Singapore Semiconductor Market (2026-2032) | Share, Industry, Value, Size, Growth, Companies, Outlook, Analysis, Forecast, Revenue & Trends

Market Forecast By Components (Memory Devices, Logic Devices, Analog IC, MPU, Discrete Power Devices, MCU, Sensors, Others), By Application (Networking & Communications, Data Processing, Industrial, Consumer Electronics, Automotive, Government) And Competitive Landscape

| Product Code: ETC031367 | Publication Date: Jul 2023 | Updated Date: Apr 2026 | Product Type: Report | |

| Publisher: 6Wresearch | Author: Ravi Bhandari | No. of Pages: 70 | No. of Figures: 35 | No. of Tables: 5 |

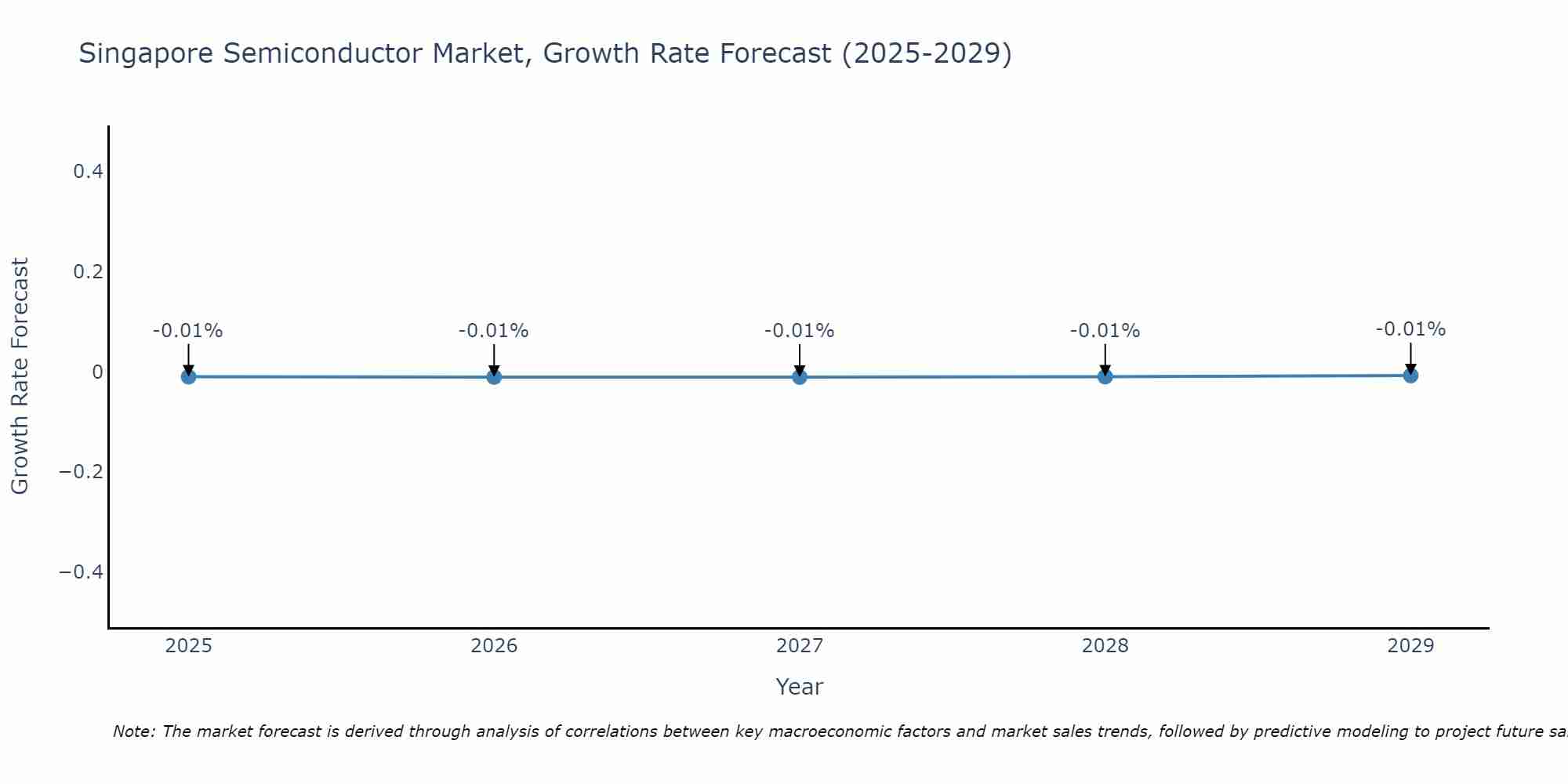

Singapore Semiconductor Market Size Growth Rate

The Singapore Semiconductor Market is projected to witness mixed growth rate patterns during 2025 to 2029. Commencing at -0.01% in 2025, growth builds up to -0.01% by 2029.

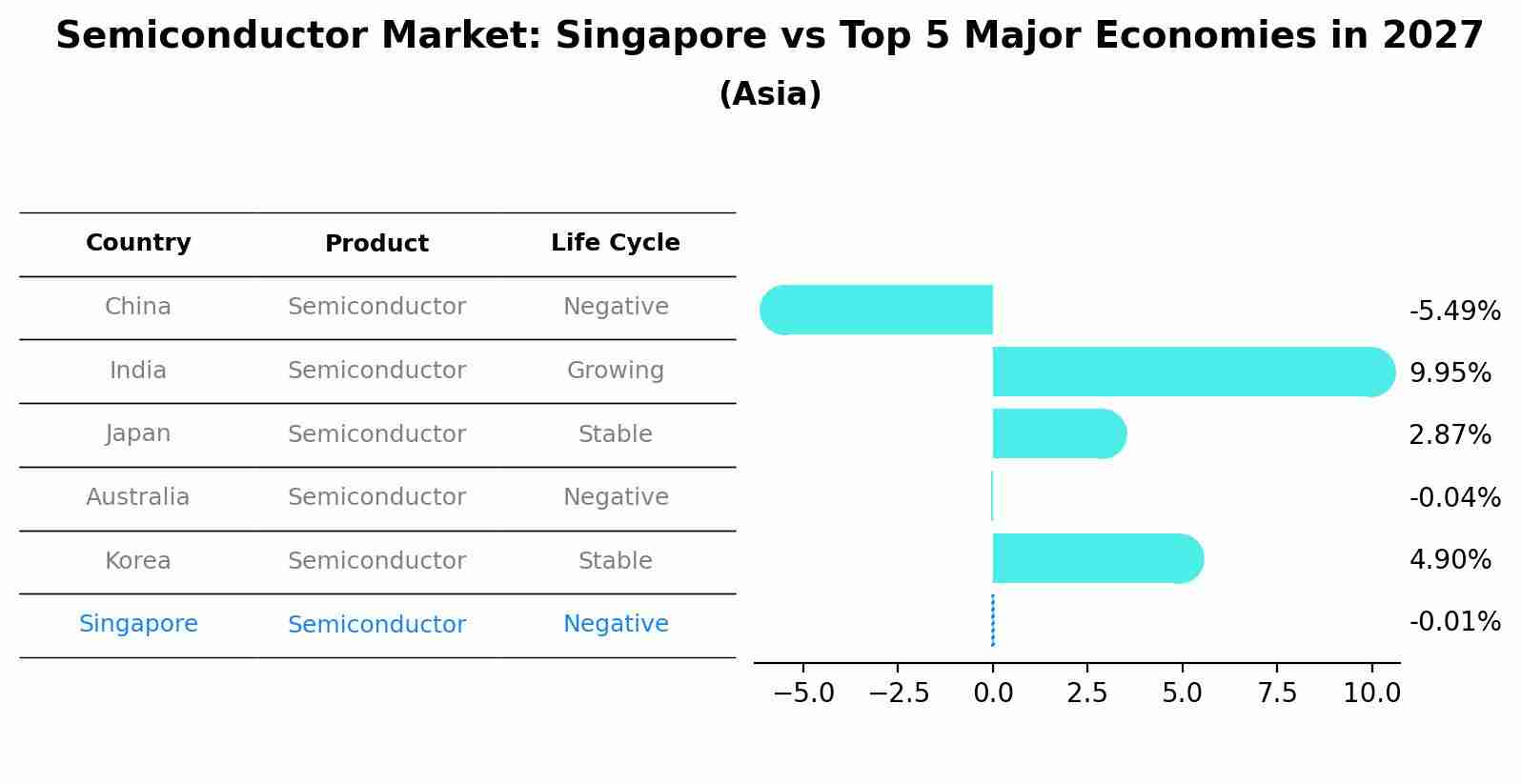

Semiconductor Market: Singapore vs Top 5 Major Economies in 2027 (Asia)

In the Asia region, the Semiconductor market in Singapore is projected to expand at a negative growth rate of -0.01% by 2027. The largest economy is China, followed by India, Japan, Australia and South Korea.

Singapore Semiconductor Market Growth Rate

According to 6Wresearch internal database and industry insights, the Singapore Semiconductor Market is projected to grow at a compound annual growth rate (CAGR) of 5.8% during the forecast period (2026-2032).

Topics Covered in the Singapore Semiconductor Market Report

The Singapore Semiconductor Market report thoroughly covers the market By Components and By Applications. The market report provides an unbiased and detailed analysis of ongoing market trends, opportunities/high growth areas, and market drivers, which help stakeholders devise and align their market strategies according to the current and future market dynamics.

Singapore Semiconductor Market Highlights

| Report Name | Singapore Semiconductor Market |

| Forecast period | 2026-2032 |

| CAGR | 5.8% |

| Growing Sector | Data Processing & Automotive |

Singapore Semiconductor Market Synopsis

Singapore Semiconductor Market Growth can be attributed to certain factors. First of all, Singapore’s geography and well-established infrastructure make it a centre of excellence for the semiconductor industry, allowing the country to boast a thriving ecosystem that promotes research, development, and production. Second, there is a growing trend in the world towards the consumption of consumer electronics that incorporates developments in IoT, AI, and cloud technologies.

Evaluation of Growth Drivers in the Singapore Semiconductor Market

Below mentioned are some prominent drivers and their influence on the market dynamics:

| Drivers | Primary Segments Affected | Why it Matters (Evidence) |

| Rise in IoT Device Demand | Memory Devices, Sensors | IoT adoption drives the demand for small, low-power semiconductor solutions. |

| Government Support for Semiconductor Manufacturing | All Types | Policies and incentives boost local manufacturing and R&D investments. |

| Increased Demand in Automotive Industry | Logic Devices, MCU, Sensors | Electrification and autonomous vehicles fuel the need for advanced semiconductor components. |

| Expansion of Data Centers & Cloud Infrastructure | Memory Devices, Logic Devices | Growing cloud infrastructure increases the demand for high-performance semiconductors. |

| 5G Deployment | All Types | The rollout of 5G accelerates the need for high-speed semiconductor devices. |

The Singapore Semiconductor Market is expected to grow at the CAGR of 5.8% during the forecast period of 2026-2032. Government support in the form of tax breaks, grants, and infrastructure development under programs like the Research, Innovation, and Enterprise (RIE) framework encourages investment and innovation in the industry. In addition, the explosive growth of cutting-edge technologies like IoT, AI, and cloud computing enhances demand for semiconductors, making Singapore a global hub for the same. The emphasis of the country to create highly qualified professionals and collaborate among corporates and research institutions maintains consistent innovation and productivity within the sector.

Evaluation of Restraints in the Singapore Semiconductor Market

Below mentioned are some major restraints and their influence on the market dynamics:

| Restraints | Primary Segments Affected | What This Means (Evidence) |

| Chip Supply Chain Disruptions | All Types | Geopolitical tensions and supply chain interruptions affect component availability. |

| High Manufacturing Costs | All Types | Advanced manufacturing processes and materials raise production costs. |

| Shortage of Skilled Labor | All Types | Demand for highly specialized semiconductor engineers exceeds supply. |

| Dependence on Imported Raw Materials | Memory Devices, Sensors | Raw material import restrictions impact the ability to scale production. |

| Increasing Environmental Regulations | All Types | Stringent regulations increase compliance costs for manufacturing and disposal. |

Singapore Semiconductor Market Challenges

However, despite having all these strengths, there are certain difficulties faced by the semiconductor market in Singapore. Some of these include the worldwide shortage of semiconductors, labor, and other related costs that make it even more difficult for firms to become competitive across the globe. Apart from that, this business is greatly impacted by the rapid technological advancement that requires constant upgrading to keep up with the changes.

Singapore Semiconductor Market Trends

Key trends evaluating the landscape of the Singapore Semiconductor Market are:

- Adoption of Advanced Packaging Technologies: The market is increasingly adopting advanced semiconductor packaging technologies to boost performance and integration in smaller devices.

- Focus on Automotive Semiconductors: With the rise of electric and autonomous vehicles, the automotive sector is becoming a key driver for semiconductor innovations.

- Development of Devices Using 5G: The deployment of 5G technology is prompting the creation of more advanced and efficient semiconductor solutions.

- AI for Semiconductor Fabrication: The application of artificial intelligence in optimizing semiconductor design and fabrication is becoming popular.

Investment Opportunities in the Singapore Semiconductor Market

Some of the most promising investment options in the Singapore Semiconductor Market are:

- Investing in New Semiconductor Production Plants: Considering the high demand, investments in new production plants would cater to the requirement for semiconductor elements.

- Investments in 5G Network Components: Investments in components that support 5G networks will be highly profitable as the technology expands worldwide.

- Research in Automotive Semiconductors: Research in automotive semiconductors is an important investment option to take advantage of the rise in electric vehicles.

- Investments in Semiconductor Recycling Plants: The establishment of semiconductor recycling plants is also a viable investment option due to increasing environmental concerns.

Top 5 Leading Players in the Singapore Semiconductor Market

Some leading players operating in the Singapore Semiconductor Market include:

Intel Corporation

| Company Name | Intel Corporation |

| Established Year | 1968 |

| Headquarters | Santa Clara, California, USA |

| Official Website | Click Here |

Intel is a global leader in semiconductor design and manufacturing, providing microprocessors and system-on-chip products for a wide range of applications.

Samsung Electronics Co., Ltd.

| Company Name | Samsung Electronics Co., Ltd. |

| Established Year | 1938 |

| Headquarters | Seoul, South Korea |

| Official Website | Click Here |

Samsung specializes in semiconductor manufacturing, including memory devices and processors for consumer electronics, mobile devices, and automotive industries.

Taiwan Semiconductor Manufacturing Company (TSMC)

| Company Name | Taiwan Semiconductor Manufacturing Company (TSMC) |

| Established Year | 1987 |

| Headquarters | Hsinchu, Taiwan |

| Official Website | Click Here |

TSMC is the world’s largest semiconductor foundry, offering advanced technology for chips used in electronics, automotive, and industrial applications.

Qualcomm Technologies, Inc.

| Company Name | Qualcomm Technologies, Inc. |

| Established Year | 1985 |

| Headquarters | San Diego, California, USA |

| Official Website | Click Here |

Qualcomm designs and manufactures semiconductors for wireless telecommunications, including 5G-enabled devices and mobile processors.

STMicroelectronics

| Company Name | STMicroelectronics |

| Established Year | 1987 |

| Headquarters | Geneva, Switzerland |

| Official Website | Click Here |

STMicroelectronics manufactures semiconductor devices used in automotive, industrial, and consumer electronics, with a strong focus on energy-efficient solutions.

Government Regulations Introduced in the Singapore Semiconductor Market

According to Singapore Government Data, The government has an important role in forming a regulatory environment within the semiconductor industry, as well as ensuring that all companies meet international regulations. This is because the EDB and Enterprise Singapore have introduced measures in the form of granting subsidies to the industry players, tax rebates, and incentives to promote innovations. The environmental laws are not left out as they include strict provisions concerning waste disposal and energy conservation in support of the green policy in Singapore.

Future Insights of the Singapore Semiconductor Market

The future of Singapore semiconductor industry looks exceptionally promising, driven by advancements in technologies like artificial intelligence (AI), 5G networks, autonomous vehicles, and Internet of Things (IoT). These new technologies are likely to grow the world's demand for semiconductors, making Singapore a key part of the supply chain. Ongoing government investment in R&D and innovation-driving initiatives will help the country keep up with changing industry demands.

Market Segmentation Analysis

The report offers a comprehensive study of the subsequent market segments and their leading categories:

Memory devices to Dominate the Market- By Components

According to Vasudha, Senior Research Analyst, 6Wresearch, Among the components, memory devices are dominating the Singapore semiconductor market share. The rising demand for high-capacity storage solutions in data-intensive industries, such as cloud computing and data centres, is driving the growth of this segment. Additionally, the proliferation of advanced smartphones, gaming consoles, and other consumer electronics further contributes to the growing dominance of memory devices, particularly DRAM and NAND flash technologies.

Networking and communications to Dominate the Market- By Application

Among the application markets, networking and communications have become the most prominent. The rapid adoption of the fifth generation technology, along with the growth in broadband networks and Internet of Things (IoT) uses, has created a lot of semiconductor demands in this category. As more and more users need fast internet access and connected gadgets, this area will remain at the forefront of the industry.

Key Attractiveness of the Report

- 10 Years of Market Numbers.

- Historical Data Starting from 2022 to 2025.

- Base Year: 2025.

- Forecast Data until 2032.

- Key Performance Indicators Impacting the Market.

- Major Upcoming Developments and Projects.

Key Highlights of the Report:

- Singapore Semiconductor Market Outlook

- Market Size of Singapore Semiconductor Market, 2025

- Forecast of Singapore Semiconductor Market, 2032

- Historical Data and Forecast of Singapore Semiconductor Revenues & Volume for the Period 2022-2032

- Singapore Semiconductor Market Trend Evolution

- Singapore Semiconductor Market Drivers and Challenges

- Singapore Semiconductor Price Trends

- Singapore Semiconductor Porter's Five Forces

- Singapore Semiconductor Industry Life Cycle

- Historical Data and Forecast of Singapore Semiconductor Market Revenues & Volume By Components for the Period 2022-2032

- Historical Data and Forecast of Singapore Semiconductor Market Revenues & Volume By Memory Devices for the Period 2022-2032

- Historical Data and Forecast of Singapore Semiconductor Market Revenues & Volume By Logic Devices for the Period 2022-2032

- Historical Data and Forecast of Singapore Semiconductor Market Revenues & Volume By Analog IC for the Period 2022-2032

- Historical Data and Forecast of Singapore Semiconductor Market Revenues & Volume By MPU for the Period 2022-2032

- Historical Data and Forecast of Singapore Semiconductor Market Revenues & Volume By Discrete Power Devices for the Period 2022-2032

- Historical Data and Forecast of Singapore Semiconductor Market Revenues & Volume By MCU for the Period 2022-2032

- Historical Data and Forecast of Singapore Semiconductor Market Revenues & Volume By Sensors for the Period 2022-2032

- Historical Data and Forecast of Singapore Memory Devices Semiconductor Market Revenues & Volume By Others for the Period 2022-2032

- Historical Data and Forecast of Singapore Semiconductor Market Revenues & Volume By Application for the Period 2022-2032

- Historical Data and Forecast of Singapore Semiconductor Market Revenues & Volume By Networking & Communications for the Period 2022-2032

- Historical Data and Forecast of Singapore Semiconductor Market Revenues & Volume By Data Processing for the Period 2022-2032

- Historical Data and Forecast of Singapore Semiconductor Market Revenues & Volume By Industrial for the Period 2022-2032

- Historical Data and Forecast of Singapore Semiconductor Market Revenues & Volume By Consumer Electronics for the Period 2022-2032

- Historical Data and Forecast of Singapore Semiconductor Market Revenues & Volume By Automotive for the Period 2022-2032

- Historical Data and Forecast of Singapore Semiconductor Market Revenues & Volume By Government for the Period 2022-2032

- Singapore Semiconductor Import Export Trade Statistics

- Market Opportunity Assessment By Components

- Market Opportunity Assessment By Application

- Singapore Semiconductor Top Companies Market Share

- Singapore Semiconductor Competitive Benchmarking By Technical and Operational Parameters

- Singapore Semiconductor Company Profiles

- Singapore Semiconductor Key Strategic Recommendations

Markets Covered

The report provides a detailed analysis of the following market segments

By Components

- Memory Devices

- Logic Devices

- Analog IC

- MPU

- Discrete Power Devices

- MCU

- Sensors

- Others

By Application

- Networking & Communications

- Data Processing

- Industrial

- Consumer Electronics

- Automotive

- Government

Singapore Semiconductor Market (2026-2032): FAQs

The Singapore Semiconductor Market is projected to grow at a CAGR of 5.8% between 2026-2032.

Growth is driven by increasing demand for data centers, automotive electronics, and government initiatives for semiconductor manufacturing.

Some possible barriers could be supply chain disruptions, expensive manufacturing, and unavailability of skilled manpower.

One such emerging trend in Singapore Semiconductors would include innovations in 5G technology and advanced packaging.

6Wresearch actively monitors the Singapore Semiconductor Market and publishes its comprehensive annual report, highlighting emerging trends, growth drivers, revenue analysis, and forecast outlook. Our insights help businesses to make data-backed strategic decisions with ongoing market dynamics. Our analysts track relevent industries related to the Singapore Semiconductor Market, allowing our clients with actionable intelligence and reliable forecasts tailored to emerging regional needs.

Yes, we provide customisation as per your requirements. To learn more, feel free to contact us on sales@6wresearch.com

| 1 Executive Summary |

| 2 Introduction |

| 2.1 Key Highlights of the Report |

| 2.2 Report Description |

| 2.3 Market Scope & Segmentation |

| 2.4 Research Methodology |

| 2.5 Assumptions |

| 3 Singapore Semiconductor Market Overview |

| 3.1 Singapore Country Macro Economic Indicators |

| 3.2 Singapore Semiconductor Market Revenues & Volume, 2022 & 2032F |

| 3.3 Singapore Semiconductor Market - Industry Life Cycle |

| 3.4 Singapore Semiconductor Market - Porter's Five Forces |

| 3.5 Singapore Semiconductor Market Revenues & Volume Share, By Components, 2022 & 2032F |

| 3.6 Singapore Semiconductor Market Revenues & Volume Share, By Application, 2022 & 2032F |

| 4 Singapore Semiconductor Market Dynamics |

| 4.1 Impact Analysis |

| 4.2 Market Drivers |

| 4.3 Market Restraints |

| 5 Singapore Semiconductor Market Trends |

| 6 Singapore Semiconductor Market, By Types |

| 6.1 Singapore Semiconductor Market, By Components |

| 6.1.1 Overview and Analysis |

| 6.1.2 Singapore Semiconductor Market Revenues & Volume, By Components, 2022-2032F |

| 6.1.3 Singapore Semiconductor Market Revenues & Volume, By Memory Devices, 2022-2032F |

| 6.1.4 Singapore Semiconductor Market Revenues & Volume, By Logic Devices, 2022-2032F |

| 6.1.5 Singapore Semiconductor Market Revenues & Volume, By Analog IC, 2022-2032F |

| 6.1.6 Singapore Semiconductor Market Revenues & Volume, By MPU, 2022-2032F |

| 6.1.7 Singapore Semiconductor Market Revenues & Volume, By Discrete Power Devices, 2022-2032F |

| 6.1.8 Singapore Semiconductor Market Revenues & Volume, By MCU, 2022-2032F |

| 6.1.9 Singapore Semiconductor Market Revenues & Volume, By Others, 2022-2032F |

| 6.1.10 Singapore Semiconductor Market Revenues & Volume, By Others, 2022-2032F |

| 6.2 Singapore Semiconductor Market, By Application |

| 6.2.1 Overview and Analysis |

| 6.2.2 Singapore Semiconductor Market Revenues & Volume, By Networking & Communications, 2022-2032F |

| 6.2.3 Singapore Semiconductor Market Revenues & Volume, By Data Processing, 2022-2032F |

| 6.2.4 Singapore Semiconductor Market Revenues & Volume, By Industrial, 2022-2032F |

| 6.2.5 Singapore Semiconductor Market Revenues & Volume, By Consumer Electronics, 2022-2032F |

| 6.2.6 Singapore Semiconductor Market Revenues & Volume, By Automotive, 2022-2032F |

| 6.2.7 Singapore Semiconductor Market Revenues & Volume, By Government, 2022-2032F |

| 7 Singapore Semiconductor Market Import-Export Trade Statistics |

| 7.1 Singapore Semiconductor Market Export to Major Countries |

| 7.2 Singapore Semiconductor Market Imports from Major Countries |

| 8 Singapore Semiconductor Market Key Performance Indicators |

| 9 Singapore Semiconductor Market - Opportunity Assessment |

| 9.1 Singapore Semiconductor Market Opportunity Assessment, By Components, 2022 & 2032F |

| 9.2 Singapore Semiconductor Market Opportunity Assessment, By Application, 2022 & 2032F |

| 10 Singapore Semiconductor Market - Competitive Landscape |

| 10.1 Singapore Semiconductor Market Revenue Share, By Companies, 2025 |

| 10.2 Singapore Semiconductor Market Competitive Benchmarking, By Operating and Technical Parameters |

| 11 Company Profiles |

| 12 Recommendations |

| 13 Disclaimer |

Global Go To Market Strategy - 2030

Export potential enables firms to identify high-growth global markets with greater confidence by combining advanced trade intelligence with a structured quantitative methodology. The framework analyzes emerging demand trends and country-level import patterns while integrating macroeconomic and trade datasets such as GDP and population forecasts, bilateral import–export flows, tariff structures, elasticity differentials between developed and developing economies, geographic distance, and import demand projections. Using weighted trade values from 2020–2024 as the base period to project country-to-country export potential for 2030, these inputs are operationalized through calculated drivers such as gravity model parameters, tariff impact factors, and projected GDP per-capita growth. Through an analysis of hidden potentials, demand hotspots, and market conditions that are most favorable to success, this method enables firms to focus on target countries, maximize returns, and global expansion with data, backed by accuracy.

By factoring in the projected importer demand gap that is currently unmet and could be potential opportunity, it identifies the potential for the Exporter (Country) among 190 countries, against the general trade analysis, which identifies the biggest importer or exporter.

To discover high-growth global markets and optimize your business strategy:

Click Here

Pricing

- Single User License$ 1,995

- Department License$ 2,400

- Site License$ 3,120

- Global License$ 3,795

Leadership Perspectives from Industry Events

Search

Thought Leadership and Analyst Meet

Our Clients

6WResearch In News

- Doha a strategic location for EV manufacturing hub: IPA Qatar

- Demand for luxury TVs surging in the GCC, says Samsung

- Empowering Growth: The Thriving Journey of Bangladesh’s Cable Industry

- Demand for luxury TVs surging in the GCC, says Samsung

- Video call with a traditional healer? Once unthinkable, it’s now common in South Africa

- Intelligent Buildings To Smooth GCC’s Path To Net Zero

Latest Reports

- New Zealand Aseptic Manufacturing Market (2026-2032)

- Netherlands Aseptic Manufacturing Market (2026-2032)

- Nauru Aseptic Manufacturing Market (2026-2032)

- Namibia Aseptic Manufacturing Market (2026-2032)

- Mozambique Aseptic Manufacturing Market (2026-2032)

- Montenegro Aseptic Manufacturing Market (2026-2032)

- Mongolia Aseptic Manufacturing Market (2026-2032)

- Monaco Aseptic Manufacturing Market (2026-2032)

- Micronesia Aseptic Manufacturing Market (2026-2032)

- Mauritius Aseptic Manufacturing Market (2026-2032)

Industry Events and Analyst Meet

HIMTEX 2026

India Refining Summit 2026

India EV Show 2026

EV tech India Expo 2026

Auto Tech Asia 2026

Whitepaper

- Middle East & Africa Commercial Security Market Click here to view more.

- Middle East & Africa Fire Safety Systems & Equipment Market Click here to view more.

- GCC Drone Market Click here to view more.

- Middle East Lighting Fixture Market Click here to view more.

- GCC Physical & Perimeter Security Market Click here to view more.