Europe Optical Wavelength Services Market (2026-2032) | Analysis, Industry, Growth, Forecast, Size, Value, Share, Companies, Trends & Revenue

Market Forecast by Countries (Germany, United Kingdom, France, Italy, Russia, Spain, Rest of Europe), By Bandwidth (Less than 10 Gbps, 40 Gbps, 100 Gbps, More than 100 Gbps), By Application (Short Haul, Metro, Long Haul), By Interface (SONET, Ethernet, OTN), By Organization Size (SMEs, Large Enterprises) And Competitive Landscape

| Product Code: ETC4609389 | Publication Date: Jul 2023 | Updated Date: Jul 2026 | Product Type: Report | |

| Publisher: 6Wresearch | Author: Ravi Bhandari | No. of Pages: 200 | No. of Figures: 90 | No. of Tables: 30 |

Europe Optical Wavelength Services Market Growth Rate

According to 6Wresearch internal database and industry insights, the Europe Optical Wavelength Services Market is growing at a compound annual growth rate (CAGR) of 8.7% during the forecast period (2026-2032).

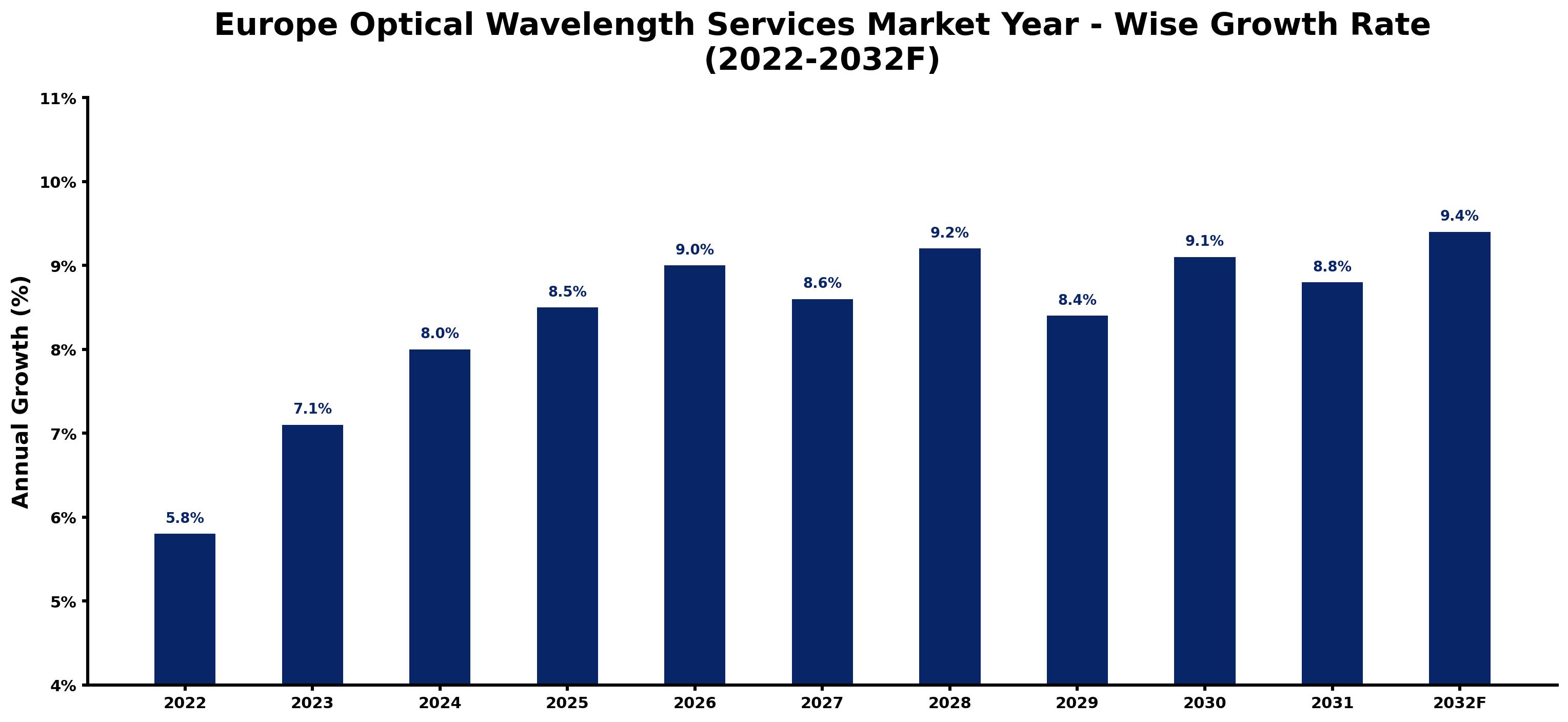

Europe Optical Wavelength Services Market Year-wise Growth Rate and Key Drivers

This graph illustrates the annual growth rates of the Europe Optical Wavelength Services Market from 2022 to 2032, highlighting stable industrial expansion, infrastructure-driven demand, and increasing adoption of precision finishing solutions.

The following table summarizes the historical and forecasted growth rates of the Europe Optical Wavelength Services Market, along with the rationale behind each year’s performance.

| Year | Estimated Growth (%) | Market Rationale |

| 2022 | 5.8% | Gradual recovery in enterprise network investments and fiber infrastructure expansion. |

| 2023 | 7.1% | Rising demand for high-capacity connectivity from cloud service providers and enterprises. |

| 2024 | 8.0% | Increased deployment of metro and long-haul optical networks across Europe. |

| 2025 | 8.5% | Growing adoption of wavelength services by hyperscale data centers and telecom operators. |

| 2026 | 9.0% | Strong investments in digital infrastructure and higher demand for low-latency connectivity. |

| 2027 | 8.6% | Market expansion supported by enterprise digital transformation and interconnection services. |

| 2028 | 9.2% | Accelerated bandwidth requirements driven by AI workloads, cloud computing, and 5G backhaul. |

| 2029 | 8.4% | Stable market growth as network deployments mature in several European countries. |

| 2030 | 9.1% | Increased cross-border connectivity projects and continued hyperscale data center expansion. |

| 2031 | 8.8% | Higher adoption of managed optical networking services across enterprises and carriers. |

| 2032 | 9.4% | Mature market supported by sustained demand for scalable, high-capacity optical wavelength services. |

Topics Covered in the Europe Optical Wavelength Services Market Report

The Europe Optical Wavelength Services Market report thoroughly covers the market by countries, bandwidth, applications, interfaces, and organization size. The market report provides an unbiased and detailed analysis of ongoing market trends, opportunities/high growth areas, and market drivers, which would help stakeholders devise and align their market strategies according to the current and future market dynamics.

Europe Optical Wavelength Services Market Highlights

| Report Name | Europe Optical Wavelength Services Market |

| Forecast Period | 2026-2032 |

| CAGR | 8.7% |

| Growing Sector | Telecommunications |

Europe Optical Wavelength Services Market Synopsis

The Europe Optical Wavelength Services Market will grow as of increased demand for high-speed internet and cloud services and government broadband infrastructure development projects. The telecom industry is experiencing market expansion through its increasing adoption of optical technologies which include the development of 5G networks. The growing data transfer needs of business clients together with their increasing use of advanced optical services drive the demand for optical wavelength services throughout Europe.

Evaluation of Growth Drivers in the Europe Optical Wavelength Services Market

Below mentioned are some growth drivers and their impact on market dynamics:

| Drivers | Primary Segments Affected | Why It Matters |

| Government Support for Broadband Infrastructure | Countries (Germany, UK, France, Italy, etc.) | Improves access to high-speed connectivity, boosting optical wavelength services demand. |

| Rising Data Transmission Demand | Bandwidth (100 Gbps, More than 100 Gbps) | Increases need for high-capacity optical networks in telecom and enterprise sectors. |

| Adoption of 5G Networks | Applications (Metro, Long Haul) | Increases demand for optical services for 5G backhaul and data networks. |

| Cloud Computing and Data Centers | Organization Size (Large Enterprises) | Makes high demand for scalable, high-bandwidth optical wavelength services. |

| Growing Need for Low-Latency Connections | Applications (Short Haul) | Drives demand for real-time data transmission in sensitive applications. |

The Europe Optical Wavelength Services Market is projected to grow significantly, with a CAGR of 8.7% during the forecast period of 2026-2032. The Europe Optical Wavelength Services Market expands as consumers require high-speed internet to access cloud services and 5G networks and data-heavy applications. Further, government initiatives, such as Horizon Europe and the Connecting Europe Facility (CEF), are increasing the investments in digital infrastructure and broadband expansion. The market grows as businesses need high-capacity data services to support their digital operations which technology advancements in optical systems can provide. The increasing trend of digital transformation together with remote work practices creates higher demand for optical wavelength services.

Evaluation of Restraints in the Europe Optical Wavelength Services Market

Below mentioned are some major restraints and their influence on market dynamics:

| Restraints | Primary Segments Affected | What This Means |

| High Infrastructure Costs | Bandwidth (100 Gbps, More than 100 Gbps) | High initial investment limits adoption of advanced optical services. |

| Technological Integration Challenges | Applications (Metro, Long Haul) | Challenges in implementing optical services, especially in legacy networks. |

| Regulatory Hurdles | Countries (Germany, UK, France) | Makes difficulty in expansion and increases compliance costs. |

| Limited Availability of Fiber Optic Infrastructure | Countries (Italy, Russia, Spain) | Lowers delivery of high-capacity services in underserved areas. |

| Competition from Alternative Transmission Technologies | Interface (SONET, Ethernet) | Alternative technologies reduce market share for optical wavelength services. |

Europe Optical Wavelength Services Market Challenges

The Europe Optical Wavelength Services Market faces challenges as deploying optical networks requires expensive infrastructure investments which become especially problematic when implementing 100 Gbps and higher bandwidth services. The process of adopting new optical technologies becomes difficult as telecom companies must integrate these technologies with their current systems which results in both technical and financial difficulties. The different regulatory requirements of various countries create obstacles which slow down the growth of the market.

Europe Optical Wavelength Services Market Trends

Some major trends contributing to the Europe Optical Wavelength Services Market Growth are:

- Cloud Computing and Virtualization: The growing reliance on cloud computing and data centers boosts the need for optical wavelength services for reliable, scalable, and high-bandwidth connectivity.

- Low-Latency Requirements: An increase in orders for services, the lowest latency, mainly from finance and real-time data applications, shapes growth in a short-haul optical service.

- Shift to High-Bandwidth Services: The demand for more than 100 Gbps optical wavelengths is on the rise as enterprises require higher speeds for data-heavy applications and high-capacity networking.

Investment Opportunities in the Europe Optical Wavelength Services Market

Here are some investment opportunities in the Europe Optical Wavelength Services Industry:

- 5G Network Expansion: Investing in optical wavelength services for 5G backhaul presents an opportunity to cater to rising demand for high-speed connections.

- Cloud Data Centers: Making of optical wavelength services tailored to cloud computing and data center connectivity can tap into the growing cloud services market.

- IoT and Smart Cities: As smart cities and IoT applications grow, investing in optical services for connectivity will support the infrastructure of these technologies.

Top 5 Leading Players in the Europe Optical Wavelength Services Market

Here are some top companies contributing to Europe Optical Wavelength Services Market Share:

1. Orange S.A.

| Company Name | Orange S.A. |

| Headquarters | Paris, France |

| Established | 1994 |

| Website | Click Here |

Orange S.A. is a key player in the European optical wavelength services market, providing high-speed optical solutions across Europe. Their strong infrastructure and service portfolio allow them to support 5G and cloud-based connectivity needs.

2. Deutsche Telekom AG

| Company Name | Deutsche Telekom AG |

| Headquarters | Bonn, Germany |

| Established | 1995 |

| Website | Click Here |

Deutsche Telekom offers a wide range of optical wavelength services, including high-capacity fiber optic solutions for enterprise and telecom applications. The company’s expansion in 5G backhaul services is a notable market strength.

3. BT Group

| Company Name | BT Group |

| Headquarters | London, United Kingdom |

| Established | 1981 |

| Website | Click Here |

BT Group provides comprehensive optical wavelength solutions across Europe, with an emphasis on high-bandwidth connectivity for data centers and telecom networks. Their focus on low-latency, high-capacity services caters to growing demands in Europe.

4. Telefónica

| Company Name | Telefónica |

| Headquarters | Madrid, Spain |

| Established | 1924 |

| Website | Click Here |

Telefónica is a leader in optical wavelength services, offering services across Europe. Their investments in fiber optic infrastructure and partnerships with cloud providers enhance their service offerings.

5. Vodafone Group

| Company Name | Vodafone Group |

| Headquarters | Newbury, United Kingdom |

| Established | 1984 |

| Website | Click Here |

Vodafone’s optical wavelength services are widely used across Europe, particularly in metro and long-haul networks. Their investments in 5G networks and fiber-to-the-home (FTTH) services help cater to growing data demands.

Government Regulations Introduced in the Europe Optical Wavelength Services Market

According to European government data, the Europe optical wavelength services market receives its regulatory framework from the European Electronic Communications Code (EECC) which mandates EU member states to establish unified network development standards. The Horizon Europe and Connecting Europe Facility (CEF) programs provide funding for broadband infrastructure initiatives which enable optical service expansion. The initiatives create digital access for all people which results in new technological solutions and develops high-speed optical wavelength networks that deliver superior connectivity to all parts of Europe which strengthens the digital economy.

Future Insights of the Europe Optical Wavelength Services Market

The future outlook for the Europe Optical Wavelength Services Market is promising, with strong growth expected. The market will continue to expand as of the increasing need for high-speed internet and 5G networks and cloud computing services. Government initiatives which improve broadband infrastructure and expand fiber optic deployment will drive market growth. Optical wavelength technology innovations, which focus on high-capacity applications, will enable service providers to develop new offerings that meet rising needs from enterprise clients and telecom operators.

Market Segmentation Analysis

The report offers a comprehensive study of the subsequent market segments and their leading categories.

Germany to Dominate the Market – By Country

According to Guneet Kaur, Senior Research Analyst, the Germany is expected to dominate the market due to its advanced telecom infrastructure, strong optical technology investments, and its key role in Europe's digital economy, driven by 5G and high-capacity data services.

More than 100 Gbps to Dominate the Market – By Bandwidth

The more than 100 Gbps segment leads the market due to increasing demand for high-capacity services in data-heavy applications, such as cloud computing and big data analytics. Enterprises and telecom operators are increasingly adopting services with more than 100 Gbps bandwidth to meet growing data requirements.

Long Haul to Dominate the Market – By Application

The market for optical services across extensive geographic areas has reached its peak demand which drives its current growth. Long haul services enable data center interconnections which create essential links for enterprise networks and worldwide connectivity throughout Europe.

SONET to Dominate the Market – By Interface

SONET interfaces are leading the market. Mainly due to their ability to provide high-speed, reliable optical wavelength services, mainly in metro and long-haul applications. Their compatibility with legacy telecom networks and ability to support high-bandwidth services make them a preferred choice.

Large Enterprises to Dominate the Market – By Organization Size

Large enterprises are leading the market. Mainly driven by their increasing demand for high-speed, scalable optical wavelength services to support cloud-based applications, data centers, and high-capacity enterprise networks.

Key attractiveness of the report

- 10 Years Market Numbers.

- Historical Data Starting from 2022 to 2025.

- Base Year: 2025

- Forecast Data until 2032.

- Key Performance Indicators Impacting the Market.

- Major Upcoming Developments and Projects.

Key Highlights of the Report:

- Europe Optical Wavelength Services Market Outlook

- Market Size of Europe Optical Wavelength Services Market, 2025

- Forecast of Europe Optical Wavelength Services Market, 2032

- Historical Data and Forecast of Europe Optical Wavelength Services Revenues & Volume for the Period 2022 - 2032

- Europe Optical Wavelength Services Market Trend Evolution

- Europe Optical Wavelength Services Market Drivers and Challenges

- Europe Optical Wavelength Services Price Trends

- Europe Optical Wavelength Services Porter's Five Forces

- Europe Optical Wavelength Services Industry Life Cycle

- Historical Data and Forecast of Europe Optical Wavelength Services Market Revenues & Volume By Bandwidth for the Period 2022 - 2032

- Historical Data and Forecast of Europe Optical Wavelength Services Market Revenues & Volume By Less than 10 Gbps for the Period 2022 - 2032

- Historical Data and Forecast of Europe Optical Wavelength Services Market Revenues & Volume By 40 Gbps for the Period 2022 - 2032

- Historical Data and Forecast of Europe Optical Wavelength Services Market Revenues & Volume By 100 Gbps for the Period 2022 - 2032

- Historical Data and Forecast of Europe Optical Wavelength Services Market Revenues & Volume By More than 100 Gbps for the Period 2022 - 2032

- Historical Data and Forecast of Germany Optical Wavelength Services Market Revenues & Volume By Bandwidth for the Period 2022 - 2032

- Historical Data and Forecast of Germany Optical Wavelength Services Market Revenues & Volume By Less than 10 Gbps for the Period 2022 - 2032

- Historical Data and Forecast of Germany Optical Wavelength Services Market Revenues & Volume By 40 Gbps for the Period 2022 - 2032

- Historical Data and Forecast of Germany Optical Wavelength Services Market Revenues & Volume By 100 Gbps for the Period 2022 - 2032

- Historical Data and Forecast of Germany Optical Wavelength Services Market Revenues & Volume By More than 100 Gbps for the Period 2022 - 2032

- Historical Data and Forecast of United Kingdom Optical Wavelength Services Market Revenues & Volume By Bandwidth for the Period 2022 - 2032

- Historical Data and Forecast of United Kingdom Optical Wavelength Services Market Revenues & Volume By Less than 10 Gbps for the Period 2022 - 2032

- Historical Data and Forecast of United Kingdom Optical Wavelength Services Market Revenues & Volume By 40 Gbps for the Period 2022 - 2032

- Historical Data and Forecast of United Kingdom Optical Wavelength Services Market Revenues & Volume By 100 Gbps for the Period 2022 - 2032

- Historical Data and Forecast of United Kingdom Optical Wavelength Services Market Revenues & Volume By More than 100 Gbps for the Period 2022 - 2032

- Historical Data and Forecast of France Optical Wavelength Services Market Revenues & Volume By Bandwidth for the Period 2022 - 2032

- Historical Data and Forecast of France Optical Wavelength Services Market Revenues & Volume By Less than 10 Gbps for the Period 2022 - 2032

- Historical Data and Forecast of France Optical Wavelength Services Market Revenues & Volume By 40 Gbps for the Period 2022 - 2032

- Historical Data and Forecast of France Optical Wavelength Services Market Revenues & Volume By 100 Gbps for the Period 2022 - 2032

- Historical Data and Forecast of France Optical Wavelength Services Market Revenues & Volume By More than 100 Gbps for the Period 2022 - 2032

- Historical Data and Forecast of Italy Optical Wavelength Services Market Revenues & Volume By Bandwidth for the Period 2022 - 2032

- Historical Data and Forecast of Italy Optical Wavelength Services Market Revenues & Volume By Less than 10 Gbps for the Period 2022 - 2032

- Historical Data and Forecast of Italy Optical Wavelength Services Market Revenues & Volume By 40 Gbps for the Period 2022 - 2032

- Historical Data and Forecast of Italy Optical Wavelength Services Market Revenues & Volume By 100 Gbps for the Period 2022 - 2032

- Historical Data and Forecast of Italy Optical Wavelength Services Market Revenues & Volume By More than 100 Gbps for the Period 2022 - 2032

- Historical Data and Forecast of Russia Optical Wavelength Services Market Revenues & Volume By Bandwidth for the Period 2022 - 2032

- Historical Data and Forecast of Russia Optical Wavelength Services Market Revenues & Volume By Less than 10 Gbps for the Period 2022 - 2032

- Historical Data and Forecast of Russia Optical Wavelength Services Market Revenues & Volume By 40 Gbps for the Period 2022 - 2032

- Historical Data and Forecast of Russia Optical Wavelength Services Market Revenues & Volume By 100 Gbps for the Period 2022 - 2032

- Historical Data and Forecast of Russia Optical Wavelength Services Market Revenues & Volume By More than 100 Gbps for the Period 2022 - 2032

- Historical Data and Forecast of Spain Optical Wavelength Services Market Revenues & Volume By Bandwidth for the Period 2022 - 2032

- Historical Data and Forecast of Spain Optical Wavelength Services Market Revenues & Volume By Less than 10 Gbps for the Period 2022 - 2032

- Historical Data and Forecast of Spain Optical Wavelength Services Market Revenues & Volume By 40 Gbps for the Period 2022 - 2032

- Historical Data and Forecast of Spain Optical Wavelength Services Market Revenues & Volume By 100 Gbps for the Period 2022 - 2032

- Historical Data and Forecast of Spain Optical Wavelength Services Market Revenues & Volume By More than 100 Gbps for the Period 2022 - 2032

- Historical Data and Forecast of Rest of Europe Optical Wavelength Services Market Revenues & Volume By Bandwidth for the Period 2022 - 2032

- Historical Data and Forecast of Rest of Europe Optical Wavelength Services Market Revenues & Volume By Less than 10 Gbps for the Period 2022 - 2032

- Historical Data and Forecast of Rest of Europe Optical Wavelength Services Market Revenues & Volume By 40 Gbps for the Period 2022 - 2032

- Historical Data and Forecast of Rest of Europe Optical Wavelength Services Market Revenues & Volume By 100 Gbps for the Period 2022 - 2032

- Historical Data and Forecast of Rest of Europe Optical Wavelength Services Market Revenues & Volume By More than 100 Gbps for the Period 2022 - 2032

- Historical Data and Forecast of Europe Optical Wavelength Services Market Revenues & Volume By Application for the Period 2022 - 2032

- Historical Data and Forecast of Europe Optical Wavelength Services Market Revenues & Volume By Short Haul for the Period 2022 - 2032

- Historical Data and Forecast of Europe Optical Wavelength Services Market Revenues & Volume By Metro for the Period 2022 - 2032

- Historical Data and Forecast of Europe Optical Wavelength Services Market Revenues & Volume By Long Haul for the Period 2022 - 2032

- Historical Data and Forecast of Germany Optical Wavelength Services Market Revenues & Volume By Application for the Period 2022 - 2032

- Historical Data and Forecast of Germany Optical Wavelength Services Market Revenues & Volume By Short Haul for the Period 2022 - 2032

- Historical Data and Forecast of Germany Optical Wavelength Services Market Revenues & Volume By Metro for the Period 2022 - 2032

- Historical Data and Forecast of Germany Optical Wavelength Services Market Revenues & Volume By Long Haul for the Period 2022 - 2032

- Historical Data and Forecast of United Kingdom Optical Wavelength Services Market Revenues & Volume By Application for the Period 2022 - 2032

- Historical Data and Forecast of United Kingdom Optical Wavelength Services Market Revenues & Volume By Short Haul for the Period 2022 - 2032

- Historical Data and Forecast of United Kingdom Optical Wavelength Services Market Revenues & Volume By Metro for the Period 2022 - 2032

- Historical Data and Forecast of United Kingdom Optical Wavelength Services Market Revenues & Volume By Long Haul for the Period 2022 - 2032

- Historical Data and Forecast of France Optical Wavelength Services Market Revenues & Volume By Application for the Period 2022 - 2032

- Historical Data and Forecast of France Optical Wavelength Services Market Revenues & Volume By Short Haul for the Period 2022 - 2032

- Historical Data and Forecast of France Optical Wavelength Services Market Revenues & Volume By Metro for the Period 2022 - 2032

- Historical Data and Forecast of France Optical Wavelength Services Market Revenues & Volume By Long Haul for the Period 2022 - 2032

- Historical Data and Forecast of Italy Optical Wavelength Services Market Revenues & Volume By Application for the Period 2022 - 2032

- Historical Data and Forecast of Italy Optical Wavelength Services Market Revenues & Volume By Short Haul for the Period 2022 - 2032

- Historical Data and Forecast of Italy Optical Wavelength Services Market Revenues & Volume By Metro for the Period 2022 - 2032

- Historical Data and Forecast of Italy Optical Wavelength Services Market Revenues & Volume By Long Haul for the Period 2022 - 2032

- Historical Data and Forecast of Russia Optical Wavelength Services Market Revenues & Volume By Application for the Period 2022 - 2032

- Historical Data and Forecast of Russia Optical Wavelength Services Market Revenues & Volume By Short Haul for the Period 2022 - 2032

- Historical Data and Forecast of Russia Optical Wavelength Services Market Revenues & Volume By Metro for the Period 2022 - 2032

- Historical Data and Forecast of Russia Optical Wavelength Services Market Revenues & Volume By Long Haul for the Period 2022 - 2032

- Historical Data and Forecast of Spain Optical Wavelength Services Market Revenues & Volume By Application for the Period 2022 - 2032

- Historical Data and Forecast of Spain Optical Wavelength Services Market Revenues & Volume By Short Haul for the Period 2022 - 2032

- Historical Data and Forecast of Spain Optical Wavelength Services Market Revenues & Volume By Metro for the Period 2022 - 2032

- Historical Data and Forecast of Spain Optical Wavelength Services Market Revenues & Volume By Long Haul for the Period 2022 - 2032

- Historical Data and Forecast of Rest of Europe Optical Wavelength Services Market Revenues & Volume By Application for the Period 2022 - 2032

- Historical Data and Forecast of Rest of Europe Optical Wavelength Services Market Revenues & Volume By Short Haul for the Period 2022 - 2032

- Historical Data and Forecast of Rest of Europe Optical Wavelength Services Market Revenues & Volume By Metro for the Period 2022 - 2032

- Historical Data and Forecast of Rest of Europe Optical Wavelength Services Market Revenues & Volume By Long Haul for the Period 2022 - 2032

- Historical Data and Forecast of Europe Optical Wavelength Services Market Revenues & Volume By Interface for the Period 2022 - 2032

- Historical Data and Forecast of Europe Optical Wavelength Services Market Revenues & Volume By SONET for the Period 2022 - 2032

- Historical Data and Forecast of Europe Optical Wavelength Services Market Revenues & Volume By Ethernet for the Period 2022 - 2032

- Historical Data and Forecast of Europe Optical Wavelength Services Market Revenues & Volume By OTN for the Period 2022 - 2032

- Historical Data and Forecast of Germany Optical Wavelength Services Market Revenues & Volume By Interface for the Period 2022 - 2032

- Historical Data and Forecast of Germany Optical Wavelength Services Market Revenues & Volume By SONET for the Period 2022 - 2032

- Historical Data and Forecast of Germany Optical Wavelength Services Market Revenues & Volume By Ethernet for the Period 2022 - 2032

- Historical Data and Forecast of Germany Optical Wavelength Services Market Revenues & Volume By OTN for the Period 2022 - 2032

- Historical Data and Forecast of United Kingdom Optical Wavelength Services Market Revenues & Volume By Interface for the Period 2022 - 2032

- Historical Data and Forecast of United Kingdom Optical Wavelength Services Market Revenues & Volume By SONET for the Period 2022 - 2032

- Historical Data and Forecast of United Kingdom Optical Wavelength Services Market Revenues & Volume By Ethernet for the Period 2022 - 2032

- Historical Data and Forecast of United Kingdom Optical Wavelength Services Market Revenues & Volume By OTN for the Period 2022 - 2032

- Historical Data and Forecast of France Optical Wavelength Services Market Revenues & Volume By Interface for the Period 2022 - 2032

- Historical Data and Forecast of France Optical Wavelength Services Market Revenues & Volume By SONET for the Period 2022 - 2032

- Historical Data and Forecast of France Optical Wavelength Services Market Revenues & Volume By Ethernet for the Period 2022 - 2032

- Historical Data and Forecast of France Optical Wavelength Services Market Revenues & Volume By OTN for the Period 2022 - 2032

- Historical Data and Forecast of Italy Optical Wavelength Services Market Revenues & Volume By Interface for the Period 2022 - 2032

- Historical Data and Forecast of Italy Optical Wavelength Services Market Revenues & Volume By SONET for the Period 2022 - 2032

- Historical Data and Forecast of Italy Optical Wavelength Services Market Revenues & Volume By Ethernet for the Period 2022 - 2032

- Historical Data and Forecast of Italy Optical Wavelength Services Market Revenues & Volume By OTN for the Period 2022 - 2032

- Historical Data and Forecast of Russia Optical Wavelength Services Market Revenues & Volume By Interface for the Period 2022 - 2032

- Historical Data and Forecast of Russia Optical Wavelength Services Market Revenues & Volume By SONET for the Period 2022 - 2032

- Historical Data and Forecast of Russia Optical Wavelength Services Market Revenues & Volume By Ethernet for the Period 2022 - 2032

- Historical Data and Forecast of Russia Optical Wavelength Services Market Revenues & Volume By OTN for the Period 2022 - 2032

- Historical Data and Forecast of Spain Optical Wavelength Services Market Revenues & Volume By Interface for the Period 2022 - 2032

- Historical Data and Forecast of Spain Optical Wavelength Services Market Revenues & Volume By SONET for the Period 2022 - 2032

- Historical Data and Forecast of Spain Optical Wavelength Services Market Revenues & Volume By Ethernet for the Period 2022 - 2032

- Historical Data and Forecast of Spain Optical Wavelength Services Market Revenues & Volume By OTN for the Period 2022 - 2032

- Historical Data and Forecast of Rest of Europe Optical Wavelength Services Market Revenues & Volume By Interface for the Period 2022 - 2032

- Historical Data and Forecast of Rest of Europe Optical Wavelength Services Market Revenues & Volume By SONET for the Period 2022 - 2032

- Historical Data and Forecast of Rest of Europe Optical Wavelength Services Market Revenues & Volume By Ethernet for the Period 2022 - 2032

- Historical Data and Forecast of Rest of Europe Optical Wavelength Services Market Revenues & Volume By OTN for the Period 2022 - 2032

- Historical Data and Forecast of Europe Optical Wavelength Services Market Revenues & Volume By Organization Size for the Period 2022 - 2032

- Historical Data and Forecast of Europe Optical Wavelength Services Market Revenues & Volume By SMEs for the Period 2022 - 2032

- Historical Data and Forecast of Europe Optical Wavelength Services Market Revenues & Volume By Large Enterprises for the Period 2022 - 2032

- Historical Data and Forecast of Germany Optical Wavelength Services Market Revenues & Volume By Organization Size for the Period 2022 - 2032

- Historical Data and Forecast of Germany Optical Wavelength Services Market Revenues & Volume By SMEs for the Period 2022 - 2032

- Historical Data and Forecast of Germany Optical Wavelength Services Market Revenues & Volume By Large Enterprises for the Period 2022 - 2032

- Historical Data and Forecast of United Kingdom Optical Wavelength Services Market Revenues & Volume By Organization Size for the Period 2022 - 2032

- Historical Data and Forecast of United Kingdom Optical Wavelength Services Market Revenues & Volume By SMEs for the Period 2022 - 2032

- Historical Data and Forecast of United Kingdom Optical Wavelength Services Market Revenues & Volume By Large Enterprises for the Period 2022 - 2032

- Historical Data and Forecast of France Optical Wavelength Services Market Revenues & Volume By Organization Size for the Period 2022 - 2032

- Historical Data and Forecast of France Optical Wavelength Services Market Revenues & Volume By SMEs for the Period 2022 - 2032

- Historical Data and Forecast of France Optical Wavelength Services Market Revenues & Volume By Large Enterprises for the Period 2022 - 2032

- Historical Data and Forecast of Italy Optical Wavelength Services Market Revenues & Volume By Organization Size for the Period 2022 - 2032

- Historical Data and Forecast of Italy Optical Wavelength Services Market Revenues & Volume By SMEs for the Period 2022 - 2032

- Historical Data and Forecast of Italy Optical Wavelength Services Market Revenues & Volume By Large Enterprises for the Period 2022 - 2032

- Historical Data and Forecast of Russia Optical Wavelength Services Market Revenues & Volume By Organization Size for the Period 2022 - 2032

- Historical Data and Forecast of Russia Optical Wavelength Services Market Revenues & Volume By SMEs for the Period 2022 - 2032

- Historical Data and Forecast of Russia Optical Wavelength Services Market Revenues & Volume By Large Enterprises for the Period 2022 - 2032

- Historical Data and Forecast of Spain Optical Wavelength Services Market Revenues & Volume By Organization Size for the Period 2022 - 2032

- Historical Data and Forecast of Spain Optical Wavelength Services Market Revenues & Volume By SMEs for the Period 2022 - 2032

- Historical Data and Forecast of Spain Optical Wavelength Services Market Revenues & Volume By Large Enterprises for the Period 2022 - 2032

- Historical Data and Forecast of Rest of Europe Optical Wavelength Services Market Revenues & Volume By Organization Size for the Period 2022 - 2032

- Historical Data and Forecast of Rest of Europe Optical Wavelength Services Market Revenues & Volume By SMEs for the Period 2022 - 2032

- Historical Data and Forecast of Rest of Europe Optical Wavelength Services Market Revenues & Volume By Large Enterprises for the Period 2022 - 2032

- Europe Optical Wavelength Services Market - Key Performance Indicators

- Europe Optical Wavelength Services Market - Import Export Trade Statistics

- Europe Optical Wavelength Services Market - Opportunity Assessment By Countries

- Europe Optical Wavelength Services Market - Opportunity Assessment By Bandwidth

- Europe Optical Wavelength Services Market - Opportunity Assessment By Application

- Europe Optical Wavelength Services Market - Opportunity Assessment By Interface

- Europe Optical Wavelength Services Market - Opportunity Assessment By Organization Size

- Europe Optical Wavelength Services Market - Top Companies Market Share

- Europe Optical Wavelength Services Market - Top Companies Profiles

- Europe Optical Wavelength Services Market - Comparison of Players in Technical and Operating Parameters

- Europe Optical Wavelength Services Market - Strategic Recommendations

Market covered

The report subsequently covers the market by following segments and subsegments.

By Countries

- Germany

- United Kingdom

- France

- Italy

- Russia

- Spain

- Rest of Europe

By Bandwidth

- Less than 10 Gbps

- 40 Gbps

- 100 Gbps

- More than 100 Gbps

By Application

- Short Haul

- Metro

- Long Haul

By Interface

- SONET

- Ethernet

- OTN

By Organization Size

- SMEs

- Large Enterprises

Europe Optical Wavelength Services Market (2026-2032): FAQs

The Europe Optical Wavelength Services Market is projected to grow at a CAGR of 8.7%during the forecast period.

There are advancements in 5G, cloud technologies, and high-capacity optical services are enhancing data transmission and improving network efficiency.

The market growth drivers include of the demand for higher bandwidth and rising data consumption in telecom and enterprise sectors.

The market opportunities include 5G backhaul services and infrastructure development in underserved regions.

6Wresearch actively monitors the Europe Optical Wavelength Services Market and publishes its comprehensive annual report, highlighting emerging trends, growth drivers, revenue analysis, and forecast outlook. Our insights help businesses to make data-backed strategic decisions with ongoing market dynamics. Our analysts track relevent industries related to the Europe Optical Wavelength Services Market, allowing our clients with actionable intelligence and reliable forecasts tailored to emerging regional needs.

Yes, we provide customisation as per your requirements. To learn more, feel free to contact us on sales@6wresearch.com

|

1 Executive Summary |

|

2 Introduction |

|

2.1 Key Highlights of the Report |

|

2.2 Report Description |

|

2.3 Market Scope & Segmentation |

|

2.4 Research Methodology |

|

2.5 Assumptions |

|

3 Europe Optical Wavelength Services Market Overview |

|

3.1 Europe Regional Macro Economic Indicators |

|

3.2 Europe Optical Wavelength Services Market Revenues & Volume, 2022 & 2032F |

|

3.3 Europe Optical Wavelength Services Market - Industry Life Cycle |

|

3.4 Europe Optical Wavelength Services Market - Porter's Five Forces |

|

3.5 Europe Optical Wavelength Services Market Revenues & Volume Share, By Countries, 2022 & 2032F |

|

3.6 Europe Optical Wavelength Services Market Revenues & Volume Share, By Bandwidth, 2022 & 2032F |

|

3.7 Europe Optical Wavelength Services Market Revenues & Volume Share, By Application, 2022 & 2032F |

|

3.8 Europe Optical Wavelength Services Market Revenues & Volume Share, By Interface, 2022 & 2032F |

|

3.9 Europe Optical Wavelength Services Market Revenues & Volume Share, By Organization Size, 2022 & 2032F |

|

4 Europe Optical Wavelength Services Market Dynamics |

|

4.1 Impact Analysis |

|

4.2 Market Drivers |

|

4.3 Market Restraints |

|

5 Europe Optical Wavelength Services Market Trends |

|

6 Europe Optical Wavelength Services Market, 2022 - 2032 |

|

6.1 Europe Optical Wavelength Services Market, Revenues & Volume, By Bandwidth, 2022 - 2032 |

|

6.2 Europe Optical Wavelength Services Market, Revenues & Volume, By Application, 2022 - 2032 |

|

6.3 Europe Optical Wavelength Services Market, Revenues & Volume, By Interface, 2022 - 2032 |

|

6.4 Europe Optical Wavelength Services Market, Revenues & Volume, By Organization Size, 2022 - 2032 |

|

7 Germany Optical Wavelength Services Market, 2022 - 2032 |

|

7.1 Germany Optical Wavelength Services Market, Revenues & Volume, By Bandwidth, 2022 - 2032 |

|

7.2 Germany Optical Wavelength Services Market, Revenues & Volume, By Application, 2022 - 2032 |

|

7.3 Germany Optical Wavelength Services Market, Revenues & Volume, By Interface, 2022 - 2032 |

|

7.4 Germany Optical Wavelength Services Market, Revenues & Volume, By Organization Size, 2022 - 2032 |

|

8 United Kingdom Optical Wavelength Services Market, 2022 - 2032 |

|

8.1 United Kingdom Optical Wavelength Services Market, Revenues & Volume, By Bandwidth, 2022 - 2032 |

|

8.2 United Kingdom Optical Wavelength Services Market, Revenues & Volume, By Application, 2022 - 2032 |

|

8.3 United Kingdom Optical Wavelength Services Market, Revenues & Volume, By Interface, 2022 - 2032 |

|

8.4 United Kingdom Optical Wavelength Services Market, Revenues & Volume, By Organization Size, 2022 - 2032 |

|

9 France Optical Wavelength Services Market, 2022 - 2032 |

|

9.1 France Optical Wavelength Services Market, Revenues & Volume, By Bandwidth, 2022 - 2032 |

|

9.2 France Optical Wavelength Services Market, Revenues & Volume, By Application, 2022 - 2032 |

|

9.3 France Optical Wavelength Services Market, Revenues & Volume, By Interface, 2022 - 2032 |

|

9.4 France Optical Wavelength Services Market, Revenues & Volume, By Organization Size, 2022 - 2032 |

|

10 Italy Optical Wavelength Services Market, 2022 - 2032 |

|

10.1 Italy Optical Wavelength Services Market, Revenues & Volume, By Bandwidth, 2022 - 2032 |

|

10.2 Italy Optical Wavelength Services Market, Revenues & Volume, By Application, 2022 - 2032 |

|

10.3 Italy Optical Wavelength Services Market, Revenues & Volume, By Interface, 2022 - 2032 |

|

10.4 Italy Optical Wavelength Services Market, Revenues & Volume, By Organization Size, 2022 - 2032 |

|

11 Russia Optical Wavelength Services Market, 2022 - 2032 |

|

11.1 Russia Optical Wavelength Services Market, Revenues & Volume, By Bandwidth, 2022 - 2032 |

|

11.2 Russia Optical Wavelength Services Market, Revenues & Volume, By Application, 2022 - 2032 |

|

11.3 Russia Optical Wavelength Services Market, Revenues & Volume, By Interface, 2022 - 2032 |

|

11.4 Russia Optical Wavelength Services Market, Revenues & Volume, By Organization Size, 2022 - 2032 |

|

12 Spain Optical Wavelength Services Market, 2022 - 2032 |

|

12.1 Spain Optical Wavelength Services Market, Revenues & Volume, By Bandwidth, 2022 - 2032 |

|

12.2 Spain Optical Wavelength Services Market, Revenues & Volume, By Application, 2022 - 2032 |

|

12.3 Spain Optical Wavelength Services Market, Revenues & Volume, By Interface, 2022 - 2032 |

|

12.4 Spain Optical Wavelength Services Market, Revenues & Volume, By Organization Size, 2022 - 2032 |

|

13 Rest of Europe Optical Wavelength Services Market, 2022 - 2032 |

|

13.1 Rest of Europe Optical Wavelength Services Market, Revenues & Volume, By Bandwidth, 2022 - 2032 |

|

13.2 Rest of Europe Optical Wavelength Services Market, Revenues & Volume, By Application, 2022 - 2032 |

|

13.3 Rest of Europe Optical Wavelength Services Market, Revenues & Volume, By Interface, 2022 - 2032 |

|

13.4 Rest of Europe Optical Wavelength Services Market, Revenues & Volume, By Organization Size, 2022 - 2032 |

|

14 Europe Optical Wavelength Services Market Key Performance Indicators |

|

15 Europe Optical Wavelength Services Market - Opportunity Assessment |

|

15.1 Europe Optical Wavelength Services Market Opportunity Assessment, By Countries, 2022 & 2032F |

|

15.2 Europe Optical Wavelength Services Market Opportunity Assessment, By Bandwidth, 2022 & 2032F |

|

15.3 Europe Optical Wavelength Services Market Opportunity Assessment, By Application, 2022 & 2032F |

|

15.4 Europe Optical Wavelength Services Market Opportunity Assessment, By Interface, 2022 & 2032F |

|

15.5 Europe Optical Wavelength Services Market Opportunity Assessment, By Organization Size, 2022 & 2032F |

|

16 Europe Optical Wavelength Services Market - Competitive Landscape |

|

16.1 Europe Optical Wavelength Services Market Revenue Share, By Companies, 2025 |

|

16.2 Europe Optical Wavelength Services Market Competitive Benchmarking, By Operating and Technical Parameters |

|

17 Company Profiles |

|

18 Recommendations |

|

19 Disclaimer |

Global Go To Market Strategy - 2030

Export potential enables firms to identify high-growth global markets with greater confidence by combining advanced trade intelligence with a structured quantitative methodology. The framework analyzes emerging demand trends and country-level import patterns while integrating macroeconomic and trade datasets such as GDP and population forecasts, bilateral import–export flows, tariff structures, elasticity differentials between developed and developing economies, geographic distance, and import demand projections. Using weighted trade values from 2020–2024 as the base period to project country-to-country export potential for 2030, these inputs are operationalized through calculated drivers such as gravity model parameters, tariff impact factors, and projected GDP per-capita growth. Through an analysis of hidden potentials, demand hotspots, and market conditions that are most favorable to success, this method enables firms to focus on target countries, maximize returns, and global expansion with data, backed by accuracy.

By factoring in the projected importer demand gap that is currently unmet and could be potential opportunity, it identifies the potential for the Exporter (Country) among 190 countries, against the general trade analysis, which identifies the biggest importer or exporter.

To discover high-growth global markets and optimize your business strategy:

Click Here

Pricing

- Single User License$ 4,560

- Department License$ 5,055

- Site License$ 5,595

- Global License$ 6,000

Leadership Perspectives from Industry Events

Search

Thought Leadership and Analyst Meet

Our Clients

6WResearch In News

- India Export Attractiveness Tracker 2026

- India Air Conditioner Market Set for Strong Rebound in 2026 After Weather-Led Correction and GST-Driven Recovery: 6Wresearch

- ADAS in India: How Automatic Emergency Braking, Blind Spot Detection & Driver Monitoring are Transforming Road Safety

- Doha a strategic location for EV manufacturing hub: IPA Qatar

- Demand for luxury TVs surging in the GCC, says Samsung

- Empowering Growth: The Thriving Journey of Bangladesh’s Cable Industry

Latest Reports

- Greece Insulated Sandwich Panels Market (2026-2032)

- Qatar Access and Home Network Market (2026-2032)

- Nicaragua RPG Gaming Market (2026-2032)

- New Zealand RPG Gaming Market (2026-2032)

- Netherlands RPG Gaming Market (2026-2032)

- Nauru RPG Gaming Market (2026-2032)

- Namibia RPG Gaming Market (2026-2032)

- Mozambique RPG Gaming Market (2026-2032)

- Montenegro RPG Gaming Market (2026-2032)

- Mongolia RPG Gaming Market (2026-2032)

Industry Events and Analyst Meet

EV India Expo 2026

HIMTEX 2026

India Refining Summit 2026

India EV Show 2026

EV tech India Expo 2026

Whitepaper

- Middle East & Africa Commercial Security Market Click here to view more.

- Middle East & Africa Fire Safety Systems & Equipment Market Click here to view more.

- GCC Drone Market Click here to view more.

- Middle East Lighting Fixture Market Click here to view more.

- GCC Physical & Perimeter Security Market Click here to view more.