France Automotive Biofuels Market (2025-2031) | Revenue, Value, Pricing Analysis, Size, Regulations, Companies, Strategic Insights, Technological Advancements, Growth, Consumer Insights, Innovation, Competition, Restraints, Opportunities, Supply, Outlook, Future Prospects, Analysis, Segments, Landscape, Trends, Strategy, Industry, Demand, Competitive Landscape, Drivers, Investment Trends, Forecast, Challenges, Market Penetration, Share, Segmentation

Market Forecast By Type (Ethanol, Biodiesel, Renewable Diesel, Bioethanol), By Feedstock (Sugarcane, Corn, Vegetable Oil, Algae, Waste Oils, Agricultural Waste), By Vehicle Type (Passenger Cars, Commercial Vehicles, Electric Vehicles, Heavy-Duty Trucks) And Competitive Landscape

| Product Code: ETC10801801 | Publication Date: Apr 2025 | Updated Date: Nov 2025 | Product Type: Market Research Report | |

| Publisher: 6Wresearch | Author: Summon Dutta | No. of Pages: 65 | No. of Figures: 34 | No. of Tables: 19 |

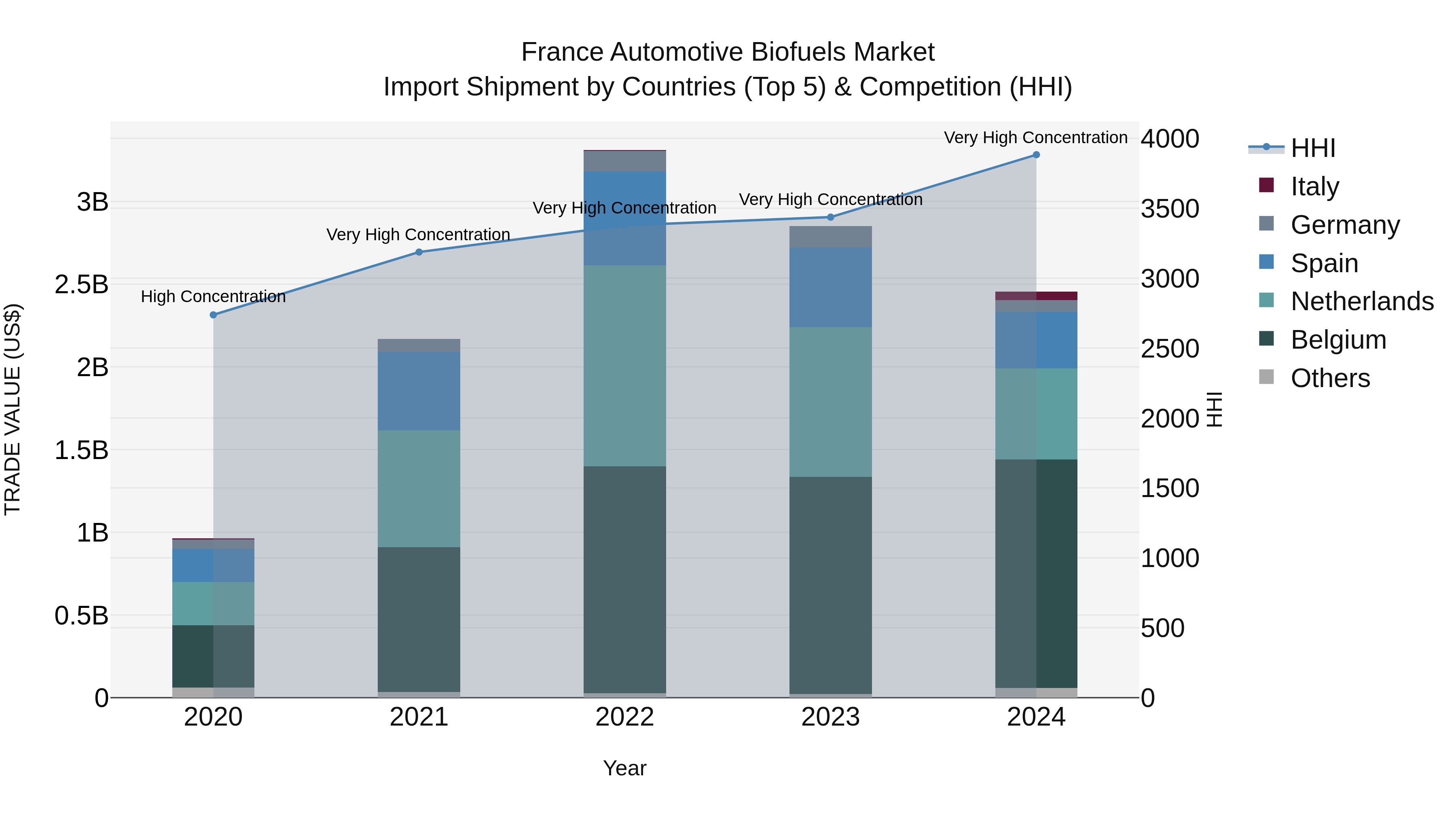

France Automotive Biofuels Market Top 5 Importing Countries and Market Competition (HHI) Analysis

In 2024, France continued to heavily rely on imports of automotive biofuels, with key suppliers including Belgium, Netherlands, Spain, Germany, and Italy. Despite a high level of market concentration indicated by the Herfindahl-Hirschman Index (HHI), the industry experienced significant growth with a compound annual growth rate (CAGR) of 26.32% from 2020 to 2024. However, there was a slight decline in growth rate from 2023 to 2024, reflecting a challenging year for the sector. France`s dependence on these import sources underscores the importance of diversifying supply chains and enhancing domestic biofuel production capabilities.

France Automotive Biofuels Market Overview

The France automotive biofuels market is characterized by steady growth, driven by stringent EU emissions regulations, strong governmental support, and a national commitment to renewable energy transition. France is among the leading biofuel consumers in Europe, with biodiesel (mainly from rapeseed oil) dominating the market, followed by bioethanol blended in gasoline. The Energy Transition for Green Growth Act and tax incentives have encouraged biofuel production and adoption. However, sustainability criteria, such as restrictions on palm oil-based biofuels, are influencing feedstock selection and investment decisions. Advanced biofuels, derived from waste and non-food sources, are gaining traction, supported by rising R&D and pilot projects. Despite challenges like fluctuating feedstock prices and competition from electric vehicles, the automotive biofuels sector in France remains resilient, with anticipated moderate growth as blending mandates rise and decarbonization efforts intensify toward meeting Franceâs 2030 and 2050 climate targets.

Trends of the Market

The France automotive biofuels market is experiencing steady growth, driven by stringent EU and national policies focused on reducing carbon emissions and increasing renewable energy adoption in transportation. Key trends include rising demand for advanced biofuels, such as second-generation biodiesel and bioethanol made from non-food biomass, to comply with Franceâs ambitious targets under the Renewable Energy Directive II. The market is also witnessing increased investments in domestic biofuel production facilities and technological innovations to enhance fuel efficiency and sustainability. Additionally, collaborations between fuel companies and agricultural sectors are intensifying to ensure a stable supply of feedstock. However, challenges remain, including competition from electric vehicles, fluctuating feedstock prices, and the need for further infrastructure development to support higher biofuel blends. Overall, the market outlook remains positive, supported by regulatory incentives and a growing focus on decarbonizing road transport.

Challenges of the Market

The France automotive biofuels market faces several challenges that hinder its growth and adoption. Stringent European Union sustainability regulations and evolving national policies create uncertainty for producers and investors. High production costs, particularly for advanced biofuels, and limited availability of feedstocks such as sustainable crops and waste materials, constrain supply. The dominance of traditional fossil fuels and the increasing focus on electrification in the French automotive sector further dampen demand for biofuels. Additionally, infrastructure limitations, such as insufficient distribution networks and blending facilities, restrict market expansion. Public perception concerns regarding land use changes and food versus fuel debates pose further obstacles. Collectively, these factors challenge the scalability and competitiveness of biofuels in Franceâs transition toward greener transportation solutions.

Investment Opportunities of the market

The France automotive biofuels market offers promising investment opportunities driven by stringent EU emissions regulations, government incentives for renewable energy, and increasing demand for sustainable mobility solutions. Key areas include the production and distribution of advanced biofuels such as biodiesel (from waste oils and agricultural residues) and bioethanol (from non-food feedstocks), which benefit from favorable policies and blending mandates. Investments in R&D for next-generation biofuels, supply chain infrastructure, and partnerships with automotive OEMs for flex-fuel vehicle adoption also present growth prospects. Additionally, Franceâs commitment to carbon neutrality by 2050 and its robust agricultural sector provide a strong foundation for innovative projects, particularly in waste-to-energy and circular economy models. Overall, the market is attractive for investors focused on clean energy, technological innovation, and long-term sustainability.

Government Policy of the market

The French government actively promotes the use of biofuels in the automotive sector as part of its broader climate goals and commitment to reducing greenhouse gas emissions. Key policies include blending mandates that require a certain percentage of bioethanol (E10 and E85) and biodiesel (B7 and B10) in conventional fuels, supported by tax incentives and reduced excise duties for biofuel blends. France also aligns with the European Unionâs Renewable Energy Directive (RED II), which sets targets for renewable energy use in transport. Additionally, the government invests in research, infrastructure, and domestic production of sustainable biofuels, while restricting the use of food-crop-based biofuels to favor advanced, second-generation options. These policies collectively aim to support local agriculture, enhance energy security, and accelerate the decarbonization of the transport sector.

Future Outlook of the market

The future outlook for the France automotive biofuels market is positive, driven by stringent government regulations targeting carbon emissions and the promotion of renewable energy sources in transportation. Franceâs commitment to the EUâs Green Deal and Fit for 55 targets is accelerating the adoption of biofuels, particularly advanced biodiesel and bioethanol blends. Investments in bio-refineries and incentives for low-carbon fuels are boosting domestic production. However, challenges such as feedstock availability, competition from electric vehicles, and evolving sustainability criteria may temper rapid growth. Despite these hurdles, the market is expected to expand steadily through 2030, supported by regulatory mandates, technological advancements, and increasing consumer and corporate demand for cleaner mobility solutions.

Key Highlights of the Report:

- France Automotive Biofuels Market Outlook

- Market Size of France Automotive Biofuels Market, 2024

- Forecast of France Automotive Biofuels Market, 2031

- Historical Data and Forecast of France Automotive Biofuels Revenues & Volume for the Period 2022-2031

- France Automotive Biofuels Market Trend Evolution

- France Automotive Biofuels Market Drivers and Challenges

- France Automotive Biofuels Price Trends

- France Automotive Biofuels Porter's Five Forces

- France Automotive Biofuels Industry Life Cycle

- Historical Data and Forecast of France Automotive Biofuels Market Revenues & Volume By Type for the Period 2022-2031

- Historical Data and Forecast of France Automotive Biofuels Market Revenues & Volume By Ethanol for the Period 2022-2031

- Historical Data and Forecast of France Automotive Biofuels Market Revenues & Volume By Biodiesel for the Period 2022-2031

- Historical Data and Forecast of France Automotive Biofuels Market Revenues & Volume By Renewable Diesel for the Period 2022-2031

- Historical Data and Forecast of France Automotive Biofuels Market Revenues & Volume By Bioethanol for the Period 2022-2031

- Historical Data and Forecast of France Automotive Biofuels Market Revenues & Volume By Feedstock for the Period 2022-2031

- Historical Data and Forecast of France Automotive Biofuels Market Revenues & Volume By Sugarcane, Corn for the Period 2022-2031

- Historical Data and Forecast of France Automotive Biofuels Market Revenues & Volume By Vegetable Oil for the Period 2022-2031

- Historical Data and Forecast of France Automotive Biofuels Market Revenues & Volume By Algae, Waste Oils for the Period 2022-2031

- Historical Data and Forecast of France Automotive Biofuels Market Revenues & Volume By Agricultural Waste for the Period 2022-2031

- Historical Data and Forecast of France Automotive Biofuels Market Revenues & Volume By Vehicle Type for the Period 2022-2031

- Historical Data and Forecast of France Automotive Biofuels Market Revenues & Volume By Passenger Cars for the Period 2022-2031

- Historical Data and Forecast of France Automotive Biofuels Market Revenues & Volume By Commercial Vehicles for the Period 2022-2031

- Historical Data and Forecast of France Automotive Biofuels Market Revenues & Volume By Electric Vehicles for the Period 2022-2031

- Historical Data and Forecast of France Automotive Biofuels Market Revenues & Volume By Heavy-Duty Trucks for the Period 2022-2031

- France Automotive Biofuels Import Export Trade Statistics

- Market Opportunity Assessment By Type

- Market Opportunity Assessment By Feedstock

- Market Opportunity Assessment By Vehicle Type

- France Automotive Biofuels Top Companies Market Share

- France Automotive Biofuels Competitive Benchmarking By Technical and Operational Parameters

- France Automotive Biofuels Company Profiles

- France Automotive Biofuels Key Strategic Recommendations

Frequently Asked Questions About the Market Study (FAQs):

6Wresearch actively monitors the France Automotive Biofuels Market and publishes its comprehensive annual report, highlighting emerging trends, growth drivers, revenue analysis, and forecast outlook. Our insights help businesses to make data-backed strategic decisions with ongoing market dynamics. Our analysts track relevent industries related to the France Automotive Biofuels Market, allowing our clients with actionable intelligence and reliable forecasts tailored to emerging regional needs.

Yes, we provide customisation as per your requirements. To learn more, feel free to contact us on sales@6wresearch.com

1 Executive Summary |

2 Introduction |

2.1 Key Highlights of the Report |

2.2 Report Description |

2.3 Market Scope & Segmentation |

2.4 Research Methodology |

2.5 Assumptions |

3 France Automotive Biofuels Market Overview |

3.1 France Country Macro Economic Indicators |

3.2 France Automotive Biofuels Market Revenues & Volume, 2024 & 2031F |

3.3 France Automotive Biofuels Market - Industry Life Cycle |

3.4 France Automotive Biofuels Market - Porter's Five Forces |

3.5 France Automotive Biofuels Market Revenues & Volume Share, By Type, 2024 & 2031F |

3.6 France Automotive Biofuels Market Revenues & Volume Share, By Feedstock, 2024 & 2031F |

3.7 France Automotive Biofuels Market Revenues & Volume Share, By Vehicle Type, 2024 & 2031F |

4 France Automotive Biofuels Market Dynamics |

4.1 Impact Analysis |

4.2 Market Drivers |

4.3 Market Restraints |

5 France Automotive Biofuels Market Trends |

6 France Automotive Biofuels Market, By Types |

6.1 France Automotive Biofuels Market, By Type |

6.1.1 Overview and Analysis |

6.1.2 France Automotive Biofuels Market Revenues & Volume, By Type, 2022 - 2031F |

6.1.3 France Automotive Biofuels Market Revenues & Volume, By Ethanol, 2022 - 2031F |

6.1.4 France Automotive Biofuels Market Revenues & Volume, By Biodiesel, 2022 - 2031F |

6.1.5 France Automotive Biofuels Market Revenues & Volume, By Renewable Diesel, 2022 - 2031F |

6.1.6 France Automotive Biofuels Market Revenues & Volume, By Bioethanol, 2022 - 2031F |

6.2 France Automotive Biofuels Market, By Feedstock |

6.2.1 Overview and Analysis |

6.2.2 France Automotive Biofuels Market Revenues & Volume, By Sugarcane, Corn, 2022 - 2031F |

6.2.3 France Automotive Biofuels Market Revenues & Volume, By Vegetable Oil, 2022 - 2031F |

6.2.4 France Automotive Biofuels Market Revenues & Volume, By Algae, Waste Oils, 2022 - 2031F |

6.2.5 France Automotive Biofuels Market Revenues & Volume, By Agricultural Waste, 2022 - 2031F |

6.3 France Automotive Biofuels Market, By Vehicle Type |

6.3.1 Overview and Analysis |

6.3.2 France Automotive Biofuels Market Revenues & Volume, By Passenger Cars, 2022 - 2031F |

6.3.3 France Automotive Biofuels Market Revenues & Volume, By Commercial Vehicles, 2022 - 2031F |

6.3.4 France Automotive Biofuels Market Revenues & Volume, By Electric Vehicles, 2022 - 2031F |

6.3.5 France Automotive Biofuels Market Revenues & Volume, By Heavy-Duty Trucks, 2022 - 2031F |

7 France Automotive Biofuels Market Import-Export Trade Statistics |

7.1 France Automotive Biofuels Market Export to Major Countries |

7.2 France Automotive Biofuels Market Imports from Major Countries |

8 France Automotive Biofuels Market Key Performance Indicators |

9 France Automotive Biofuels Market - Opportunity Assessment |

9.1 France Automotive Biofuels Market Opportunity Assessment, By Type, 2024 & 2031F |

9.2 France Automotive Biofuels Market Opportunity Assessment, By Feedstock, 2024 & 2031F |

9.3 France Automotive Biofuels Market Opportunity Assessment, By Vehicle Type, 2024 & 2031F |

10 France Automotive Biofuels Market - Competitive Landscape |

10.1 France Automotive Biofuels Market Revenue Share, By Companies, 2024 |

10.2 France Automotive Biofuels Market Competitive Benchmarking, By Operating and Technical Parameters |

11 Company Profiles |

12 Recommendations |

13 Disclaimer |

Global Go To Market Strategy - 2030

Export potential enables firms to identify high-growth global markets with greater confidence by combining advanced trade intelligence with a structured quantitative methodology. The framework analyzes emerging demand trends and country-level import patterns while integrating macroeconomic and trade datasets such as GDP and population forecasts, bilateral import–export flows, tariff structures, elasticity differentials between developed and developing economies, geographic distance, and import demand projections. Using weighted trade values from 2020–2024 as the base period to project country-to-country export potential for 2030, these inputs are operationalized through calculated drivers such as gravity model parameters, tariff impact factors, and projected GDP per-capita growth. Through an analysis of hidden potentials, demand hotspots, and market conditions that are most favorable to success, this method enables firms to focus on target countries, maximize returns, and global expansion with data, backed by accuracy.

By factoring in the projected importer demand gap that is currently unmet and could be potential opportunity, it identifies the potential for the Exporter (Country) among 190 countries, against the general trade analysis, which identifies the biggest importer or exporter.

To discover high-growth global markets and optimize your business strategy:

Click Here

Pricing

- Single User License$ 1,995

- Department License$ 2,400

- Site License$ 3,120

- Global License$ 3,795

Leadership Perspectives from Industry Events

Search

Thought Leadership and Analyst Meet

Our Clients

6WResearch In News

- India Export Attractiveness Tracker 2026

- India Air Conditioner Market Set for Strong Rebound in 2026 After Weather-Led Correction and GST-Driven Recovery: 6Wresearch

- ADAS in India: How Automatic Emergency Braking, Blind Spot Detection & Driver Monitoring are Transforming Road Safety

- Doha a strategic location for EV manufacturing hub: IPA Qatar

- Demand for luxury TVs surging in the GCC, says Samsung

- Empowering Growth: The Thriving Journey of Bangladesh’s Cable Industry

Latest Reports

- Qatar Access and Home Network Market (2026-2032)

- Nicaragua RPG Gaming Market (2026-2032)

- New Zealand RPG Gaming Market (2026-2032)

- Netherlands RPG Gaming Market (2026-2032)

- Nauru RPG Gaming Market (2026-2032)

- Namibia RPG Gaming Market (2026-2032)

- Mozambique RPG Gaming Market (2026-2032)

- Montenegro RPG Gaming Market (2026-2032)

- Mongolia RPG Gaming Market (2026-2032)

- Monaco RPG Gaming Market (2026-2032)

Industry Events and Analyst Meet

EV India Expo 2026

HIMTEX 2026

India Refining Summit 2026

India EV Show 2026

EV tech India Expo 2026

Whitepaper

- Middle East & Africa Commercial Security Market Click here to view more.

- Middle East & Africa Fire Safety Systems & Equipment Market Click here to view more.

- GCC Drone Market Click here to view more.

- Middle East Lighting Fixture Market Click here to view more.

- GCC Physical & Perimeter Security Market Click here to view more.