Spain Carbon Market (2026-2032) | Share, Value, Companies, Analysis, Industry, Outlook, Trends, Forecast, Growth, Size & Revenue

Market Forecast By Product Types (Amorphous Carbon, Graphite, Diamond), By Applications (Automotive, Construction, Engineering Industries, Aerospace, Others) And Competitive Landscape

| Product Code: ETC004156 | Publication Date: Sep 2020 | Updated Date: Mar 2026 | Product Type: Report | |

| Publisher: 6Wresearch | Author: Ravi Bhandari | No. of Pages: 70 | No. of Figures: 35 | No. of Tables: 5 |

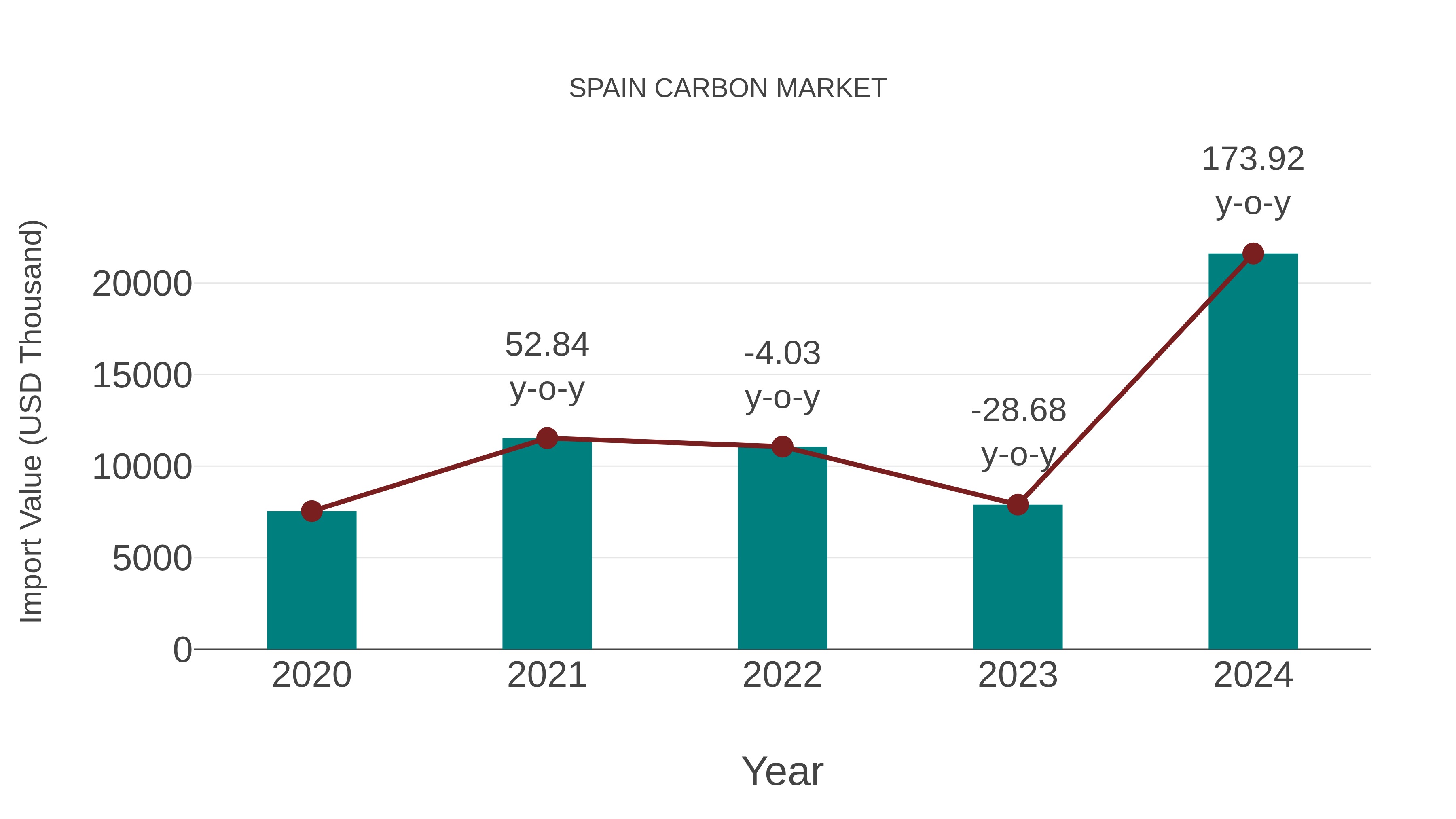

Spain Carbon Market: Import Trend Analysis

In 2024, Spain`s carbon market saw a notable increase in imports. This trend was driven by rising demand for carbon-related products and services. The surge in imports reflects Spain`s growing reliance on international markets to meet its carbon needs.

Spain Carbon Market Highlights

| Report Name | Spain Carbon Market |

| Forecast period | 2025-2031 |

| CAGR | 11.12% |

| Growing Sector | Automotive |

Topics Covered in the Spain Carbon Market Report

Spain Carbon Market report thoroughly covers the market by product types and by Applications. The market report provides an unbiased and detailed analysis of the ongoing market trends, opportunities/high growth areas, and market drivers, which would help the stakeholders to devise and align their market strategies according to the current and future market dynamics.

Spain Carbon Market Synopsis

Spain carbon market is witnessing tremendous growth, led by stringent European Union policies, carbon pricing instruments, and sustainability obligations. The adoption of emissions trading systems (ETS) and incentives for renewable energy projects are promoting carbon credit trading and corporate engagement. Spain's drive towards denationalization, along with its renewable energy shift, is opening up opportunities for companies to invest in carbon offsetting projects. But regulatory complexity and market uncertainty are challenges, necessitating ongoing policy refinement to deliver a clear, effective, and resilient carbon market that sustains long-term goals of sustainability.

According to 6Wresearch, the Spain Carbon Market is projected to grow at CAGR of 11.12% during the forecast period 2025-2031. Spain Carbon Market Growth is expanding due to stringent regulations, carbon trading advancements, and sustainability investments. driven by rigorous European Union regulations, carbon pricing measures, and Spain's aim to become climate neutral. In this case, the participation of the country in the EU Emissions Trading System (EU ETS) is becoming a key driver in the emission of greenhouse gases by levying charges on carbon emissions and encouraging firms to adopt cleaner technology.

Further, incentives for investing in renewable energies, energy efficiency, and trading in carbon credits under government policy are inducing investment in sustainable technologies. Growing deployments of CCUS technologies and increased recognition of the importance of sustainability promises made by firms, also help promote growth in the market. However, there can be several challenges for growth in the market. Regulatory risks, price volatility of carbon credits, and the complexity of compliance regimes are obstacles to industries that must transition to low-carbon operations.

Furthermore, sophisticated monitoring and reporting infrastructure must be put in place to provide market transparency and prevent market manipulation. Economic constraints, especially for small and medium-sized enterprises (SMEs), can discourage widespread adoption of carbon reduction activities. However, Spain's pioneering move to bring policy into conformity with global climate goals and constantly refining its carbon market system is sure to make markets more effective. With the demand for carbon credits growing and sustainability-driven investments gaining prominence, the Spain carbon market will remain at the forefront of European and global denationalization efforts.

Spain Carbon Market Trends

Spain carbon market is facing radical shifts, driven by business sustainability initiatives, regulatory regimes, and technological change. The nation's membership of the EU Emissions Trading System (EU ETS) continues to reshape market trends, compelling sectors to adopt greener technologies and smaller carbon footprints. The expansion of sustainable carbon credit trading and offset programs is further encouraging companies to invest in cleaner ventures, such as energy efficiency, renewable energy, and carbon capture technology.

The primary trend is the growing uptake of carbon pricing measures that encourage firms to decrease emissions as well as trigger green investments. In addition, the wider application of voluntary carbon markets enables businesses to make emissions offset over and above obligatory targets. Innovative progress in CCUS and digital platforms for emission measurement is improving transparency and enforcement ability. Nevertheless, price volatility and regulation issues remain an issue. Despite all these difficulties, Spain's commitment to achieving net-zero emissions will continue to drive carbon market growth and innovation.

Investments Opportunities in the Spain Carbon Market

Spain carbon Industry presents increasing investment opportunities, driven by regulation-facilitated incentives, carbon pricing, and sustainability requirements. The government's participation in the EU Emissions Trading System (EU ETS) and pro-carbon credit trading policies have created a supportive environment for investments in renewable energy, energy efficiency, and carbon capture technologies.

The growing adoption of carbon offsetting schemes has attracted local and foreign investors who want to invest in emission reduction projects and accrue financial returns. Investments in green hydrogen, solar, and wind projects are gaining traction as Spain transitions toward becoming a net-zero country. Voluntary carbon markets are also opening new doors for firms to sell carbon credits and increase their sustainability portfolios. However, some problems, such as uncertainty in market price and regulatory complexity, continue to exist. Despite these problems, the transition to a low-carbon economy, along with government-backed incentives and private sector investment, will remain a key driver for long-term investment growth in the Spain carbon market.

Leading Players in the Spain Carbon Market

Spain carbon market is backed by prominent players that are involved in emissions reduction, carbon credit trade, and renewable energy projects. Iberdrola, one of the world's top multinational electric utilities, is the driving force in decarbonization efforts, with a significant investment in renewable energy schemes and carbon-neutral technologies. Endesa, another prominent energy player, is heavily involved in emission offset schemes and expanding its dependence on renewable energy sources in order to comply with Spain's carbon neutrality targets.

Moreover, Repsol, an international energy business, has pledged to achieve net-zero emissions by 2031, with emphasis on carbon capture, storage technologies, and other alternative fuels in order to decrease its carbon footprint. Acciona, a company specializing in infrastructure and renewable energies, is making a major contribution through wind power and solar power projects, reducing overall emissions.

The market is also supported by financial institutions and sustainability-oriented companies investing in carbon offset schemes. As the rules get tighter and demand for sustainability increases, these companies will be pivotal in influencing Spain's move towards a low-carbon economy.

Government Regulations

Spain government has put in place extensive regulatory frameworks to propel the development of the carbon market and facilitate emissions reduction. Spain is an active member of the European Union Emissions Trading System (EU ETS), which imposes emission limits on industries and promotes carbon trading to achieve reduction levels. The government has also launched national policies and incentives to boost the shift to a low-carbon economy, such as subsidies for renewable energy, carbon pricing schemes, and emissions reduction requirements.

The Integrated National Energy and Climate Plan (PNIEC) defines Spain 2031 carbon neutrality pledge through the growth of renewable energy, energy efficiency, and carbon capture technologies. The government further promotes the establishment of voluntary carbon markets, which enable companies to buy and sell credits and invest in emission-reducing projects. Yet, policy uncertainties and compliance costs are still issues of concern for market players. To this end, Spain continues to enhance its policies so that it has a transparent, efficient, and well-regulated carbon market that reconciles economic growth with environmental sustainability.

Future Insights of the Spain Carbon Market

Spain Carbon Market is likely to witness significant growth based on improved regulatory environments, more corporate sustainability pledges, and innovations in carbon trading regimes. Spain's membership in the EU Emissions Trading System (EU ETS) will remain key to market growth, motivating companies to invest in carbon offset projects, renewable energy, and emission reduction measures.

Future expansion will also be shaped by Spain's Integrated National Energy and Climate Plan (PNIEC), which is aimed at reaching carbon neutrality by 2050. Voluntary carbon market development will likely attract both foreign and local investors, further building the market's infrastructure. Technology development in carbon capture, utilization, and storage (CCUS) will also help in emission reductions. Nonetheless, economic constraints, market volatility, and regulatory uncertainties can be challenging. Nevertheless, financial incentives, policy refinements, and investment based on sustainability will consolidate Spain's position as a leader in the global shift to a low-carbon economy.

Market Segmentation Analysis

The Report offers a comprehensive study of the subsequent market segments and their leading categories.

Graphite to Dominate the Market- By Product Types

Graphite is expected to dominate the market among various carbon-based product categories due to its widespread applications across multiple industries. Spain Carbon Market share is rising, driven by regulatory frameworks, carbon credit trading, and increasing sustainability initiatives. Graphite is highly valued for its superior thermal and electrical conductivity, making it essential for energy storage, battery manufacturing, and high-performance industrial applications.

Automotive to Dominate the Market -By Applications

According to Kapil, Senior Research Analyst, 6Wresearch, In the Spain Carbon Market, the automotive sector is projected to Grow among various application categories due to the increasing demand for lightweight, high-performance materials that enhance fuel efficiency and reduce carbon emissions.

Key Attractiveness of the Report

- 10 Years of Market Numbers.

- Historical Data Starting from 2021 to 2024.

- Base Year: 2024

- Forecast Data until 2031.

- Key Performance Indicators Impacting the market.

- Major Upcoming Developments and Projects.

Key Highlights of the Report:

- Spain Carbon Market Overview

- Spain Carbon Market Outlook

- Market Size of Spain Carbon Market, 2025

- Forecast of Spain Carbon Market, 2032

- Historical Data and Forecast of Spain Carbon Revenues & Volume for the Period 2022 - 2032F

- Spain Carbon Market Trend Evolution

- Spain Carbon Market Drivers and Challenges

- Spain Carbon Price Trends

- Spain Carbon Porter's Five Forces

- Spain Carbon Industry Life Cycle

- Historical Data and Forecast of Spain Carbon Market Revenues & Volume By Product Types for the Period 2022 - 2032F

- Historical Data and Forecast of Spain Carbon Market Revenues & Volume By Amorphous Carbon for the Period 2022 - 2032F

- Historical Data and Forecast of Spain Carbon Market Revenues & Volume By Graphite for the Period 2022 - 2032F

- Historical Data and Forecast of Spain Carbon Market Revenues & Volume By Diamond for the Period 2022 - 2032F

- Historical Data and Forecast of Spain Carbon Market Revenues & Volume By Applications for the Period 2022 - 2032F

- Historical Data and Forecast of Spain Carbon Market Revenues & Volume By Automotive for the Period 2022 - 2032F

- Historical Data and Forecast of Spain Carbon Market Revenues & Volume By Construction for the Period 2022 - 2032F

- Historical Data and Forecast of Spain Carbon Market Revenues & Volume By Engineering Industries for the Period 2022 - 2032F

- Historical Data and Forecast of Spain Carbon Market Revenues & Volume By Aerospace for the Period 2022 - 2032F

- Historical Data and Forecast of Spain Carbon Market Revenues & Volume By Others for the Period 2022 - 2032F

- Spain Carbon Import Export Trade Statistics

- Market Opportunity Assessment By Product Types

- Market Opportunity Assessment By Applications

- Spain Carbon Top Companies Market Share

- Spain Carbon Competitive Benchmarking By Technical and Operational Parameters

- Spain Carbon Company Profiles

- Spain Carbon Key Strategic Recommendations

Market Segmentation Analysis

The Report offers a comprehensive study of the subsequent market segments and their leading categories.

By Product Types

- Amorphous Carbon

- Graphite

- Diamond

By Applications

- Automotive

- Construction

- Engineering Industries

- Aerospace

- Others

Spain Carbon Market (2026-2032): FAQs

The market is expanding due to EU ETS regulations, corporate sustainability initiatives, and investments in renewable energy projects.

Challenges include regulatory uncertainties, economic constraints, and the need for stronger private-sector participation in carbon offset initiatives.

The market is expected to grow with enhanced carbon trading mechanisms, investment in carbon capture technologies, and stricter emission policies.

The government promotes the market through EU ETS participation, the PNIEC strategy, carbon pricing mechanisms, and incentives for emissions reduction projects.

6Wresearch actively monitors the Spain Carbon Market and publishes its comprehensive annual report, highlighting emerging trends, growth drivers, revenue analysis, and forecast outlook. Our insights help businesses to make data-backed strategic decisions with ongoing market dynamics. Our analysts track relevent industries related to the Spain Carbon Market, allowing our clients with actionable intelligence and reliable forecasts tailored to emerging regional needs.

Yes, we provide customisation as per your requirements. To learn more, feel free to contact us on sales@6wresearch.com

| Table of Contents |

| 1. Executive Summary |

| 2. Introduction |

| 2.1. Key Highlights of the Report |

| 2.2. Report Description |

| 2.3. Market Scope & Segmentation |

| 2.4. Research Methodology |

| 2.5. Assumptions |

| 3. Spain Carbon Market Overview |

| 3.1. Spain Country Macro Economic Indicators |

| 3.2. Spain Carbon Market Revenues & Volume, 2022 & 2032F |

| 3.3. Spain Carbon Market - Industry Life Cycle |

| 3.4. Spain Carbon Market - Porter's Five Forces |

| 3.5. Spain Carbon Market Revenues & Volume Share, By Product Types, 2022 & 2032F |

| 3.6. Spain Carbon Market Revenues & Volume Share, By Applications, 2022 & 2032F |

| 4. Spain Carbon Market Dynamics |

| 4.1. Impact Analysis |

| 4.2. Market Drivers |

| 4.2.1 Increasing government regulations and policies promoting carbon emissions reduction |

| 4.2.2 Growing awareness and concern about climate change among consumers and businesses |

| 4.2.3 Technological advancements in carbon capture and storage solutions |

| 4.3. Market Restraints |

| 4.3.1 Volatility in carbon prices and market uncertainty |

| 4.3.2 Lack of standardized regulations across different regions |

| 4.3.3 Competition from alternative energy sources |

| 5. Spain Carbon Market Trends |

| 6. Spain Carbon Market, By Types |

| 6.1. Spain Carbon Market, By Product Types |

| 6.1.1 Overview and Analysis |

| 6.1.2. Spain Carbon Market Revenues & Volume, By Product Types, 2022-2032F |

| 6.1.3. Spain Carbon Market Revenues & Volume, By Amorphous Carbon, 2022-2032F |

| 6.1.4. Spain Carbon Market Revenues & Volume, By Graphite, 2022-2032F |

| 6.1.5. Spain Carbon Market Revenues & Volume, By Diamond, 2022-2032F |

| 6.2. Spain Carbon Market, By Applications |

| 6.2.1. Overview and Analysis |

| 6.2.2. Spain Carbon Market Revenues & Volume, By Automotive, 2022-2032F |

| 6.2.3. Spain Carbon Market Revenues & Volume, By Construction, 2022-2032F |

| 6.2.4. Spain Carbon Market Revenues & Volume, By Engineering Industries, 2022-2032F |

| 6.2.5. Spain Carbon Market Revenues & Volume, By Aerospace, 2022-2032F |

| 6.2.6. Spain Carbon Market Revenues & Volume, By Others, 2022-2032F |

| 7. Spain Carbon Market Import-Export Trade Statistics |

| 7.1 Spain Carbon Market Export to Major Countries |

| 7.2. Spain Carbon Market Imports from Major Countries |

| 8. Spain Carbon Market Key Performance Indicators |

| 8.1 Number of companies participating in carbon offsetting programs |

| 8.2 Percentage of renewable energy sources in Spain's energy mix |

| 8.3 Investment in research and development for carbon reduction technologies |

| 9. Spain Carbon Market - Opportunity Assessment |

| 9.1. Spain Carbon Market Opportunity Assessment, By Product Types, 2022 & 2032F |

| 9.2. Spain Carbon Market Opportunity Assessment, By Applications, 2022 & 2032F |

| 10. Spain Carbon Market - Competitive Landscape |

| 10.1. Spain Carbon Market Revenue Share, By Companies, 2025 |

| 10.2. Spain Carbon Market Competitive Benchmarking, By Operating and Technical Parameters |

| 11. Company Profiles |

| 12. Recommendations |

| 13. Disclaimer |

Global Go To Market Strategy - 2030

Export potential enables firms to identify high-growth global markets with greater confidence by combining advanced trade intelligence with a structured quantitative methodology. The framework analyzes emerging demand trends and country-level import patterns while integrating macroeconomic and trade datasets such as GDP and population forecasts, bilateral import–export flows, tariff structures, elasticity differentials between developed and developing economies, geographic distance, and import demand projections. Using weighted trade values from 2020–2024 as the base period to project country-to-country export potential for 2030, these inputs are operationalized through calculated drivers such as gravity model parameters, tariff impact factors, and projected GDP per-capita growth. Through an analysis of hidden potentials, demand hotspots, and market conditions that are most favorable to success, this method enables firms to focus on target countries, maximize returns, and global expansion with data, backed by accuracy.

By factoring in the projected importer demand gap that is currently unmet and could be potential opportunity, it identifies the potential for the Exporter (Country) among 190 countries, against the general trade analysis, which identifies the biggest importer or exporter.

To discover high-growth global markets and optimize your business strategy:

Click Here

Pricing

- Single User License$ 1,995

- Department License$ 2,400

- Site License$ 3,120

- Global License$ 3,795

Leadership Perspectives from Industry Events

Search

Thought Leadership and Analyst Meet

Our Clients

6WResearch In News

- India Export Attractiveness Tracker 2026

- India Air Conditioner Market Set for Strong Rebound in 2026 After Weather-Led Correction and GST-Driven Recovery: 6Wresearch

- ADAS in India: How Automatic Emergency Braking, Blind Spot Detection & Driver Monitoring are Transforming Road Safety

- Doha a strategic location for EV manufacturing hub: IPA Qatar

- Demand for luxury TVs surging in the GCC, says Samsung

- Empowering Growth: The Thriving Journey of Bangladesh’s Cable Industry

Latest Reports

- Nicaragua RPG Gaming Market (2026-2032)

- New Zealand RPG Gaming Market (2026-2032)

- Netherlands RPG Gaming Market (2026-2032)

- Nauru RPG Gaming Market (2026-2032)

- Namibia RPG Gaming Market (2026-2032)

- Mozambique RPG Gaming Market (2026-2032)

- Montenegro RPG Gaming Market (2026-2032)

- Mongolia RPG Gaming Market (2026-2032)

- Monaco RPG Gaming Market (2026-2032)

- Micronesia RPG Gaming Market (2026-2032)

Industry Events and Analyst Meet

EV India Expo 2026

HIMTEX 2026

India Refining Summit 2026

India EV Show 2026

EV tech India Expo 2026

Whitepaper

- Middle East & Africa Commercial Security Market Click here to view more.

- Middle East & Africa Fire Safety Systems & Equipment Market Click here to view more.

- GCC Drone Market Click here to view more.

- Middle East Lighting Fixture Market Click here to view more.

- GCC Physical & Perimeter Security Market Click here to view more.