Singapore Construction Materials Market (2025-2031) | Growth, Analysis, Size, Companies, Share, Trends, Outlook, Industry, Value, Revenue & Forecast

Market Forecast By Product Type (Construction aggregates, Concrete bricks, Cement, Construction metals), By Application (Residential, Commercial, Industrial) And Competitive Landscape

| Product Code: ETC016727 | Publication Date: Oct 2020 | Updated Date: Mar 2026 | Product Type: Report | |

| Publisher: 6Wresearch | Author: Ravi Bhandari | No. of Pages: 70 | No. of Figures: 35 | No. of Tables: 5 |

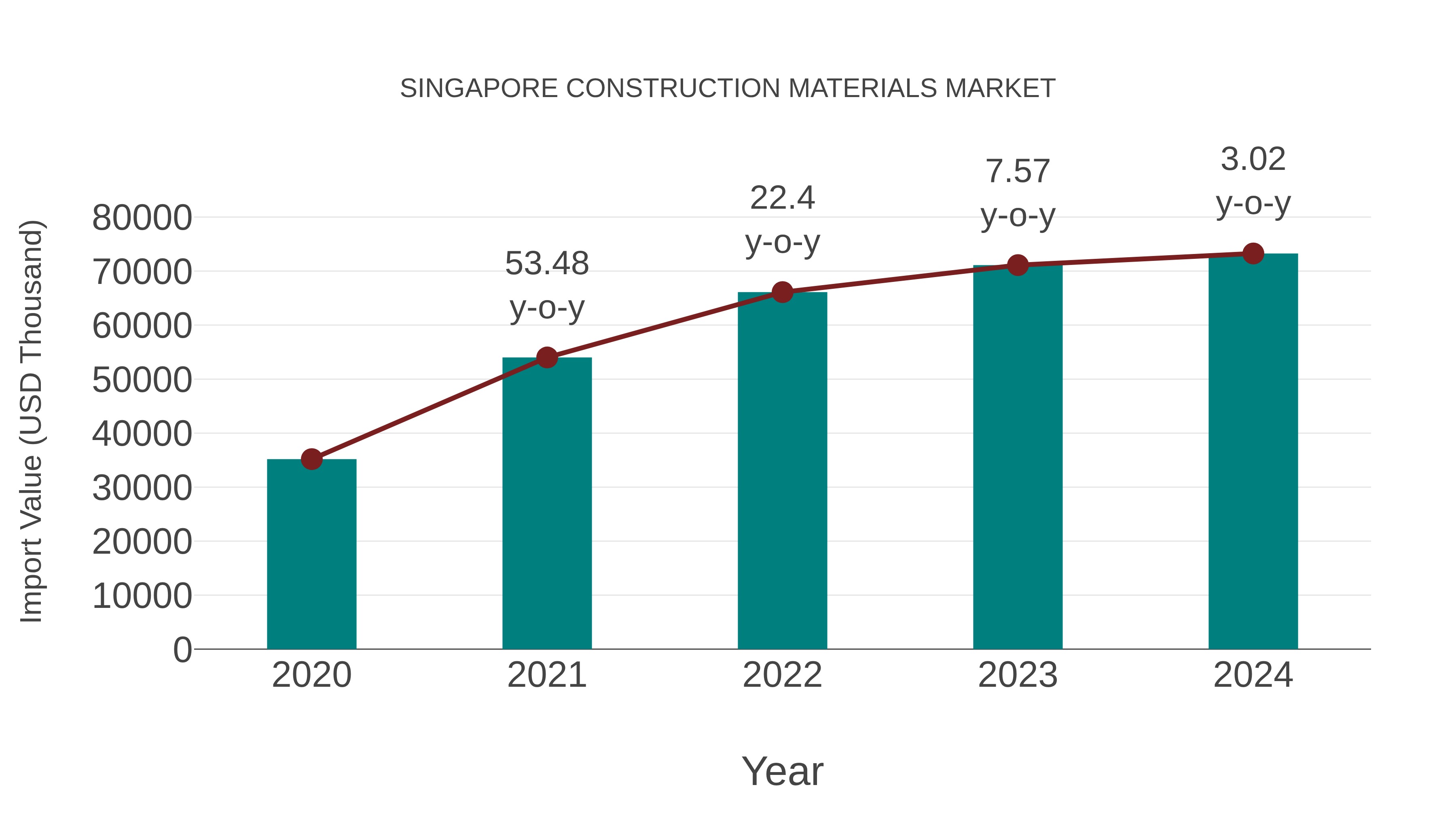

Singapore Construction Materials Market: Import Trend Analysis

In the Singapore construction materials market, the import trend showed a growth rate of 3.02% from 2023 to 2024, with a compound annual growth rate (CAGR) of 20.12% for the period 2020-2024. This upward import momentum can be attributed to the sustained demand for construction materials in response to ongoing infrastructure development projects within the region.

Singapore Construction Materials Market Growth Rate

According to 6Wresearch internal database and industry insights, the Singapore Construction Materials Market is projected to grow at a compound annual growth rate (CAGR) of 5.6% during the forecast period (2025–2031).

Singapore Construction Materials Market Highlights

| Report Name | Singapore Construction Materials Market |

| Forecast period | 2025-2031 |

| CAGR | 5.6% |

| Growing Sector | Construction and Infrastructure |

Five-Year Growth Trajectory of the Singapore Construction Materials Market with Core Drivers

Below mentioned are the evaluation of year-wise growth rate along with key drivers:

| Year | Est. Annual Growth () | Growth Drivers |

| 2020 | 1.8 | Essential public works, HDB handovers, and maintenance programs preserved baseline materials demand. |

| 2021 | 2.7 | Restart of major tenders and productivity push via PPVC/DFMA supported concrete and steel orders. |

| 2022 | 3.9 | Acceleration of MRT and road packages; façade upgrades in commercial assets increased glass demand. |

| 2023 | 4.8 | Tuas Mega Port and Changi Terminal 5 enabling works lifted cement and precast volumes. |

| 2024 | 5.5 | Higher HDB launches, urban renewal, and Green Mark upgrades drove steady ready-mix and rebar consumption |

Topics Covered in the Singapore Construction Materials Market Report

The Singapore Construction Materials Market report thoroughly covers the market by material types, applications, end users, form, and distribution channels. The report provides an unbiased and detailed analysis of ongoing market trends, opportunities/high-growth areas, and market drivers that will help stakeholders devise and align strategies according to current and future market dynamics.

Singapore Construction Materials Market Synopsis

Singapore Construction Materials Market is expected to witness steady growth on the back of a robust public infrastructure pipeline, sustained public housing supply, and renewal of mature estates. The demand for concrete, cement, steel, high-performance glass, and engineered wood is supported by multi-year investments in MRT lines, port consolidation at Tuas, airport expansion, and brownfield asset upgrades. Strong regulatory emphasis on quality (SNI equivalent via SS/BCA specifications), productivity (PPVC/DFMA), and sustainability (Green Mark, Super Low Energy) underpins consistent materials uptake across residential, commercial, industrial, and infrastructure works.

Evaluation of Growth Drivers in the Singapore Construction Materials Market

Below mentioned are some prominent drivers and their influence on the Singapore Construction Materials Market dynamics:

| Drivers | Primary Segments Affected | Why it Matters (Evidence) |

| Public Infrastructure Pipeline (MRT, Roads, Water) | Cement, Concrete, Steel, Glass | Multi-year rail and water projects secure bulk procurement for ready-mix, precast, rebar, and architectural glazing. |

| Tuas Mega Port & Changi T5 Programs | Cement, Concrete, Steel | Mega platforms and terminals intensify demand for marine-grade concrete, aggregates, and structural steel. |

| HDB Supply & Estate Renewal | Concrete, Glass, Wood | Continuous public housing launches and upgrading spur steady orders for blocks, finishes, and façades. |

| Green Mark & Super Low Energy Standards | Glass, Concrete, Wood, Steel | Efficiency targets favor high-spec glass, admixture-optimized concrete, engineered wood, and recycled materials. |

Singapore Construction Materials Market is expected to grow steadily at 5.6% CAGR between 2025 and 2031. The Growth of the market is attributed to continuous public infrastructure development, steady public housing programs, and large-scale asset rejuvenation in core business districts. The Singapore Construction Materials Market Growth is further strengthened by sustained investments in transport, water, and urban redevelopment projects. Concrete and cement will remain a major player due to their wide application in structural works, while steel demand continues to increase with industrial and bridge projects. Additionally, high-performance glass benefits from Green Mark–driven façade and energy-efficient building upgrades.

Evaluation of Restraints in the Singapore Construction Materials Market

Below mentioned are some major restraints and their influence on the Singapore Construction Materials Market dynamics:

| Restraints | Primary Segments Affected | What this Means (Evidence) |

| Import Dependence for Aggregates & Steel | Cement, Concrete, Steel | Sourcing sensitivity to regional supply and freight can affect pricing and availability. |

| Land & Logistics Constraints | All Materials | Limited storage space and urban logistics windows raise handling costs and scheduling complexity. |

| Tight Manpower Supply & Wage Pressures | Concrete, Steel, Wood | Higher labor costs and quotas drive adoption of PPVC/DFMA but raise upfront pricing for some products. |

| Stringent Specifications & Compliance Costs | Glass, Concrete, Steel | High performance and testing requirements increase capex for plants and QA systems. |

Singapore Construction Materials Market Challenges

The Singapore Construction Materials Industry faces a delicate balancing act in achieving cost control while maintaining strict performance standards. The space constraints of batching and recycling operations and the reliance on imported aggregates and steel influence volatile supply and costs. Additionally, labor shortages are motivating the use of prefabricated and modular methods of construction such as Prefabricated Prefinished Volumetric Construction (PPVC) and Design for Manufacturing and Assembly (DFMA). The sector must also be able to improve permitting processes, logistics, and environmental sustainability in a densely urbanized enclave to remain competitive.

Singapore Construction Materials Market Trends

Several significant trends are impacting Singapore Construction Materials Market:

- Adoption of PPVC/DFMA: Wider use of modular/precast systems shortens schedules and improves quality, lifting demand for precast elements and performance concretes.

- Green Mark–Driven Façade Upgrades: Energy targets spur low-e/solar-control glass and better insulation, increasing premium façade materials.

- Lower-Carbon Concrete & SCMs: Blended cements and admixtures reduce clinker intensity while maintaining strength and durability.

- C&D Recycling & Circularity: Higher utilization of recycled aggregates and asphalt enhances resource efficiency and reduces landfill.

- Digital Procurement & E-Delivery: E-platforms improve price discovery, logistics visibility, and compliance tracking across projects.

Investment Opportunities in the Singapore Construction Materials Industry

Some of the notable investment opportunities are:

- Precast & PPVC Facilities: Add automated plants near growth corridors to serve housing and healthcare builds.

- Low-Carbon Materials & Admixtures: Invest in SCM supply chains, performance admixtures, and EPD-backed concrete mixes.

- High-Performance Façade Systems: Growing capacity for unitized façades and low-e glass to achieve Green Mark target.

- Urban Logistics & Micro-warehousing: Create just-in-time distribution hubs to alleviate last-mile constraints.

- C&D Waste Processing: Increase advanced recycling for aggregates and reclaimed asphalt to help circular construction.

Top 5 Leading Players in the Singapore Construction Materials Market

Below is the list of prominent companies leading in the Singapore Construction Materials Market Share:

1. Pan-United Corporation Ltd

| Company Name | Pan-United Corporation Ltd |

|---|---|

| Headquarters | Singapore |

| Established Year | 1993 |

| Official Website | Click Here |

Pan-United Corporation Ltd is a leading producer of ready-mix and low-carbon concrete in Singapore. The company supplies high-performance concrete mixes for major infrastructure projects such as MRT lines, ports, and large-scale building developments. It is recognised for its innovation in sustainable construction materials and digital concrete solutions.

2. Holcim (Singapore) Ltd

| Company Name | Holcim (Singapore) Ltd |

|---|---|

| Headquarters | Singapore |

| Established Year | 2004 |

| Official Website | Click Here |

Holcim Singapore is a subsidiary of the global Holcim Group, offering cement, ready-mix concrete, and green construction technologies. The company supports commercial, residential, and infrastructure projects, focusing on decarbonisation and circular construction practices to meet Singapore’s sustainability goals.

3. NatSteel Holdings Pte Ltd

| Company Name | NatSteel Holdings Pte Ltd |

|---|---|

| Headquarters | Singapore |

| Established Year | 1961 |

| Official Website | Click Here |

NatSteel Holdings Pte Ltd is one of Singapore’s key steel manufacturers, producing reinforcing steel and wire products. The company serves construction, housing, and industrial sectors, providing sustainable steel solutions that meet regional infrastructure demands and green building standards.

4. BRC Asia Limited

| Company Name | BRC Asia Limited |

|---|---|

| Headquarters | Singapore |

| Established Year | 1938 |

| Official Website | Click Here |

BRC Asia Limited is a major reinforcement steel solutions provider, specialising in prefabricated rebar, welded mesh, and reinforcement steel products. The company plays a crucial role in high-rise building and civil engineering projects, ensuring efficiency, safety, and compliance with modern construction standards.

5. Samwoh Corporation Pte Ltd

| Company Name | Samwoh Corporation Pte Ltd |

|---|---|

| Headquarters | Singapore |

| Established Year | 1975 |

| Official Website | Click Here |

Samwoh Corporation Pte Ltd offers a diverse portfolio in construction materials and infrastructure services, including asphalt, aggregates, and recycled materials. The company is a pioneer in sustainable road construction, airport works, and circular economy initiatives, driving Singapore’s vision for a greener built environment.

Government Regulations Introduced in the Singapore Construction Materials Market

According to Singaporean Government data, several initiatives strengthen construction activity and material quality: (i) BCA Green Mark and Super Low Energy standards incentivize energy-efficient materials (low-e glass, high-performance insulation); (ii) PPVC/DFMA adoption policies drive modular and precast uptake; (iii) the Built Environment Industry Transformation Map (ITM) and BuildSG programs enhance productivity and digitalization; (iv) continued MRT expansion, Tuas Mega Port, and Changi T5 programs sustain bulk material demand; (v) HDB public housing and estate renewal pipelines ensure steady residential materials flow; and (vi) Resource Sustainability Act promotes C&D waste reduction and recycled aggregates use. These measures collectively support standardized, higher-quality demand across the market.

Future Insights of the Singapore Construction Materials Market

Singapore Construction Materials Industry will maintain momentum as public infrastructure and housing continue, while stricter sustainability targets accelerate the shift to low-carbon mixes, engineered façades, and circular materials. Investment in PPVC/DFMA capacity, digital procurement, and urban logistics hubs will raise productivity and reliability. Over the forecast period, the supply base will become greener and more integrated, with resilience enhanced by diversified imports, advanced recycling, and performance certifications aligned to Green Mark outcomes.

Market Segmentation Analysis

The report offers a comprehensive study of the subsequent market segments and their leading categories.

By Material Type – Concrete to Dominate the Market

According to Ritika Kalra, Senior Research Analyst, 6Wresearch, Concrete is projected to dominate the Singapore Construction Materials Market Share due to its pervasive use in high-rise buildings, MRT structures, ports, and airport works. Ready-mix and precast components underpin rapid, high-quality construction, supported by stringent specifications and productivity mandates.

By Application – Infrastructure Development to Dominate the Market

Infrastructure Development holds the largest share given the scale of MRT extensions, Tuas Mega Port, airport expansion, water treatment, and coastal protection works. These programs require sustained procurement of ready-mix, precast, rebar, and façade systems under multi-year contracts, outweighing single-asset commercial or industrial builds and ensuring consistent plant utilization.

By End User – Government Agencies to Dominate the Market

Government Agencies lead the market through public sector projects and specifications that shape materials selection (Green Mark thresholds, PPVC adoption, testing protocols). Their multi-year tenders for transport and housing create predictable offtake for concrete, steel, and façade materials, surpassing the aggregated demand from private developers, contractors, and architects.

By Form – Liquid to Dominate the Market

Liquid forms (notably ready-mix concrete and specialty admixtures) dominate due to the city-state’s reliance on just-in-time deliveries for dense urban sites. Continuous pours for high-rise and infrastructure elements, combined with advanced admixture designs, favor liquid materials over powders (cement), solids (steel, wood), granules (aggregates), or blocks (AAC).

By Distribution Channel – Direct Sales to Dominate the Market

Direct Sales command the largest share as major projects procure directly from producers under framework or project-specific agreements. This model ensures specification control, QA/QC traceability, and assured capacity, exceeding the roles of distributors, wholesale suppliers, specialty stores, and emerging online retail channels.

Key Attractiveness of the Report

- 10 Years of Market Numbers

- Historical Data Starting from 2021 to 2024

- Base Year: 2024

- Forecast Data until 2031

- Key Performance Indicators Impacting the Market

- Major Upcoming Developments and Projects

Key Highlights of the Report:

- Singapore Construction Materials Market Outlook

- Market Size of Singapore Construction Materials Market

- Forecast of Singapore Construction Materials Market, 2031

- Historical Data and Forecast of Singapore Construction Materials Revenues & Volume for the Period 2021 - 2031

- Singapore Construction Materials Market Trend Evolution

- Singapore Construction Materials Market Drivers and Challenges

- Singapore Construction Materials Price Trends

- Singapore Construction Materials Porter's Five Forces

- Singapore Construction Materials Industry Life Cycle

- Historical Data and Forecast of Singapore Construction Materials Market Revenues & Volume By Product Type for the Period 2021 - 2031

- Historical Data and Forecast of Singapore Construction Materials Market Revenues & Volume By Construction Aggregates for the Period 2021 - 2031

- Historical Data and Forecast of Singapore Construction Materials Market Revenues & Volume By Concrete Bricks for the Period 2021 - 2031

- Historical Data and Forecast of Singapore Construction Materials Market Revenues & Volume By Cement for the Period 2021 - 2031

- Historical Data and Forecast of Singapore Construction Materials Market Revenues & Volume By Construction Metals for the Period 2021 - 2031

- Historical Data and Forecast of Singapore Construction Materials Market Revenues & Volume By Application for the Period 2021 - 2031

- Historical Data and Forecast of Singapore Construction Materials Market Revenues & Volume By Residential for the Period 2021 - 2031

- Historical Data and Forecast of Singapore Construction Materials Market Revenues & Volume By Commercial for the Period 2021 - 2031

- Historical Data and Forecast of Singapore Construction Materials Market Revenues & Volume By Industrial for the Period 2021 - 2031

- Singapore Construction Materials Import Export Trade Statistics

- Market Opportunity Assessment By Product Type

- Market Opportunity Assessment By Application

- Singapore Construction Materials Top Companies Market Share

- Singapore Construction Materials Competitive Benchmarking By Technical and Operational Parameters

- Singapore Construction Materials Company Profiles

- Singapore Construction Materials Key Strategic Recommendations

Market Covered

The report offers a comprehensive study of the subsequent market segments:

By Product Type

- Construction Aggregates

- Concrete Bricks

- Cement

- Construction Metals

By Application

- Residential

- Commercial

- Industrial

Singapore Construction Materials Market (2025-2031): FAQs

The Singapore Construction Materials Market is projected to grow at a CAGR of 5.6 during the forecast period.

Concrete dominates the market given pervasive use in high-rise, rail, port, and airport projects, supported by PPVC/DFMA and strict quality specifications.

Infrastructure Development leads due to continuous MRT expansion, Tuas Mega Port, airport works, and water projects that anchor bulk procurement.

Green Mark and Super Low Energy standards are lifting demand for low-e glass, low-carbon concrete mixes, insulation, and engineered wood solutions.

6Wresearch actively monitors the Singapore Construction Materials Market and publishes its comprehensive annual report, highlighting emerging trends, growth drivers, revenue analysis, and forecast outlook. Our insights help businesses to make data-backed strategic decisions with ongoing market dynamics. Our analysts track relevent industries related to the Singapore Construction Materials Market, allowing our clients with actionable intelligence and reliable forecasts tailored to emerging regional needs.

Yes, we provide customisation as per your requirements. To learn more, feel free to contact us on sales@6wresearch.com

| 1 Executive Summary |

| 2 Introduction |

| 2.1 Key Highlights of the Report |

| 2.2 Report Description |

| 2.3 Market Scope & Segmentation |

| 2.4 Research Methodology |

| 2.5 Assumptions |

| 3 Singapore Construction Materials Market Overview |

| 3.1 Singapore Country Macro Economic Indicators |

| 3.2 Singapore Construction Materials Market Revenues & Volume, 2021 & 2031F |

| 3.3 Singapore Construction Materials Market - Industry Life Cycle |

| 3.4 Singapore Construction Materials Market - Porter's Five Forces |

| 3.5 Singapore Construction Materials Market Revenues & Volume Share, By Product type, 2021 & 2031F |

| 3.6 Singapore Construction Materials Market Revenues & Volume Share, By Application, 2021 & 2031F |

| 4 Singapore Construction Materials Market Dynamics |

| 4.1 Impact Analysis |

| 4.2 Market Drivers |

| 4.3 Market Restraints |

| 5 Singapore Construction Materials Market Trends |

| 6 Singapore Construction Materials Market, By Types |

| 6.1 Singapore Construction Materials Market, By Product type |

| 6.1.1 Overview and Analysis |

| 6.1.2 Singapore Construction Materials Market Revenues & Volume, By Product type, 2021 - 2031F |

| 6.1.3 Singapore Construction Materials Market Revenues & Volume, By Construction aggregates, 2021 - 2031F |

| 6.1.4 Singapore Construction Materials Market Revenues & Volume, By Concrete bricks, 2021 - 2031F |

| 6.1.5 Singapore Construction Materials Market Revenues & Volume, By Cement, 2021 - 2031F |

| 6.1.6 Singapore Construction Materials Market Revenues & Volume, By Construction metals, 2021 - 2031F |

| 6.2 Singapore Construction Materials Market, By Application |

| 6.2.1 Overview and Analysis |

| 6.2.2 Singapore Construction Materials Market Revenues & Volume, By Residential, 2021 - 2031F |

| 6.2.3 Singapore Construction Materials Market Revenues & Volume, By Commercial, 2021 - 2031F |

| 6.2.4 Singapore Construction Materials Market Revenues & Volume, By Industrial, 2021 - 2031F |

| 7 Singapore Construction Materials Market Import-Export Trade Statistics |

| 7.1 Singapore Construction Materials Market Export to Major Countries |

| 7.2 Singapore Construction Materials Market Imports from Major Countries |

| 8 Singapore Construction Materials Market Key Performance Indicators |

| 9 Singapore Construction Materials Market - Opportunity Assessment |

| 9.1 Singapore Construction Materials Market Opportunity Assessment, By Product type, 2021 & 2031F |

| 9.2 Singapore Construction Materials Market Opportunity Assessment, By Application, 2021 & 2031F |

| 10 Singapore Construction Materials Market - Competitive Landscape |

| 10.1 Singapore Construction Materials Market Revenue Share, By Companies, 2024 |

| 10.2 Singapore Construction Materials Market Competitive Benchmarking, By Operating and Technical Parameters |

| 11 Company Profiles |

| 12 Recommendations |

| 13 Disclaimer |

Global Go To Market Strategy - 2030

Export potential enables firms to identify high-growth global markets with greater confidence by combining advanced trade intelligence with a structured quantitative methodology. The framework analyzes emerging demand trends and country-level import patterns while integrating macroeconomic and trade datasets such as GDP and population forecasts, bilateral import–export flows, tariff structures, elasticity differentials between developed and developing economies, geographic distance, and import demand projections. Using weighted trade values from 2020–2024 as the base period to project country-to-country export potential for 2030, these inputs are operationalized through calculated drivers such as gravity model parameters, tariff impact factors, and projected GDP per-capita growth. Through an analysis of hidden potentials, demand hotspots, and market conditions that are most favorable to success, this method enables firms to focus on target countries, maximize returns, and global expansion with data, backed by accuracy.

By factoring in the projected importer demand gap that is currently unmet and could be potential opportunity, it identifies the potential for the Exporter (Country) among 190 countries, against the general trade analysis, which identifies the biggest importer or exporter.

To discover high-growth global markets and optimize your business strategy:

Click Here

Pricing

- Single User License$ 1,995

- Department License$ 2,400

- Site License$ 3,120

- Global License$ 3,795

Leadership Perspectives from Industry Events

Search

Thought Leadership and Analyst Meet

Our Clients

6WResearch In News

- India Export Attractiveness Tracker 2026

- India Air Conditioner Market Set for Strong Rebound in 2026 After Weather-Led Correction and GST-Driven Recovery: 6Wresearch

- ADAS in India: How Automatic Emergency Braking, Blind Spot Detection & Driver Monitoring are Transforming Road Safety

- Doha a strategic location for EV manufacturing hub: IPA Qatar

- Demand for luxury TVs surging in the GCC, says Samsung

- Empowering Growth: The Thriving Journey of Bangladesh’s Cable Industry

Latest Reports

- Nicaragua RPG Gaming Market (2026-2032)

- New Zealand RPG Gaming Market (2026-2032)

- Netherlands RPG Gaming Market (2026-2032)

- Nauru RPG Gaming Market (2026-2032)

- Namibia RPG Gaming Market (2026-2032)

- Mozambique RPG Gaming Market (2026-2032)

- Montenegro RPG Gaming Market (2026-2032)

- Mongolia RPG Gaming Market (2026-2032)

- Monaco RPG Gaming Market (2026-2032)

- Micronesia RPG Gaming Market (2026-2032)

Industry Events and Analyst Meet

EV India Expo 2026

HIMTEX 2026

India Refining Summit 2026

India EV Show 2026

EV tech India Expo 2026

Whitepaper

- Middle East & Africa Commercial Security Market Click here to view more.

- Middle East & Africa Fire Safety Systems & Equipment Market Click here to view more.

- GCC Drone Market Click here to view more.

- Middle East Lighting Fixture Market Click here to view more.

- GCC Physical & Perimeter Security Market Click here to view more.