Saudi Arabia Oil and Gas Market (2026-2032) | Outlook, Industry, Growth, Segmentation, Value, Companies, Analysis, Size & Revenue, Trends, Share, Forecast, Competitive Landscape

Market Forecast By Type (Upstream, Midstream, Downstream) And Competitive Landscape

| Product Code: ETC9171621 | Publication Date: Sep 2024 | Updated Date: Mar 2026 | Product Type: Market Research Report | |

| Publisher: 6Wresearch | Author: Shubham Deep | No. of Pages: 75 | No. of Figures: 35 | No. of Tables: 20 |

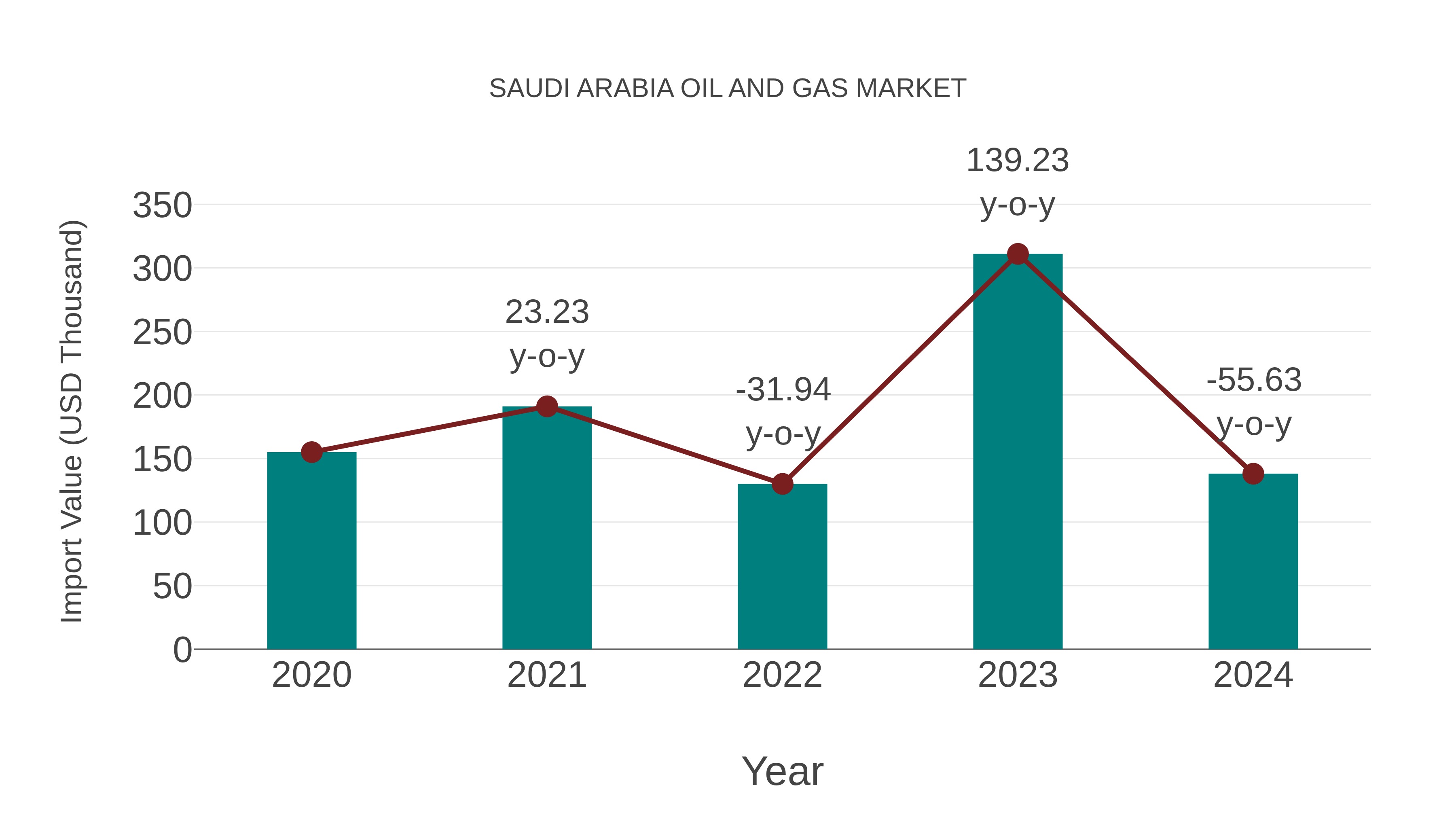

Saudi Arabia Oil and Gas Market: Import Trend Analysis

Saudi Arabia`s import trend in the oil and gas market showed a decline from 2023 to 2024, with a growth rate of -55.63%. The compound annual growth rate (CAGR) for the period 2020-2024 stood at -2.86%. This negative import momentum may be attributed to shifts in global demand patterns or changes in trade policies impacting market stability.

Saudi Arabia Oil and Gas Market Growth Rate

According to 6Wresearch internal database and industry insights, the Saudi Arabia Oil and Gas Market is projected to grow at a compound annual growth rate (CAGR) of 4.6% during the forecast period (2026-2032).

Five-Year Growth Trajectory of the Saudi Arabia Oil and Gas Market with Core Drivers

Below mentioned are the evaluation of years-wise growth rate along with key growth drivers:

| Year | Est. Annual Growth (%) | Growth Drivers |

| 2021 | 2.1 | Stabilisation of crude oil production and export optimisation |

| 2022 | 2.8 | Incremental upstream investments and enhanced drilling activity |

| 2023 | 3.5 | Expansion of gas processing capacity and petrochemical integration |

| 2024 | 4 | Downstream refinery modernisation and export diversification |

| 2025 | 4.3 | Increased focus on natural gas, LNG, and value-added refining |

Topics Covered in the Saudi Arabia Oil and Gas Market Report

The Saudi Arabia Oil and Gas Market report thoroughly covers the market by type. The market report provides an unbiased and detailed analysis of ongoing market trends, opportunities/high growth areas, and market drivers, which help stakeholders devise and align their market strategies according to the current and future market dynamics.

Saudi Arabia Oil and Gas Market Highlights

| Report Name | Saudi Arabia Oil and Gas Market |

| Forecast period | 2026-2032 |

| CAGR | 4.6% |

| Growing Sector | Downstream |

Saudi Arabia Oil and Gas Market Synopsis

The Saudi Arabia Oil and Gas Market is anticipated to record steady expansion supported by long-term production optimisation strategies, strong state-backed investments, and continuous integration across upstream, midstream, and downstream activities. The market benefits from abundant hydrocarbon reserves, advanced extraction technologies, and large-scale refining and petrochemical capacity expansions. Furthermore, policy-led diversification of the energy sector to the natural gas industry, the use of cleaner fuels, and export-oriented downstream projects is increasing the creation of value, also facilitating energy security and the sector's endurance in the long run.

Evaluation of Growth Drivers in the Saudi Arabia Oil and Gas Market

Below mentioned are some prominent drivers and their influence to the market dynamics:

| Drivers | Primary Segments Affected | Why it Matters (Evidence) |

| Upstream Capacity Optimization | Upstream | Enhanced recovery techniques improve output from mature fields and extend reservoir life. |

| Gas Field Development | Upstream, Midstream | Non-associated gas projects support power generation and rising industrial energy demand. |

| Refinery Expansion Projects | Downstream | New and upgraded refining units increase export-ready fuel production capacity. |

| Petrochemical Integration | Downstream | Value-added processing improves profit margins and strengthens global competitiveness. |

| Government Energy Diversification Policy | All Types | Long-term national strategies support sustainable oil and gas monetization and sector stability. |

The Saudi Arabia Oil and Gas Market is expected to grow at the CAGR of 4.6% during the forecast period of 2026-2032. Growth is driven by disciplined crude production management, accelerating natural gas investments, and continuous downstream capacity upgrades. Additional momentum comes from large-scale state-led projects, rising petrochemical demand, and export diversification initiatives that collectively enhance value realisation across the oil and gas supply chain.

Evaluation of Restraints in the Saudi Arabia Oil and Gas Market

Below mentioned are some major restraints and their influence to the market dynamics:

| Restraints | Primary Segments Affected | What This Means (Evidence) |

| Oil Price Volatility | Upstream | Revenue fluctuations influence investment planning cycles and impact long-term upstream project commitments. |

| High Capital Intensity | Upstream, Downstream | Large, scale exploration, refining, and petrochemical projects inherently necessitate the infusion of sizeable capital over a prolonged period as well as the exercise of financial discipline. |

| Environmental Compliance Requirements | All Types | More stringent environmental standards lead to increased costs for operations and monitoring throughout the value chain. |

| Dependence on Global Demand | Downstream | The revenues from exports continue to be very vulnerable to the changes in the pattern of international energy use and the dynamics of trade. |

| Skilled Workforce Constraints | Midstream, Downstream | The continuous talent development and provision of technical training become imperative in advanced processing and transportation operations. |

Saudi Arabia Oil and Gas Market Challenges

Irrespective of strong resource availability and state backing, the Saudi Arabia Oil and Gas Market Growth faces challenges such as managing long-term oil price uncertainty, balancing production discipline with revenue optimisation, and addressing rising environmental compliance expectations. In addition, the complex operations resulting from the need for a capital-intensive project execution, being dependent on the international energy demand, and the requirement of advanced technical skills necessitate constantly aligning policies, adopting technology, and engaging in workforce development initiatives.

Saudi Arabia Oil and Gas Market Trends

Major trends influencing the Saudi Arabia Oil and Gas Market Growth are:

- Expansion of Natural Gas Production: Increasing investments in gas fields support domestic power generation and industrial growth while reducing reliance on liquid fuels.

- Integration Across the Downstream Value Chain: The integration of refining with petrochemical production improves the competitiveness of the exported fuels and therefore allows for increased overall profitability.

- Digital Oilfield Adoption: The use of advanced analytics and automation facilitates efficiency, safety, and reservoir management results.

Investment Opportunities in the Saudi Arabia Oil and Gas Market

Opportunities for investment in the Oil and Gas Market of Saudi Arabia are abundantly available, which include the following:

- Developing Natural Gas Facilities and Pipelines :Building of new facilities and pipelines to enable the domestic energy transition process.

- Development of Refineries :- Investment in Advanced Technology Refineries that will develop new fuel products.

- New Petrochemical Development : Increasing production capacity for domestic and international markets.

Top 5 Leading Players in the Saudi Arabia Oil and Gas Market

The Saudi Arabia Oil and Gas Market is characterised by the presence of several leading industry players, including:

1. Saudi Aramco

| Company Name | Saudi Aramco |

|---|---|

| Established Year | 1933 |

| Headquarters | Dhahran, Saudi Arabia |

| Official Website | Click Here |

Saudi Aramco leads integrated oil and gas operations with extensive upstream, refining, and petrochemical capabilities supporting national energy objectives.

2. SABIC

| Company Name | SABIC |

|---|---|

| Established Year | 1976 |

| Headquarters | Riyadh, Saudi Arabia |

| Official Website | Click Here |

SABIC plays a key role in petrochemical integration, converting hydrocarbons into high-value industrial and consumer products.

3. Schlumberger

| Company Name | Schlumberger |

|---|---|

| Established Year | 1926 |

| Headquarters | Houston, USA |

| Official Website | Click Here |

Schlumberger provides advanced oilfield services and digital solutions supporting efficient upstream development in Saudi Arabia.

4. Halliburton

| Company Name | Halliburton | |

|---|---|---|

| Established Year | 1919 | |

| Headquarters | Houston, USA | |

| Official Website | Click Here |

Halliburton supports drilling, evaluation, and production optimization across major Saudi oil and gas fields.

5. Baker Hughes

| Company Name | Baker Hughes |

|---|---|

| Established Year | 1907 |

| Headquarters | Houston, USA |

| Official Website | Click Here |

Baker Hughes supplies energy technology solutions spanning upstream equipment, gas turbines, and LNG systems.

Government Regulations Introduced in the Saudi Arabia Oil and Gas Market

According to Saudi Government Data, long-term national energy policies that correspond with Vision 2030 and highlight the importance of sustainable resource utilisation and value chain extension mainly determine the Saudi Arabia Oil and Gas Market. The National Investment Strategy is designed to improve the production side of the oil industry, increase the localisation of the downstream sector, and promote the development of the gas sector, while the regulatory reforms facilitate the private and foreign investments. Moreover, the adoption of cleaner fuels, the reduction of flaring, and the setting of energy efficiency standards improve the operational sustainability of the industry.

Future Insights of the Saudi Arabia Oil and Gas Market

The Saudi Arabia Oil and Gas Industry outlook remains strong as continued investments in natural gas, refining modernisation, and petrochemical integration reshape the sector’s growth trajectory. Ongoing digital transformation, enhanced recovery technologies, and export-focused downstream projects are expected to improve operational efficiency and revenue resilience, while policy-driven diversification ensures sustained relevance of the oil and gas industry within the evolving national energy framework.

Market Segmentation Analysis

The report offers a comprehensive study of the subsequent market segments and their leading categories.

Downstream Segment to Dominate the Market – By Type

According to Bhushan, Senior Research Analyst, 6Wresearch, the Downstream segment dominates the Saudi Arabia Oil and Gas Market Share due to strong refinery expansion programs, rising petrochemical integration, and sustained government focus on maximising value addition from crude resources. Large-scale investments in complex refining units, export-oriented fuel production, and downstream industrial clusters enhance profitability and global competitiveness. Additionally, growing demand for refined fuels, chemicals, and speciality products supports capacity utilisation, while strategic location advantages strengthen Saudi Arabia role as a key downstream energy hub.

Key Attractiveness of the Report

- 10 Years of Market Numbers.

- Historical Data Starting from 2022 to 2025.

- Base Year: 2025.

- Forecast Data until 2032.

- Key Performance Indicators Impacting the Market.

- Major Upcoming Developments and Projects.

Key Highlights of the Report:

- Saudi Arabia Oil and Gas Market Outlook

- Market Size of Saudi Arabia Oil and Gas Market, 2025

- Forecast of Saudi Arabia Oil and Gas Market, 2032

- Historical Data and Forecast of Saudi Arabia Oil and Gas Revenues & Volume for the Period 2022- 2032

- Saudi Arabia Oil and Gas Market Trend Evolution

- Saudi Arabia Oil and Gas Market Drivers and Challenges

- Saudi Arabia Oil and Gas Price Trends

- Saudi Arabia Oil and Gas Porter's Five Forces

- Saudi Arabia Oil and Gas Industry Life Cycle

- Historical Data and Forecast of Saudi Arabia Oil and Gas Market Revenues & Volume By Type for the Period 2022- 2032

- Historical Data and Forecast of Saudi Arabia Oil and Gas Market Revenues & Volume By Upstream for the Period 2022- 2032

- Historical Data and Forecast of Saudi Arabia Oil and Gas Market Revenues & Volume By Midstream for the Period 2022- 2032

- Historical Data and Forecast of Saudi Arabia Oil and Gas Market Revenues & Volume By Downstream for the Period 2022- 2032

- Saudi Arabia Oil and Gas Import Export Trade Statistics

- Market Opportunity Assessment By Type

- Saudi Arabia Oil and Gas Top Companies Market Share

- Saudi Arabia Oil and Gas Competitive Benchmarking By Technical and Operational Parameters

- Saudi Arabia Oil and Gas Company Profiles

- Saudi Arabia Oil and Gas Key Strategic Recommendations

Market Covered

The report offers a comprehensive study of the subsequent market segments:

By Type

- Upstream

- Midstream

- Downstream

Saudi Arabia Oil and Gas Market (2026-2032): FAQs

Saudi Arabia Oil and Gas Market is projected to grow at a CAGR of 4.6% between 2026-2032.

The main contributors to the market are the top five oil and gas companies and service providers are Saudi Aramco, SABIC, Schlumberger, Halliburton, and Baker Hughes.

A long term equilibrium of the market is supported by continuous government investment, big hydrocarbon reserves and integration of the downstream sector.

The upstream segment leads due to strong production capacity, advanced recovery technologies, and consistent field development initiatives.

6Wresearch actively monitors the Saudi Arabia Oil and Gas Market and publishes its comprehensive annual report, highlighting emerging trends, growth drivers, revenue analysis, and forecast outlook. Our insights help businesses to make data-backed strategic decisions with ongoing market dynamics. Our analysts track relevent industries related to the Saudi Arabia Oil and Gas Market, allowing our clients with actionable intelligence and reliable forecasts tailored to emerging regional needs.

Yes, we provide customisation as per your requirements. To learn more, feel free to contact us on sales@6wresearch.com

| 1 Executive Summary |

| 2 Introduction |

| 2.1 Key Highlights of the Report |

| 2.2 Report Description |

| 2.3 Market Scope & Segmentation |

| 2.4 Research Methodology |

| 2.5 Assumptions |

| 3 Saudi Arabia Oil and Gas Market Overview |

| 3.1 Saudi Arabia Country Macro Economic Indicators |

| 3.2 Saudi Arabia Oil and Gas Market Revenues & Volume, 2022 & 2032F |

| 3.3 Saudi Arabia Oil and Gas Market - Industry Life Cycle |

| 3.4 Saudi Arabia Oil and Gas Market - Porter's Five Forces |

| 3.5 Saudi Arabia Oil and Gas Market Revenues & Volume Share, By Type, 2022 & 2032F |

| 4 Saudi Arabia Oil and Gas Market Dynamics |

| 4.1 Impact Analysis |

| 4.2 Market Drivers |

| 4.2.1 Government initiatives and investments in the oil and gas sector |

| 4.2.2 Technological advancements in exploration and production techniques |

| 4.2.3 Growing global energy demand and consumption |

| 4.3 Market Restraints |

| 4.3.1 Fluctuating oil prices and market volatility |

| 4.3.2 Environmental concerns and regulations impacting operations |

| 4.3.3 Geopolitical tensions affecting production and distribution |

| 5 Saudi Arabia Oil and Gas Market Trends |

| 6 Saudi Arabia Oil and Gas Market, By Types |

| 6.1 Saudi Arabia Oil and Gas Market, By Type |

| 6.1.1 Overview and Analysis |

| 6.1.2 Saudi Arabia Oil and Gas Market Revenues & Volume, By Type, 2022- 2032F |

| 6.1.3 Saudi Arabia Oil and Gas Market Revenues & Volume, By Upstream, 2022- 2032F |

| 6.1.4 Saudi Arabia Oil and Gas Market Revenues & Volume, By Midstream, 2022- 2032F |

| 6.1.5 Saudi Arabia Oil and Gas Market Revenues & Volume, By Downstream, 2022- 2032F |

| 7 Saudi Arabia Oil and Gas Market Import-Export Trade Statistics |

| 7.1 Saudi Arabia Oil and Gas Market Export to Major Countries |

| 7.2 Saudi Arabia Oil and Gas Market Imports from Major Countries |

| 8 Saudi Arabia Oil and Gas Market Key Performance Indicators |

| 8.1 Exploration success rate |

| 8.2 Operational efficiency metrics (e.g., drilling efficiency, production uptime) |

| 8.3 Investment in research and development for new technologies |

| 8.4 Health, safety, and environmental performance indicators |

| 8.5 Infrastructure development progress (e.g., pipeline construction, refinery capacity expansion) |

| 9 Saudi Arabia Oil and Gas Market - Opportunity Assessment |

| 9.1 Saudi Arabia Oil and Gas Market Opportunity Assessment, By Type, 2022 & 2032F |

| 10 Saudi Arabia Oil and Gas Market - Competitive Landscape |

| 10.1 Saudi Arabia Oil and Gas Market Revenue Share, By Companies, 2022-2032F |

| 10.2 Saudi Arabia Oil and Gas Market Competitive Benchmarking, By Operating and Technical Parameters |

| 11 Company Profiles |

| 12 Recommendations |

| 13 Disclaimer |

Global Go To Market Strategy - 2030

Export potential enables firms to identify high-growth global markets with greater confidence by combining advanced trade intelligence with a structured quantitative methodology. The framework analyzes emerging demand trends and country-level import patterns while integrating macroeconomic and trade datasets such as GDP and population forecasts, bilateral import–export flows, tariff structures, elasticity differentials between developed and developing economies, geographic distance, and import demand projections. Using weighted trade values from 2020–2024 as the base period to project country-to-country export potential for 2030, these inputs are operationalized through calculated drivers such as gravity model parameters, tariff impact factors, and projected GDP per-capita growth. Through an analysis of hidden potentials, demand hotspots, and market conditions that are most favorable to success, this method enables firms to focus on target countries, maximize returns, and global expansion with data, backed by accuracy.

By factoring in the projected importer demand gap that is currently unmet and could be potential opportunity, it identifies the potential for the Exporter (Country) among 190 countries, against the general trade analysis, which identifies the biggest importer or exporter.

To discover high-growth global markets and optimize your business strategy:

Click Here

Pricing

- Single User License$ 1,995

- Department License$ 2,400

- Site License$ 3,120

- Global License$ 3,795

Leadership Perspectives from Industry Events

Search

Thought Leadership and Analyst Meet

Our Clients

6WResearch In News

- India Export Attractiveness Tracker 2026

- India Air Conditioner Market Set for Strong Rebound in 2026 After Weather-Led Correction and GST-Driven Recovery: 6Wresearch

- ADAS in India: How Automatic Emergency Braking, Blind Spot Detection & Driver Monitoring are Transforming Road Safety

- Doha a strategic location for EV manufacturing hub: IPA Qatar

- Demand for luxury TVs surging in the GCC, says Samsung

- Empowering Growth: The Thriving Journey of Bangladesh’s Cable Industry

Latest Reports

- Nicaragua RPG Gaming Market (2026-2032)

- New Zealand RPG Gaming Market (2026-2032)

- Netherlands RPG Gaming Market (2026-2032)

- Nauru RPG Gaming Market (2026-2032)

- Namibia RPG Gaming Market (2026-2032)

- Mozambique RPG Gaming Market (2026-2032)

- Montenegro RPG Gaming Market (2026-2032)

- Mongolia RPG Gaming Market (2026-2032)

- Monaco RPG Gaming Market (2026-2032)

- Micronesia RPG Gaming Market (2026-2032)

Industry Events and Analyst Meet

EV India Expo 2026

HIMTEX 2026

India Refining Summit 2026

India EV Show 2026

EV tech India Expo 2026

Whitepaper

- Middle East & Africa Commercial Security Market Click here to view more.

- Middle East & Africa Fire Safety Systems & Equipment Market Click here to view more.

- GCC Drone Market Click here to view more.

- Middle East Lighting Fixture Market Click here to view more.

- GCC Physical & Perimeter Security Market Click here to view more.