Philippines Vitamins And Supplement Market (2025-2031) | Outlook, Value, Growth, Analysis, Revenue, Industry, Trends, Forecast, Companies, Share & Size

Market Forecast By Type (Multivitamins, Calcium Supplements, Pediatric Supplements, Others), By Form (Capsule, Tablet, Powder, Liquid/Gel), By Distribution Channel (Supermarkets/Hypermarkets, Convenience Stores, Specialty Stores, Online Retails) And Competitive Landscape

| Product Code: ETC352109 | Publication Date: Aug 2022 | Updated Date: Nov 2025 | Product Type: Report | |

| Publisher: 6Wresearch | Author: Ravi Bhandari | No. of Pages: 70 | No. of Figures: 35 | No. of Tables: 5 |

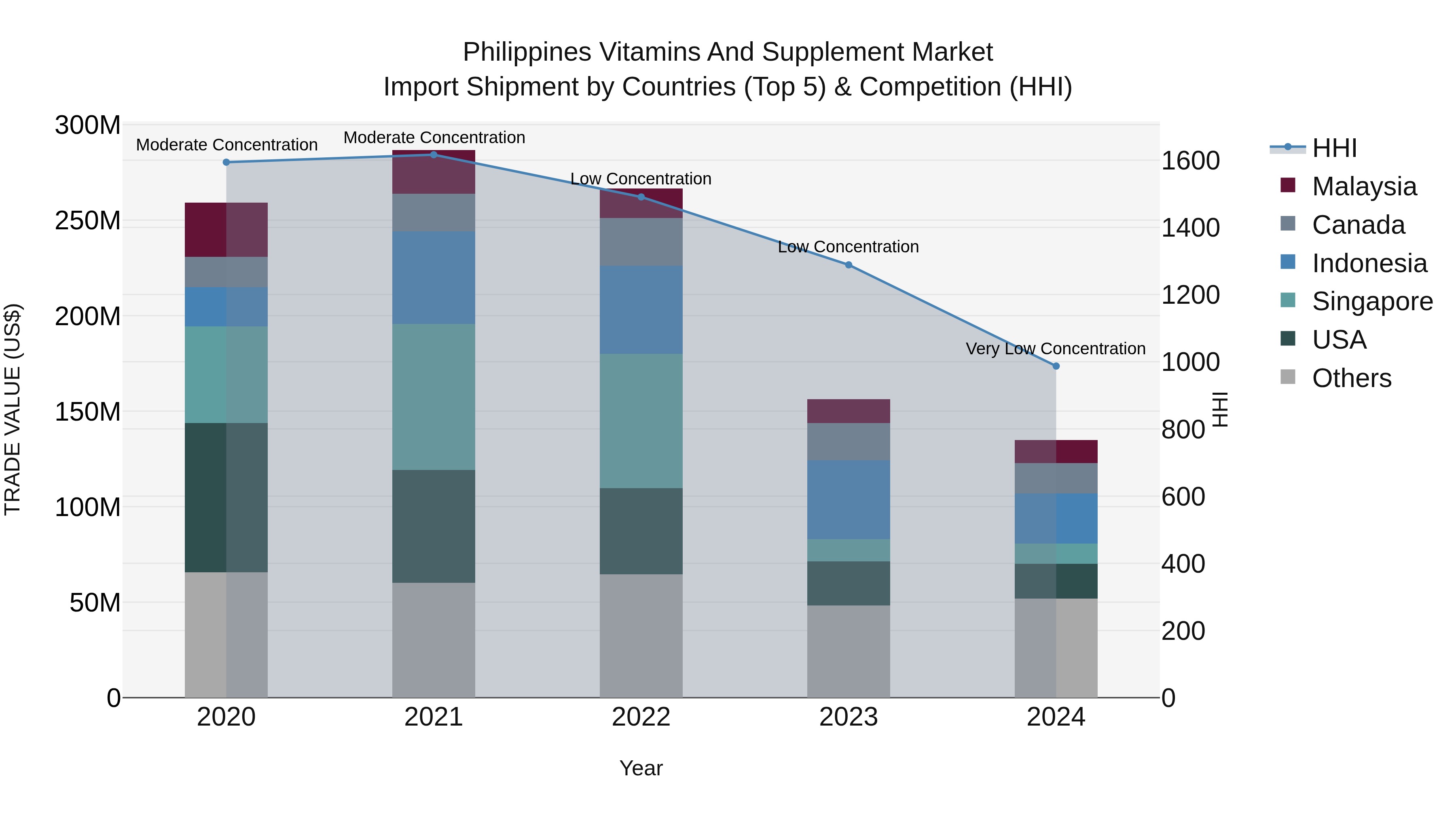

Philippines Vitamins And Supplement Market Top 5 Importing Countries and Market Competition (HHI) Analysis

The Philippines saw a decrease in vitamin and supplement import shipments in 2024, with top exporting countries being Indonesia, USA, Canada, Malaysia, and India. The market experienced very low concentration levels, indicating a diverse range of sources for these products. The compound annual growth rate (CAGR) from 2020 to 2024 was -15.07%, with a slight improvement in the growth rate from 2023 to 2024 at -13.69%. These figures suggest a challenging market environment, potentially driven by shifting consumer preferences and economic factors.

Philippines Vitamins and Supplement Market Size & Growth Rate

As Per 6Wresearch, the Philippines Vitamins and Supplement Market is anticipated to grow, with a CAGR of approximately 9.2% from 2025 to 2031. This growth is propelled by increasing health awareness among the population.

Philippines Vitamins and Supplement Market Highlights

| Report Name | Philippines Vitamins and Supplement Market |

| Forecast period | 2025-2031 |

| CAGR | 9.2% |

| Growing Sector | Healthcare and Wellness |

Topics Covered in the Philippines Vitamins and Supplement Market Report

Philippines Vitamins and Supplement Market report thoroughly covers the market By Type, By Form, and By Distribution Channel. The market report provides an unbiased and detailed analysis of the ongoing market trends, opportunities/high growth areas, and market drivers which would help the stakeholders to devise and align their market strategies according to the current and future market dynamics.

Philippines Vitamins and Supplement Market Synopsis

Philippines Vitamins and Supplements Industry has been witnessing steady growth, driven by an increasing health-conscious population and the rising awareness around the importance of maintaining overall wellness. This growth is also complemented by an increase in demand for natural and organic products, as consumers are gravitating towards healthier alternatives. Moreover, increased healthcare infrastructure and product availability through various retail and digital channels offer convenience and accessibility, driving consumer spending. The increasing middle-class population, along with increased disposable incomes, also allows people to invest more resources in nutraceuticals and health-improving products. These elements all contribute towards the strong growth of the market, promising continued growth in the next few years.

Philippines Vitamins and Supplement Market size is expected to grow at a CAGR of 9.2% during 2025-2031. Increased health awareness among Filipinos is also necessary, with more and more individuals giving priority to preventive care and wellness-oriented living. The online sites' infestation has also made it easy for consumers to access these types of products more easily, whereby consumers can simply find and purchase a variety. In addition, endorsement by health practitioners further feed into confidence and forces consumers to incorporate supplements as part of one's lifestyle.

However, the market also faces significant challenges. Price sensitivity, particularly among low-income groups, can limit widespread adoption. Furthermore, the availability of counterfeit goods and regulatory loopholes threaten consumer safety and trust. These are reasons for tougher industry regulations as well as public awareness campaigns to guarantee market reliability and sustain growth.

Philippines Vitamins and Supplement Market Trends

The Philippines vitamins and supplement market is witnessing several impactful trends shaping its trajectory. One of the trends is the rising consumer preference for natural and organic products. As there is greater awareness of the possible side effects linked to synthetic ingredients, consumers in the Philippines are increasingly opting for supplements from natural sources. This has led manufacturers to develop new products and diversify their portfolios to cover organic and plant-based supplements. One of the more significant trends is the growth in e-commerce as a channel of distribution. The ease of shopping online, combined with competitive prices and easy availability of an array of products, has greatly contributed to the upsurge in supplements on digital platforms.

Supplements are also being promoted by many brands through online promotional campaigns to connect with an internet-savvy population, which is further driving sales on the internet. There is also an increasing focus on preventive care, and consumers are actively on the lookout for supplements that aid immunity, digestibility, and general well-being. Supplements such as C, D, and Zinc-based have become more popular for this purpose. Personalization is finally becoming a key area of interest in the market. Firms are looking to provide customized solutions for health based on individual requirements, lifestyle, and health status. These range from innovations like subscription models and targeted supplements, catering to the specific needs of various demographic segments. These evolving trends indicate a dynamic and competitive market landscape with significant growth potential.

Investment Opportunities in the Philippines Vitamins and Supplement Market

The Philippines presents a rewarding opportunity for both local and international investors in the vitamins and supplement sector. As more consumers develop greater health consciousness, demand for nutritional supplements has continued to increase steadily over the last few years. Contributing factors include the increasing middle class, higher disposable incomes, and popularity of preventive health care propelling the industry to growth. Furthermore, investments in the health and wellness sector have been boosted by the government with a friendly regulatory framework.

Investors can look to opportunities in different segments, such as herbal and organic supplements, which are becoming popular due to a shift towards natural products. Online platforms also hold great potential, as e-commerce continues to grow throughout the nation. Collaboration with local distributors or using digital marketing techniques can assist new players in gaining a strong presence in this competitive market. With its promising growth prospects and evolving consumer demands, the Philippines stands out as a strategic destination for investment in the vitamins and supplement industry.

Leading Players in the Philippines Vitamins and Supplement Industry

The vitamins and supplement market in the Philippines features several prominent players that have established strong brand recognition and market presence. Among these are multinationals like Pfizer, Bayer, and Abbott that bank on their wide product offerings and research-driven formulations. Similarly, homegrown brands like Unilab also enjoy a considerable chunk, owing to their emphasis on price points and meeting the unique needs of Filipino consumers. Furthermore, newer players in the form of organic and plant-based supplements are making inroads as consumer demand turns towards natural and sustainable alternatives. These industry players successfully utilize both conventional retailing and online business channels to enhance their reach and stay competitive in this emerging sector.

Government Regulations

The vitamins and supplements market in the Philippines operates under strict government regulations to ensure consumer safety and product efficacy. The Food and Drug Administration (FDA) Philippines acts as the central agency in charge of the registration, approval, and regulation of dietary supplements under the Food-Drug-Cosmetic Act and related regulations. Manufacturers must obtain a Certificate of Product Registration (CPR) from the FDA prior to product sale, including assessing product claims, ingredients, and manufacturing. For instance, therapeutic products must back their claims with scientific evidence. These products may face penalties or even be withdrawn from the market if they fail to live up to these standards.

In addition, the FDA requires appropriate labelling procedures, which demand that supplements be clearly labelled with nutritional content, suggested dosages, and possible side effects. Brands like USANA and local players like Bewell-C adhere to these guidelines to build consumer trust. Regular inspections and random sampling further ensure compliance, helping maintain quality and safety in this growing industry.

Future Insights of the Philippines Vitamins and Supplement Market

In the future years, Philippines Vitamins and Supplement Market Growth is expected to proliferate due to increasing health consciousness as consumers are increasingly taking charge of their health, with an increasing emphasis on products that promote immunity, general wellness, and particular health issues such as weight control or stress management. This change in consumer behaviour will drive demand for a broad array of supplements, including multivitamins, botanicals, and specialty products. Innovation will be the key driver of the market's future.

Brands that invest in R&D to develop premium, science-based products will enjoy a competitive advantage. Personalization is also one of the rising trends, with businesses using technology to provide bespoke solutions tailored to individual preferences and needs. Technology is also being integrated into digital marketing and online sales, where channels like Lazada and Shopee are making brands more accessible to the masses. With sustained government patronage and stricter regulation, the sector is geared towards upholding high standards of practice while expanding accessibility to healthy and effective products. The Filipino vitamins and supplements industry is ready to flourish, reflecting consumer need for health-centric innovation and ease.

Market Segmentation Analysis

The report offers a comprehensive study of the subsequent market segments and their leading categories.

Multivitamins to Dominate the Market- By Type

According to Vasu, Senior Research Analyst, 6Wresearch, Among the various types of supplements, multivitamins are expected to dominate the Philippines Vitamins and Supplement Market Share due to their broad appeal and the convenience of addressing multiple nutritional needs in a single product. Consumers increasingly prefer multivitamins to fill dietary gaps and boost overall wellness, making this segment the most sought-after. Calcium supplements and paediatric supplements also hold significant shares, catering to specific demographics like older adults and children, but multivitamins remain the primary choice for a majority of consumers.

Tablets to Dominate the Market- By Form

When it comes to form, tablets lead the market as they are easy to produce, store, and transport while offering precise dosages to users. Capsules are also popular for their ease of swallowing and ability to mask unpleasant tastes. However, liquid and gel supplements are growing steadily due to their suitability for children and individuals who struggle with swallowing pills. While powders are less dominant, they still hold a niche market, especially among athletes and health enthusiasts.

Online retail channels to Dominate the Market- By Distribution Channel

Online retail channels have seen tremendous growth, driven by the convenience of home delivery, competitive pricing, and the ability to compare products online. Platforms like Lazada and Shopee have become key players in this segment. Meanwhile, supermarkets and hypermarkets remain strong contenders for traditional shoppers who value buying products in person. Specialty stores and convenience stores also cater to specific customer needs but account for a smaller market share compared to online platforms and larger retailers.

Key Attractiveness of the Report

- 10 Years of Market Numbers.

- Historical Data Starting from 2021 to 2024

- Base Year 2024

- Forecast Data until 2031

- Key Performance Indicators Impacting the Market

- Major Upcoming Developments and Projects

Key Highlights of the Report:

- Philippines Vitamins and Supplement Market Outlook

- Market Size of Philippines Vitamins and Supplement Market, 2024

- Forecast of Philippines Vitamins and Supplement Market, 2031

- Historical Data and Forecast of Philippines Vitamins and Supplement Revenues & Volume for the Period 2021-2031

- Philippines Vitamins and Supplement Market Trend Evolution

- Philippines Vitamins and Supplement Market Drivers and Challenges

- Philippines Vitamins and Supplement Price Trends

- Philippines Vitamins and Supplement Porter's Five Forces

- Philippines Vitamins and Supplement Industry Life Cycle

- Historical Data and Forecast of Philippines Vitamins and Supplement Market Revenues & Volume By Type for the Period 2021-2031

- Historical Data and Forecast of Philippines Vitamins and Supplement Market Revenues & Volume By Multivitamins for the Period 2021-2031

- Historical Data and Forecast of Philippines Vitamins and Supplement Market Revenues & Volume By Calcium Supplements for the Period 2021-2031

- Historical Data and Forecast of Philippines Vitamins and Supplement Market Revenues & Volume By Pediatric Supplements for the Period 2021-2031

- Historical Data and Forecast of Philippines Vitamins and Supplement Market Revenues & Volume By Others for the Period 2021-2031

- Historical Data and Forecast of Philippines Vitamins and Supplement Market Revenues & Volume By Form for the Period 2021-2031

- Historical Data and Forecast of Philippines Vitamins and Supplement Market Revenues & Volume By Capsule for the Period 2021-2031

- Historical Data and Forecast of Philippines Vitamins and Supplement Market Revenues & Volume By Tablet for the Period 2021-2031

- Historical Data and Forecast of Philippines Vitamins and Supplement Market Revenues & Volume By Powder for the Period 2021-2031

- Historical Data and Forecast of Philippines Vitamins and Supplement Market Revenues & Volume By Liquid/Gel for the Period 2021-2031

- Historical Data and Forecast of Philippines Vitamins and Supplement Market Revenues & Volume By Distribution Channel for the Period 2021-2031

- Historical Data and Forecast of Philippines Vitamins and Supplement Market Revenues & Volume By Supermarkets/Hypermarkets for the Period 2021-2031

- Historical Data and Forecast of Philippines Vitamins and Supplement Market Revenues & Volume By Convenience Stores for the Period 2021-2031

- Historical Data and Forecast of Philippines Vitamins and Supplement Market Revenues & Volume By Specialty Stores for the Period 2021-2031

- Historical Data and Forecast of Philippines Vitamins and Supplement Market Revenues & Volume By Online Retails for the Period 2021-2031

- Philippines Vitamins and Supplement Import Export Trade Statistics

- Market Opportunity Assessment By Type

- Market Opportunity Assessment By Form

- Market Opportunity Assessment By Distribution Channel

- Philippines Vitamins and Supplement Top Companies Market Share

- Philippines Vitamins and Supplement Competitive Benchmarking By Technical and Operational Parameters

- Philippines Vitamins and Supplement Company Profiles

- Philippines Vitamins and Supplement Key Strategic Recommendations

Markets Covered

The report provides a detailed analysis of the following market segments

By Type

- Multivitamins

- Calcium Supplements

- Paediatric Supplements

- Others

By Form

- Capsule

- Tablet

- Powder

- Liquid/Gel

By Distribution Channel

- Supermarkets/Hypermarkets

- Convenience Stores

- Specialty Stores

- Online Retails

Philippines Vitamins And Supplement Market (2025-2031): FAQs

The Philippines Vitamins and Supplement Market is projected to grow at a CAGR of 9.2% from 2025 to 2031.

Multivitamins dominate the Philippines Vitamins and Supplement Market due to their broad appeal and convenience.

Online retail channels, especially platforms like Lazada and Shopee, are the leading distribution channels in the market.

Challenges in the Philippines Vitamins and Supplement Market include price sensitivity, counterfeit products, and regulatory gaps.

6Wresearch actively monitors the Philippines Vitamins And Supplement Market and publishes its comprehensive annual report, highlighting emerging trends, growth drivers, revenue analysis, and forecast outlook. Our insights help businesses to make data-backed strategic decisions with ongoing market dynamics. Our analysts track relevent industries related to the Philippines Vitamins And Supplement Market, allowing our clients with actionable intelligence and reliable forecasts tailored to emerging regional needs.

Yes, we provide customisation as per your requirements. To learn more, feel free to contact us on sales@6wresearch.com

| 1 Executive Summary |

| 2 Introduction |

| 2.1 Key Highlights of the Report |

| 2.2 Report Description |

| 2.3 Market Scope & Segmentation |

| 2.4 Research Methodology |

| 2.5 Assumptions |

| 3 Philippines Vitamins And Supplement Market Overview |

| 3.1 Philippines Country Macro Economic Indicators |

| 3.2 Philippines Vitamins And Supplement Market Revenues & Volume, 2021 & 2031F |

| 3.3 Philippines Vitamins And Supplement Market - Industry Life Cycle |

| 3.4 Philippines Vitamins And Supplement Market - Porter's Five Forces |

| 3.5 Philippines Vitamins And Supplement Market Revenues & Volume Share, By Type, 2021 & 2031F |

| 3.6 Philippines Vitamins And Supplement Market Revenues & Volume Share, By Form, 2021 & 2031F |

| 3.7 Philippines Vitamins And Supplement Market Revenues & Volume Share, By Distribution Channel, 2021 & 2031F |

| 4 Philippines Vitamins And Supplement Market Dynamics |

| 4.1 Impact Analysis |

| 4.2 Market Drivers |

| 4.2.1 Increasing health awareness among the population |

| 4.2.2 Growing aging population in the Philippines |

| 4.2.3 Rise in disposable income leading to higher spending on healthcare products |

| 4.3 Market Restraints |

| 4.3.1 Lack of stringent regulations in the vitamins and supplements market |

| 4.3.2 Presence of counterfeit products affecting consumer trust |

| 5 Philippines Vitamins And Supplement Market Trends |

| 6 Philippines Vitamins And Supplement Market, By Types |

| 6.1 Philippines Vitamins And Supplement Market, By Type |

| 6.1.1 Overview and Analysis |

| 6.1.2 Philippines Vitamins And Supplement Market Revenues & Volume, By Type, 2021-2031F |

| 6.1.3 Philippines Vitamins And Supplement Market Revenues & Volume, By Multivitamins, 2021-2031F |

| 6.1.4 Philippines Vitamins And Supplement Market Revenues & Volume, By Calcium Supplements, 2021-2031F |

| 6.1.5 Philippines Vitamins And Supplement Market Revenues & Volume, By Pediatric Supplements, 2021-2031F |

| 6.1.6 Philippines Vitamins And Supplement Market Revenues & Volume, By Others, 2021-2031F |

| 6.2 Philippines Vitamins And Supplement Market, By Form |

| 6.2.1 Overview and Analysis |

| 6.2.2 Philippines Vitamins And Supplement Market Revenues & Volume, By Capsule, 2021-2031F |

| 6.2.3 Philippines Vitamins And Supplement Market Revenues & Volume, By Tablet, 2021-2031F |

| 6.2.4 Philippines Vitamins And Supplement Market Revenues & Volume, By Powder, 2021-2031F |

| 6.2.5 Philippines Vitamins And Supplement Market Revenues & Volume, By Liquid/Gel, 2021-2031F |

| 6.3 Philippines Vitamins And Supplement Market, By Distribution Channel |

| 6.3.1 Overview and Analysis |

| 6.3.2 Philippines Vitamins And Supplement Market Revenues & Volume, By Supermarkets/Hypermarkets, 2021-2031F |

| 6.3.3 Philippines Vitamins And Supplement Market Revenues & Volume, By Convenience Stores, 2021-2031F |

| 6.3.4 Philippines Vitamins And Supplement Market Revenues & Volume, By Specialty Stores, 2021-2031F |

| 6.3.5 Philippines Vitamins And Supplement Market Revenues & Volume, By Online Retails, 2021-2031F |

| 7 Philippines Vitamins And Supplement Market Import-Export Trade Statistics |

| 7.1 Philippines Vitamins And Supplement Market Export to Major Countries |

| 7.2 Philippines Vitamins And Supplement Market Imports from Major Countries |

| 8 Philippines Vitamins And Supplement Market Key Performance Indicators |

| 8.1 Consumer demand for natural and organic supplements |

| 8.2 Adoption rate of online sales channels for purchasing vitamins and supplements |

| 8.3 Number of new product launches in the market segment |

| 9 Philippines Vitamins And Supplement Market - Opportunity Assessment |

| 9.1 Philippines Vitamins And Supplement Market Opportunity Assessment, By Type, 2021 & 2031F |

| 9.2 Philippines Vitamins And Supplement Market Opportunity Assessment, By Form, 2021 & 2031F |

| 9.3 Philippines Vitamins And Supplement Market Opportunity Assessment, By Distribution Channel, 2021 & 2031F |

| 10 Philippines Vitamins And Supplement Market - Competitive Landscape |

| 10.1 Philippines Vitamins And Supplement Market Revenue Share, By Companies, 2024 |

| 10.2 Philippines Vitamins And Supplement Market Competitive Benchmarking, By Operating and Technical Parameters |

| 11 Company Profiles |

| 12 Recommendations |

| 13 Disclaimer |

Global Go To Market Strategy - 2030

Export potential enables firms to identify high-growth global markets with greater confidence by combining advanced trade intelligence with a structured quantitative methodology. The framework analyzes emerging demand trends and country-level import patterns while integrating macroeconomic and trade datasets such as GDP and population forecasts, bilateral import–export flows, tariff structures, elasticity differentials between developed and developing economies, geographic distance, and import demand projections. Using weighted trade values from 2020–2024 as the base period to project country-to-country export potential for 2030, these inputs are operationalized through calculated drivers such as gravity model parameters, tariff impact factors, and projected GDP per-capita growth. Through an analysis of hidden potentials, demand hotspots, and market conditions that are most favorable to success, this method enables firms to focus on target countries, maximize returns, and global expansion with data, backed by accuracy.

By factoring in the projected importer demand gap that is currently unmet and could be potential opportunity, it identifies the potential for the Exporter (Country) among 190 countries, against the general trade analysis, which identifies the biggest importer or exporter.

To discover high-growth global markets and optimize your business strategy:

Click Here

Pricing

- Single User License$ 1,995

- Department License$ 2,400

- Site License$ 3,120

- Global License$ 3,795

Leadership Perspectives from Industry Events

Search

Thought Leadership and Analyst Meet

Our Clients

6WResearch In News

- India Air Conditioner Market Set for Strong Rebound in 2026 After Weather-Led Correction and GST-Driven Recovery: 6Wresearch

- ADAS in India: How Automatic Emergency Braking, Blind Spot Detection & Driver Monitoring are Transforming Road Safety

- Doha a strategic location for EV manufacturing hub: IPA Qatar

- Demand for luxury TVs surging in the GCC, says Samsung

- Empowering Growth: The Thriving Journey of Bangladesh’s Cable Industry

- Demand for luxury TVs surging in the GCC, says Samsung

Latest Reports

- Poland Fire Protection Systems Market (2026-2032)

- Cape Verde Portable Hand-Thrown Extinguisher Market (2026-2032)

- Canada Portable Hand-Thrown Extinguisher Market (2026-2032)

- Cameroon Portable Hand-Thrown Extinguisher Market (2026-2032)

- Burundi Portable Hand-Thrown Extinguisher Market (2026-2032)

- Burkina Faso Portable Hand-Thrown Extinguisher Market (2026-2032)

- Bulgaria Portable Hand-Thrown Extinguisher Market (2026-2032)

- Brunei Portable Hand-Thrown Extinguisher Market (2026-2032)

- Botswana Portable Hand-Thrown Extinguisher Market (2026-2032)

- Bosnia and Herzegovina Portable Hand-Thrown Extinguisher Market (2026-2032)

Industry Events and Analyst Meet

HIMTEX 2026

India Refining Summit 2026

India EV Show 2026

EV tech India Expo 2026

Auto Tech Asia 2026

Whitepaper

- Middle East & Africa Commercial Security Market Click here to view more.

- Middle East & Africa Fire Safety Systems & Equipment Market Click here to view more.

- GCC Drone Market Click here to view more.

- Middle East Lighting Fixture Market Click here to view more.

- GCC Physical & Perimeter Security Market Click here to view more.