India Jewellery Market (2025-2031) | Industry, Trends, Companies, Analysis, Size, Value, Outlook, Revenue, Share, Forecast & Growth

Market Forecast By Product (Necklace, Ring, Earrings, Bracelet, Others), By Material (Gold, Platinum, Diamond, Others) And Competitive Landscape

| Product Code: ETC021644 | Publication Date: Aug 2023 | Updated Date: Nov 2025 | Product Type: Report | |

| Publisher: 6Wresearch | Author: Ravi Bhandari | No. of Pages: 70 | No. of Figures: 35 | No. of Tables: 5 |

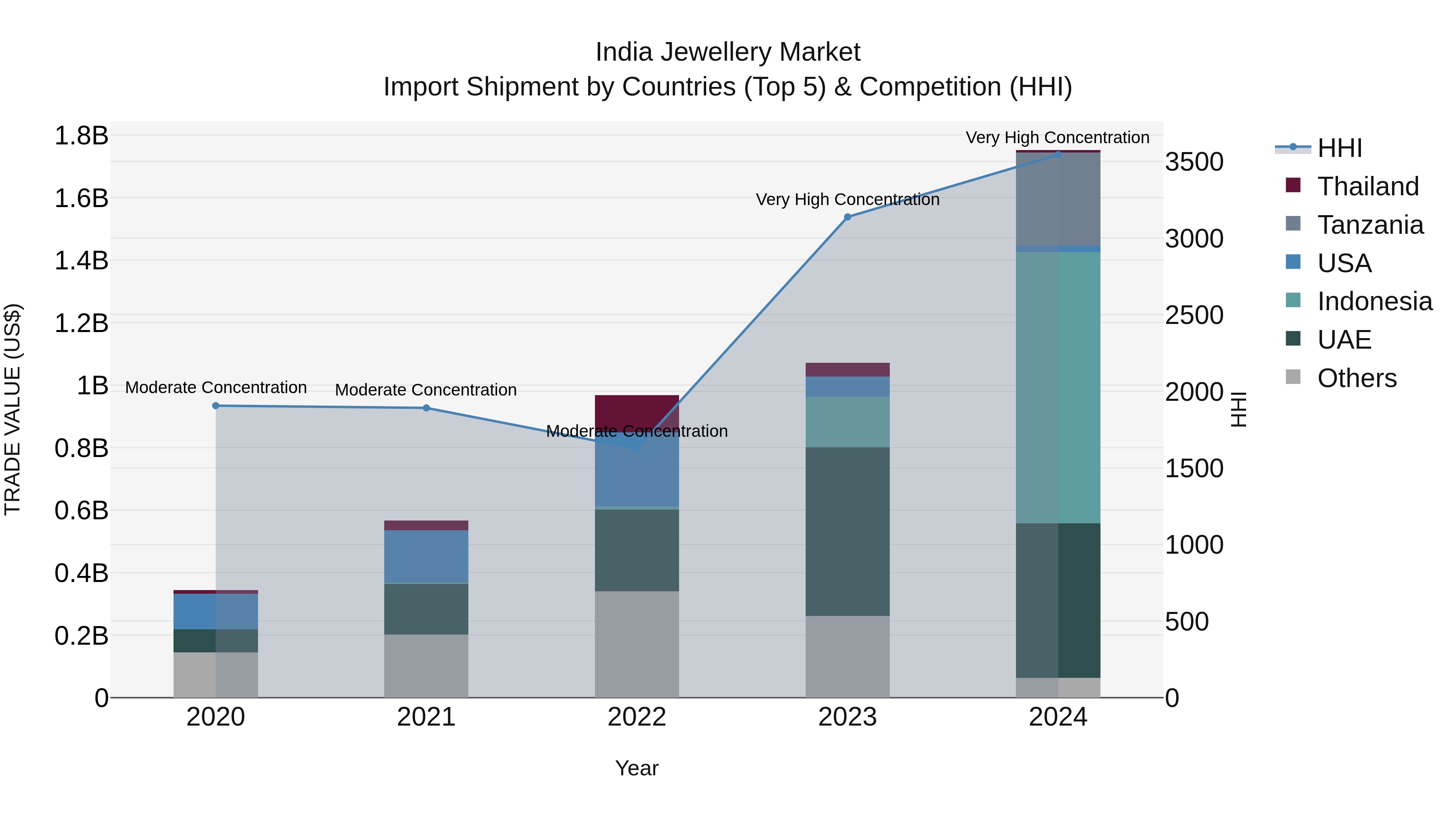

India Jewellery Market Top 5 Importing Countries and Market Competition (HHI) Analysis

India`s jewellery import shipments in 2024 saw a significant influx from top exporting countries including Indonesia, UAE, Tanzania, Italy, and the USA. The high Herfindahl-Hirschman Index (HHI) indicates a concentrated market, with a remarkable Compound Annual Growth Rate (CAGR) of 50.16% from 2020 to 2024. The impressive growth rate of 63.42% from 2023 to 2024 reflects a thriving demand for jewellery imports in India, presenting lucrative opportunities for market players and indicating strong consumer interest in international jewellery offerings.

India Jewellery Market Growth Rate

According to 6Wresearch internal database and industry insights, the India Jewellery Market is projected to grow at a compound annual growth rate (CAGR) of 7.3% during the forecast period (2025-2031).

India Jewellery Market Highlights

| Report Name | India Jewellery Market |

| Forecast period | 2025-2031 |

| CAGR | 7.3% |

| Growing Sector | Luxury Goods and Lifestyle |

Topics Covered in the India Jewellery Market Report

The India Jewellery Market report thoroughly covers the market by product and material. The market report provides an unbiased and detailed analysis of ongoing market trends, opportunities/high growth areas, and market drivers, which would help stakeholders to devise and align their market strategies according to the current and future market dynamics.

India Jewellery Market Synopsis

The India Jewellery Industry has experienced substantial growth over the past few years owing to rising disposable incomes in urban and Tier-II/III cities, strong cultural affinity toward gold and bridal purchases, and rapid formalization of retail through national chains and hallmarking compliance. Further, e-commerce discovery, omni-channel models, and design innovation in lightweight daily-wear and studded jewellery are expanding addressable demand among younger consumers.

Evaluation of Growth Drivers in the India Jewellery Market

Below mentioned are some prominent drivers and their influence to the market dynamics:

| Drivers | Primary Segments Affected | Why it Matters |

| Hallmarking & Quality Compliance (HUID) | Gold; Diamond; Organized Retail | Mandatory hallmarking increases trust and boosts organized jewellery sales. |

| Rising Bridal & Festive Expenditure | Necklace; Earrings; Rings | Weddings and festivals drive big-ticket purchases and higher sales volumes. |

| Shift to Organized & Omni-Channel Retail | All products; Gold & Diamond | Organized and digital retailers enhance transparency and purchasing facility. |

| Design Innovation & Lightweight Trend | Rings; Earrings; Bracelets | Advance lightweight designs attract young buyers and encourage frequent purchases. |

| Export Competitiveness & SEZ Ecosystem | Diamond; Platinum; Studded | Jewellery hubs like Mumbai and Surat help exports and large-scale manufacture. |

India Jewellery Market size is projected to grow at a CAGR of 7.3% during the forecast period of 2025-2031.This upward trajectory is underpinned by hallmarking-led formalization, sustained wedding demand, and premiumization in studded jewellery. On the other hand, market size and revenue are further supported by omni-channel expansion, buyback/upgrade programs, and product innovation in lightweight daily wear that unlocks repeat purchases. Upcoming retailers are accelerating investments in store networks, karigar (artisan) ecosystems, and technology for sourcing, design, and inventory turn—critical for profitability in both metros and high-potential Tier-II/III catchments. Additionally, rising export opportunities and increasing consumer preference for certified, traceable jewellery are further strengthening the India Jewellery Market Growth.

Evaluation of Restraints in the India Jewellery Market

Below mentioned are some major restraints and their influence on market dynamics:

| Restraints | Primary Segments Affected | What this Means |

| Gold Price Volatility | Gold-dominant products | Frequent gold price changes delay buying decisions and reduce profit margins. |

| Working Capital Intensity | Gold; Diamond; Multi-category chains | High inventory and financing needs limit retailers’ expansion plans. |

| Informal Competition in Select Pockets | Unorganized local retailers | Local unorganized jewellers increase price competition in the market. |

| Import Duties & Policy Changes | Diamond & Platinum; Studded | Fluctuating import duties surge costs and impact the pricing and exports. |

| Skilled Artisan Supply Gaps | High-craft segments (Kundan/Polki) | Shortage of skilled artisans raises production time and costs. |

India Jewellery Market Challenges

There are numerous challenges hampering the India jewellery market growth. In general, volatility in bullion prices can elongate decision cycles and push consumers toward lighter grammage. Along with that, working capital intensity and compliance investments puts pressure on small-scale players transforming them into organized structures. Furthermore, import duties and policy tweaks on bullion and diamonds can impact pricing, while capacity restraints in skilled craftsmanship cause supply bottlenecks for high-value traditional sectors.

India Jewellery Market Trends

Some emerging trends shaping the market landscape are:

- Omni-Channel & Phygital Selling: Retailers integrate online discovery, virtual try-ons, appointment-led consultations, and in-store fulfillment to improve conversion and basket size.

- Lightweight & Everyday Collections: Gold and diamond lines less than ten grams of gold and diamonds are targetting younger buyers to encourage them to buy again, leading in higher turns and margins.

- Transparent Pricing & Buyback Programs: Making charges transparency and lifetime exchange policies boost trust and retention, supporting organized market share gains.

- Designer Collaborations & Personalization: Exclusive-edition capsules, regional motifs, and made-to-order services raises differentiation and willingness to pay.

- Sustainability & Traceability: Conflict-free sourcing, recycled gold, and digital certificates (blockchain-backed) improve brand equity and export acceptance.

Investment Opportunities in the India Jewellery Industry

Some of the key investment opportunities in the India Jewellery Market are:

- Store Network Expansion in Tier-II/III: High-ROIC formats in underpenetrated cities with focused assortments and local design palettes.

- Technology & Supply Chain Digitization: PLM/CAD for rapid design cycles, RFID-led inventory accuracy, and analytics for assortment optimization.

- Hallmarking, Certification & Traceability Solutions: Platforms for HUID integration, digital certificates, and provenance tracking for studded jewellery.

- Bridal & Premium Studded Portfolio: Higher margins in diamonds/platinum with curated bridal trousseau packages and financing/EMI tie-ups.

Top 5 Leading Companies in the India Jewellery Market

Here is a comprehensive list of key players dominating the India Jewellery Market Share:

1. Titan Company Ltd. (Tanishq)

| Company Name | Titan Company Ltd. (Tanishq) |

|---|---|

| Headquarters | Bengaluru, India |

| Established Year | 1984 |

| Official Website | Click Here |

Tanishq is the leading organized jewellery retailer in India, offering certified gold and diamond jewellery with strong hallmarking standards, design innovation, and extensive buyback/exchange programs.

2. Kalyan Jewellers India Ltd.

| Company Name | Kalyan Jewellers India Ltd. |

|---|---|

| Headquarters | Thrissur, India |

| Established Year | 1993 |

| Official Website | Click Here |

Kalyan operates a large-format network across India and the Middle East, focusing on bridal and regional collections with transparent pricing and strong brand endorsements.

3. Malabar Gold & Diamonds

| Company Name | Malabar Gold & Diamonds |

|---|---|

| Headquarters | Kozhikode, India |

| Established Year | 1993 |

| Official Website | Click Here |

Malabar offers a wide portfolio spanning gold, diamond, and platinum with global footprints, strong craftsmanship ecosystems, and customer-centric loyalty programs.

4. PC Jeweller Ltd.

| Company Name | PC Jeweller Ltd. |

|---|---|

| Headquarters | New Delhi, India |

| Established Year | 2005 |

| Official Website | Click Here |

PC Jeweller specializes in certified diamond and gold jewellery with contemporary designs, export presence, and omni-channel sales initiatives.

5. Senco Gold Ltd.

| Company Name | Senco Gold Ltd. |

|---|---|

| Headquarters | Kolkata, India |

| Established Year | 1994 |

| Official Website | Click Here |

Senco is known for craftsmanship-led collections across gold, diamond, and traditional Bengali designs, expanding through franchise and company-owned stores.

Government Regulations Introduced in the India Jewellery Market

According to Indian Government Data, it is essential for the gold to be marked with a Hallmark Unique Identification (HUID) number that is being phased across districts. It helps in strengthening purity assurance and acquiring customer trust. Duty frameworks on gold and special stones are periodically calibrated to manage trade balances, while schemes such as Gold Monetization and Sovereign Gold Bonds focus to formalize savings and reduce dependency on imported bullion. State-supported hallmarking centers, BIS authorization, and training through skill missions bolster compliance and artisan potential.

Future Insights of the India Jewellery Market

The India Jewellery Market is anticipated to undergo steady and sustained growth over the upcoming years. Premiumization through studded and designer-led collections, greater acknowledgment of lightweight daily-wear, and omni-channel convenience will continue to shape consumer choices. Along with that, hallmarking-led trust, expanding organized retail in Tier-II/III cities, and export opportunities in studded jewellery will further bolster India Jewellery Market Growth. Additionally, the rise of digital-first jewellery brands and tech-enabled personalization is forecasted to improve customer engagement and stimulate future sales.

Market Segmentation Analysis

The report offers a comprehensive study of the subsequent market segments and their leading categories.

Necklace to Dominate the Market - By Product

According to Mansi Ahuja, Senior Research Analyst at 6Wresearch, Necklace emerges as the dominating category in the India Jewellery Market Share owing to its central role in bridal trousseau and festive purchases, high average ticket size, and versatility across regional designs (temple, kundan, polki, and contemporary sets).

Gold to Dominate the Market - By Material

Gold remains the dominant material due to deep-rooted cultural significance, liquidity and exchange value, and wide availability across organized and local formats. Mandatory hallmarking with HUID strengthens purity assurance and boosts organized share.

Key Attractiveness of the Report

- 10 Years of Market Numbers

- Historical Data: Starting from 2021 to 2024

- Base Year: 2024

- Forecast Data until 2031

- Key Performance Indicators Impacting the Market

- Major Upcoming Developments and Projects

Key Highlights of the Report:

- India Jewellery Market Outlook

- Market Size of India Jewellery Market, 2024

- Forecast of India Jewellery Market, 2031

- Historical Data and Forecast of India Jewellery Revenues & Volume for the Period 2021 - 2031

- India Jewellery Market Trend Evolution

- India Jewellery Market Drivers and Challenges

- India Jewellery Price Trends

- India Jewellery Porter's Five Forces

- India Jewellery Industry Life Cycle

- Historical Data and Forecast of India Jewellery Market Revenues & Volume By Product for the Period 2021 - 2031

- Historical Data and Forecast of India Jewellery Market Revenues & Volume By Necklace for the Period 2021 - 2031

- Historical Data and Forecast of India Jewellery Market Revenues & Volume By Ring for the Period 2021 - 2031

- Historical Data and Forecast of India Jewellery Market Revenues & Volume By Earrings for the Period 2021 - 2031

- Historical Data and Forecast of India Jewellery Market Revenues & Volume By Bracelet for the Period 2021 - 2031

- Historical Data and Forecast of India Jewellery Market Revenues & Volume By Others for the Period 2021 - 2031

- Historical Data and Forecast of India Jewellery Market Revenues & Volume By Material for the Period 2021 - 2031

- Historical Data and Forecast of India Jewellery Market Revenues & Volume By Gold for the Period 2021 - 2031

- Historical Data and Forecast of India Jewellery Market Revenues & Volume By Platinum for the Period 2021 - 2031

- Historical Data and Forecast of India Jewellery Market Revenues & Volume By Diamond for the Period 2021 - 2031

- Historical Data and Forecast of India Jewellery Market Revenues & Volume By Others for the Period 2021 - 2031

- India Jewellery Import Export Trade Statistics

- Market Opportunity Assessment By Product

- Market Opportunity Assessment By Material

- India Jewellery Top Companies Market Share

- India Jewellery Competitive Benchmarking By Technical and Operational Parameters

- India Jewellery Company Profiles

- India Jewellery Key Strategic Recommendations

Markets Covered

The report provides a detailed analysis of the following market segments:

By Product

- Necklace

- Ring

- Earring

- Bracelet

- Others

By Material

- Gold

- Platinum

- Diamond

- Others

India Jewellery Market (2025-2031): FAQs

The market is expected to grow at a CAGR of 7.3% from 2025 to 2031.

Diamond-studded jewellery is likely to see faster premiumization due to design innovation, certification-led trust, and increasing adoption in bridal and occasion wear.

This upward trajectory is underpinned by hallmarking-led formalization, premiumization in studded jewellery and increasing consumer preference for certified.

Challenges include volatility in bullion prices can elongate decision cycles and push consumers toward lighter grammage.

6Wresearch actively monitors the India Jewellery Market and publishes its comprehensive annual report, highlighting emerging trends, growth drivers, revenue analysis, and forecast outlook. Our insights help businesses to make data-backed strategic decisions with ongoing market dynamics. Our analysts track relevent industries related to the India Jewellery Market, allowing our clients with actionable intelligence and reliable forecasts tailored to emerging regional needs.

Yes, we provide customisation as per your requirements. To learn more, feel free to contact us on sales@6wresearch.com

| 1 Executive Summary |

| 2 Introduction |

| 2.1 Key Highlights of the Report |

| 2.2 Report Description |

| 2.3 Market Scope & Segmentation |

| 2.4 Research Methodology |

| 2.5 Assumptions |

| 3 India Jewellery Market Overview |

| 3.1 India Country Macro Economic Indicators |

| 3.2 India Jewellery Market Revenues & Volume, 2021 & 2031F |

| 3.3 India Jewellery Market - Industry Life Cycle |

| 3.4 India Jewellery Market - Porter's Five Forces |

| 3.5 India Jewellery Market Revenues & Volume Share, By Product, 2021 & 2031F |

| 3.6 India Jewellery Market Revenues & Volume Share, By Material, 2021 & 2031F |

| 4 India Jewellery Market Dynamics |

| 4.1 Impact Analysis |

| 4.2 Market Drivers |

| 4.2.1 Increasing disposable income of the middle-class population in India |

| 4.2.2 Growing adoption of online channels for jewelry shopping |

| 4.2.3 Rising demand for customized and designer jewelry |

| 4.3 Market Restraints |

| 4.3.1 Fluctuating prices of precious metals and gemstones |

| 4.3.2 Intense competition from unorganized local jewelry makers |

| 4.3.3 Changing consumer preferences towards non-traditional jewelry |

| 5 India Jewellery Market Trends |

| 6 India Jewellery Market, By Types |

| 6.1 India Jewellery Market, By Product |

| 6.1.1 Overview and Analysis |

| 6.1.2 India Jewellery Market Revenues & Volume, By Product, 2021 - 2031F |

| 6.1.3 India Jewellery Market Revenues & Volume, By Necklace, 2021 - 2031F |

| 6.1.4 India Jewellery Market Revenues & Volume, By Ring, 2021 - 2031F |

| 6.1.5 India Jewellery Market Revenues & Volume, By Earrings, 2021 - 2031F |

| 6.1.6 India Jewellery Market Revenues & Volume, By Bracelet, 2021 - 2031F |

| 6.1.7 India Jewellery Market Revenues & Volume, By Others, 2021 - 2031F |

| 6.2 India Jewellery Market, By Material |

| 6.2.1 Overview and Analysis |

| 6.2.2 India Jewellery Market Revenues & Volume, By Gold, 2021 - 2031F |

| 6.2.3 India Jewellery Market Revenues & Volume, By Platinum, 2021 - 2031F |

| 6.2.4 India Jewellery Market Revenues & Volume, By Diamond, 2021 - 2031F |

| 6.2.5 India Jewellery Market Revenues & Volume, By Others, 2021 - 2031F |

| 7 India Jewellery Market Import-Export Trade Statistics |

| 7.1 India Jewellery Market Export to Major Countries |

| 7.2 India Jewellery Market Imports from Major Countries |

| 8 India Jewellery Market Key Performance Indicators |

| 8.1 Average order value per customer |

| 8.2 Repeat purchase rate |

| 8.3 Customer satisfaction score |

| 8.4 Percentage of revenue from new product launches |

| 8.5 Online traffic conversion rate |

| 9 India Jewellery Market - Opportunity Assessment |

| 9.1 India Jewellery Market Opportunity Assessment, By Product, 2021 & 2031F |

| 9.2 India Jewellery Market Opportunity Assessment, By Material, 2021 & 2031F |

| 10 India Jewellery Market - Competitive Landscape |

| 10.1 India Jewellery Market Revenue Share, By Companies, 2024 |

| 10.2 India Jewellery Market Competitive Benchmarking, By Operating and Technical Parameters |

| 11 Company Profiles |

| 12 Recommendations |

| 13 Disclaimer |

Global Go To Market Strategy - 2030

Export potential enables firms to identify high-growth global markets with greater confidence by combining advanced trade intelligence with a structured quantitative methodology. The framework analyzes emerging demand trends and country-level import patterns while integrating macroeconomic and trade datasets such as GDP and population forecasts, bilateral import–export flows, tariff structures, elasticity differentials between developed and developing economies, geographic distance, and import demand projections. Using weighted trade values from 2020–2024 as the base period to project country-to-country export potential for 2030, these inputs are operationalized through calculated drivers such as gravity model parameters, tariff impact factors, and projected GDP per-capita growth. Through an analysis of hidden potentials, demand hotspots, and market conditions that are most favorable to success, this method enables firms to focus on target countries, maximize returns, and global expansion with data, backed by accuracy.

By factoring in the projected importer demand gap that is currently unmet and could be potential opportunity, it identifies the potential for the Exporter (Country) among 190 countries, against the general trade analysis, which identifies the biggest importer or exporter.

To discover high-growth global markets and optimize your business strategy:

Click Here

Pricing

- Single User License$ 1,995

- Department License$ 2,400

- Site License$ 3,120

- Global License$ 3,795

Leadership Perspectives from Industry Events

Search

Thought Leadership and Analyst Meet

Our Clients

6WResearch In News

- India Air Conditioner Market Set for Strong Rebound in 2026 After Weather-Led Correction and GST-Driven Recovery: 6Wresearch

- ADAS in India: How Automatic Emergency Braking, Blind Spot Detection & Driver Monitoring are Transforming Road Safety

- Doha a strategic location for EV manufacturing hub: IPA Qatar

- Demand for luxury TVs surging in the GCC, says Samsung

- Empowering Growth: The Thriving Journey of Bangladesh’s Cable Industry

- Demand for luxury TVs surging in the GCC, says Samsung

Latest Reports

- Nicaragua RPG Gaming Market (2026-2032)

- New Zealand RPG Gaming Market (2026-2032)

- Netherlands RPG Gaming Market (2026-2032)

- Nauru RPG Gaming Market (2026-2032)

- Namibia RPG Gaming Market (2026-2032)

- Mozambique RPG Gaming Market (2026-2032)

- Montenegro RPG Gaming Market (2026-2032)

- Mongolia RPG Gaming Market (2026-2032)

- Monaco RPG Gaming Market (2026-2032)

- Micronesia RPG Gaming Market (2026-2032)

Industry Events and Analyst Meet

HIMTEX 2026

India Refining Summit 2026

India EV Show 2026

EV tech India Expo 2026

Auto Tech Asia 2026

Whitepaper

- Middle East & Africa Commercial Security Market Click here to view more.

- Middle East & Africa Fire Safety Systems & Equipment Market Click here to view more.

- GCC Drone Market Click here to view more.

- Middle East Lighting Fixture Market Click here to view more.

- GCC Physical & Perimeter Security Market Click here to view more.