United States (US) Laser Cladding Equipment Market (2025-2031) | Competitive Landscape, Size & Revenue, Share, Trends, Companies, Industry, Value, Forecast, Outlook, Segmentation, Analysis, Growth

Market Forecast By Power (High Power, Low Power), By Application (Power Generation, Industrial, Mining, Others) And Competitive Landscape

| Product Code: ETC9969039 | Publication Date: Sep 2024 | Updated Date: Nov 2025 | Product Type: Market Research Report | |

| Publisher: 6Wresearch | Author: Bhawna Singh | No. of Pages: 75 | No. of Figures: 35 | No. of Tables: 20 |

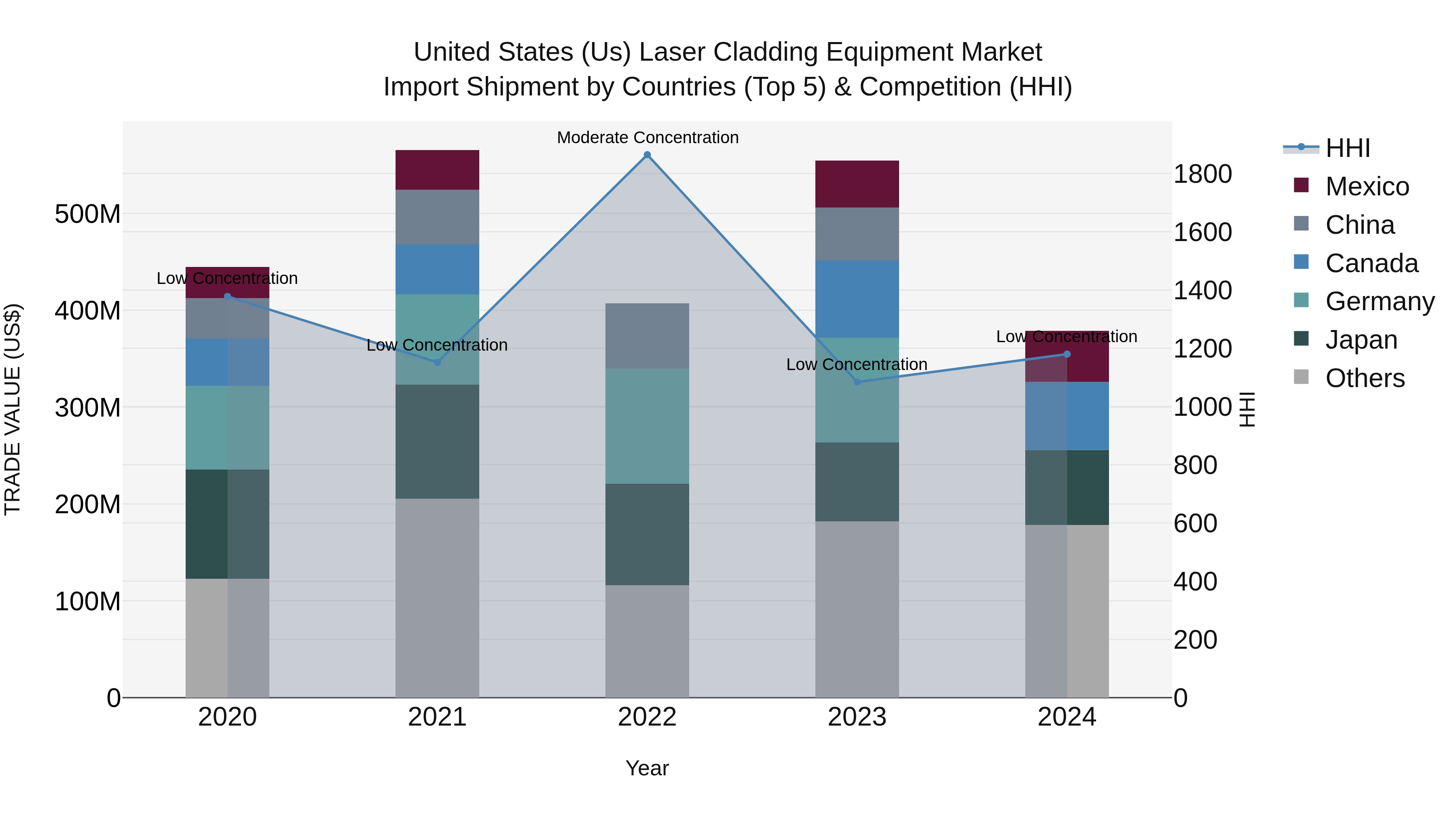

United States (US) Laser Cladding Equipment Market Top 5 Importing Countries and Market Competition (HHI) Analysis

Laser cladding equipment import shipments to the United States in 2024 were primarily sourced from Japan, Canada, Mexico, South Korea, and Switzerland. Despite the negative CAGR of -3.93% from 2020 to 2024, there was a significant decline in growth rate from 2023 to 2024 at -31.68%. The market remained fairly diversified with a low Herfindahl-Hirschman Index (HHI) concentration, indicating a competitive landscape among the exporting countries. This data suggests a challenging market environment for laser cladding equipment imports in the US, with fluctuations in growth rates impacting the industry dynamics.

United States (US) Laser Cladding Equipment Market Synopsis

The United States Laser Cladding Equipment Market is witnessing steady growth due to the increasing adoption of advanced manufacturing technologies across industries such as automotive, aerospace, and healthcare. Laser cladding equipment is utilized for enhancing the surface properties of components, improving wear resistance, and extending the lifespan of parts. The market is driven by the demand for high-quality and efficient manufacturing processes, leading to improved productivity and cost savings. Key players in the US market include Coherent Inc., IPG Photonics Corporation, and Trumpf Group, among others. Technological advancements, such as the integration of automation and robotics in laser cladding systems, are expected to further drive market growth in the coming years.

United States (US) Laser Cladding Equipment Market Trends

The US Laser Cladding Equipment Market is experiencing growth driven by increasing demand from industries such as aerospace, automotive, and oil & gas for advanced surface coating solutions. Key trends include the adoption of automation and robotics in laser cladding processes to improve efficiency and precision, as well as the development of high-performance laser cladding materials for enhanced durability and performance. Opportunities in the market lie in the expansion of applications to new industries like medical devices and renewable energy, as well as the integration of artificial intelligence and machine learning for process optimization. Additionally, the growing focus on sustainable manufacturing practices presents a promising avenue for the adoption of laser cladding equipment for eco-friendly surface treatment solutions.

United States (US) Laser Cladding Equipment Market Challenges

In the US Laser Cladding Equipment Market, some key challenges include high initial investment costs associated with purchasing and installing advanced laser cladding equipment, which can deter smaller businesses from adoption. Additionally, there is a shortage of skilled technicians and engineers with the expertise needed to operate and maintain these complex systems effectively. Regulatory hurdles and compliance requirements related to safety standards and environmental concerns also pose challenges for manufacturers in the market. Furthermore, the competitive landscape is evolving rapidly, with new entrants introducing innovative technologies, leading to market saturation and pricing pressures. Overall, navigating these obstacles requires companies to invest in training programs, research and development initiatives, and strategic partnerships to stay competitive in the dynamic US Laser Cladding Equipment Market.

United States (US) Laser Cladding Equipment Market Investment Opportunities

The United States Laser Cladding Equipment Market is primarily driven by the growing demand for advanced manufacturing technologies across industries such as automotive, aerospace, and healthcare. Laser cladding equipment offers benefits such as precision, efficiency, and cost-effectiveness in repairing and enhancing metal components, leading to its increasing adoption in various applications. Additionally, the rising focus on additive manufacturing and the need for customized solutions further propel the market growth. Technological advancements in laser cladding equipment, such as the integration of automation and robotics for enhanced productivity and quality, also play a significant role in driving the market forward. Moreover, the emphasis on reducing carbon emissions and improving sustainability practices is encouraging the adoption of laser cladding equipment for eco-friendly manufacturing processes.

United States (US) Laser Cladding Equipment Market Government Polices

The United States government has implemented various policies that impact the Laser Cladding Equipment Market. These include regulations from agencies such as the Occupational Safety and Health Administration (OSHA) and the Environmental Protection Agency (EPA) to ensure workplace safety and environmental compliance when using laser cladding equipment. Additionally, trade policies and tariffs imposed by the government can affect the import and export of laser cladding equipment, influencing market dynamics. Furthermore, government funding for research and development initiatives in advanced manufacturing technologies, including laser cladding, can drive innovation and growth in the market. Overall, government policies play a significant role in shaping the regulatory environment and market conditions for laser cladding equipment in the US.

United States (US) Laser Cladding Equipment Market Future Outlook

The United States Laser Cladding Equipment Market is expected to witness significant growth in the coming years due to increasing demand for advanced manufacturing technologies across various industries such as aerospace, automotive, and healthcare. The market is projected to be driven by factors such as the growing adoption of additive manufacturing processes, rising investments in research and development activities, and the need for enhanced surface properties and material performance. Additionally, the focus on reducing manufacturing costs and improving efficiency is likely to further propel the market growth. Technological advancements in laser cladding equipment, such as improved precision and versatility, are anticipated to drive market expansion as companies seek to enhance their production capabilities and stay competitive in the evolving industrial landscape.

Key Highlights of the Report:

- United States (US) Laser Cladding Equipment Market Outlook

- Market Size of United States (US) Laser Cladding Equipment Market, 2024

- Forecast of United States (US) Laser Cladding Equipment Market, 2031

- Historical Data and Forecast of United States (US) Laser Cladding Equipment Revenues & Volume for the Period 2021- 2031

- United States (US) Laser Cladding Equipment Market Trend Evolution

- United States (US) Laser Cladding Equipment Market Drivers and Challenges

- United States (US) Laser Cladding Equipment Price Trends

- United States (US) Laser Cladding Equipment Porter's Five Forces

- United States (US) Laser Cladding Equipment Industry Life Cycle

- Historical Data and Forecast of United States (US) Laser Cladding Equipment Market Revenues & Volume By Power for the Period 2021- 2031

- Historical Data and Forecast of United States (US) Laser Cladding Equipment Market Revenues & Volume By High Power for the Period 2021- 2031

- Historical Data and Forecast of United States (US) Laser Cladding Equipment Market Revenues & Volume By Low Power for the Period 2021- 2031

- Historical Data and Forecast of United States (US) Laser Cladding Equipment Market Revenues & Volume By Application for the Period 2021- 2031

- Historical Data and Forecast of United States (US) Laser Cladding Equipment Market Revenues & Volume By Power Generation for the Period 2021- 2031

- Historical Data and Forecast of United States (US) Laser Cladding Equipment Market Revenues & Volume By Industrial for the Period 2021- 2031

- Historical Data and Forecast of United States (US) Laser Cladding Equipment Market Revenues & Volume By Mining for the Period 2021- 2031

- Historical Data and Forecast of United States (US) Laser Cladding Equipment Market Revenues & Volume By Others for the Period 2021- 2031

- United States (US) Laser Cladding Equipment Import Export Trade Statistics

- Market Opportunity Assessment By Power

- Market Opportunity Assessment By Application

- United States (US) Laser Cladding Equipment Top Companies Market Share

- United States (US) Laser Cladding Equipment Competitive Benchmarking By Technical and Operational Parameters

- United States (US) Laser Cladding Equipment Company Profiles

- United States (US) Laser Cladding Equipment Key Strategic Recommendations

Frequently Asked Questions About the Market Study (FAQs):

6Wresearch actively monitors the United States (US) Laser Cladding Equipment Market and publishes its comprehensive annual report, highlighting emerging trends, growth drivers, revenue analysis, and forecast outlook. Our insights help businesses to make data-backed strategic decisions with ongoing market dynamics. Our analysts track relevent industries related to the United States (US) Laser Cladding Equipment Market, allowing our clients with actionable intelligence and reliable forecasts tailored to emerging regional needs.

Yes, we provide customisation as per your requirements. To learn more, feel free to contact us on sales@6wresearch.com

1 Executive Summary |

2 Introduction |

2.1 Key Highlights of the Report |

2.2 Report Description |

2.3 Market Scope & Segmentation |

2.4 Research Methodology |

2.5 Assumptions |

3 United States (US) Laser Cladding Equipment Market Overview |

3.1 United States (US) Country Macro Economic Indicators |

3.2 United States (US) Laser Cladding Equipment Market Revenues & Volume, 2021 & 2031F |

3.3 United States (US) Laser Cladding Equipment Market - Industry Life Cycle |

3.4 United States (US) Laser Cladding Equipment Market - Porter's Five Forces |

3.5 United States (US) Laser Cladding Equipment Market Revenues & Volume Share, By Power, 2021 & 2031F |

3.6 United States (US) Laser Cladding Equipment Market Revenues & Volume Share, By Application, 2021 & 2031F |

4 United States (US) Laser Cladding Equipment Market Dynamics |

4.1 Impact Analysis |

4.2 Market Drivers |

4.2.1 Increasing demand for laser cladding equipment in industries such as automotive, aerospace, and healthcare due to its precision and efficiency. |

4.2.2 Technological advancements leading to improved capabilities and efficiency of laser cladding equipment. |

4.3 Market Restraints |

4.3.1 High initial investment cost associated with purchasing and installing laser cladding equipment. |

4.3.2 Limited availability of skilled professionals proficient in operating and maintaining laser cladding equipment. |

5 United States (US) Laser Cladding Equipment Market Trends |

6 United States (US) Laser Cladding Equipment Market, By Types |

6.1 United States (US) Laser Cladding Equipment Market, By Power |

6.1.1 Overview and Analysis |

6.1.2 United States (US) Laser Cladding Equipment Market Revenues & Volume, By Power, 2021- 2031F |

6.1.3 United States (US) Laser Cladding Equipment Market Revenues & Volume, By High Power, 2021- 2031F |

6.1.4 United States (US) Laser Cladding Equipment Market Revenues & Volume, By Low Power, 2021- 2031F |

6.2 United States (US) Laser Cladding Equipment Market, By Application |

6.2.1 Overview and Analysis |

6.2.2 United States (US) Laser Cladding Equipment Market Revenues & Volume, By Power Generation, 2021- 2031F |

6.2.3 United States (US) Laser Cladding Equipment Market Revenues & Volume, By Industrial, 2021- 2031F |

6.2.4 United States (US) Laser Cladding Equipment Market Revenues & Volume, By Mining, 2021- 2031F |

6.2.5 United States (US) Laser Cladding Equipment Market Revenues & Volume, By Others, 2021- 2031F |

7 United States (US) Laser Cladding Equipment Market Import-Export Trade Statistics |

7.1 United States (US) Laser Cladding Equipment Market Export to Major Countries |

7.2 United States (US) Laser Cladding Equipment Market Imports from Major Countries |

8 United States (US) Laser Cladding Equipment Market Key Performance Indicators |

8.1 Average utilization rate of laser cladding equipment in the US market. |

8.2 Rate of adoption of laser cladding technology by key industries in the US. |

8.3 Percentage of companies investing in RD for enhancing laser cladding equipment capabilities. |

9 United States (US) Laser Cladding Equipment Market - Opportunity Assessment |

9.1 United States (US) Laser Cladding Equipment Market Opportunity Assessment, By Power, 2021 & 2031F |

9.2 United States (US) Laser Cladding Equipment Market Opportunity Assessment, By Application, 2021 & 2031F |

10 United States (US) Laser Cladding Equipment Market - Competitive Landscape |

10.1 United States (US) Laser Cladding Equipment Market Revenue Share, By Companies, 2024 |

10.2 United States (US) Laser Cladding Equipment Market Competitive Benchmarking, By Operating and Technical Parameters |

11 Company Profiles |

12 Recommendations |

13 Disclaimer |

Export potential assessment - trade Analytics for 2030

Export potential enables firms to identify high-growth global markets with greater confidence by combining advanced trade intelligence with a structured quantitative methodology. The framework analyzes emerging demand trends and country-level import patterns while integrating macroeconomic and trade datasets such as GDP and population forecasts, bilateral import–export flows, tariff structures, elasticity differentials between developed and developing economies, geographic distance, and import demand projections. Using weighted trade values from 2020–2024 as the base period to project country-to-country export potential for 2030, these inputs are operationalized through calculated drivers such as gravity model parameters, tariff impact factors, and projected GDP per-capita growth. Through an analysis of hidden potentials, demand hotspots, and market conditions that are most favorable to success, this method enables firms to focus on target countries, maximize returns, and global expansion with data, backed by accuracy.

By factoring in the projected importer demand gap that is currently unmet and could be potential opportunity, it identifies the potential for the Exporter (Country) among 190 countries, against the general trade analysis, which identifies the biggest importer or exporter.

To discover high-growth global markets and optimize your business strategy:

Click Here

Pricing

- Single User License$ 1,995

- Department License$ 2,400

- Site License$ 3,120

- Global License$ 3,795

Search

Thought Leadership and Analyst Meet

Our Clients

Latest Reports

- France Thermally Conductive Filler Dispersants Market (2026-2032) | Challenges, Restraints, Value, Share, Size, segmentation, Analysis, Trends, Investment Opportunities, Outlook, Pricing, Demand, Forecast, Revenue, Companies, Growth, Drivers, Strategy, Insights, Competition

- Egypt Thermally Conductive Filler Dispersants Market (2026-2032) | Competition, Forecast, Strategy, Value, Insights, Outlook, Investment Opportunities, Pricing, Demand, Share, segmentation, Drivers, Size, Companies, Restraints, Growth, Trends, Revenue, Challenges, Analysis

- Czech Republic Thermally Conductive Filler Dispersants Market (2026-2032) | Forecast, Pricing, Analysis, Drivers, Insights, Size, Demand, Growth, Challenges, segmentation, Competition, Outlook, Trends, Investment Opportunities, Companies, Strategy, Revenue, Share, Value, Restraints

- Colombia Thermally Conductive Filler Dispersants Market (2026-2032) | segmentation, Trends, Share, Drivers, Strategy, Companies, Demand, Insights, Size, Challenges, Value, Competition, Analysis, Growth, Revenue, Restraints, Forecast, Pricing, Outlook, Investment Opportunities

- China Thermally Conductive Filler Dispersants Market (2026-2032) | Restraints, Investment Opportunities, Pricing, Companies, Share, Size, Challenges, Trends, Outlook, Value, Analysis, Competition, Revenue, Drivers, Forecast, Demand, Insights, Growth, Strategy, segmentation

- Chile Thermally Conductive Filler Dispersants Market (2026-2032) | Investment Opportunities, Trends, Value, Restraints, Share, Companies, Forecast, segmentation, Pricing, Challenges, Demand, Size, Analysis, Drivers, Outlook, Growth, Competition, Strategy, Revenue, Insights

- Cambodia Thermally Conductive Filler Dispersants Market (2026-2032) | Analysis, Share, Outlook, Strategy, Pricing, Demand, Size, Growth, segmentation, Insights, Revenue, Forecast, Challenges, Competition, Companies, Investment Opportunities, Trends, Restraints, Value, Drivers

- Brazil Thermally Conductive Filler Dispersants Market (2026-2032) | Restraints, Forecast, Competition, Size, Revenue, Value, Investment Opportunities, Trends, Insights, Outlook, Growth, Analysis, Drivers, segmentation, Pricing, Challenges, Strategy, Share, Companies, Demand

- Bangladesh Thermally Conductive Filler Dispersants Market (2026-2032) | Restraints, Trends, Analysis, Competition, Insights, Forecast, Value, Investment Opportunities, Pricing, Share, Demand, Outlook, Revenue, segmentation, Companies, Drivers, Growth, Size, Challenges, Strategy

- Bahrain Thermally Conductive Filler Dispersants Market (2026-2032) | Trends, Outlook, Pricing, Demand, Value, Competition, Forecast, Growth, segmentation, Revenue, Companies, Analysis, Insights, Size, Drivers, Challenges, Strategy, Investment Opportunities, Share, Restraints

Industry Events and Analyst Meet

HIMTEX 2026

India Refining Summit 2026

India EV Show 2026

EV tech India Expo 2026

Auto Tech Asia 2026

Whitepaper

- Middle East & Africa Commercial Security Market Click here to view more.

- Middle East & Africa Fire Safety Systems & Equipment Market Click here to view more.

- GCC Drone Market Click here to view more.

- Middle East Lighting Fixture Market Click here to view more.

- GCC Physical & Perimeter Security Market Click here to view more.

6WResearch In News

- Doha a strategic location for EV manufacturing hub: IPA Qatar

- Demand for luxury TVs surging in the GCC, says Samsung

- Empowering Growth: The Thriving Journey of Bangladesh’s Cable Industry

- Demand for luxury TVs surging in the GCC, says Samsung

- Video call with a traditional healer? Once unthinkable, it’s now common in South Africa

- Intelligent Buildings To Smooth GCC’s Path To Net Zero