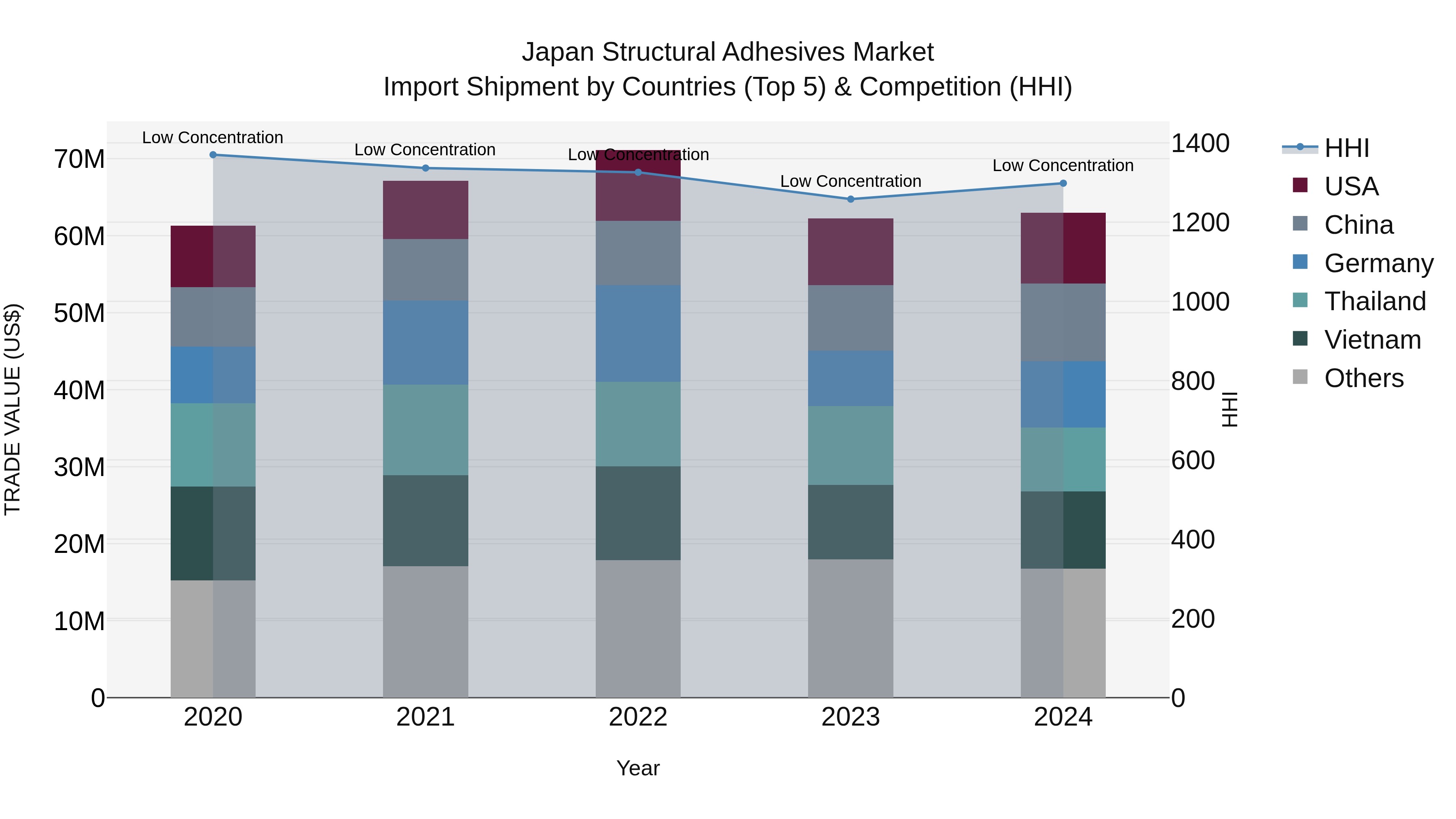

Japan Structural Adhesives Market Import Shipment by Countries (Top 5) & Competition (HHI)

Japan continues to see a steady increase in structural adhesives import shipments, with top exporters including China, Vietnam, USA, Germany, and Thailand. Despite the influx of imports, the market remains fragmented with low concentration indicated by the Herfindahl-Hirschman Index (HHI) in 2024. The compound annual growth rate (CAGR) from 2020 to 2024 stands at 0.68%, showcasing a stable trajectory. Moreover, the growth rate from 2023 to 2024 is a promising 1.17%, indicating a potential uptick in demand for structural adhesives in the Japanese market.

Japan Structural Adhesives Market Growth Rate

According to 6Wresearch internal database and industry insights, the Japan Structural Adhesives Market is growing at a compound annual growth rate (CAGR) of 6.2% during the forecast period (2026-2032).

Topics Covered in the Japan Structural Adhesives Market Report

The Japan Structural Adhesives Market report thoroughly covers the market by product types and end-users. The report provides an unbiased and detailed analysis of ongoing market trends, opportunities/high growth areas, and market drivers, helping stakeholders devise and align their market strategies according to the current and future market dynamics.

Japan Structural Adhesives Market Highlights

| Report Name | Japan Structural Adhesives Market |

| Forecast period | 2026-2032 |

| CAGR | 6.2% |

| Growing Sector | Automotive |

Japan Structural Adhesives Market Synopsis

The Japan Structural Adhesives Market is expected to grow significantly as of increasing demand for lightweight materials and high-performance materials used in the automotive and aerospace and construction sectors. The market expansion is supported by technological progress in adhesive formulations and the development of electric vehicle and wind energy industries. The market trends are being shaped by the growing demand for sustainable eco-friendly adhesives as both consumers and manufacturers want to decrease their environmental impact.

Evaluation of Growth Drivers in the Japan Structural Adhesives Market

Below mentioned are some growth drivers and their impact on market dynamics:

| Drivers | Primary Segments Affected | Why It Matters |

| Growth in Electric Vehicles | End-user (Automotive, Aerospace) | Increased demand for high-performance, lightweight adhesives in vehicle production. |

| Technological Advancements | Product Types (Epoxy, Acrylic, Others) | New advancements in adhesive technology makes more durable bonds and makes performance better. |

| Growing Renewable Energy Adoption | End-user (Wind Energy) | Increasing demand for structural adhesives in wind turbine manufacturing to increase durability and efficiency. |

| Expansion of Building & Construction | End-user (Building & Construction) | Increasing construction activities and demand for durable adhesives for structural bonding. |

| Sustainability Focus | Product Types (Epoxy, Urethanes) | Growing focus on eco-friendly and low-emission adhesives aligns with global sustainability goals. |

The Japan Structural Adhesives Market is projected to grow at a CAGR of 6.2% during the forecast period of 2026-2032. The primary factors that drive the Japan Structural Adhesives Market forward include two main trends which see both the automotive and aerospace industries demanding lightweight materials while adhesive technologies continue to develop new adhesive solutions. The market expansion appears to be fueled by the increasing adoption of structural adhesives within renewable energy applications which include wind energy systems. The market expansion across different sectors results from three main factors which include rising demand for high-performance adhesives, shift toward eco-friendly products and government support for sustainable practices.

Evaluation of Restraints in the Japan Structural Adhesives Market

Below mentioned are some major restraints and their influence on market dynamics:

| Restraints | Primary Segments Affected | What This Means |

| High Cost of Raw Materials | Product Types (All Types) | Increases production costs, limiting market accessibility for price-sensitive sectors. |

| Stringent Environmental Regulations | Product Types (All Types) | It basically makes manufacturers to comply with strict emission and increasing costs. |

| Limited Availability of Skilled Labor | End-user (Automotive, Aerospace) | Less availability of skilled labours impacts the market growth and effects production rates. |

| Competition from Alternative Materials | End-user (Building & Construction) | Competitors from other bonding technologies (e.g., welding) may reduce adhesive demand. |

| Technological Barriers | Product Types (Epoxy, Urethanes) | Technological complexities in developing advanced adhesives could slow down market adoption |

Japan Structural Adhesives Market Challenges

The Japan Structural Adhesives Market faces two main difficulties as high raw material costs create challenges for product pricing which decreases market competitiveness. The production process becomes more difficult and expensive as of strict environmental regulations which control the chemical makeup and emission levels of adhesives. The lack of skilled workers who can handle advanced adhesive applications together with technological obstacles which prevent the development of better adhesive materials create difficulties for manufacturers. The adhesive market experiences growth limitations as of competition from various bonding technologies including welding.

Japan Structural Adhesives Market Trends

Some major trends contributing to the development of the Japan Structural Adhesives Market Growth are:

- Sustainability in Adhesive Products: There is a growing demand among companies for eco-friendly, low-emission, and recyclable adhesives due to stricter government regulations.

- Growth of Electric Vehicle Market: There is a changing shift toward advanced adhesives for bonding lightweight materials and ensuring long-lasting performance.

- Rise in DIY and Consumer Adhesive Products: There is a growing consumers preference for DIY adhesives for various applications, including home improvement and repairs.

Investment Opportunities in the Japan Structural Adhesives Market

Here are some investment opportunities in the Japan Structural Adhesives Industry:

- R&D in Advanced Adhesive Technologies: Putting more funds in research to develop high-performance adhesives for use in the automotive, aerospace, and wind energy industries.

- Electric Vehicle Adhesives: The investors are increasingly investing more in the development of adhesives specifically designed for lightweight automotive and electric vehicle applications.

- Wind Energy Adhesives: Investing in adhesive formulations that meet the performance requirements for wind turbine manufacturing, offering improved durability and strength.

Top 5 Leading Players in the Japan Structural Adhesives Market

Here are some top companies contributing to the Japan Structural Adhesives Market Share:

1. Henkel AG & Co. KGaA

| Company Name | Henkel AG & Co. KGaA |

|---|---|

| Established Year | 1876 |

| Headquarters | Düsseldorf, Germany |

| Official Website | Click Here |

Henkel is a leading player in the Japan structural adhesives market, providing innovative solutions for automotive, aerospace, and industrial applications. Their range of adhesives offers high strength, durability, and environmental compliance.

2. 3M Japan Ltd.

| Company Name | 3M Japan Ltd. |

|---|---|

| Established Year | 1949 |

| Headquarters | Tokyo, Japan |

| Official Website | Click Here |

3M is a global leader in adhesive technologies, offering advanced structural adhesives for automotive, aerospace, and construction applications. The company focuses on high-performance adhesives that meet the needs of the Japanese market.

3. Sika AG

| Company Name | Sika AG |

|---|---|

| Established Year | 1910 |

| Headquarters | Baar, Switzerland |

| Official Website | Click Here |

Sika provides a range of structural adhesives, focusing on high-strength bonding solutions for construction, automotive, and industrial sectors. Their adhesives are recognized for superior bonding strength and durability in Japan.

4. H.B. Fuller

| Company Name | H.B. Fuller |

|---|---|

| Established Year | 1887 |

| Headquarters | St. Paul, USA |

| Official Website | Click Here |

H.B. Fuller offers a broad portfolio of structural adhesives for various industries in Japan, including automotive, wind energy, and building materials. Their adhesives are known for their excellent bonding properties and reliability.

5. BASF SE

| Company Name | BASF SE |

|---|---|

| Established Year | 1865 |

| Headquarters | Ludwigshafen, Germany |

| Official Website | Click Here |

BASF provides structural adhesives solutions that cater to multiple industries in Japan, focusing on sustainable and high-performance adhesives for automotive, aerospace, and construction.

Government Initiatives in the Japan Structural Adhesives Market

According to the Japanese government data, the organization has supported the creation of modern adhesive technologies through its programs dedicated to sustainable development and energy efficient solutions and environmentally friendly methods. The Japan Adhesives Industry Association (JAIA) promotes high-performance adhesive solutions for use in the automotive construction and wind energy industries. The government provides research and development incentives for sustainable material innovations which support adhesive innovation and help structural adhesives gain traction in Japan's expanding industrial market.

Future Insights of the Japan Structural Adhesives Market

The Japan Structural Adhesives Market will experience growth as new adhesive technologies have developed for use in electric vehicle and renewable energy applications. The market will expand as automotive and aerospace and construction industries are increasing their demand for products. The market will develop through three main factors which include sustainable adhesive solutions, better manufacturing processes and government backing for industrial growth. The development of advanced adhesive formulations will create new business opportunities which will focus on producing high-performance and environmentally friendly products.

Market Segmentation Analysis

The report offers a comprehensive study of the subsequent market segments and their leading categories.

Epoxy to Dominate the Market – By Product Type

According to Guneet Kaur, Senior Research Analyst, 6Wresearch, the Epoxy-based structural adhesives is leading the market. Mainly due to their high bonding strength and durability in harsh conditions. They are widely used in the automotive, aerospace, and construction industries for bonding metal, plastic, and composite materials.

Automotive to Dominate the Market – By End-use

The automotive industry dominates the market because vehicle manufacturing requires both lightweight materials and strong bonding technologies. Automotive manufacturers now prefer epoxy and polyurethane adhesives to bond components which include windshields and doors and panels.

Key Attractiveness of the Report

- 10 Years Market Numbers

- Historical Data Starting from 2022 to 2025

- Base Year: 2025

- Forecast Data until 2032

- Key Performance Indicators Impacting the Market

- Major Upcoming Developments and Projects

Key Highlights of the Report:

- Japan Structural Adhesives Market Outlook

- Market Size of Japan Structural Adhesives Market, 2025

- Forecast of Japan Structural Adhesives Market, 2032

- Historical Data and Forecast of Japan Structural Adhesives Revenues & Volume for the Period 2022- 2032

- Japan Structural Adhesives Market Trend Evolution

- Japan Structural Adhesives Market Drivers and Challenges

- Japan Structural Adhesives Price Trends

- Japan Structural Adhesives Porter's Five Forces

- Japan Structural Adhesives Industry Life Cycle

- Historical Data and Forecast of Japan Structural Adhesives Market Revenues & Volume By Product Type for the Period 2022- 2032

- Historical Data and Forecast of Japan Structural Adhesives Market Revenues & Volume By Epoxy for the Period 2022- 2032

- Historical Data and Forecast of Japan Structural Adhesives Market Revenues & Volume By Acrylic for the Period 2022- 2032

- Historical Data and Forecast of Japan Structural Adhesives Market Revenues & Volume By Urethanes for the Period 2022- 2032

- Historical Data and Forecast of Japan Structural Adhesives Market Revenues & Volume By Cyanoacrylate for the Period 2022- 2032

- Historical Data and Forecast of Japan Structural Adhesives Market Revenues & Volume By Others for the Period 2022- 2032

- Historical Data and Forecast of Japan Structural Adhesives Market Revenues & Volume By End- use for the Period 2022- 2032

- Historical Data and Forecast of Japan Structural Adhesives Market Revenues & Volume By Automotive for the Period 2022- 2032

- Historical Data and Forecast of Japan Structural Adhesives Market Revenues & Volume By Aerospace for the Period 2022- 2032

- Historical Data and Forecast of Japan Structural Adhesives Market Revenues & Volume By Marine for the Period 2022- 2032

- Historical Data and Forecast of Japan Structural Adhesives Market Revenues & Volume By Building & Construction for the Period 2022- 2032

- Historical Data and Forecast of Japan Structural Adhesives Market Revenues & Volume By Wind Energy for the Period 2022- 2032

- Historical Data and Forecast of Japan Structural Adhesives Market Revenues & Volume By Others for the Period 2022- 2032

- Japan Structural Adhesives Import Export Trade Statistics

- Market Opportunity Assessment By Product Type

- Market Opportunity Assessment By End- use

- Japan Structural Adhesives Top Companies Market Share

- Japan Structural Adhesives Competitive Benchmarking By Technical and Operational Parameters

- Japan Structural Adhesives Company Profiles

- Japan Structural Adhesives Key Strategic Recommendations

Market Covered

The report subsequently covers the market by following segments and subsegments.

By Product Type

- Epoxy

- Acrylic

- Urethanes

- Cyanoacrylate

- Others

By End-use

- Automotive

- Aerospace

- Marine

- Building & Construction

- Wind Energy

- Others

Japan Structural Adhesives Market (2026-2032): FAQs

High raw material costs and stringent environmental regulations are the main challenges for the market.

key growth drivers of the market includes growing demand for lightweight materials in automotive and aerospace, along with advancements in adhesive technologies.

The government encourages sustainability through initiatives like the Japan Adhesives Industry Association and provides support for eco-friendly adhesive solutions.

The Japan Structural Adhesives Market is projected to grow at a CAGR of 6.2% during the forecast period of 2026-2032.

6Wresearch actively monitors the Japan Structural Adhesives Market and publishes its comprehensive annual report, highlighting emerging trends, growth drivers, revenue analysis, and forecast outlook. Our insights help businesses to make data-backed strategic decisions with ongoing market dynamics. Our analysts track relevent industries related to the Japan Structural Adhesives Market, allowing our clients with actionable intelligence and reliable forecasts tailored to emerging regional needs.

Yes, we provide customisation as per your requirements. To learn more, feel free to contact us on sales@6wresearch.com

| 1 Executive Summary |

| 2 Introduction |

| 2.1 Key Highlights of the Report |

| 2.2 Report Description |

| 2.3 Market Scope & Segmentation |

| 2.4 Research Methodology |

| 2.5 Assumptions |

| 3 Japan Structural Adhesives Market Overview |

| 3.1 Japan Country Macro Economic Indicators |

| 3.2 Japan Structural Adhesives Market Revenues & Volume, 2022 & 2032F |

| 3.3 Japan Structural Adhesives Market - Industry Life Cycle |

| 3.4 Japan Structural Adhesives Market - Porter's Five Forces |

| 3.5 Japan Structural Adhesives Market Revenues & Volume Share, By Product Type, 2022 & 2032F |

| 3.6 Japan Structural Adhesives Market Revenues & Volume Share, By End- use, 2022 & 2032F |

| 4 Japan Structural Adhesives Market Dynamics |

| 4.1 Impact Analysis |

| 4.2 Market Drivers |

| 4.2.1 Growing demand for lightweight and high-performance materials in industries such as automotive, aerospace, and construction. |

| 4.2.2 Increasing focus on sustainability and environmental regulations driving the adoption of structural adhesives over traditional fastening methods. |

| 4.2.3 Technological advancements leading to the development of innovative and high-strength structural adhesives. |

| 4.3 Market Restraints |

| 4.3.1 High initial investment costs associated with switching to structural adhesives from conventional bonding methods. |

| 4.3.2 Concerns regarding the durability and long-term performance of structural adhesives in extreme conditions. |

| 4.3.3 Lack of standardized testing methods and regulations for structural adhesives leading to quality control issues. |

| 5 Japan Structural Adhesives Market Trends |

| 6 Japan Structural Adhesives Market, By Types |

| 6.1 Japan Structural Adhesives Market, By Product Type |

| 6.1.1 Overview and Analysis |

| 6.1.2 Japan Structural Adhesives Market Revenues & Volume, By Product Type, 2022- 2032F |

| 6.1.3 Japan Structural Adhesives Market Revenues & Volume, By Epoxy, 2022- 2032F |

| 6.1.4 Japan Structural Adhesives Market Revenues & Volume, By Acrylic, 2022- 2032F |

| 6.1.5 Japan Structural Adhesives Market Revenues & Volume, By Urethanes, 2022- 2032F |

| 6.1.6 Japan Structural Adhesives Market Revenues & Volume, By Cyanoacrylate, 2022- 2032F |

| 6.1.7 Japan Structural Adhesives Market Revenues & Volume, By Others, 2022- 2032F |

| 6.2 Japan Structural Adhesives Market, By End- use |

| 6.2.1 Overview and Analysis |

| 6.2.2 Japan Structural Adhesives Market Revenues & Volume, By Automotive, 2022- 2032F |

| 6.2.3 Japan Structural Adhesives Market Revenues & Volume, By Aerospace, 2022- 2032F |

| 6.2.4 Japan Structural Adhesives Market Revenues & Volume, By Marine, 2022- 2032F |

| 6.2.5 Japan Structural Adhesives Market Revenues & Volume, By Building & Construction, 2022- 2032F |

| 6.2.6 Japan Structural Adhesives Market Revenues & Volume, By Wind Energy, 2022- 2032F |

| 6.2.7 Japan Structural Adhesives Market Revenues & Volume, By Others, 2022- 2032F |

| 7 Japan Structural Adhesives Market Import-Export Trade Statistics |

| 7.1 Japan Structural Adhesives Market Export to Major Countries |

| 7.2 Japan Structural Adhesives Market Imports from Major Countries |

| 8 Japan Structural Adhesives Market Key Performance Indicators |

| 8.1 Research and development investment in new adhesive technologies. |

| 8.2 Adoption rate of structural adhesives in key industries. |

| 8.3 Number of patents filed for new structural adhesive formulations. |

| 8.4 Growth in demand for lightweight materials in industries using structural adhesives. |

| 8.5 Environmental impact assessment of structural adhesive products. |

| 9 Japan Structural Adhesives Market - Opportunity Assessment |

| 9.1 Japan Structural Adhesives Market Opportunity Assessment, By Product Type, 2022 & 2032F |

| 9.2 Japan Structural Adhesives Market Opportunity Assessment, By End- use, 2022 & 2032F |

| 10 Japan Structural Adhesives Market - Competitive Landscape |

| 10.1 Japan Structural Adhesives Market Revenue Share, By Companies, 2025 |

| 10.2 Japan Structural Adhesives Market Competitive Benchmarking, By Operating and Technical Parameters |

| 11 Company Profiles |

| 12 Recommendations |

| 13 Disclaimer |

Export potential assessment - trade Analytics for 2030

Export potential enables firms to identify high-growth global markets with greater confidence by combining advanced trade intelligence with a structured quantitative methodology. The framework analyzes emerging demand trends and country-level import patterns while integrating macroeconomic and trade datasets such as GDP and population forecasts, bilateral import–export flows, tariff structures, elasticity differentials between developed and developing economies, geographic distance, and import demand projections. Using weighted trade values from 2020–2024 as the base period to project country-to-country export potential for 2030, these inputs are operationalized through calculated drivers such as gravity model parameters, tariff impact factors, and projected GDP per-capita growth. Through an analysis of hidden potentials, demand hotspots, and market conditions that are most favorable to success, this method enables firms to focus on target countries, maximize returns, and global expansion with data, backed by accuracy.

By factoring in the projected importer demand gap that is currently unmet and could be potential opportunity, it identifies the potential for the Exporter (Country) among 190 countries, against the general trade analysis, which identifies the biggest importer or exporter.

To discover high-growth global markets and optimize your business strategy:

Click Here

Pricing

- Single User License$ 1,995

- Department License$ 2,400

- Site License$ 3,120

- Global License$ 3,795

Search

Thought Leadership and Analyst Meet

Our Clients

Latest Reports

- Taiwan Food Delivery Platform Market (2026-2032) | Companies, Outlook, Analysis, Trends, Value, Revenue, Segmentation, Share, Forecast, Competitive Landscape, Growth, Size & Forecast

- United Kingdom (UK) Long-term Care Insurance Market (2026-2032) | Growth, Share, Consumer Insights, Drivers, Opportunities, Competition, Pricing Analysis, Segments, Restraints, Companies, Competitive, Value, Outlook, Size, Demand, Analysis, Challenges, Strategic Insights, Investment Trends, Revenue, Trends, Supply, Forecast

- United Kingdom (UK) Long Term Care Market (2026-2032) | Companies, Outlook, Analysis, Trends, Value, Revenue, Segmentation, Share, Forecast, Competitive Landscape, Growth, Size & Forecast

- Iraq Insulation and Waterproofing Market (2026-2032) | Outlook, Drivers, Growth, Size, Share, Industry, Revenue, Trends, Demand, Competitive, Strategic Insights, Opportunities, Segments, Companies, Challenges, Strategy, Consumer Insights, Analysis, Investment Trends, Value, Segmentation, Forecast, Restraints

- India Switchgear Market Outlook (2026-2032) | Size, Share, Trends, Growth, Revenue, Forecast, Analysis, Value, Outlook

- Pakistan Contraceptive Implants Market (2025-2031) | Demand, Growth, Size, Share, Industry, Pricing Analysis, Competitive, Strategic Insights, Strategy, Consumer Insights, Analysis, Investment Trends, Opportunities, Revenue, Segments, Value, Segmentation, Supply, Forecast, Restraints, Outlook, Competition, Drivers, Trends, Companies, Challenges

- Sri Lanka Packaging Market (2026-2032) | Outlook, Competition, Drivers, Trends, Demand, Pricing Analysis, Competitive, Strategic Insights, Companies, Challenges, Strategy, Consumer Insights, Analysis, Investment Trends, Opportunities, Growth, Size, Share, Industry, Revenue, Segments, Value, Segmentation, Supply, Forecast, Restraints

- India Kids Watches Market (2026-2032) | Strategy, Consumer Insights, Analysis, Investment Trends, Opportunities, Growth, Size, Share, Industry, Revenue, Segments, Value, Segmentation, Supply, Forecast, Restraints, Outlook, Competition, Drivers, Trends, Demand, Pricing Analysis, Competitive, Strategic Insights, Companies, Challenges

- Saudi Arabia Core Assurance Service Market (2025-2031) | Strategy, Consumer Insights, Analysis, Investment Trends, Opportunities, Growth, Size, Share, Industry, Revenue, Segments, Value, Segmentation, Supply, Forecast, Restraints, Outlook, Competition, Drivers, Trends, Demand, Pricing Analysis, Competitive, Strategic Insights, Companies, Challenges

- Romania Uninterruptible Power Supply (UPS) Market (2026-2032) | Industry, Analysis, Revenue, Size, Forecast, Outlook, Value, Trends, Share, Growth & Companies

Industry Events and Analyst Meet

India EV Show 2026

EV tech India Expo 2026

Auto Tech Asia 2026

Battery Tech India 2026

Smart Production Solutions Guangzhou 2026

Whitepaper

- Middle East & Africa Commercial Security Market Click here to view more.

- Middle East & Africa Fire Safety Systems & Equipment Market Click here to view more.

- GCC Drone Market Click here to view more.

- Middle East Lighting Fixture Market Click here to view more.

- GCC Physical & Perimeter Security Market Click here to view more.

6WResearch In News

- Doha a strategic location for EV manufacturing hub: IPA Qatar

- Demand for luxury TVs surging in the GCC, says Samsung

- Empowering Growth: The Thriving Journey of Bangladesh’s Cable Industry

- Demand for luxury TVs surging in the GCC, says Samsung

- Video call with a traditional healer? Once unthinkable, it’s now common in South Africa

- Intelligent Buildings To Smooth GCC’s Path To Net Zero