India Aggregates Market (2026-2032) | Strategic Insights, Drivers, Revenue, Analysis, Companies, Consumer Insights, Forecast, Competitive, Opportunities, Strategy, Restraints, Value, Outlook, Segmentation, Investment Trends, Trends, Demand, Share, Supply, Segments, Challenges, Pricing Analysis, Industry, Competition, Growth, Size

Market Forecast By Product Type (Crushed Stone, Sand, Gravel, Recycled Aggregates), By Application (Construction Materials, Road Construction, Concrete Production, Landscaping), By End User (Construction Industry, Residential, Commercial) And Competitive Landscape

| Product Code: ETC12712206 | Publication Date: Apr 2025 | Updated Date: Feb 2026 | Product Type: Market Research Report | |

| Publisher: 6Wresearch | Author: Vasudha | No. of Pages: 65 | No. of Figures: 34 | No. of Tables: 19 |

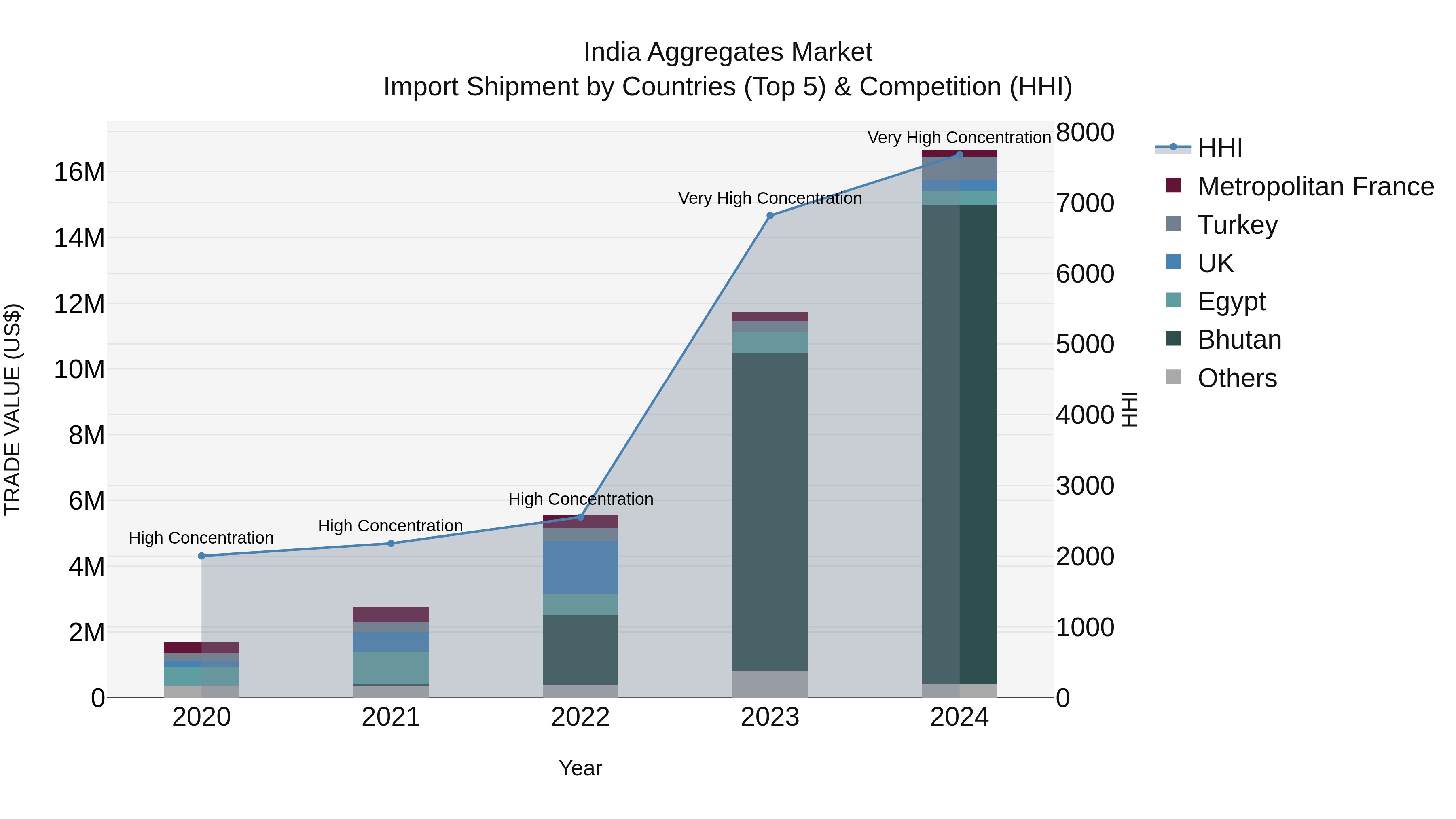

India Aggregates Market Top 5 Importing Countries and Market Competition (HHI) Analysis

India`s aggregates import market in 2024 saw significant contributions from top exporting countries such as Bhutan, Turkey, Egypt, UK, and Bangladesh. The high Herfindahl-Hirschman Index (HHI) indicates a concentrated market, reflecting the dominance of key players. The impressive compound annual growth rate (CAGR) of 77.19% from 2020 to 2024 highlights the robust demand for aggregates in India. Moreover, the growth rate of 42.02% from 2023 to 2024 underscores the accelerating pace of expansion in the sector, signaling promising opportunities for both domestic and international suppliers.

India Aggregates Market Growth Rate

According to 6Wresearch internal database and industry insights, the India Aggregates Market is projected to grow at a compound annual growth rate (CAGR) of 8.9% during the forecast period (2026-2032).

Topics Covered in the India Aggregates Market Report

The India Aggregates Market report thoroughly covers the market by product type, applications, and end users. The market report provides an unbiased and detailed analysis of ongoing market trends, opportunities/high growth areas, and market drivers, which help stakeholders devise and align their market strategies according to the current and future market dynamics.

India Aggregates Market Highlights

| Report Name | India Aggregates Market |

| Forecast Period | 2026–2032 |

| CAGR | 8.9% |

| Growing Sector | Infrastructure & Road Construction |

India Aggregates Market Synopsis

India Aggregates Market is expected to witness steady growth due to rapid urbanization, expanding infrastructure initiatives, and increasing investments in residential and commercial construction. The consumption of crushed stone, sand, and gravel is being substantially influenced by the increasing demand for roads, highways, metro systems, and industrial corridors. Furthermore, the demand for materials is being exacerbated by government initiatives, including infrastructure development plans and affordable housing programs. The long-term growth of the market is further supported by the expansion of private real estate developments in tier-II and tier-III cities and the increasing adoption of ready-mix concrete.

Evaluation of Growth Drivers in the India Aggregates Market

Below mentioned are some prominent drivers and their influence on the market dynamics:

| Drivers | Primary Segments Affected | Why it Matters (Evidence) |

| Government Infrastructure Investments | Crushed Stone; Construction & Roads | Large highway, railway, metro, and public infrastructure projects significantly increase bulk aggregate demand. |

| Growth in Urban Housing Projects | Sand & Gravel; Residential | Affordable housing schemes and urban residential development drive higher consumption of construction materials. |

| Expansion of Ready-Mix Concrete Industry | Crushed Stone & Sand; Concrete Production | Increased use of ready-mix concrete improves construction efficiency, quality consistency, and project timelines. |

| Industrial and Commercial Development | All Types; Commercial Construction | Construction of warehouses, factories, and office spaces requires large volumes of aggregates. |

| Smart Cities and Urban Development Programs | Recycled & Natural Aggregates; Construction | Urban redevelopment and smart city initiatives are increasing demand for sustainable and environmentally friendly materials. |

India Aggregates Market is expected to record a CAGR of 8. 9% between 2026 - 2032. The market's major growth driver is massive infrastructure development, alongside increasing investments in highways, railways, airports as well as urban development projects. The government is implementing large, scale programs such as Bharatmala, Smart Cities Mission, and PM Awas Yojana, which are strongly driving construction activities throughout the country. Besides that, the increased use of ready, mix concrete, fast industrialization, and aggressive private real estate investments are propelling the requirement for top, quality aggregates.

Evaluation of Restraints in the India Aggregates Market

Below mentioned are some major restraints and their influence on the market dynamics:

| Restraints | Primary Segments Affected | What This Means (Evidence) |

| Environmental Regulations on Mining | Crushed Stone & Sand; Construction | Restrictions on quarrying limit raw material availability. |

| Illegal Sand Mining Issues | Sand; Construction Materials | Supply disruptions create price volatility and project delays. |

| High Transportation Costs | All Types; End Users | Aggregates are bulky, increasing logistics expenses over long distances. |

| Land Acquisition Challenges | Crushed Stone; Mining Operations | Delays in approvals affect production capacity expansion. |

| Seasonal Construction Slowdowns | All Types; Construction Industry | Monsoon periods reduce demand and disrupt supply chains. |

India Aggregates Industry Challenges

Despite strong growth prospects, the India Aggregates Industry faces several operational challenges that affect consistent supply and pricing. Environmental regulations have become very strict and there are limited permissions for quarrying activities, which has resulted in shortage of natural resources and supply problems in some regions. Besides that, illegal sand mining, as well as irregularities in the local regulatory enforcement, are causing instability in prices and delays in projects. The transportation of aggregates invariably costs a lot as they are heavy and it is necessary to be near the construction site. Apart from the impact of monsoons, which cause production slowdowns, delays in land acquisition or environmental clearances also contribute to the disruption of production and, in general, the operational efficiency of the industry.

India Aggregates Market Trends

Some of the emerging trends that are shaping the India Aggregates Market Growth are:

- Increasing Use of Recycled Aggregates: Construction companies are slowly shifting to the use of recycled materials in order to help reduce their impact on the environment. This trend is getting a lot of traction especially since sustainability and environmentally friendly buildings are becoming key factors in decisions.

- Regional Supply Chain Optimization: Enterprises have been setting up isolated manufacturing units close to their target markets. This decreases the cost of transportation and it helps in getting timely supply of materials.

- Adoption of Advanced Crushing and Screening Technologies: Aggregate producers are increasingly investing in modern crushing, washing, and screening equipment to improve product quality and operational efficiency.

Investment Opportunities in the India Aggregates Market

Some of the key investment areas ahead that are providing strong opportunities are:

- New Quarry Sites Development: Unlocking major infrastructure projects is what investors may consider by looking at areas that are still virgin for development. Developers can secure supply contracts for many years by strategically locating quarries next to the urban growth corridors.

- Recycled Aggregate Plants: There is an increasing need for the recycling of construction and demolition waste, which calls for more such recycling facilities.

- Integrated Facilities for Ready, Mix and Aggregate: The blending of the aggregate production unit and ready, mix concrete plant is one of the ways of elevating the level of operation efficiency.

- Logistics and Materials Handling: Investments in bulk transportation, rail connectivity and the possession of advanced handling systems can result in reduced delivery costs.

Top 5 Leading Players in the India Aggregates Market

Some leading players operating in the India Aggregates Market include:

1. UltraTech Cement Ltd.

| Company Name | UltraTech Cement Ltd. |

|---|---|

| Established Year | 1983 |

| Headquarters | Mumbai, India |

| Official Website | Click Here |

UltraTech operates multiple aggregate and ready-mix concrete facilities across India. The company supports large infrastructure and real estate projects by providing high-quality construction materials and integrated supply solutions.

2. Larsen & Toubro Limited

| Company Name | Larsen & Toubro Limited |

|---|---|

| Established Year | 1938 |

| Headquarters | Mumbai, India |

| Official Website | Click Here |

Larsen & Toubro produces aggregates for its extensive infrastructure and construction projects. Its integrated operations ensure reliable material supply for highways, metro systems, and large industrial developments.

3. Adani Group

| Company Name | Adani Group |

|---|---|

| Established Year | 1988 |

| Headquarters | Ahmedabad, India |

| Official Website | Click Here |

Adani Group is expanding its presence in construction materials through integrated infrastructure and logistics capabilities. The company focuses on supporting large-scale infrastructure and urban development projects.

4. CRH Plc

| Company Name | CRH Plc |

|---|---|

| Established Year | 1970 |

| Headquarters | Dublin, Ireland |

| Official Website | Click Here |

CRH supplies aggregates and construction materials through global operations and strategic partnerships. The company focuses on sustainable production practices and efficient material supply for major infrastructure developments.

5. Heidelberg Materials India Ltd.

| Company Name | Heidelberg Materials India Ltd. |

|---|---|

| Established Year | 2006 |

| Headquarters | Gurgaon, India |

| Official Website | - |

Heidelberg Materials India produces aggregates and related construction materials for infrastructure and housing projects. The company emphasizes quality production, operational efficiency, and environmentally responsible mining practices.

Government Regulations Introduced in the India Aggregates Market

The Government of India has launched multiple initiatives to both facilitate infrastructure growth and ensure sustainable resource management. These days, Bharatmala Pariyojana, Sagarmala, Smart Cities Mission, PM Awas Yojana, etc. are a few examples of programs that have considerably pushed up the demand for construction raw materials including aggregates. At the same time, to cut down illegal extraction and promote responsible quarrying, the Ministry of Environment, Forest and Climate Change has redrafted mining laws and tightened the environmentally friendly clearance process. Several state governments, too, have issued online mineral tracking systems and e, auction policies with the help of which they have increased transparency. All these activities are focused on maintaining a balance between infrastructure development, environmental protection, and efficient resource utilization.

Future Insights of the India Aggregates Market

India Aggregates Market is expected to maintain steady growth as infrastructure development remains a key priority for economic expansion. Increasing investments in transportation networks, industrial corridors, renewable energy projects, and urban housing will continue to drive material demand. The market is also likely to witness greater adoption of recycled aggregates and advanced production technologies to address environmental concerns and resource constraints. As construction activities expand into emerging cities and industrial regions, localized production and efficient logistics will become increasingly important. Strong government spending, private sector participation, and sustainable construction practices will collectively support long-term market growth.

Market Segmentation Analysis

The report offers a comprehensive study of the subsequent market segments and their leading categories.

Crushed Stone to Dominate the Market – By Product Type

According to Mohit, Senior Research Analyst, 6Wresearch, the Crushed Stone holds the largest segment in the India Aggregates Market Share due to its extensive use in concrete production, road construction, and large infrastructure projects. Its better strength, lasting power, and constant availability are some of the reasons it is the most widely used material for highways, railways, bridges, and commercial construction. The increasing need for ready, mix concrete and asphalt mixtures also makes crushed stone consumption more robust. As government expenditures in transportation and urban infrastructure continue, this segment being the biggest one will drive the general market growth.

Road Construction to Dominate the Market - By Application

The road segment represents the primary application segment as India increases its highway and rural road networks. Large, scale projects under Bharatmala and state, level infrastructure programs require great quantities of aggregates for base layers, asphalt mixes, and pavement constructions. The strength of the government in improving the connectivity of cities, industrial zones, and rural areas is one of the reasons why the demand is rising. Moreover, the construction of expressways, economic corridors, and logistics parks is putting a premium on high, quality aggregates, hence, road construction is a big contributor to the total market consumption.

Key Attractiveness of the Report

- 10 Years of Market Numbers.

- Historical Data Starting from 2022 to 2025.

- Base Year: 2025.

- Forecast Data until 2032.

- Key Performance Indicators Impacting the Market.

- Major Upcoming Developments and Projects.

Key Highlights of the Report:

- India Aggregates Market Outlook

- Market Size of India Aggregates Market, 2025

- Forecast of India Aggregates Market, 2032

- Historical Data and Forecast of India Aggregates Revenues & Volume for the Period 2022-2032

- India Aggregates Market Trend Evolution

- India Aggregates Market Drivers and Challenges

- India Aggregates Price Trends

- India Aggregates Porter's Five Forces

- India Aggregates Industry Life Cycle

- Historical Data and Forecast of India Aggregates Market Revenues & Volume By Product Type for the Period 2022-2032

- Historical Data and Forecast of India Aggregates Market Revenues & Volume By Crushed Stone for the Period 2022-2032

- Historical Data and Forecast of India Aggregates Market Revenues & Volume By Sand for the Period 2022-2032

- Historical Data and Forecast of India Aggregates Market Revenues & Volume By Gravel for the Period 2022-2032

- Historical Data and Forecast of India Aggregates Market Revenues & Volume By Recycled Aggregates for the Period 2022-2032

- Historical Data and Forecast of India Aggregates Market Revenues & Volume By Application for the Period 2022-2032

- Historical Data and Forecast of India Aggregates Market Revenues & Volume By Construction Materials for the Period 2022-2032

- Historical Data and Forecast of India Aggregates Market Revenues & Volume By Road Construction for the Period 2022-2032

- Historical Data and Forecast of India Aggregates Market Revenues & Volume By Concrete Production for the Period 2022-2032

- Historical Data and Forecast of India Aggregates Market Revenues & Volume By Landscaping for the Period 2022-2032

- Historical Data and Forecast of India Aggregates Market Revenues & Volume By End User for the Period 2022-2032

- Historical Data and Forecast of India Aggregates Market Revenues & Volume By Construction Industry for the Period 2022-2032

- Historical Data and Forecast of India Aggregates Market Revenues & Volume By Residential for the Period 2022-2032

- Historical Data and Forecast of India Aggregates Market Revenues & Volume By Commercial for the Period 2022-2032

- India Aggregates Import Export Trade Statistics

- Market Opportunity Assessment By Product Type

- Market Opportunity Assessment By Application

- Market Opportunity Assessment By End User

- India Aggregates Top Companies Market Share

- India Aggregates Competitive Benchmarking By Technical and Operational Parameters

- India Aggregates Company Profiles

- India Aggregates Key Strategic Recommendations

Market Covered

The report offers a comprehensive study of the subsequent market segments:

By Product Type

- Crushed Stone

- Sand

- Gravel

- Recycled Aggregates

By Application

- Construction Materials

- Road Construction

- Concrete Production

- Landscaping

By End User

- Construction Industry

- Residential

- Commercial

India Aggregates Market (2026-2032): FAQs

The India Aggregates Market is projected to grow at a CAGR of 8.9% during the forecast period 2026-2032.

Growth is driven by large infrastructure investments, urban housing demand, expansion of road networks, and increasing use of ready-mix concrete.

Programs such as Bharatmala, Smart Cities Mission, PM Awas Yojana, and stricter mining transparency systems are supporting market growth.

Road construction and concrete production dominate due to large-scale highway expansion and infrastructure development projects.

6Wresearch actively monitors the India Aggregates Market and publishes its comprehensive annual report, highlighting emerging trends, growth drivers, revenue analysis, and forecast outlook. Our insights help businesses to make data-backed strategic decisions with ongoing market dynamics. Our analysts track relevent industries related to the India Aggregates Market, allowing our clients with actionable intelligence and reliable forecasts tailored to emerging regional needs.

Yes, we provide customisation as per your requirements. To learn more, feel free to contact us on sales@6wresearch.com

| 1 Executive Summary |

| 2 Introduction |

| 2.1 Key Highlights of the Report |

| 2.2 Report Description |

| 2.3 Market Scope & Segmentation |

| 2.4 Research Methodology |

| 2.5 Assumptions |

| 3 India Aggregates Market Overview |

| 3.1 India Country Macro Economic Indicators |

| 3.2 India Aggregates Market Revenues & Volume, 2022 & 2032F |

| 3.3 India Aggregates Market - Industry Life Cycle |

| 3.4 India Aggregates Market - Porter's Five Forces |

| 3.5 India Aggregates Market Revenues & Volume Share, By Product Type, 2022 & 2032F |

| 3.6 India Aggregates Market Revenues & Volume Share, By Application, 2022 & 2032F |

| 3.7 India Aggregates Market Revenues & Volume Share, By End User, 2022 & 2032F |

| 4 India Aggregates Market Dynamics |

| 4.1 Impact Analysis |

| 4.2 Market Drivers |

| 4.2.1 Rapid urbanization and infrastructure development in India |

| 4.2.2 Government initiatives to boost the construction sector |

| 4.2.3 Growing demand for residential and commercial real estate projects |

| 4.2.4 Increase in road construction projects |

| 4.2.5 Expansion of the mining industry in India |

| 4.3 Market Restraints |

| 4.3.1 Environmental regulations and concerns related to quarrying and mining activities |

| 4.3.2 Fluctuating prices of raw materials like sand and gravel |

| 4.3.3 Lack of standardized quality control measures in the aggregates industry |

| 4.3.4 Infrastructure bottlenecks leading to delays in project execution |

| 4.3.5 Competition from alternative materials like recycled aggregates |

| 5 India Aggregates Market Trends |

| 6 India Aggregates Market, By Types |

| 6.1 India Aggregates Market, By Product Type |

| 6.1.1 Overview and Analysis |

| 6.1.2 India Aggregates Market Revenues & Volume, By Product Type, 2022 - 2032F |

| 6.1.3 India Aggregates Market Revenues & Volume, By Crushed Stone, 2022 - 2032F |

| 6.1.4 India Aggregates Market Revenues & Volume, By Sand, 2022 - 2032F |

| 6.1.5 India Aggregates Market Revenues & Volume, By Gravel, 2022 - 2032F |

| 6.1.6 India Aggregates Market Revenues & Volume, By Recycled Aggregates, 2022 - 2032F |

| 6.2 India Aggregates Market, By Application |

| 6.2.1 Overview and Analysis |

| 6.2.2 India Aggregates Market Revenues & Volume, By Construction Materials, 2022 - 2032F |

| 6.2.3 India Aggregates Market Revenues & Volume, By Road Construction, 2022 - 2032F |

| 6.2.4 India Aggregates Market Revenues & Volume, By Concrete Production, 2022 - 2032F |

| 6.2.5 India Aggregates Market Revenues & Volume, By Landscaping, 2022 - 2032F |

| 6.3 India Aggregates Market, By End User |

| 6.3.1 Overview and Analysis |

| 6.3.2 India Aggregates Market Revenues & Volume, By Construction Industry, 2022 - 2032F |

| 6.3.3 India Aggregates Market Revenues & Volume, By Residential, 2022 - 2032F |

| 6.3.4 India Aggregates Market Revenues & Volume, By Commercial, 2022 - 2032F |

| 7 India Aggregates Market Import-Export Trade Statistics |

| 7.1 India Aggregates Market Export to Major Countries |

| 7.2 India Aggregates Market Imports from Major Countries |

| 8 India Aggregates Market Key Performance Indicators |

| 8.1 Average selling price of aggregates |

| 8.2 Utilization rate of aggregate production facilities |

| 8.3 Percentage of infrastructure projects using aggregates |

| 8.4 Adoption rate of sustainable practices in aggregate production |

| 8.5 Customer satisfaction index for aggregate suppliers |

| 9 India Aggregates Market - Opportunity Assessment |

| 9.1 India Aggregates Market Opportunity Assessment, By Product Type, 2022 & 2032F |

| 9.2 India Aggregates Market Opportunity Assessment, By Application, 2022 & 2032F |

| 9.3 India Aggregates Market Opportunity Assessment, By End User, 2022 & 2032F |

| 10 India Aggregates Market - Competitive Landscape |

| 10.1 India Aggregates Market Revenue Share, By Companies, 2025 |

| 10.2 India Aggregates Market Competitive Benchmarking, By Operating and Technical Parameters |

| 11 Company Profiles |

| 12 Recommendations |

| 13 Disclaimer |

Export potential assessment - trade Analytics for 2030

Export potential enables firms to identify high-growth global markets with greater confidence by combining advanced trade intelligence with a structured quantitative methodology. The framework analyzes emerging demand trends and country-level import patterns while integrating macroeconomic and trade datasets such as GDP and population forecasts, bilateral import–export flows, tariff structures, elasticity differentials between developed and developing economies, geographic distance, and import demand projections. Using weighted trade values from 2020–2024 as the base period to project country-to-country export potential for 2030, these inputs are operationalized through calculated drivers such as gravity model parameters, tariff impact factors, and projected GDP per-capita growth. Through an analysis of hidden potentials, demand hotspots, and market conditions that are most favorable to success, this method enables firms to focus on target countries, maximize returns, and global expansion with data, backed by accuracy.

By factoring in the projected importer demand gap that is currently unmet and could be potential opportunity, it identifies the potential for the Exporter (Country) among 190 countries, against the general trade analysis, which identifies the biggest importer or exporter.

To discover high-growth global markets and optimize your business strategy:

Click Here

Pricing

- Single User License$ 1,995

- Department License$ 2,400

- Site License$ 3,120

- Global License$ 3,795

Search

Thought Leadership and Analyst Meet

Our Clients

Latest Reports

- United Kingdom (UK) Long-term Care Insurance Market (2026-2032) | Growth, Share, Consumer Insights, Drivers, Opportunities, Competition, Pricing Analysis, Segments, Restraints, Companies, Competitive, Value, Outlook, Size, Demand, Analysis, Challenges, Strategic Insights, Investment Trends, Revenue, Trends, Supply, Forecast

- United Kingdom (UK) Long Term Care Market (2026-2032) | Companies, Outlook, Analysis, Trends, Value, Revenue, Segmentation, Share, Forecast, Competitive Landscape, Growth, Size & Forecast

- Iraq Insulation and Waterproofing Market (2026-2032) | Outlook, Drivers, Growth, Size, Share, Industry, Revenue, Trends, Demand, Competitive, Strategic Insights, Opportunities, Segments, Companies, Challenges, Strategy, Consumer Insights, Analysis, Investment Trends, Value, Segmentation, Forecast, Restraints

- India Switchgear Market Outlook (2026 - 2032) | Size, Share, Trends, Growth, Revenue, Forecast, Analysis, Value, Outlook

- Pakistan Contraceptive Implants Market (2025-2031) | Demand, Growth, Size, Share, Industry, Pricing Analysis, Competitive, Strategic Insights, Strategy, Consumer Insights, Analysis, Investment Trends, Opportunities, Revenue, Segments, Value, Segmentation, Supply, Forecast, Restraints, Outlook, Competition, Drivers, Trends, Companies, Challenges

- Sri Lanka Packaging Market (2026-2032) | Outlook, Competition, Drivers, Trends, Demand, Pricing Analysis, Competitive, Strategic Insights, Companies, Challenges, Strategy, Consumer Insights, Analysis, Investment Trends, Opportunities, Growth, Size, Share, Industry, Revenue, Segments, Value, Segmentation, Supply, Forecast, Restraints

- India Kids Watches Market (2026-2032) | Strategy, Consumer Insights, Analysis, Investment Trends, Opportunities, Growth, Size, Share, Industry, Revenue, Segments, Value, Segmentation, Supply, Forecast, Restraints, Outlook, Competition, Drivers, Trends, Demand, Pricing Analysis, Competitive, Strategic Insights, Companies, Challenges

- Saudi Arabia Core Assurance Service Market (2025-2031) | Strategy, Consumer Insights, Analysis, Investment Trends, Opportunities, Growth, Size, Share, Industry, Revenue, Segments, Value, Segmentation, Supply, Forecast, Restraints, Outlook, Competition, Drivers, Trends, Demand, Pricing Analysis, Competitive, Strategic Insights, Companies, Challenges

- Romania Uninterruptible Power Supply (UPS) Market (2026-2032) | Industry, Analysis, Revenue, Size, Forecast, Outlook, Value, Trends, Share, Growth & Companies

- Saudi Arabia Car Window Tinting Film, Paint Protection Film (PPF), and Ceramic Coating Market (2025-2031) | Strategy, Consumer Insights, Analysis, Investment Trends, Opportunities, Growth, Size, Share, Industry, Revenue, Segments, Value, Segmentation, Supply, Forecast, Restraints, Outlook, Competition, Drivers, Trends, Demand, Pricing Analysis, Competitive, Strategic Insights, Companies, Challenges

Industry Events and Analyst Meet

India EV Show 2026

EV tech India Expo 2026

Auto Tech Asia 2026

Battery Tech India 2026

Smart Production Solutions Guangzhou 2026

Whitepaper

- Middle East & Africa Commercial Security Market Click here to view more.

- Middle East & Africa Fire Safety Systems & Equipment Market Click here to view more.

- GCC Drone Market Click here to view more.

- Middle East Lighting Fixture Market Click here to view more.

- GCC Physical & Perimeter Security Market Click here to view more.

6WResearch In News

- Doha a strategic location for EV manufacturing hub: IPA Qatar

- Demand for luxury TVs surging in the GCC, says Samsung

- Empowering Growth: The Thriving Journey of Bangladesh’s Cable Industry

- Demand for luxury TVs surging in the GCC, says Samsung

- Video call with a traditional healer? Once unthinkable, it’s now common in South Africa

- Intelligent Buildings To Smooth GCC’s Path To Net Zero