Saudi Arabia Power Rental Market (2026-2032) | Outlook, Industry, Companies, Size, Forecast, Growth, Trends, Value, Share, Revenue & Analysis

Market Forecast By Fuel Type (Diesel, Natural Gas), By Equipment (Generators, Transformers, Load Banks), By Power Rating (Up to 50 kW, 51“500 kW, 501-2500 kW, Above 2500 kW), By Application (Standby power, Peak shaving, Base load/ continuous power), By End User (Utilities, Oil & gas, Construction, Manufacturing, Metal & Mining, IT and Data centers, Corporate & Retail) And Competitive Landscape

| Product Code: ETC4530940 | Publication Date: Jul 2023 | Updated Date: Feb 2026 | Product Type: Report | |

| Publisher: 6Wresearch | Author: Ravi Bhandari | No. of Pages: 85 | No. of Figures: 45 | No. of Tables: 25 |

Saudi Arabia Power Rental Market Growth Rate

According to 6Wresearch internal database and industry insights, the Saudi Arabia Power Rental Market is projected to grow at a compound annual growth rate (CAGR) of 7.6% during the forecast period (2026-2032).

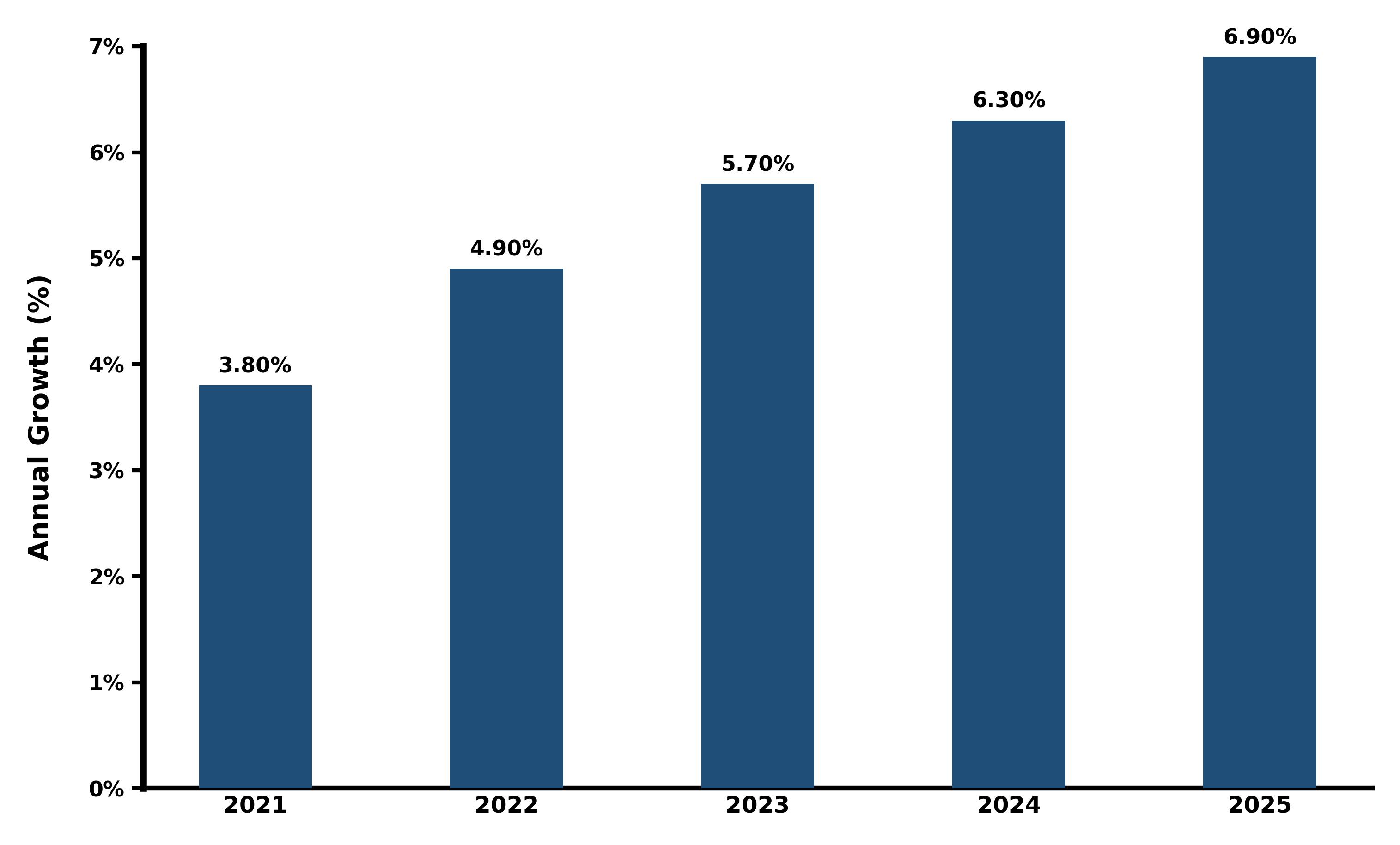

Saudi Arabia Power Rental Market Year-wise Growth Rate and Key Drivers

This graph highlights how the Saudi Arabia Power Rental Market has steadily grown over the past five years, supported by major growth factors.

The table below presents the year‑wise growth rates along with the key drivers influencing the market

| Years | Est. Annual Growth (%) | Growth Drivers |

| 2021 | 3.8% | Reliability needs for remote oilfield sites and Brownfield maintenance. |

| 2022 | 4.9% | Construction restarts and mega-project mobilization under Vision 2030. |

| 2023 | 5.7% | Data center build-outs and utility peak-load support in summer. |

| 2024 | 6.3% | Industrial expansion and tighter grid redundancy requirements. |

| 2025 | 6.9% | NEOM/Red Sea project phases and growing demand for gas-fueled rentals. |

Topics Covered in the Saudi Arabia Power Rental Market Report

Saudi Arabia Power Rental Market report thoroughly covers the market by fuel type, equipment, power rating, application, and end user. The market report provides an unbiased and detailed analysis of ongoing market trends, opportunities/high growth areas, and market drivers, which would help stakeholders devise and align their market strategies according to the current and future market dynamics.

Saudi Arabia Power Rental Market Highlights

| Report Name | Saudi Arabia Power Rental Market |

| Forecast period | 2026-2032 |

| CAGR | 7.6% |

| Growing Sector | Energy & Utilities |

Growing Sector-Saudi Arabia Power Rental Market Synopsis

Significant growth is on the horizon for the Saudi Arabia Power Rental Market fueled by continued investment in giga-projects, activity in oil & gas fields, and growth in industrial development. The desire for seasonal peak demand, activities in extreme operating conditions, and the necessity for fast-tracked power has led to adoption across segments such as utilities, construction and critical facilities. Economic diversification and localization initiatives led by the government are supporting greater in-kingdom service capability. Additionally, improving operating economics and emissions profiles due to increased preference will also be gas and hybrid rental solutions will lead to stable market growth in the Kingdom.

Evaluation of Growth Drivers in the Saudi Arabia Power Rental Market

Below mentioned some growth drivers and their impact on market dynamics:

| Drivers | Primary Segments Affected | Why It Matters |

| Mega-Projects & Infrastructure (NEOM, Red Sea, Qiddiya) | Generators, 501–2500 kW, Construction | Drives long-duration, multi-megawatt deployments. |

| Oil & Gas Field Requirements | Utilities, Oil & Gas, 51–500 kW and 501–2500 kW | Needs reliable prime and standby power in remote sites. |

| Utility Peak Shaving & Outage Support | Standby & Peak Shaving, Utilities | Stabilizes grid during summer peaks and maintenance. |

| Data Center & ICT Growth | IT & Data Centers, Base Load | Requires high-availability power with rapid mobilization. |

| Shift to Gas/Hybrid Sets | Natural Gas, Hybrid Controls | Reduces fuel cost and emissions, improving TCO for rentals. |

Saudi Arabia Power Rental Market is expected to grow significantly, with a CAGR of 7.6% during the forecast period of 2026-2032. The Saudi Arabia Power Rental Market is seeing strong growth due to large scale infrastructure developments for projects, like NEOM, Red Sea, and Qiddiya, and the overall uptick in energy consumption for industrial and oil and gas usages. The growing emphasis on reliable standby power and peak-shaving power solution resulting from abnormal weather patterns and over consumption of energy are also driving the Saudi Arabia Power Rental Market Growth. The rapid upscaling of the data center industry in Saudi Arabia is enabling additional growth as well along with the expanding use of natural gas and hybrid power systems that promote efficiency, emissions reductions and provide sustainable energy usage in critical sectors.

Evaluation of Restraints in the Saudi Arabia Power Rental Market

Below mentioned are some major restraints and their influence on market dynamics:

| Restraints | Primary Segments Affected | What This Means |

| Fuel Price Variability & Logistics | Diesel Fleets, Remote Sites | Impacts OPEX and project budgeting for long runs. |

| Procurement Cycles & Compliance | All Segments | Extended approvals can delay deployments. |

| High Ambient & Dust Conditions | Generators, Load Banks | Increases maintenance frequency and derating. |

| OEM Lead Times & Parts Availability | 501–2500 kW, Above 2500 kW | May constrain large fleet readiness. |

| Emissions & Noise Requirements | Urban Projects, Data Centers | Drives need for gas/hybrid and advanced muffling. |

Saudi Arabia Power Rental Market Challenges

Despite significant demand, the Saudi Arabia Power Rental Industry is experiencing challenges from inordinate extreme heat and dust, resulting in frequent maintenance and derating. The logistics to remote sites and the need for uptime certainty for those critical users makes it harder to operate. Other considerations like fuel efficiency, emissions compliance, and noise control in urban areas add to operating costs. Furthermore, sector-specific competition with capital equipment purchases impacts utilization for rental fleets across various environments affecting profitability and fleet readiness.

Saudi Arabia Power Rental Market Trends

Some major trends contributing to the development of the Saudi Arabia Power Rental Market growth are:

- Shift Toward Natural Gas & Hybrid Fleets: Operators expand gas-fired and hybrid sets to reduce fuel cost, extend maintenance intervals, and lower emissions.

- Digitization & Remote Monitoring: Telematics and predictive maintenance improve uptime, optimize fuel burn, and reduce unplanned downtime.

- Long-Term Project Contracts: Multi-year frameworks for giga-projects enhance fleet visibility and encourage investment in larger kW classes.

- High-Capacity Modular Deployments: Containerized 1–2.5 MW blocks enable rapid scaling for utilities and data centers.

- Sound Attenuation & Low-Emission Packages: Urban sites adopt advanced enclosures, SCRs, and filtration to meet site-specific limits.

Investment Opportunities in the Saudi Arabia Power Rental Market

Here are some investment opportunities in the Saudi Arabia Power Rental Industry:

- Gas-Fired Rental Capacity: Expand gas genset fleets and dual-fuel capability to win long-duration base-load contracts.

- Hybrid/Battery Integration: Add battery energy storage with smart controls to cut diesel runtime and fuel cost.

- Data Center Power Solutions: Develop Tier-ready rental packages with redundancy, load banks, and rapid switchgear.

- Desert-Hardened Fleets: Invest in high-ambient-rated units, advanced filtration, and service hubs near remote corridors.

- Local Service & IKTVA Alignment: Build in-kingdom overhaul, parts, and training to improve bid competitiveness.

Top 5 Leading Players in the Saudi Arabia Power Rental Market

Here are some top companies contributing to Saudi Arabia Power Rental Market Share:

1. Aggreko Middle East

| Company Name | Aggreko Middle East |

| Established Year | 1962 |

| Headquarters | Riyadh, Saudi Arabia |

| Official Website | Click Here |

Provider of temporary power and temperature control solutions with large multi-MW fleets supporting utilities, data centers, and mega-projects across the Kingdom.

2. Altaaqa Alternative Solutions (Zahid Group)

| Company Name | Altaaqa Alternative Solutions (Zahid Group) |

| Established Year | 2004 |

| Headquarters | Jeddah, Saudi Arabia |

| Official Website | Click Here |

Saudi leader in distributed power solutions offering diesel and gas rentals, turnkey EPC, and long-term O&M aligned with IKTVA goals.

3. Byrne Equipment Rental

| Company Name | Byrne Equipment Rental |

| Established Year | 1992 |

| Headquarters | Al Khobar, Saudi Arabia |

| Official Website | Click Here |

Integrated equipment and power rental provider with strong presence in oil & gas and construction, offering high-ambient-rated fleets and site services.

4. Saudi Diesel Equipment Co.

| Company Name | Saudi Diesel Equipment Co. |

| Established Year | 1978 |

| Headquarters | Dammam, Saudi Arabia |

| Official Website | Click Here |

Local manufacturer/distributor with rental offerings for generators and power systems, providing maintenance, parts, and rapid-response support.

5. Jubaili Bros

| Company Name | Jubaili Bros |

| Established Year | 1977 |

| Headquarters | Al Khobar, Saudi Arabia |

| Official Website | Click Here |

Regional generator specialist supplying and renting diesel/gas sets, switchgear, and load banks for industrial and utility applications.

Government Regulations Introduced in the Saudi Arabia Power Rental Market

According to Saudi Arabian government data, the Kingdom advances power availability and localization through Vision 2030 and the National Renewable Energy Program (NREP). Policies promoting in-kingdom value addition include Saudi Aramco’s IKTVA initiative, encouraging local manufacturing, service hubs, and workforce development. Grid reliability projects via the Saudi Electricity Company (SEC) and GCC Interconnection Authority enhance peak support and contingency readiness. Giga-projects such as NEOM and the Red Sea Project require strict environmental, noise, and safety standards, steering rentals toward gas/hybrid solutions and advanced attenuation packages, while public procurement frameworks favor vendors with strong in-kingdom service capabilities.

Future Insights of the Saudi Arabia Power Rental Market

The Saudi Arabia Power Rental Market is expected to undergo substantial growth throughout the duration of the forecast. Strong demand for utility peak shaving, the power requirements for various giga-projects, and the demand for high-uptime industrial operations will fuel this growth and rental providers will utilize equipment, with improved efficiencies and profits, using gas and hybrid systems, along with digitized fleet management and modular multi-megawatt blocks. In addition, localization efforts and the creation of strategic service hubs across the Kingdom will allow Saudi power rental providers to become more competitive, creating growth opportunities for the power rental providers and OEMs.

Market Segmentation Analysis

The report offers a comprehensive study of the subsequent market segments and their leading categories.

Diesel to Dominate the Market – By Fuel Type

According to Ritika Kalra, Senior Research Analyst, 6Wresearch, Diesel remains the dominant fuel type owing to its rapid availability, robust logistics, and flexibility for short-notice mobilizations across construction and oilfield operations. While gas penetration is rising, diesel fleets continue to secure the majority of short- to medium-duration standby and prime contracts, particularly in remote or shifting sites where pipeline access is limited.

2Generators to Dominate the Market – By Equipment

Generators account for the largest share as they form the core of temporary power packages across utilities, construction, and industrial users. Their modularity, availability in high-ambient-rated enclosures, and compatibility with advanced control systems make them the preferred equipment, with transformers and load banks deployed as supporting assets.

501–2500 kW to Dominate the Market – By Power Rating

The 501–2500 kW range leads demand due to large construction clusters, utility peak support, and multi-MW data center requirements that favor containerized 1–2.5 MW blocks. This rating balances fast mobilization with lower installed cost per kW and integrates easily with switchgear, paralleling, and load management systems.

Standby Power to Dominate the Market – By Application

Standby power holds the leading share driven by seasonal peak demand, outage coverage during maintenance, and redundancy mandates for critical loads. Rapid deployment and high reliability make rental standby packages the first choice for utilities, healthcare, and commercial hubs, while base-load sets grow in long-duration project sites.

Utilities to Dominate the Market By End User

Utilities remain the dominant end user as the Saudi Electricity Company and municipal utilities increasingly deploy rental fleets for peak shaving, maintenance outages, and contingency plans. Their need for scalable, quickly dispatchable power positions rental solutions as a strategic tool, with oil & gas and data centers growing as high-value niches.

Key attractiveness of the report

- 10 Years Market Numbers.

- Historical Data Starting from 2022 to 2025.

- Base Year: 2025

- Forecast Data until 2032.

- Key Performance Indicators Impacting the Market.

- Major Upcoming Developments and Projects.

Key Highlights of the Report:

- Saudi Arabia Power Rental Market Outlook

- Market Size of Saudi Arabia Power Rental Market, 2025

- Forecast of Saudi Arabia Power Rental Market, 2032

- Historical Data and Forecast of Saudi Arabia Power Rental Revenues & Volume for the Period 2022-2032

- Saudi Arabia Power Rental Market Trend Evolution

- Saudi Arabia Power Rental Market Drivers and Challenges

- Saudi Arabia Power Rental Price Trends

- Saudi Arabia Power Rental Porter's Five Forces

- Saudi Arabia Power Rental Industry Life Cycle

- Historical Data and Forecast of Saudi Arabia Power Rental Market Revenues & Volume By Fuel Type for the Period 2022-2032

- Historical Data and Forecast of Saudi Arabia Power Rental Market Revenues & Volume By Diesel for the Period 2022-2032

- Historical Data and Forecast of Saudi Arabia Power Rental Market Revenues & Volume By Natural Gas for the Period 2022-2032

- Historical Data and Forecast of Saudi Arabia Power Rental Market Revenues & Volume By Equipment for the Period 2022-2032

- Historical Data and Forecast of Saudi Arabia Power Rental Market Revenues & Volume By Generators for the Period 2022-2032

- Historical Data and Forecast of Saudi Arabia Power Rental Market Revenues & Volume By Transformers for the Period 2022-2032

- Historical Data and Forecast of Saudi Arabia Power Rental Market Revenues & Volume By Load Banks for the Period 2022-2032

- Historical Data and Forecast of Saudi Arabia Power Rental Market Revenues & Volume By Power Rating for the Period 2022-2032

- Historical Data and Forecast of Saudi Arabia Power Rental Market Revenues & Volume By Up to 50 kW for the Period 2022-2032

- Historical Data and Forecast of Saudi Arabia Power Rental Market Revenues & Volume By 51??500 kW for the Period 2022-2032

- Historical Data and Forecast of Saudi Arabia Power Rental Market Revenues & Volume By 501-2500 kW for the Period 2022-2032

- Historical Data and Forecast of Saudi Arabia Power Rental Market Revenues & Volume By Above 2500 kW for the Period 2022-2032

- Historical Data and Forecast of Saudi Arabia Power Rental Market Revenues & Volume By Application for the Period 2022-2032

- Historical Data and Forecast of Saudi Arabia Power Rental Market Revenues & Volume By Standby power for the Period 2022-2032

- Historical Data and Forecast of Saudi Arabia Power Rental Market Revenues & Volume By Peak shaving for the Period 2022-2032

- Historical Data and Forecast of Saudi Arabia Power Rental Market Revenues & Volume By Base load/ continuous power for the Period 2022-2032

- Historical Data and Forecast of Saudi Arabia Power Rental Market Revenues & Volume By End User for the Period 2022-2032

- Historical Data and Forecast of Saudi Arabia Power Rental Market Revenues & Volume By Utilities for the Period 2022-2032

- Historical Data and Forecast of Saudi Arabia Power Rental Market Revenues & Volume By Oil & gas for the Period 2022-2032

- Historical Data and Forecast of Saudi Arabia Power Rental Market Revenues & Volume By Construction for the Period 2022-2032

- Historical Data and Forecast of Saudi Arabia Power Rental Market Revenues & Volume By Manufacturing for the Period 2022-2032

- Historical Data and Forecast of Saudi Arabia Power Rental Market Revenues & Volume By Metal & Mining for the Period 2022-2032

- Historical Data and Forecast of Saudi Arabia Power Rental Market Revenues & Volume By IT and Data centers for the Period 2022-2032

- Historical Data and Forecast of Saudi Arabia Power Rental Market Revenues & Volume By Corporate & Retail for the Period 2022-2032

- Saudi Arabia Power Rental Import Export Trade Statistics

- Market Opportunity Assessment By Fuel Type

- Market Opportunity Assessment By Equipment

- Market Opportunity Assessment By Power Rating

- Market Opportunity Assessment By Application

- Market Opportunity Assessment By End User

- Saudi Arabia Power Rental Top Companies Market Share

- Saudi Arabia Power Rental Competitive Benchmarking By Technical and Operational Parameters

- Saudi Arabia Power Rental Company Profiles

- Saudi Arabia Power Rental Key Strategic Recommendations

Market Covered

The report subsequently covers the market by following segments and subsegments:

By Fuel Type

- Diesel

- Natural Gas

By Equipment

- Generators

- Transformers

- Load Banks

By Power Rating

- Up to 50 kW

- 51–500 kW

- 501–2500 kW

- Above 2500 kW

By Application

- Standby power

- Peak shaving

- Base load/ continuous power

By End User

- Utilities

- Oil & gas

- Construction

- Manufacturing

- Metal & Mining

- IT and Data centers

- Corporate & Retail

Saudi Arabia Power Rental Market (2026-2032): FAQs

The market is projected to grow at a CAGR of around 7.6% during 2026–2032.

Growth is being driven by giga-project timelines, summer peak-load support, data center expansion, and adoption of gas/hybrid rental solutions.

Opportunities include gas-fired and hybrid fleets, battery integration, Tier-ready data center packages, and desert-hardened high-ambient units with local service hubs.

Generators remain the dominant equipment category in the Saudi Arabia power rental market.

6Wresearch actively monitors the Saudi Arabia Power Rental Market and publishes its comprehensive annual report, highlighting emerging trends, growth drivers, revenue analysis, and forecast outlook. Our insights help businesses to make data-backed strategic decisions with ongoing market dynamics. Our analysts track relevent industries related to the Saudi Arabia Power Rental Market, allowing our clients with actionable intelligence and reliable forecasts tailored to emerging regional needs.

Yes, we provide customisation as per your requirements. To learn more, feel free to contact us on sales@6wresearch.com

| 1 Executive Summary |

| 2 Introduction |

| 2.1 Key Highlights of the Report |

| 2.2 Report Description |

| 2.3 Market Scope & Segmentation |

| 2.4 Research Methodology |

| 2.5 Assumptions |

| 3 Saudi Arabia Power Rental Market Overview |

| 3.1 Saudi Arabia Country Macro Economic Indicators |

| 3.2 Saudi Arabia Power Rental Market Revenues & Volume, 2022 & 2032F |

| 3.3 Saudi Arabia Power Rental Market - Industry Life Cycle |

| 3.4 Saudi Arabia Power Rental Market - Porter's Five Forces |

| 3.5 Saudi Arabia Power Rental Market Revenues & Volume Share, By Fuel Type, 2022 & 2032F |

| 3.6 Saudi Arabia Power Rental Market Revenues & Volume Share, By Equipment, 2022 & 2032F |

| 3.7 Saudi Arabia Power Rental Market Revenues & Volume Share, By Power Rating, 2022 & 2032F |

| 3.8 Saudi Arabia Power Rental Market Revenues & Volume Share, By Application, 2022 & 2032F |

| 3.9 Saudi Arabia Power Rental Market Revenues & Volume Share, By End User, 2022 & 2032F |

| 4 Saudi Arabia Power Rental Market Dynamics |

| 4.1 Impact Analysis |

| 4.2 Market Drivers |

| 4.2.1 Increasing construction activities and infrastructure projects in Saudi Arabia |

| 4.2.2 Growth in events and entertainment industry leading to higher demand for temporary power solutions |

| 4.2.3 Expansion of oil and gas industry requiring power rental services |

| 4.3 Market Restraints |

| 4.3.1 Fluctuating fuel prices impacting operational costs of power rental companies |

| 4.3.2 Stringent environmental regulations influencing choice of power sources |

| 4.3.3 Economic volatility affecting investments in power rental equipment |

| 5 Saudi Arabia Power Rental Market Trends |

| 6 Saudi Arabia Power Rental Market, By Types |

| 6.1 Saudi Arabia Power Rental Market, By Fuel Type |

| 6.1.1 Overview and Analysis |

| 6.1.2 Saudi Arabia Power Rental Market Revenues & Volume, By Fuel Type, 2022-2032F |

| 6.1.3 Saudi Arabia Power Rental Market Revenues & Volume, By Diesel, 2022-2032F |

| 6.1.4 Saudi Arabia Power Rental Market Revenues & Volume, By Natural Gas, 2022-2032F |

| 6.2 Saudi Arabia Power Rental Market, By Equipment |

| 6.2.1 Overview and Analysis |

| 6.2.2 Saudi Arabia Power Rental Market Revenues & Volume, By Generators, 2022-2032F |

| 6.2.3 Saudi Arabia Power Rental Market Revenues & Volume, By Transformers, 2022-2032F |

| 6.2.4 Saudi Arabia Power Rental Market Revenues & Volume, By Load Banks, 2022-2032F |

| 6.3 Saudi Arabia Power Rental Market, By Power Rating |

| 6.3.1 Overview and Analysis |

| 6.3.2 Saudi Arabia Power Rental Market Revenues & Volume, By Up to 50 kW, 2022-2032F |

| 6.3.3 Saudi Arabia Power Rental Market Revenues & Volume, By 51??500 kW, 2022-2032F |

| 6.3.4 Saudi Arabia Power Rental Market Revenues & Volume, By 501-2500 kW, 2022-2032F |

| 6.3.5 Saudi Arabia Power Rental Market Revenues & Volume, By Above 2500 kW, 2022-2032F |

| 6.4 Saudi Arabia Power Rental Market, By Application |

| 6.4.1 Overview and Analysis |

| 6.4.2 Saudi Arabia Power Rental Market Revenues & Volume, By Standby power, 2022-2032F |

| 6.4.3 Saudi Arabia Power Rental Market Revenues & Volume, By Peak shaving, 2022-2032F |

| 6.4.4 Saudi Arabia Power Rental Market Revenues & Volume, By Base load/ continuous power, 2022-2032F |

| 6.5 Saudi Arabia Power Rental Market, By End User |

| 6.5.1 Overview and Analysis |

| 6.5.2 Saudi Arabia Power Rental Market Revenues & Volume, By Utilities, 2022-2032F |

| 6.5.3 Saudi Arabia Power Rental Market Revenues & Volume, By Oil & gas, 2022-2032F |

| 6.5.4 Saudi Arabia Power Rental Market Revenues & Volume, By Construction, 2022-2032F |

| 6.5.5 Saudi Arabia Power Rental Market Revenues & Volume, By Manufacturing, 2022-2032F |

| 6.5.6 Saudi Arabia Power Rental Market Revenues & Volume, By Metal & Mining, 2022-2032F |

| 6.5.7 Saudi Arabia Power Rental Market Revenues & Volume, By IT and Data centers, 2022-2032F |

| 7 Saudi Arabia Power Rental Market Import-Export Trade Statistics |

| 7.1 Saudi Arabia Power Rental Market Export to Major Countries |

| 7.2 Saudi Arabia Power Rental Market Imports from Major Countries |

| 8 Saudi Arabia Power Rental Market Key Performance Indicators |

| 8.1 Average utilization rate of power rental equipment |

| 8.2 Percentage of revenue from long-term contracts |

| 8.3 Number of new power rental projects secured |

| 8.4 Average rental rates for various power equipment |

| 8.5 Customer satisfaction scores for power rental services |

| 9 Saudi Arabia Power Rental Market - Opportunity Assessment |

| 9.1 Saudi Arabia Power Rental Market Opportunity Assessment, By Fuel Type, 2022 & 2032F |

| 9.2 Saudi Arabia Power Rental Market Opportunity Assessment, By Equipment, 2022 & 2032F |

| 9.3 Saudi Arabia Power Rental Market Opportunity Assessment, By Power Rating, 2022 & 2032F |

| 9.4 Saudi Arabia Power Rental Market Opportunity Assessment, By Application, 2022 & 2032F |

| 9.5 Saudi Arabia Power Rental Market Opportunity Assessment, By End User, 2022 & 2032F |

| 10 Saudi Arabia Power Rental Market - Competitive Landscape |

| 10.1 Saudi Arabia Power Rental Market Revenue Share, By Companies, 2025 |

| 10.2 Saudi Arabia Power Rental Market Competitive Benchmarking, By Operating and Technical Parameters |

| 11 Company Profiles |

| 12 Recommendations |

| 13 Disclaimer |

Global Go To Market Strategy - 2030

Export potential enables firms to identify high-growth global markets with greater confidence by combining advanced trade intelligence with a structured quantitative methodology. The framework analyzes emerging demand trends and country-level import patterns while integrating macroeconomic and trade datasets such as GDP and population forecasts, bilateral import–export flows, tariff structures, elasticity differentials between developed and developing economies, geographic distance, and import demand projections. Using weighted trade values from 2020–2024 as the base period to project country-to-country export potential for 2030, these inputs are operationalized through calculated drivers such as gravity model parameters, tariff impact factors, and projected GDP per-capita growth. Through an analysis of hidden potentials, demand hotspots, and market conditions that are most favorable to success, this method enables firms to focus on target countries, maximize returns, and global expansion with data, backed by accuracy.

By factoring in the projected importer demand gap that is currently unmet and could be potential opportunity, it identifies the potential for the Exporter (Country) among 190 countries, against the general trade analysis, which identifies the biggest importer or exporter.

To discover high-growth global markets and optimize your business strategy:

Click Here

Pricing

- Single User License$ 1,995

- Department License$ 2,400

- Site License$ 3,120

- Global License$ 3,795

Leadership Perspectives from Industry Events

Search

Thought Leadership and Analyst Meet

Our Clients

6WResearch In News

- India Export Attractiveness Tracker 2026

- India Air Conditioner Market Set for Strong Rebound in 2026 After Weather-Led Correction and GST-Driven Recovery: 6Wresearch

- ADAS in India: How Automatic Emergency Braking, Blind Spot Detection & Driver Monitoring are Transforming Road Safety

- Doha a strategic location for EV manufacturing hub: IPA Qatar

- Demand for luxury TVs surging in the GCC, says Samsung

- Empowering Growth: The Thriving Journey of Bangladesh’s Cable Industry

Latest Reports

- Nicaragua RPG Gaming Market (2026-2032)

- New Zealand RPG Gaming Market (2026-2032)

- Netherlands RPG Gaming Market (2026-2032)

- Nauru RPG Gaming Market (2026-2032)

- Namibia RPG Gaming Market (2026-2032)

- Mozambique RPG Gaming Market (2026-2032)

- Montenegro RPG Gaming Market (2026-2032)

- Mongolia RPG Gaming Market (2026-2032)

- Monaco RPG Gaming Market (2026-2032)

- Micronesia RPG Gaming Market (2026-2032)

Industry Events and Analyst Meet

EV India Expo 2026

HIMTEX 2026

India Refining Summit 2026

India EV Show 2026

EV tech India Expo 2026

Whitepaper

- Middle East & Africa Commercial Security Market Click here to view more.

- Middle East & Africa Fire Safety Systems & Equipment Market Click here to view more.

- GCC Drone Market Click here to view more.

- Middle East Lighting Fixture Market Click here to view more.

- GCC Physical & Perimeter Security Market Click here to view more.