United Kingdom (UK) Bioethanol Market (2026-2032) Outlook | Analysis, Forecast, Growth, Industry, Companies, Trends, Revenue, Value, Size & Share

Market Forecast By Feedstock (Starch based, sugar based, cellulose based), By End Use Industry (transportation, pharmaceuticals, cosmetics, alcoholic beverages), By Fuel blend (E5, E10, E15 to E70, E75 & E85) And Competitive Landscape

| Product Code: ETC4485610 | Publication Date: Jul 2023 | Updated Date: Mar 2026 | Product Type: Report | |

| Publisher: 6Wresearch | Author: Ravi Bhandari | No. of Pages: 85 | No. of Figures: 45 | No. of Tables: 25 |

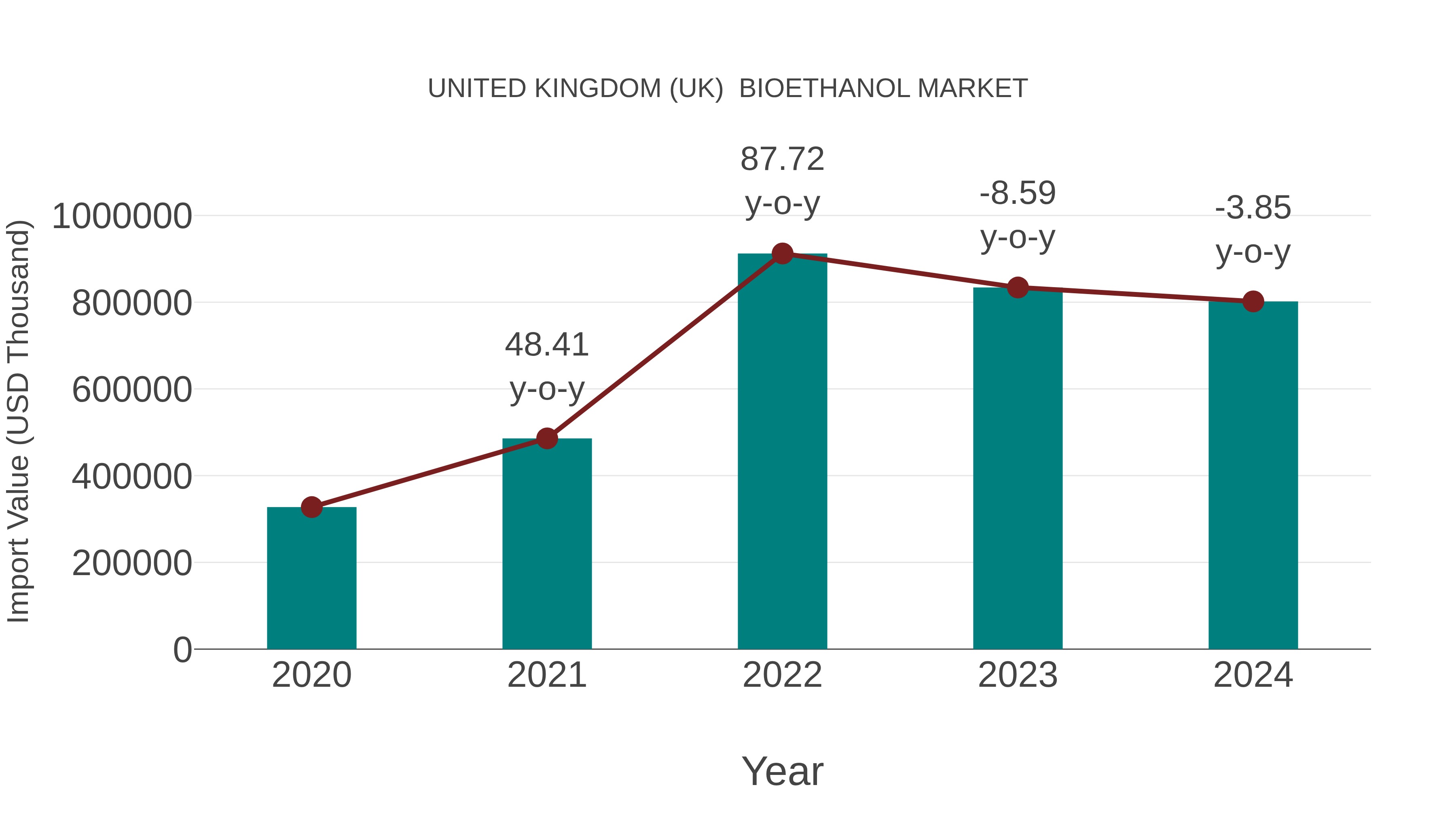

United Kingdom (UK) Bioethanol Market: Import Trend Analysis

The United Kingdom import trend for the bioethanol market showed a decline from 2023 to 2024, with a growth rate of -3.85%. However, the compound annual growth rate (CAGR) for the period 2020-2024 was 25.09%. This decrease in import momentum could be attributed to shifting demand dynamics or changes in trade policies affecting market stability.

United Kingdom (UK) Bioethanol Market Overview

The United Kingdom Bioethanol Market is experiencing steady growth due to increasing government initiatives promoting renewable fuels and reducing greenhouse gas emissions. Bioethanol, a renewable fuel derived from organic matter such as corn, sugar cane, or wheat, is being utilized as a cleaner alternative to traditional fossil fuels in the transportation sector. Key players in the UK market include bioethanol producers like Vivergo Fuels and Ensus, along with automotive companies incorporating bioethanol blends into their products. The market is also influenced by factors such as fluctuating feedstock prices, government regulations, and consumer demand for eco-friendly fuel options. With a growing emphasis on sustainability and reducing carbon footprints, the UK Bioethanol Market is poised for further expansion in the coming years.

United Kingdom (UK) Bioethanol Market Trends and Opportunities

The United Kingdom Bioethanol Market is experiencing growth due to increasing focus on renewable energy sources and sustainability. The demand for bioethanol, a renewable fuel derived from biomass such as corn or sugarcane, is rising as the UK aims to reduce greenhouse gas emissions and meet renewable energy targets. The government`s support through policies promoting the use of biofuels is driving market growth. Additionally, consumer awareness about the environmental benefits of bioethanol is creating opportunities for market expansion. Innovation in bioethanol production processes and investments in advanced technologies are also contributing to market development. Overall, the UK Bioethanol Market presents promising trends and opportunities for companies operating in the renewable energy sector.

United Kingdom (UK) Bioethanol Market Challenges

In the United Kingdom Bioethanol Market, one of the main challenges faced is the competition from other renewable energy sources, such as biodiesel and biogas. This competition can create pricing pressures and market saturation, impacting the profitability and growth potential of bioethanol producers. Additionally, regulatory uncertainty and changing government policies regarding renewable energy incentives and mandates can pose challenges for bioethanol producers in terms of planning investments and long-term sustainability. Furthermore, the availability and cost of feedstock, such as wheat, sugar beet, and corn, can also impact the production and profitability of bioethanol, especially during periods of fluctuating agricultural prices or shortages. Overall, navigating these challenges requires strategic planning, innovation, and adaptation to market dynamics in order to succeed in the UK Bioethanol Market.

United Kingdom (UK) Bioethanol Market Drivers

The United Kingdom (UK) Bioethanol market is primarily driven by the increasing focus on reducing carbon emissions and promoting sustainability in the transportation sector. Government regulations and initiatives aimed at promoting the use of biofuels, such as the Renewable Transport Fuel Obligation (RTFO), have created a favorable environment for the growth of the bioethanol industry. Additionally, rising awareness among consumers about the environmental impact of traditional fuels has led to an increased demand for bioethanol as an alternative, cleaner fuel source. The availability of feedstock such as wheat, sugar beet, and waste products also contributes to the growth of the market. Overall, the push towards renewable energy sources and the need to reduce dependence on fossil fuels are key drivers shaping the UK bioethanol market.

United Kingdom (UK) Bioethanol Market Government Policy

The UK government has implemented various policies to support the development and growth of the bioethanol market. One key policy is the Renewable Transport Fuel Obligation (RTFO), which requires fuel suppliers to ensure that a certain percentage of the fuel they supply comes from renewable sources such as bioethanol. The RTFO aims to reduce greenhouse gas emissions from the transportation sector and promote the use of sustainable biofuels. Additionally, the government provides financial incentives and grants to bioethanol producers to encourage investment in research and development of new technologies for biofuel production. These policies are in line with the UK`s commitment to reducing carbon emissions and transitioning to a more sustainable and environmentally friendly energy sector.

United Kingdom (UK) Bioethanol Market Future Outlook

The future outlook for the United Kingdom Bioethanol Market appears promising due to the increasing focus on reducing carbon emissions and transitioning towards more sustainable energy sources. Government initiatives and regulations supporting the use of bioethanol as a renewable fuel are likely to drive market growth. Additionally, the growing demand for bioethanol as a cleaner alternative to traditional fossil fuels in the transportation sector is expected to boost market expansion. Technological advancements in biofuel production processes and the potential for increased investments in the sector also bode well for the future of the UK bioethanol market. Overall, the market is anticipated to experience steady growth as sustainability and environmental concerns continue to drive the transition towards bio-based energy solutions.

Key Highlights of the Report:

- United Kingdom (UK) Bioethanol Market Outlook

- Market Size of United Kingdom (UK) Bioethanol Market, 2025

- Forecast of United Kingdom (UK) Bioethanol Market, 2032

- Historical Data and Forecast of United Kingdom (UK) Bioethanol Revenues & Volume for the Period 2022 - 2032F

- United Kingdom (UK) Bioethanol Market Trend Evolution

- United Kingdom (UK) Bioethanol Market Drivers and Challenges

- United Kingdom (UK) Bioethanol Price Trends

- United Kingdom (UK) Bioethanol Porter's Five Forces

- United Kingdom (UK) Bioethanol Industry Life Cycle

- Historical Data and Forecast of United Kingdom (UK) Bioethanol Market Revenues & Volume By Feedstock for the Period 2022 - 2032F

- Historical Data and Forecast of United Kingdom (UK) Bioethanol Market Revenues & Volume By Starch based for the Period 2022 - 2032F

- Historical Data and Forecast of United Kingdom (UK) Bioethanol Market Revenues & Volume By sugar based for the Period 2022 - 2032F

- Historical Data and Forecast of United Kingdom (UK) Bioethanol Market Revenues & Volume By cellulose based for the Period 2022 - 2032F

- Historical Data and Forecast of United Kingdom (UK) Bioethanol Market Revenues & Volume By End Use Industry for the Period 2022 - 2032F

- Historical Data and Forecast of United Kingdom (UK) Bioethanol Market Revenues & Volume By transportation for the Period 2022 - 2032F

- Historical Data and Forecast of United Kingdom (UK) Bioethanol Market Revenues & Volume By pharmaceuticals for the Period 2022 - 2032F

- Historical Data and Forecast of United Kingdom (UK) Bioethanol Market Revenues & Volume By cosmetics for the Period 2022 - 2032F

- Historical Data and Forecast of United Kingdom (UK) Bioethanol Market Revenues & Volume By alcoholic beverages for the Period 2022 - 2032F

- Historical Data and Forecast of United Kingdom (UK) Bioethanol Market Revenues & Volume By Fuel blend for the Period 2022 - 2032F

- Historical Data and Forecast of United Kingdom (UK) Bioethanol Market Revenues & Volume By E5 for the Period 2022 - 2032F

- Historical Data and Forecast of United Kingdom (UK) Bioethanol Market Revenues & Volume By E10 for the Period 2022 - 2032F

- Historical Data and Forecast of United Kingdom (UK) Bioethanol Market Revenues & Volume By E15 to E70 for the Period 2022 - 2032F

- Historical Data and Forecast of United Kingdom (UK) Bioethanol Market Revenues & Volume By E75 & E85 for the Period 2022 - 2032F

- United Kingdom (UK) Bioethanol Import Export Trade Statistics

- Market Opportunity Assessment By Feedstock

- Market Opportunity Assessment By End Use Industry

- Market Opportunity Assessment By Fuel blend

- United Kingdom (UK) Bioethanol Top Companies Market Share

- United Kingdom (UK) Bioethanol Competitive Benchmarking By Technical and Operational Parameters

- United Kingdom (UK) Bioethanol Company Profiles

- United Kingdom (UK) Bioethanol Key Strategic Recommendations

United Kingdom (UK) Bioethanol Market (2026-2032): FAQs

6Wresearch actively monitors the United Kingdom (UK) Bioethanol Market and publishes its comprehensive annual report, highlighting emerging trends, growth drivers, revenue analysis, and forecast outlook. Our insights help businesses to make data-backed strategic decisions with ongoing market dynamics. Our analysts track relevent industries related to the United Kingdom (UK) Bioethanol Market, allowing our clients with actionable intelligence and reliable forecasts tailored to emerging regional needs.

Yes, we provide customisation as per your requirements. To learn more, feel free to contact us on sales@6wresearch.com

1 Executive Summary |

2 Introduction |

2.1 Key Highlights of the Report |

2.2 Report Description |

2.3 Market Scope & Segmentation |

2.4 Research Methodology |

2.5 Assumptions |

3 United Kingdom (UK) Bioethanol Market Overview |

3.1 United Kingdom (UK) Country Macro Economic Indicators |

3.2 United Kingdom (UK) Bioethanol Market Revenues & Volume, 2022 & 2032F |

3.3 United Kingdom (UK) Bioethanol Market - Industry Life Cycle |

3.4 United Kingdom (UK) Bioethanol Market - Porter's Five Forces |

3.5 United Kingdom (UK) Bioethanol Market Revenues & Volume Share, By Feedstock, 2022 & 2032F |

3.6 United Kingdom (UK) Bioethanol Market Revenues & Volume Share, By End Use Industry, 2022 & 2032F |

3.7 United Kingdom (UK) Bioethanol Market Revenues & Volume Share, By Fuel blend, 2022 & 2032F |

4 United Kingdom (UK) Bioethanol Market Dynamics |

4.1 Impact Analysis |

4.2 Market Drivers |

4.2.1 Increasing government support and incentives for biofuels in the UK |

4.2.2 Growing focus on reducing carbon emissions and achieving sustainability goals |

4.2.3 Rising demand for renewable energy sources in the transportation sector |

4.3 Market Restraints |

4.3.1 Fluctuating feedstock prices impacting bioethanol production costs |

4.3.2 Competition from other renewable energy sources like biodiesel and electric vehicles in the UK market |

4.3.3 Regulatory challenges and uncertainties related to bioethanol production and distribution |

5 United Kingdom (UK) Bioethanol Market Trends |

6 United Kingdom (UK) Bioethanol Market, By Types |

6.1 United Kingdom (UK) Bioethanol Market, By Feedstock |

6.1.1 Overview and Analysis |

6.1.2 United Kingdom (UK) Bioethanol Market Revenues & Volume, By Feedstock, 2022-2032F |

6.1.3 United Kingdom (UK) Bioethanol Market Revenues & Volume, By Starch based, 2022-2032F |

6.1.4 United Kingdom (UK) Bioethanol Market Revenues & Volume, By sugar based, 2022-2032F |

6.1.5 United Kingdom (UK) Bioethanol Market Revenues & Volume, By cellulose based, 2022-2032F |

6.2 United Kingdom (UK) Bioethanol Market, By End Use Industry |

6.2.1 Overview and Analysis |

6.2.2 United Kingdom (UK) Bioethanol Market Revenues & Volume, By transportation, 2022-2032F |

6.2.3 United Kingdom (UK) Bioethanol Market Revenues & Volume, By pharmaceuticals, 2022-2032F |

6.2.4 United Kingdom (UK) Bioethanol Market Revenues & Volume, By cosmetics, 2022-2032F |

6.2.5 United Kingdom (UK) Bioethanol Market Revenues & Volume, By alcoholic beverages, 2022-2032F |

6.3 United Kingdom (UK) Bioethanol Market, By Fuel blend |

6.3.1 Overview and Analysis |

6.3.2 United Kingdom (UK) Bioethanol Market Revenues & Volume, By E5, 2022-2032F |

6.3.3 United Kingdom (UK) Bioethanol Market Revenues & Volume, By E10, 2022-2032F |

6.3.4 United Kingdom (UK) Bioethanol Market Revenues & Volume, By E15 to E70, 2022-2032F |

6.3.5 United Kingdom (UK) Bioethanol Market Revenues & Volume, By E75 & E85, 2022-2032F |

7 United Kingdom (UK) Bioethanol Market Import-Export Trade Statistics |

7.1 United Kingdom (UK) Bioethanol Market Export to Major Countries |

7.2 United Kingdom (UK) Bioethanol Market Imports from Major Countries |

8 United Kingdom (UK) Bioethanol Market Key Performance Indicators |

8.1 Percentage of bioethanol produced from sustainable feedstocks |

8.2 Carbon intensity reduction achieved through bioethanol use in transportation |

8.3 Investment in research and development for bioethanol production technologies |

8.4 Number of partnerships and collaborations for expanding bioethanol distribution network |

8.5 Percentage of vehicles using bioethanol as a fuel source |

9 United Kingdom (UK) Bioethanol Market - Opportunity Assessment |

9.1 United Kingdom (UK) Bioethanol Market Opportunity Assessment, By Feedstock, 2022 & 2032F |

9.2 United Kingdom (UK) Bioethanol Market Opportunity Assessment, By End Use Industry, 2022 & 2032F |

9.3 United Kingdom (UK) Bioethanol Market Opportunity Assessment, By Fuel blend, 2022 & 2032F |

10 United Kingdom (UK) Bioethanol Market - Competitive Landscape |

10.1 United Kingdom (UK) Bioethanol Market Revenue Share, By Companies, 2025 |

10.2 United Kingdom (UK) Bioethanol Market Competitive Benchmarking, By Operating and Technical Parameters |

11 Company Profiles |

12 Recommendations |

13 Disclaimer |

Global Go To Market Strategy - 2030

Export potential enables firms to identify high-growth global markets with greater confidence by combining advanced trade intelligence with a structured quantitative methodology. The framework analyzes emerging demand trends and country-level import patterns while integrating macroeconomic and trade datasets such as GDP and population forecasts, bilateral import–export flows, tariff structures, elasticity differentials between developed and developing economies, geographic distance, and import demand projections. Using weighted trade values from 2020–2024 as the base period to project country-to-country export potential for 2030, these inputs are operationalized through calculated drivers such as gravity model parameters, tariff impact factors, and projected GDP per-capita growth. Through an analysis of hidden potentials, demand hotspots, and market conditions that are most favorable to success, this method enables firms to focus on target countries, maximize returns, and global expansion with data, backed by accuracy.

By factoring in the projected importer demand gap that is currently unmet and could be potential opportunity, it identifies the potential for the Exporter (Country) among 190 countries, against the general trade analysis, which identifies the biggest importer or exporter.

To discover high-growth global markets and optimize your business strategy:

Click Here

Pricing

- Single User License$ 1,995

- Department License$ 2,400

- Site License$ 3,120

- Global License$ 3,795

Leadership Perspectives from Industry Events

Search

Thought Leadership and Analyst Meet

Our Clients

6WResearch In News

- Doha a strategic location for EV manufacturing hub: IPA Qatar

- Demand for luxury TVs surging in the GCC, says Samsung

- Empowering Growth: The Thriving Journey of Bangladesh’s Cable Industry

- Demand for luxury TVs surging in the GCC, says Samsung

- Video call with a traditional healer? Once unthinkable, it’s now common in South Africa

- Intelligent Buildings To Smooth GCC’s Path To Net Zero

Latest Reports

- Taiwan Airport Wireless Infrastructure Market (2026-2032)

- Vietnam Airport Wireless Infrastructure Market (2026-2032)

- Thailand Airport Wireless Infrastructure Market (2026-2032)

- South Korea Airport Wireless Infrastructure Market (2026-2032)

- Romania Airport Wireless Infrastructure Market (2026-2032)

- Qatar Airport Wireless Infrastructure Market (2026-2032)

- Philippines Airport Wireless Infrastructure Market (2026-2032)

- Japan Airport Wireless Infrastructure Market (2026-2032)

- Taiwan Airport Winter Services Market (2026-2032)

- Vietnam Airport Winter Services Market (2026-2032)

Industry Events and Analyst Meet

HIMTEX 2026

India Refining Summit 2026

India EV Show 2026

EV tech India Expo 2026

Auto Tech Asia 2026

Whitepaper

- Middle East & Africa Commercial Security Market Click here to view more.

- Middle East & Africa Fire Safety Systems & Equipment Market Click here to view more.

- GCC Drone Market Click here to view more.

- Middle East Lighting Fixture Market Click here to view more.

- GCC Physical & Perimeter Security Market Click here to view more.