Tanzania Oil and Gas Downstream Market (2025-2031) | Segmentation, Share, Value, Trends, Outlook, Industry, Size & Revenue, Growth, Companies, Forecast, Analysis, Competitive Landscape

Market Forecast By Sector (Refinery Sector, Petrochemical Sector) And Competitive Landscape

| Product Code: ETC9669099 | Publication Date: Sep 2024 | Updated Date: Nov 2025 | Product Type: Market Research Report | |

| Publisher: 6Wresearch | Author: Shubham Deep | No. of Pages: 75 | No. of Figures: 35 | No. of Tables: 20 |

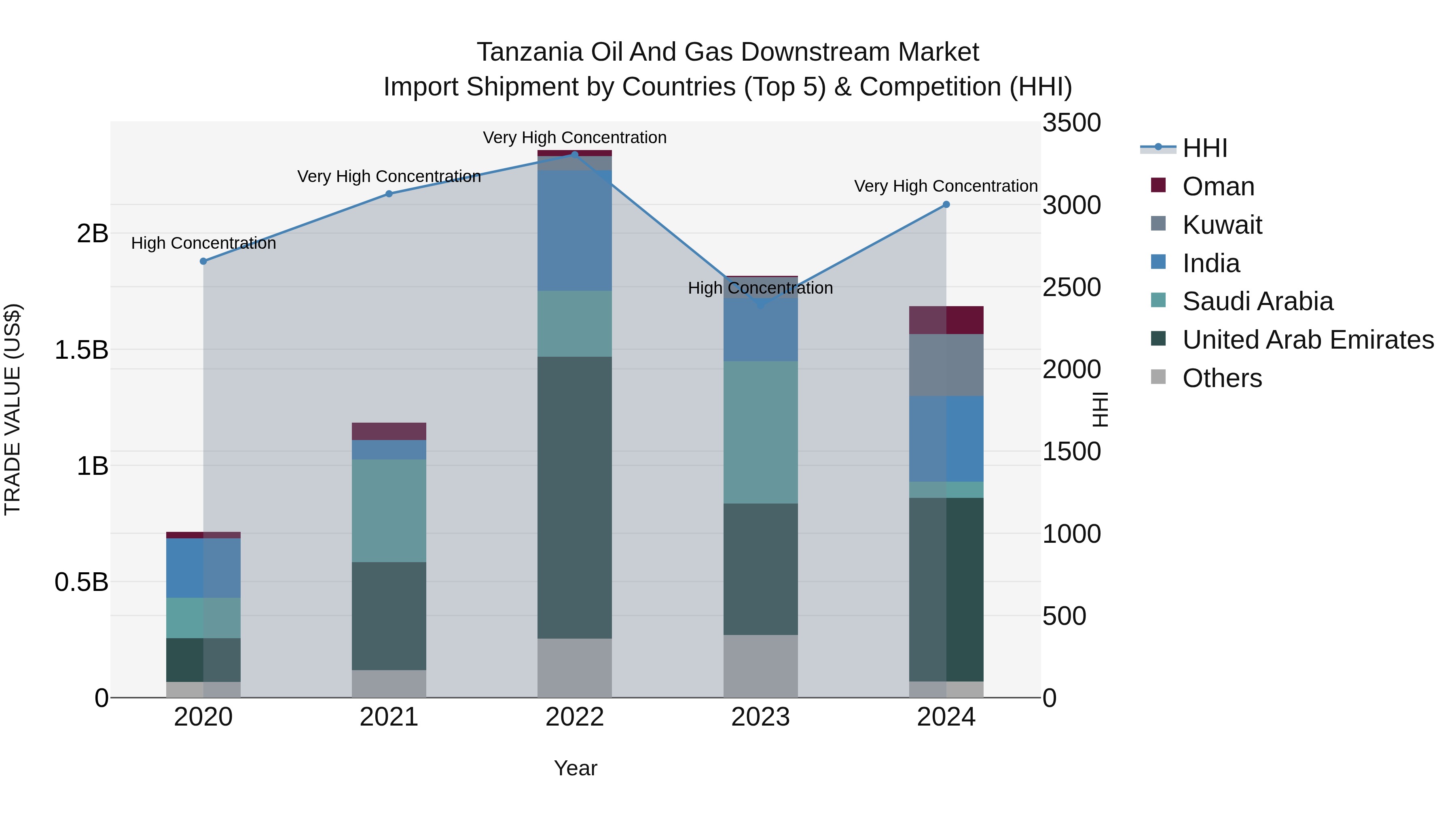

Tanzania Oil and Gas Downstream Market: Top 5 Importing Countries and Market Competition (HHI) Analysis

Tanzania`s oil and gas downstream import shipments in 2024 reflect a high concentration of imports from top exporting countries such as UAE, India, Kuwait, Oman, and Saudi Arabia. The Herfindahl-Hirschman Index (HHI) indicates a significant increase in market concentration from 2023 to 2024. Despite a strong compound annual growth rate (CAGR) of 23.99% from 2020 to 2024, there was a slight decline in the growth rate from 2023 to 2024 at -7.23%. This data suggests a complex landscape for Tanzania`s oil and gas downstream imports, influenced by key players in the global market.

Tanzania Oil and Gas Downstream Market Synopsis

The Tanzania Oil and Gas Downstream Market is a crucial sector in the country`s economy, marked by a growing demand for petroleum products due to increasing industrialization and urbanization. The market is dominated by state-owned Tanzania Petroleum Development Corporation (TPDC) and international oil companies. Key players in the downstream sector include fuel retail companies, storage and transportation providers, and distributors. The government plays a significant role in regulating the market through pricing mechanisms and policies to ensure supply security and fair competition. With ongoing investments in infrastructure development and exploration activities, the Tanzania Oil and Gas Downstream Market is poised for further growth and opportunities for both domestic and foreign investors.

Tanzania Oil and Gas Downstream Market Trends

The Tanzania Oil and Gas Downstream Market is experiencing significant growth driven by increasing demand for petroleum products, particularly due to the expanding transportation sector and rising industrial activities. The government`s efforts to attract foreign investments in the downstream sector, coupled with ongoing infrastructure development projects, are further fueling market expansion. Additionally, the shift towards cleaner energy sources and the adoption of more sustainable practices are emerging trends shaping the market landscape. Key players in the industry are focusing on enhancing operational efficiencies, investing in technology upgrades, and exploring opportunities for diversification and expansion. Overall, the Tanzania Oil and Gas Downstream Market is poised for continued growth and development in the coming years.

Tanzania Oil and Gas Downstream Market Challenges

In the Tanzania Oil and Gas Downstream Market, challenges include inadequate infrastructure for storage and distribution, leading to supply chain inefficiencies and product shortages in remote areas. Regulatory hurdles, such as complex licensing requirements and pricing regulations, also pose obstacles for companies operating in the sector. Additionally, the market faces competition from imported petroleum products, which can undermine the competitiveness of local refineries and distributors. Limited access to financing and investment capital further hinders the development and expansion of downstream activities in the country. Overall, addressing these challenges will be crucial to unlocking the full potential of the Tanzania Oil and Gas Downstream Market and ensuring a reliable and efficient supply of petroleum products for consumers nationwide.

Tanzania Oil and Gas Downstream Market Investment Opportunities

The Tanzania Oil and Gas Downstream Market presents various investment opportunities, including retail fuel distribution, storage facilities, and infrastructure development. With increasing demand for petroleum products driven by economic growth and urbanization, investing in retail fuel stations or distribution networks can be lucrative. Additionally, building storage facilities to meet the country`s growing storage capacity needs and developing infrastructure such as pipelines and terminals can offer long-term returns. As Tanzania aims to become a regional energy hub, there are opportunities for partnerships with international companies to capitalize on the potential growth in the downstream sector. However, investors should be mindful of regulatory frameworks, market competition, and potential environmental considerations when exploring investment opportunities in the Tanzania Oil and Gas Downstream Market.

Jordan Agar Market Government Policies

The Tanzanian government has put in place various policies to regulate the oil and gas downstream market. These policies include the Energy Policy of 2003, the Natural Gas Policy of 2013, and the Petroleum Act of 2015. The Energy Policy aims to promote efficient downstream operations, ensure quality of petroleum products, and encourage competition in the market. The Natural Gas Policy seeks to facilitate the development of a sustainable natural gas sector, including downstream activities such as distribution and transmission. The Petroleum Act regulates the downstream sector by establishing licensing requirements, safety standards, and environmental protection measures. Overall, these policies aim to promote investment, ensure energy security, and protect the interests of consumers in the Tanzania oil and gas downstream market.

Tanzania Oil and Gas Downstream Market Future Outlook

The future outlook for the Tanzania Oil and Gas Downstream Market looks promising with significant growth potential driven by ongoing infrastructure developments and increasing demand for petroleum products. The government`s initiatives to attract foreign investments and streamline regulations are expected to further boost the market. Additionally, the discovery of new oil and gas reserves in the region presents opportunities for expansion and diversification. With a growing population and rising urbanization trends, the demand for downstream products such as gasoline, diesel, and LPG is projected to increase, leading to a favorable market outlook for key players in the Tanzania Oil and Gas Downstream sector. However, challenges such as fluctuating global oil prices and environmental concerns may impact the market dynamics and require strategic planning for sustainable growth.

Key Highlights of the Report:

- Tanzania Oil and Gas Downstream Market Outlook

- Market Size of Tanzania Oil and Gas Downstream Market, 2024

- Forecast of Tanzania Oil and Gas Downstream Market, 2031

- Historical Data and Forecast of Tanzania Oil and Gas Downstream Revenues & Volume for the Period 2021- 2031

- Tanzania Oil and Gas Downstream Market Trend Evolution

- Tanzania Oil and Gas Downstream Market Drivers and Challenges

- Tanzania Oil and Gas Downstream Price Trends

- Tanzania Oil and Gas Downstream Porter's Five Forces

- Tanzania Oil and Gas Downstream Industry Life Cycle

- Historical Data and Forecast of Tanzania Oil and Gas Downstream Market Revenues & Volume By Sector for the Period 2021- 2031

- Historical Data and Forecast of Tanzania Oil and Gas Downstream Market Revenues & Volume By Refinery Sector for the Period 2021- 2031

- Historical Data and Forecast of Tanzania Oil and Gas Downstream Market Revenues & Volume By Petrochemical Sector for the Period 2021- 2031

- Tanzania Oil and Gas Downstream Import Export Trade Statistics

- Market Opportunity Assessment By Sector

- Tanzania Oil and Gas Downstream Top Companies Market Share

- Tanzania Oil and Gas Downstream Competitive Benchmarking By Technical and Operational Parameters

- Tanzania Oil and Gas Downstream Company Profiles

- Tanzania Oil and Gas Downstream Key Strategic Recommendations

Frequently Asked Questions About the Market Study (FAQs):

6Wresearch actively monitors the Tanzania Oil and Gas Downstream Market and publishes its comprehensive annual report, highlighting emerging trends, growth drivers, revenue analysis, and forecast outlook. Our insights help businesses to make data-backed strategic decisions with ongoing market dynamics. Our analysts track relevent industries related to the Tanzania Oil and Gas Downstream Market, allowing our clients with actionable intelligence and reliable forecasts tailored to emerging regional needs.

Yes, we provide customisation as per your requirements. To learn more, feel free to contact us on sales@6wresearch.com

1 Executive Summary |

2 Introduction |

2.1 Key Highlights of the Report |

2.2 Report Description |

2.3 Market Scope & Segmentation |

2.4 Research Methodology |

2.5 Assumptions |

3 Tanzania Oil and Gas Downstream Market Overview |

3.1 Tanzania Country Macro Economic Indicators |

3.2 Tanzania Oil and Gas Downstream Market Revenues & Volume, 2021 & 2031F |

3.3 Tanzania Oil and Gas Downstream Market - Industry Life Cycle |

3.4 Tanzania Oil and Gas Downstream Market - Porter's Five Forces |

3.5 Tanzania Oil and Gas Downstream Market Revenues & Volume Share, By Sector, 2021 & 2031F |

4 Tanzania Oil and Gas Downstream Market Dynamics |

4.1 Impact Analysis |

4.2 Market Drivers |

4.2.1 Increasing urbanization and industrialization leading to higher demand for energy products. |

4.2.2 Government initiatives to boost investments in the oil and gas downstream sector. |

4.2.3 Growing population and rising disposable income driving consumption of oil and gas products. |

4.3 Market Restraints |

4.3.1 Fluctuating global oil prices impacting profit margins for companies in the Tanzanian market. |

4.3.2 Regulatory challenges and compliance requirements affecting market entry and operations. |

4.3.3 Infrastructure limitations and lack of adequate distribution networks hindering market growth. |

5 Tanzania Oil and Gas Downstream Market Trends |

6 Tanzania Oil and Gas Downstream Market, By Types |

6.1 Tanzania Oil and Gas Downstream Market, By Sector |

6.1.1 Overview and Analysis |

6.1.2 Tanzania Oil and Gas Downstream Market Revenues & Volume, By Sector, 2021- 2031F |

6.1.3 Tanzania Oil and Gas Downstream Market Revenues & Volume, By Refinery Sector, 2021- 2031F |

6.1.4 Tanzania Oil and Gas Downstream Market Revenues & Volume, By Petrochemical Sector, 2021- 2031F |

7 Tanzania Oil and Gas Downstream Market Import-Export Trade Statistics |

7.1 Tanzania Oil and Gas Downstream Market Export to Major Countries |

7.2 Tanzania Oil and Gas Downstream Market Imports from Major Countries |

8 Tanzania Oil and Gas Downstream Market Key Performance Indicators |

8.1 Average daily refining capacity utilization rate. |

8.2 Number of new investments and projects in the downstream sector. |

8.3 Percentage increase in energy consumption per capita. |

9 Tanzania Oil and Gas Downstream Market - Opportunity Assessment |

9.1 Tanzania Oil and Gas Downstream Market Opportunity Assessment, By Sector, 2021 & 2031F |

10 Tanzania Oil and Gas Downstream Market - Competitive Landscape |

10.1 Tanzania Oil and Gas Downstream Market Revenue Share, By Companies, 2024 |

10.2 Tanzania Oil and Gas Downstream Market Competitive Benchmarking, By Operating and Technical Parameters |

11 Company Profiles |

12 Recommendations |

13 Disclaimer |

Pricing

- Single User License$ 1,995

- Department License$ 2,400

- Site License$ 3,120

- Global License$ 3,795

Search

Thought Leadership and Analyst Meet

Our Clients

Related Reports

- Canada Oil and Gas Market (2026-2032) | Share, Segmentation, Value, Industry, Trends, Forecast, Analysis, Size & Revenue, Growth, Competitive Landscape, Outlook, Companies

- Germany Breakfast Food Market (2026-2032) | Industry, Share, Growth, Size, Companies, Value, Analysis, Revenue, Trends, Forecast & Outlook

- Australia Briquette Market (2025-2031) | Growth, Size, Revenue, Forecast, Analysis, Trends, Value, Share, Industry & Companies

- Vietnam System Integrator Market (2025-2031) | Size, Companies, Analysis, Industry, Value, Forecast, Growth, Trends, Revenue & Share

- ASEAN and Thailand Brain Health Supplements Market (2025-2031) | Strategy, Consumer Insights, Analysis, Investment Trends, Opportunities, Growth, Size, Share, Industry, Revenue, Segments, Value, Segmentation, Supply, Forecast, Restraints, Outlook, Competition, Drivers, Trends, Demand, Pricing Analysis, Competitive, Strategic Insights, Companies, Challenges

- ASEAN Bearings Market (2025-2031) | Strategy, Consumer Insights, Analysis, Investment Trends, Opportunities, Growth, Size, Share, Industry, Revenue, Segments, Value, Segmentation, Supply, Forecast, Restraints, Outlook, Competition, Drivers, Trends, Demand, Pricing Analysis, Competitive, Strategic Insights, Companies, Challenges

- Europe Flooring Market (2025-2031) | Outlook, Share, Industry, Trends, Forecast, Companies, Revenue, Size, Analysis, Growth & Value

- Saudi Arabia Manlift Market (2025-2031) | Outlook, Size, Growth, Trends, Companies, Industry, Revenue, Value, Share, Forecast & Analysis

- Uganda Excavator, Crane, and Wheel Loaders Market (2025-2031) | Strategy, Consumer Insights, Analysis, Investment Trends, Opportunities, Growth, Size, Share, Industry, Revenue, Segments, Value, Segmentation, Supply, Forecast, Restraints, Outlook, Competition, Drivers, Trends, Demand, Pricing Analysis, Competitive, Strategic Insights, Companies, Challenges

- Rwanda Excavator, Crane, and Wheel Loaders Market (2025-2031) | Strategy, Consumer Insights, Analysis, Investment Trends, Opportunities, Growth, Size, Share, Industry, Revenue, Segments, Value, Segmentation, Supply, Forecast, Restraints, Outlook, Competition, Drivers, Trends, Demand, Pricing Analysis, Competitive, Strategic Insights, Companies, Challenges

Industry Events and Analyst Meet

Stationery & Paper Expo Saudi Arabia 2026

Kids & Toys Expo Saudi Arabia 2026

Gifts & Homeware Expo Saudi Arabia 2026

Smart Home Expo 2026

Industrial Facilities Management Expo 2025

Whitepaper

- Middle East & Africa Commercial Security Market Click here to view more.

- Middle East & Africa Fire Safety Systems & Equipment Market Click here to view more.

- GCC Drone Market Click here to view more.

- Middle East Lighting Fixture Market Click here to view more.

- GCC Physical & Perimeter Security Market Click here to view more.

6WResearch In News

- Doha a strategic location for EV manufacturing hub: IPA Qatar

- Demand for luxury TVs surging in the GCC, says Samsung

- Empowering Growth: The Thriving Journey of Bangladesh’s Cable Industry

- Demand for luxury TVs surging in the GCC, says Samsung

- Video call with a traditional healer? Once unthinkable, it’s now common in South Africa

- Intelligent Buildings To Smooth GCC’s Path To Net Zero