China Bus Market (2025-2031) | Outlook, Forecast, Size, Share, Value, Companies, Trends, Revenue, Industry, Growth & Analysis

Market Forecast By Type (Single Deck, Double Deck), By Application (Transit, Coaches, Others), By Fuel Type (Diesel, Electric and Hybrid, Others), By Seat Capacity (15-30 Seats, 31-50 Seats, More than 50 Seats) And Competitive Landscape

| Product Code: ETC361101 | Publication Date: Aug 2022 | Updated Date: Oct 2025 | Product Type: Market Research Report | |

| Publisher: 6Wresearch | Author: Sachin Kumar Rai | No. of Pages: 75 | No. of Figures: 35 | No. of Tables: 20 |

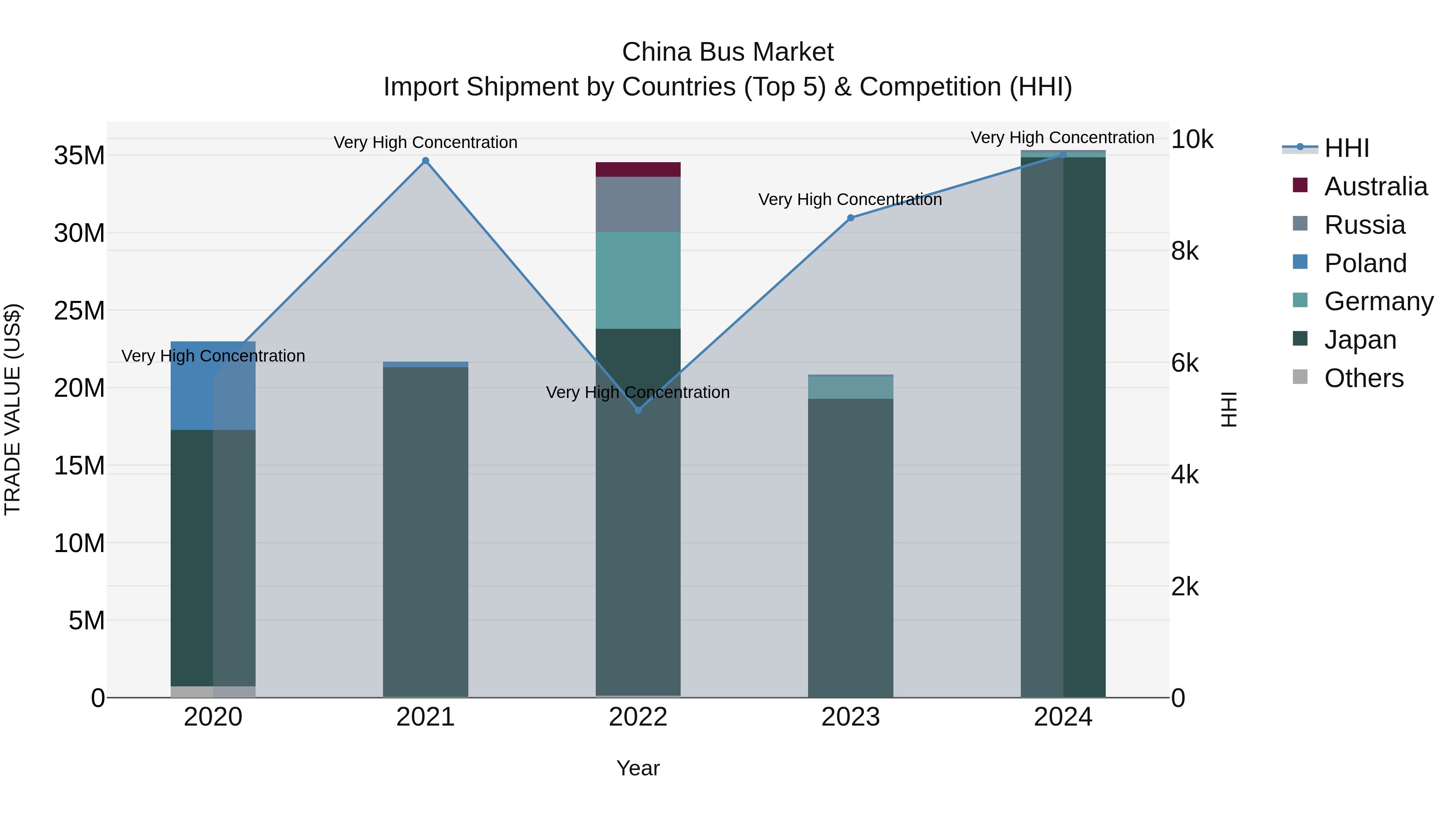

China Bus Market Top 5 Importing Countries and Market Competition (HHI) Analysis

In 2024, China bus import market continued to thrive with significant contributions from top exporters Japan, Germany, Russia, Vietnam, and Hungary. The high Herfindahl-Hirschman Index (HHI) indicates a concentrated market landscape. The impressive compound annual growth rate (CAGR) of 11.35% from 2020-2024 showcases sustained expansion. Moreover, the exceptional growth rate of 69.38% from 2023-2024 signals a surge in demand for imported buses in China, reflecting a promising outlook for the industry.

China Bus Market Growth Rate

According to 6Wresearch internal database and industry insights, the China Bus Market is growing at a compound annual growth rate (CAGR) of 8.5% during the forecast period (2025–2031). The market is driven by urban growth, green mobility goals, government support, tech advances, and integration with transport modes.

China Bus Market Highlights

| Report Name | China Bus Market |

| Forecast Period | 2025–2031 |

| CAGR | 8.5% |

| Growing Sector | Electric and Hybrid Buses |

Topics Covered in the China Bus Market Report

The China Bus Market report thoroughly covers the market by type, application, fuel type, seat capacity, and regions. The market report provides an unbiased and detailed analysis of ongoing market trends, key drivers, upcoming opportunities, and regional demand variations to help stakeholders design their growth strategies effectively.

China Bus Market Synopsis

China Bus Market shows impressive growth, backed by expanding public transport infrastructure, supportive government policies, and rising interest in green mobility options. Urban expansion and environmental focus encourage the adoption of electric and hybrid buses in China. Advances in battery performance and autonomous vehicle technologies are reshaping bus manufacturing and fleet management, raising China’s status as a global bus industry leader.

The China Bus Market is projected to grow steadily at a compound annual growth rate CAGR of 8.5% during the forecast period of 2025 to 2031. Growth in the China Bus Market stems from increasing intercity and intracity transit needs, increased investments in smart city infrastructure, and the renewal of aging diesel bus fleets. Supportive financing schemes and improvements in electric vehicle charging infrastructure are aiding market expansion. Chinese OEMs are also increasing production and exports, strengthening their global presence and securing regional dominance. Collectively, these aspects improve industry growth, competitiveness, and sustainability over the long term across segments.

China Bus Market Challenges

The expansion of the China Bus Market Growth is mainly challenged by increasing input costs, fluctuating raw material prices, and rising global trade rules and regulations. Operational challenges like battery disposal, electric grid constraints, and regional policy differences can slow seamless adoption. In addition, high initial costs for electric and hybrid buses discourage small fleet operators. A lack of skilled maintenance staff and varied component standards across provinces also affect market efficiency and logistics planning.

China Bus Market Trends

Emerging trends in the China Bus Market include AI-powered route optimization, smart telematics for real-time diagnostics, and the move toward hydrogen-powered buses. Autonomous bus pilot projects are active in cities like Shanghai and Shenzhen. Bus makers are using lightweight materials and modular designs to attract consumers. Subscription fleet leasing and MaaS concepts are growing majorly in popularity. Electric bus exports to Europe, Africa, and Southeast Asia are steadily increasing.

Investment opportunities in China Bus Market

The China Bus Industry provides with significant investment opportunities in battery innovation, charging infrastructure, and digital mobility systems. There is growing emphasis on R&D for long-range electric buses and hydrogen fuel cells. Startups and OEMs are funding fleet analytics platforms, smart dashboards, and energy management tools. Expansion of high-speed charging stations, particularly along intercity routes, is creating new growth paths. Partnerships with regional transport authorities support localized production efforts.

Leading Players of the China Bus Market

The China Bus Market Share is dominated by players with strong capabilities in electric mobility, autonomous technologies, and mass production. Leading companies include Yutong Bus Co. Ltd, BYD Auto Co. Ltd, King Long Motor Group, and Zhongtong Bus. These manufacturers have robust domestic presence and export networks. Tech-based disruptors like NIO Bus and Foton AUV are emerging through innovation in AI-driven navigation and connected bus platforms, altering the competitive landscape across application segments.

Government Regulations Introduced in the China Bus Market

According to Chinese government data, several initiatives have been introduced to promote electric buses, including the New Energy Vehicle (NEV) Subsidy Program, which encourages adoption through tax exemptions and rebates. Low-emission public transit is supported by the Green Transport Action Plan, while provinces including Guangdong and Zhejiang have adopted strict emission standards and mandated electric-only bus fleets. In addition, regulatory frameworks like GB/T charging standards provide uniformity for charging infrastructure, aiding the nationwide deployment of clean and connected mobility solutions.

Future Insights of the China Bus Market

The bus market in China is forecast to expand steadily as smart mobility efforts extend into smaller urban areas beyond the largest cities. Future developments include Level 4 autonomous buses that require minimal human control, solar-powered electric buses, and cutting-edge 5G-enabled fleet monitoring technologies. The 14th Five-Year Plan reinforces China’s emphasis on environmental protection and green mobility, encouraging wider use of eco-friendly buses. Furthermore, integrating buses alongside other transportation modes will enhance their role in city mobility frameworks.

Market Segmentation Analysis

The report offers a comprehensive study of the subsequent market segments and their leading categories.

Single Deck Buses to Dominate the Market – By Type

According to Guneet Kaur , Senior Research Analyst , 6Wresearch, the single deck segment leads the China Bus Market owing to its operational suitability for urban and suburban transport. These buses are preferred by city municipalities due to their efficiency in high-density routes and lower costs compared to double-deckers. Enhanced comfort features, energy efficiency, and modular seating make them ideal for school, corporate, and feeder services. Several city transport networks are replacing older diesel models with electric single-deck buses to meet green transport goals.

Transit Buses to Dominate the Market – By Application

Transit buses represent the dominant application segment in the China Bus Market. Rapid metro expansion, growing population density, and rising daily ridership have led to increased demand for efficient mass transit buses. Government subsidies for transit infrastructure and deployment of smart ticketing systems are fueling transit fleet upgrades.

Electric and Hybrid Buses to Dominate the Market – By Fuel Type

Electric and hybrid buses are rapidly gaining ground and lead the China Bus Market by fuel type. The government’s strong push for zero-emission transport, availability of incentives, and growing environmental awareness have positioned this segment for exponential growth. Domestic brands are innovating battery technologies to enhance mileage and reduce charging time.

31–50 Seats to Dominate the Market– By Seat Capacity

Buses with 31–50 seat capacity dominate the China Bus Market due to their balance between capacity and maneuverability. These buses are widely used in intercity routes, corporate shuttle services, and urban transportation. They offer greater revenue per trip without excessive fuel consumption or parking constraints. Transit authorities prefer this capacity range for both city and long-haul applications.

Key Attractiveness of the Report

- 10 Years of Market Numbers.

- Historical Data Starting from 2021 to 2024.

- Base Year: 2024.

- Forecast Data until 2031.

- Key Performance Indicators Impacting the Market.

- Major Upcoming Developments and Projects.

Key Highlights of the Report:

- China Bus Market Outlook

- Market Size of China Bus Market, 2024

- Forecast of China Bus Market, 20

- Historical Data and Forecast of China Bus Revenues & Volume for the Period 2021 - 2031F

- China Bus Market Trend Evolution

- China Bus Market Drivers and Challenges

- China Bus Price Trends

- China Bus Porter's Five Forces

- China Bus Industry Life Cycle

- Historical Data and Forecast of China Bus Market Revenues & Volume By Type for the Period 2021 - 2031F

- Historical Data and Forecast of China Bus Market Revenues & Volume By Single Deck for the Period 2021 - 2031F

- Historical Data and Forecast of China Bus Market Revenues & Volume By Double Deck for the Period 2021 - 2031F

- Historical Data and Forecast of China Bus Market Revenues & Volume By Application for the Period 2021 - 2031F

- Historical Data and Forecast of China Bus Market Revenues & Volume By Transit for the Period 2021 - 2031F

- Historical Data and Forecast of China Bus Market Revenues & Volume By Coaches for the Period 2021 - 2031F

- Historical Data and Forecast of China Bus Market Revenues & Volume By Others for the Period 2021 - 2031F

- Historical Data and Forecast of China Bus Market Revenues & Volume By Fuel Type for the Period 2021 - 2031F

- Historical Data and Forecast of China Bus Market Revenues & Volume By Diesel for the Period 2021 - 2031F

- Historical Data and Forecast of China Bus Market Revenues & Volume By Electric and Hybrid for the Period 2021 - 2031F

- Historical Data and Forecast of China Bus Market Revenues & Volume By Others for the Period 2021 - 2031F

- Historical Data and Forecast of China Bus Market Revenues & Volume By Seat Capacity for the Period 2021 - 2031F

- Historical Data and Forecast of China Bus Market Revenues & Volume By 15-30 Seats for the Period 2021 - 2031F

- Historical Data and Forecast of China Bus Market Revenues & Volume By 31-50 Seats for the Period 2021 - 2031F

- Historical Data and Forecast of China Bus Market Revenues & Volume By More than 50 Seats for the Period 2021 - 2031F

- China Bus Import Export Trade Statistics

- Market Opportunity Assessment By Type

- Market Opportunity Assessment By Application

- Market Opportunity Assessment By Fuel Type

- Market Opportunity Assessment By Seat Capacity

- China Bus Top Companies Market Share

- China Bus Competitive Benchmarking By Technical and Operational Parameters

- China Bus Company Profiles

- China Bus Key Strategic Recommendations

Market Covered

The market report provides a detailed analysis of the following market segments:

By Countries

China – All Provinces Covered

By Type

- Single Deck

- Double Deck

By Application

- Transit

- Coaches

- Others

By Fuel Type

- Diesel

- Electric and Hybrid

- Others

By Seat Capacity

- 15–30 Seats

- 31–50 Seats

- More than 50 Seats

China Bus Market (2025-2031): FAQs

China Bus Market is projected to grow at a CAGR of approximately 8.5% during the forecast period.

Guangdong Province leads in electric bus adoption due to aggressive green policy enforcement and large-scale urban transit projects.

Major players include Yutong Bus, BYD Auto, King Long, Zhongtong Bus, and Foton AUV.

Initiatives like the NEV Subsidy Program, Green Transport Action Plan, and regional mandates for electric public fleets support this growth.

6Wresearch actively monitors the China Bus Market and publishes its comprehensive annual report, highlighting emerging trends, growth drivers, revenue analysis, and forecast outlook. Our insights help businesses to make data-backed strategic decisions with ongoing market dynamics. Our analysts track relevent industries related to the China Bus Market, allowing our clients with actionable intelligence and reliable forecasts tailored to emerging regional needs.

Yes, we provide customisation as per your requirements. To learn more, feel free to contact us on sales@6wresearch.com

| 1 Executive Summary |

| 2 Introduction |

| 2.1 Key Highlights of the Report |

| 2.2 Report Description |

| 2.3 Market Scope & Segmentation |

| 2.4 Research Methodology |

| 2.5 Assumptions |

| 3 China Candle Market Overview |

| 3.1 China Country Macro Economic Indicators |

| 3.2 China Candle Market Revenues & Volume, 2021 & 2031F |

| 3.3 China Candle Market - Industry Life Cycle |

| 3.4 China Candle Market - Porter's Five Forces |

| 3.5 China Candle Market Revenues & Volume Share, By Product Type, 2021 & 2031F |

| 3.6 China Candle Market Revenues & Volume Share, By Wax, 2021 & 2031F |

| 3.7 China Candle Market Revenues & Volume Share, By Distribution Channel, 2021 & 2031F |

| 4 China Candle Market Dynamics |

| 4.1 Impact Analysis |

| 4.2 Market Drivers |

| 4.2.1 Increasing consumer preference for home décor and ambiance enhancement products |

| 4.2.2 Growing awareness about eco-friendly and sustainable candles |

| 4.2.3 Rising demand for aromatherapy and wellness products |

| 4.3 Market Restraints |

| 4.3.1 Fluctuating raw material prices, such as wax and fragrance oils |

| 4.3.2 Intense competition from alternative home fragrance products like diffusers and air fresheners |

| 4.3.3 Stringent regulations related to emissions and safety standards for candles |

| 5 China Candle Market Trends |

| 6 China Candle Market, By Types |

| 6.1 China Candle Market, By Product Type |

| 6.1.1 Overview and Analysis |

| 6.1.2 China Candle Market Revenues & Volume, By Product Type, 2021 - 2031F |

| 6.1.3 China Candle Market Revenues & Volume, By Votive, 2021 - 2031F |

| 6.1.4 China Candle Market Revenues & Volume, By Container Candle, 2021 - 2031F |

| 6.1.5 China Candle Market Revenues & Volume, By Pillars, 2021 - 2031F |

| 6.1.6 China Candle Market Revenues & Volume, By Tapers, 2021 - 2031F |

| 6.1.7 China Candle Market Revenues & Volume, By Others, 2021 - 2031F |

| 6.2 China Candle Market, By Wax |

| 6.2.1 Overview and Analysis |

| 6.2.2 China Candle Market Revenues & Volume, By Paraffin, 2021 - 2031F |

| 6.2.3 China Candle Market Revenues & Volume, By Soy Wax, 2021 - 2031F |

| 6.2.4 China Candle Market Revenues & Volume, By Beeswax, 2021 - 2031F |

| 6.2.5 China Candle Market Revenues & Volume, By Palm Wax, 2021 - 2031F |

| 6.2.6 China Candle Market Revenues & Volume, By Others, 2021 - 2031F |

| 6.3 China Candle Market, By Distribution Channel |

| 6.3.1 Overview and Analysis |

| 6.3.2 China Candle Market Revenues & Volume, By Offline, 2021 - 2031F |

| 6.3.3 China Candle Market Revenues & Volume, By Online, 2021 - 2031F |

| 7 China Candle Market Import-Export Trade Statistics |

| 7.1 China Candle Market Export to Major Countries |

| 7.2 China Candle Market Imports from Major Countries |

| 8 China Candle Market Key Performance Indicators |

| 8.1 Percentage of sales from eco-friendly and sustainable candles |

| 8.2 Number of new product launches in the aromatherapy candle segment |

| 8.3 Growth in online sales of candles |

| 8.4 Percentage of revenue from premium candle products |

| 8.5 Customer satisfaction scores for candle quality and fragrance. |

| 9 China Candle Market - Opportunity Assessment |

| 9.1 China Candle Market Opportunity Assessment, By Product Type, 2021 & 2031F |

| 9.2 China Candle Market Opportunity Assessment, By Wax, 2021 & 2031F |

| 9.3 China Candle Market Opportunity Assessment, By Distribution Channel, 2021 & 2031F |

| 10 China Candle Market - Competitive Landscape |

| 10.1 China Candle Market Revenue Share, By Companies, 2024 |

| 10.2 China Candle Market Competitive Benchmarking, By Operating and Technical Parameters |

| 11 Company Profiles |

| 12 Recommendations |

| 13 Disclaimer |

Export potential assessment - trade Analytics for 2030

Export potential enables firms to identify high-growth global markets with greater confidence by combining advanced trade intelligence with a structured quantitative methodology. The framework analyzes emerging demand trends and country-level import patterns while integrating macroeconomic and trade datasets such as GDP and population forecasts, bilateral import–export flows, tariff structures, elasticity differentials between developed and developing economies, geographic distance, and import demand projections. Using weighted trade values from 2020–2024 as the base period to project country-to-country export potential for 2030, these inputs are operationalized through calculated drivers such as gravity model parameters, tariff impact factors, and projected GDP per-capita growth. Through an analysis of hidden potentials, demand hotspots, and market conditions that are most favorable to success, this method enables firms to focus on target countries, maximize returns, and global expansion with data, backed by accuracy.

By factoring in the projected importer demand gap that is currently unmet and could be potential opportunity, it identifies the potential for the Exporter (Country) among 190 countries, against the general trade analysis, which identifies the biggest importer or exporter.

To discover high-growth global markets and optimize your business strategy:

Click Here

Pricing

- Single User License$ 1,995

- Department License$ 2,400

- Site License$ 3,120

- Global License$ 3,795

Search

Thought Leadership and Analyst Meet

Our Clients

Related Reports

- India Switchgear Market Outlook (2026 - 2032) | Size, Share, Trends, Growth, Revenue, Forecast, Analysis, Value, Outlook

- Pakistan Contraceptive Implants Market (2025-2031) | Demand, Growth, Size, Share, Industry, Pricing Analysis, Competitive, Strategic Insights, Strategy, Consumer Insights, Analysis, Investment Trends, Opportunities, Revenue, Segments, Value, Segmentation, Supply, Forecast, Restraints, Outlook, Competition, Drivers, Trends, Companies, Challenges

- Sri Lanka Packaging Market (2026-2032) | Outlook, Competition, Drivers, Trends, Demand, Pricing Analysis, Competitive, Strategic Insights, Companies, Challenges, Strategy, Consumer Insights, Analysis, Investment Trends, Opportunities, Growth, Size, Share, Industry, Revenue, Segments, Value, Segmentation, Supply, Forecast, Restraints

- India Kids Watches Market (2026-2032) | Strategy, Consumer Insights, Analysis, Investment Trends, Opportunities, Growth, Size, Share, Industry, Revenue, Segments, Value, Segmentation, Supply, Forecast, Restraints, Outlook, Competition, Drivers, Trends, Demand, Pricing Analysis, Competitive, Strategic Insights, Companies, Challenges

- Saudi Arabia Core Assurance Service Market (2025-2031) | Strategy, Consumer Insights, Analysis, Investment Trends, Opportunities, Growth, Size, Share, Industry, Revenue, Segments, Value, Segmentation, Supply, Forecast, Restraints, Outlook, Competition, Drivers, Trends, Demand, Pricing Analysis, Competitive, Strategic Insights, Companies, Challenges

- Romania Uninterruptible Power Supply (UPS) Market (2026-2032) | Industry, Analysis, Revenue, Size, Forecast, Outlook, Value, Trends, Share, Growth & Companies

- Saudi Arabia Car Window Tinting Film, Paint Protection Film (PPF), and Ceramic Coating Market (2025-2031) | Strategy, Consumer Insights, Analysis, Investment Trends, Opportunities, Growth, Size, Share, Industry, Revenue, Segments, Value, Segmentation, Supply, Forecast, Restraints, Outlook, Competition, Drivers, Trends, Demand, Pricing Analysis, Competitive, Strategic Insights, Companies, Challenges

- South Africa Stationery Market (2025-2031) | Share, Size, Industry, Value, Growth, Revenue, Analysis, Trends, Segmentation & Outlook

- Afghanistan Rocking Chairs And Adirondack Chairs Market (2026-2032) | Size & Revenue, Competitive Landscape, Share, Segmentation, Industry, Value, Outlook, Analysis, Trends, Growth, Forecast, Companies

- Afghanistan Apparel Market (2026-2032) | Growth, Outlook, Industry, Segmentation, Forecast, Size, Companies, Trends, Value, Share, Analysis & Revenue

Industry Events and Analyst Meet

India EV Show 2026

EV tech India Expo 2026

Auto Tech Asia 2026

Battery Tech India 2026

Smart Production Solutions Guangzhou 2026

Whitepaper

- Middle East & Africa Commercial Security Market Click here to view more.

- Middle East & Africa Fire Safety Systems & Equipment Market Click here to view more.

- GCC Drone Market Click here to view more.

- Middle East Lighting Fixture Market Click here to view more.

- GCC Physical & Perimeter Security Market Click here to view more.

6WResearch In News

- Doha a strategic location for EV manufacturing hub: IPA Qatar

- Demand for luxury TVs surging in the GCC, says Samsung

- Empowering Growth: The Thriving Journey of Bangladesh’s Cable Industry

- Demand for luxury TVs surging in the GCC, says Samsung

- Video call with a traditional healer? Once unthinkable, it’s now common in South Africa

- Intelligent Buildings To Smooth GCC’s Path To Net Zero