Japan Automotive Bumper Market (2025-2031) | Share, Technological Advancements, Segmentation, Restraints, Market Penetration, Industry, Future Prospects, Trends, Competition, Drivers, Landscape, Opportunities, Value, Size, Outlook, Regulations, Strategy, Companies, Challenges, Innovation, Pricing Analysis, Growth, Investment Trends, Segments, Forecast, Demand, Competitive Landscape, Revenue, Analysis, Strategic Insights, Consumer Insights, Supply

Market Forecast By Material (Plastic, Fiberglass, Carbon Fiber, Aluminum), By Technology (Energy Absorbing, Smart Sensors, Lightweight Design, High Impact Strength), By Vehicle Type (Passenger Cars, Commercial Vehicles, Electric Vehicles, Luxury Vehicles) And Competitive Landscape

| Product Code: ETC10803538 | Publication Date: Apr 2025 | Updated Date: Oct 2025 | Product Type: Market Research Report | |

| Publisher: 6Wresearch | Author: Sachin Kumar Rai | No. of Pages: 65 | No. of Figures: 34 | No. of Tables: 19 |

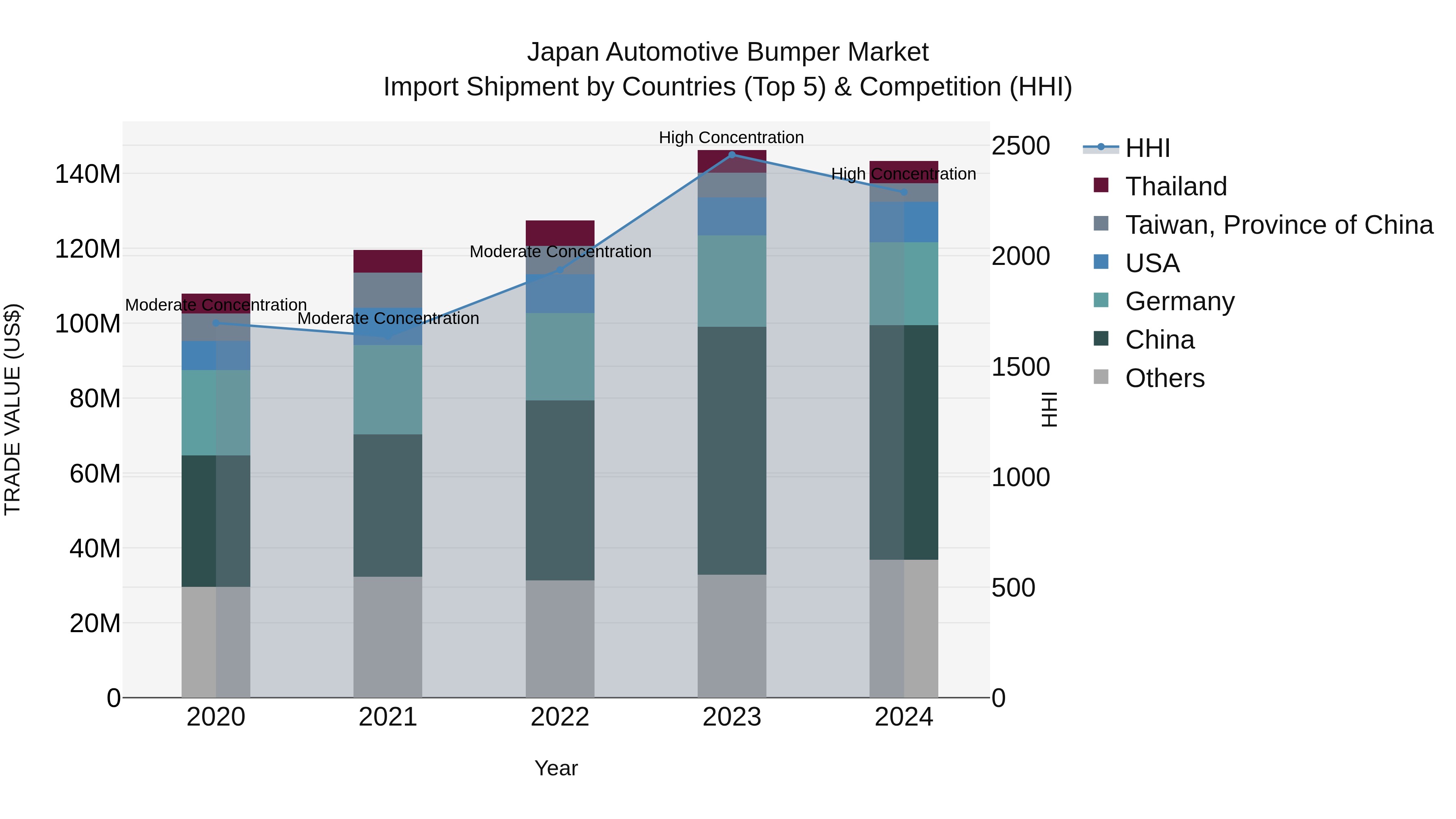

Japan Automotive Bumper Market Import Shipment by Countries (Top 5) & Competition (HHI)

Japan's automotive bumper import shipments in 2024 continued to be dominated by top exporting countries such as China, Germany, USA, Thailand, and South Korea. The market saw a high concentration with the Herfindahl-Hirschman Index (HHI) remaining elevated. Despite a slight decline in growth rate from 2023 to 2024, the compound annual growth rate (CAGR) for the period of 2020-2024 stood at a healthy 7.36%. The consistent presence of key exporting nations and the overall positive growth trend indicate a stable market for automotive bumpers in Japan.

Japan Automotive Bumper Market Overview

The Japan automotive bumper market is characterized by robust demand driven by the countryâs advanced automotive manufacturing sector and emphasis on vehicle safety and aesthetics. Major Japanese automakers, such as Toyota, Honda, and Nissan, prioritize lightweight, high-performance bumper materialsâlike thermoplastics and compositesâto enhance fuel efficiency and comply with stringent safety regulations. The market is highly competitive and innovation-driven, with key players investing in technologies such as energy-absorbing structures and pedestrian protection features. Growing electric vehicle (EV) adoption and increasing export-oriented production further stimulate bumper demand. Additionally, aftermarket replacement and repair activities contribute significantly, owing to Japanâs high vehicle ownership and aging car population. Environmental concerns and recycling mandates also shape bumper design and manufacturing, fostering the use of sustainable materials and production processes. Overall, the Japan automotive bumper market remains dynamic, supported by technological advancements, regulatory compliance, and evolving consumer preferences.

Trends of the Market

The Japan automotive bumper market is experiencing several key trends in 2024. There is a growing demand for lightweight and high-strength materials such as thermoplastic olefins and advanced composites to improve fuel efficiency and meet stringent emission regulations. Technological advancements, like the integration of sensors and cameras for advanced driver-assistance systems (ADAS), are driving the adoption of smart bumpers. Additionally, increased production of electric vehicles (EVs) is influencing bumper design and material selection, focusing on aerodynamic efficiency and safety. The market also sees a shift towards sustainability, with manufacturers adopting recycled materials and eco-friendly production processes. OEMs are partnering with local suppliers for just-in-time manufacturing, optimizing supply chains amid ongoing global disruptions. Overall, innovation, sustainability, and regulatory compliance are shaping the current landscape of Japan`s automotive bumper market.

Challenges of the Market

The Japan automotive bumper market faces several challenges, including intense competition from both domestic and international manufacturers, which puts pressure on pricing and profit margins. Increasing adoption of lightweight materials to meet stringent fuel efficiency and emission regulations demands significant R&D investments, raising production costs. Additionally, fluctuating raw material prices, particularly for plastics and composites, impact cost stability. The rapid evolution of automotive design and safety standards requires continual product innovation and adaptation, posing hurdles for smaller players. Furthermore, Japanâs declining population and stagnating vehicle sales limit market growth opportunities, while the shift towards electric vehicles (EVs) necessitates new bumper designs and integration of advanced sensors, adding complexity to manufacturing processes. Environmental regulations regarding recycling and end-of-life vehicle management also require manufacturers to develop sustainable solutions, further complicating operations in the market.

Investment Opportunities of the market

The Japan Automotive Bumper Market presents attractive investment opportunities driven by technological advancements, the shift toward lightweight and eco-friendly materials, and growing demand for electric and hybrid vehicles. Automotive manufacturers are increasingly investing in bumpers made from advanced composites and thermoplastics to meet stringent safety and fuel efficiency regulations. Additionally, the rise in vehicle customization and the premiumization trend are fueling demand for innovative bumper designs and smart bumpers with integrated sensors for advanced driver-assistance systems (ADAS). Investments in R&D, strategic partnerships with OEMs, and expansion into aftermarket services can yield strong returns. Furthermore, Japanâs robust automotive manufacturing ecosystem and export potential enhance the marketâs long-term growth prospects for investors.

Government Policy of the market

The Japanese government enforces stringent regulations impacting the automotive bumper market, primarily focusing on vehicle safety, environmental sustainability, and quality standards. The Ministry of Land, Infrastructure, Transport, and Tourism (MLIT) mandates adherence to safety standards under the Road Vehicles Act, including bumper design for pedestrian protection and crashworthiness. Environmental policies, such as the End-of-Life Vehicle (ELV) Recycling Law, require manufacturers to use recyclable materials and facilitate proper disposal of bumpers. Additionally, Japanâs support for advanced manufacturing through incentives for lightweight and energy-efficient automotive components encourages innovation in bumper materials and designs. These combined policies drive manufacturers to prioritize safety, recyclability, and technological advancement in the development and production of automotive bumpers within the Japanese market.

Future Outlook of the market

The future outlook for the Japan automotive bumper market appears moderately optimistic, driven by steady advancements in vehicle safety regulations, lightweight material innovation, and the ongoing transition toward electric and hybrid vehicles. Japanese automakers are focusing on enhancing bumper designs to meet stringent pedestrian safety standards and improve fuel efficiency through weight reduction. Growing demand for premium vehicles and the integration of smart sensors into bumpers are expected to further stimulate market growth. However, market expansion may be tempered by Japanâs declining vehicle production and an aging population, which could limit domestic demand. Nonetheless, opportunities exist in the export of advanced bumper technologies and components to other Asia-Pacific markets, supporting a stable but competitive landscape for Japanese manufacturers.

Key Highlights of the Report:

- Japan Automotive Bumper Market Outlook

- Market Size of Japan Automotive Bumper Market, 2024

- Forecast of Japan Automotive Bumper Market, 2031

- Historical Data and Forecast of Japan Automotive Bumper Revenues & Volume for the Period 2022-2031

- Japan Automotive Bumper Market Trend Evolution

- Japan Automotive Bumper Market Drivers and Challenges

- Japan Automotive Bumper Price Trends

- Japan Automotive Bumper Porter's Five Forces

- Japan Automotive Bumper Industry Life Cycle

- Historical Data and Forecast of Japan Automotive Bumper Market Revenues & Volume By Material for the Period 2022-2031

- Historical Data and Forecast of Japan Automotive Bumper Market Revenues & Volume By Plastic for the Period 2022-2031

- Historical Data and Forecast of Japan Automotive Bumper Market Revenues & Volume By Fiberglass for the Period 2022-2031

- Historical Data and Forecast of Japan Automotive Bumper Market Revenues & Volume By Carbon Fiber for the Period 2022-2031

- Historical Data and Forecast of Japan Automotive Bumper Market Revenues & Volume By Aluminum for the Period 2022-2031

- Historical Data and Forecast of Japan Automotive Bumper Market Revenues & Volume By Technology for the Period 2022-2031

- Historical Data and Forecast of Japan Automotive Bumper Market Revenues & Volume By Energy Absorbing for the Period 2022-2031

- Historical Data and Forecast of Japan Automotive Bumper Market Revenues & Volume By Smart Sensors for the Period 2022-2031

- Historical Data and Forecast of Japan Automotive Bumper Market Revenues & Volume By Lightweight Design for the Period 2022-2031

- Historical Data and Forecast of Japan Automotive Bumper Market Revenues & Volume By High Impact Strength for the Period 2022-2031

- Historical Data and Forecast of Japan Automotive Bumper Market Revenues & Volume By Vehicle Type for the Period 2022-2031

- Historical Data and Forecast of Japan Automotive Bumper Market Revenues & Volume By Passenger Cars for the Period 2022-2031

- Historical Data and Forecast of Japan Automotive Bumper Market Revenues & Volume By Commercial Vehicles for the Period 2022-2031

- Historical Data and Forecast of Japan Automotive Bumper Market Revenues & Volume By Electric Vehicles for the Period 2022-2031

- Historical Data and Forecast of Japan Automotive Bumper Market Revenues & Volume By Luxury Vehicles for the Period 2022-2031

- Japan Automotive Bumper Import Export Trade Statistics

- Market Opportunity Assessment By Material

- Market Opportunity Assessment By Technology

- Market Opportunity Assessment By Vehicle Type

- Japan Automotive Bumper Top Companies Market Share

- Japan Automotive Bumper Competitive Benchmarking By Technical and Operational Parameters

- Japan Automotive Bumper Company Profiles

- Japan Automotive Bumper Key Strategic Recommendations

Frequently Asked Questions About the Market Study (FAQs):

6Wresearch actively monitors the Japan Automotive Bumper Market and publishes its comprehensive annual report, highlighting emerging trends, growth drivers, revenue analysis, and forecast outlook. Our insights help businesses to make data-backed strategic decisions with ongoing market dynamics. Our analysts track relevent industries related to the Japan Automotive Bumper Market, allowing our clients with actionable intelligence and reliable forecasts tailored to emerging regional needs.

Yes, we provide customisation as per your requirements. To learn more, feel free to contact us on sales@6wresearch.com

1 Executive Summary |

2 Introduction |

2.1 Key Highlights of the Report |

2.2 Report Description |

2.3 Market Scope & Segmentation |

2.4 Research Methodology |

2.5 Assumptions |

3 Japan Automotive Bumper Market Overview |

3.1 Japan Country Macro Economic Indicators |

3.2 Japan Automotive Bumper Market Revenues & Volume, 2024 & 2031F |

3.3 Japan Automotive Bumper Market - Industry Life Cycle |

3.4 Japan Automotive Bumper Market - Porter's Five Forces |

3.5 Japan Automotive Bumper Market Revenues & Volume Share, By Material, 2024 & 2031F |

3.6 Japan Automotive Bumper Market Revenues & Volume Share, By Technology, 2024 & 2031F |

3.7 Japan Automotive Bumper Market Revenues & Volume Share, By Vehicle Type, 2024 & 2031F |

4 Japan Automotive Bumper Market Dynamics |

4.1 Impact Analysis |

4.2 Market Drivers |

4.3 Market Restraints |

5 Japan Automotive Bumper Market Trends |

6 Japan Automotive Bumper Market, By Types |

6.1 Japan Automotive Bumper Market, By Material |

6.1.1 Overview and Analysis |

6.1.2 Japan Automotive Bumper Market Revenues & Volume, By Material, 2022 - 2031F |

6.1.3 Japan Automotive Bumper Market Revenues & Volume, By Plastic, 2022 - 2031F |

6.1.4 Japan Automotive Bumper Market Revenues & Volume, By Fiberglass, 2022 - 2031F |

6.1.5 Japan Automotive Bumper Market Revenues & Volume, By Carbon Fiber, 2022 - 2031F |

6.1.6 Japan Automotive Bumper Market Revenues & Volume, By Aluminum, 2022 - 2031F |

6.2 Japan Automotive Bumper Market, By Technology |

6.2.1 Overview and Analysis |

6.2.2 Japan Automotive Bumper Market Revenues & Volume, By Energy Absorbing, 2022 - 2031F |

6.2.3 Japan Automotive Bumper Market Revenues & Volume, By Smart Sensors, 2022 - 2031F |

6.2.4 Japan Automotive Bumper Market Revenues & Volume, By Lightweight Design, 2022 - 2031F |

6.2.5 Japan Automotive Bumper Market Revenues & Volume, By High Impact Strength, 2022 - 2031F |

6.3 Japan Automotive Bumper Market, By Vehicle Type |

6.3.1 Overview and Analysis |

6.3.2 Japan Automotive Bumper Market Revenues & Volume, By Passenger Cars, 2022 - 2031F |

6.3.3 Japan Automotive Bumper Market Revenues & Volume, By Commercial Vehicles, 2022 - 2031F |

6.3.4 Japan Automotive Bumper Market Revenues & Volume, By Electric Vehicles, 2022 - 2031F |

6.3.5 Japan Automotive Bumper Market Revenues & Volume, By Luxury Vehicles, 2022 - 2031F |

7 Japan Automotive Bumper Market Import-Export Trade Statistics |

7.1 Japan Automotive Bumper Market Export to Major Countries |

7.2 Japan Automotive Bumper Market Imports from Major Countries |

8 Japan Automotive Bumper Market Key Performance Indicators |

9 Japan Automotive Bumper Market - Opportunity Assessment |

9.1 Japan Automotive Bumper Market Opportunity Assessment, By Material, 2024 & 2031F |

9.2 Japan Automotive Bumper Market Opportunity Assessment, By Technology, 2024 & 2031F |

9.3 Japan Automotive Bumper Market Opportunity Assessment, By Vehicle Type, 2024 & 2031F |

10 Japan Automotive Bumper Market - Competitive Landscape |

10.1 Japan Automotive Bumper Market Revenue Share, By Companies, 2024 |

10.2 Japan Automotive Bumper Market Competitive Benchmarking, By Operating and Technical Parameters |

11 Company Profiles |

12 Recommendations |

13 Disclaimer |

Export potential assessment - trade Analytics for 2030

Export potential enables firms to identify high-growth global markets with greater confidence by combining advanced trade intelligence with a structured quantitative methodology. The framework analyzes emerging demand trends and country-level import patterns while integrating macroeconomic and trade datasets such as GDP and population forecasts, bilateral import–export flows, tariff structures, elasticity differentials between developed and developing economies, geographic distance, and import demand projections. Using weighted trade values from 2020–2024 as the base period to project country-to-country export potential for 2030, these inputs are operationalized through calculated drivers such as gravity model parameters, tariff impact factors, and projected GDP per-capita growth. Through an analysis of hidden potentials, demand hotspots, and market conditions that are most favorable to success, this method enables firms to focus on target countries, maximize returns, and global expansion with data, backed by accuracy.

By factoring in the projected importer demand gap that is currently unmet and could be potential opportunity, it identifies the potential for the Exporter (Country) among 190 countries, against the general trade analysis, which identifies the biggest importer or exporter.

To discover high-growth global markets and optimize your business strategy:

Click Here

Pricing

- Single User License$ 1,995

- Department License$ 2,400

- Site License$ 3,120

- Global License$ 3,795

Search

Thought Leadership and Analyst Meet

Our Clients

Latest Reports

- Canada Cloud CFD Market (2026-2032) | Size & Revenue, Industry, Growth, Competitive Landscape, Forecast, Segmentation, Value, Outlook, Trends, Share, Analysis, Companies

- Taiwan Food Delivery Platform Market (2026-2032) | Companies, Outlook, Analysis, Trends, Value, Revenue, Segmentation, Share, Forecast, Competitive Landscape, Growth, Size & Forecast

- United Kingdom (UK) Long-term Care Insurance Market (2026-2032) | Growth, Share, Consumer Insights, Drivers, Opportunities, Competition, Pricing Analysis, Segments, Restraints, Companies, Competitive, Value, Outlook, Size, Demand, Analysis, Challenges, Strategic Insights, Investment Trends, Revenue, Trends, Supply, Forecast

- United Kingdom (UK) Long Term Care Market (2026-2032) | Companies, Outlook, Analysis, Trends, Value, Revenue, Segmentation, Share, Forecast, Competitive Landscape, Growth, Size & Forecast

- Iraq Insulation and Waterproofing Market (2026-2032) | Outlook, Drivers, Growth, Size, Share, Industry, Revenue, Trends, Demand, Competitive, Strategic Insights, Opportunities, Segments, Companies, Challenges, Strategy, Consumer Insights, Analysis, Investment Trends, Value, Segmentation, Forecast, Restraints

- India Switchgear Market Outlook (2026-2032) | Size, Share, Trends, Growth, Revenue, Forecast, Analysis, Value, Outlook

- Pakistan Contraceptive Implants Market (2025-2031) | Demand, Growth, Size, Share, Industry, Pricing Analysis, Competitive, Strategic Insights, Strategy, Consumer Insights, Analysis, Investment Trends, Opportunities, Revenue, Segments, Value, Segmentation, Supply, Forecast, Restraints, Outlook, Competition, Drivers, Trends, Companies, Challenges

- Sri Lanka Packaging Market (2026-2032) | Outlook, Competition, Drivers, Trends, Demand, Pricing Analysis, Competitive, Strategic Insights, Companies, Challenges, Strategy, Consumer Insights, Analysis, Investment Trends, Opportunities, Growth, Size, Share, Industry, Revenue, Segments, Value, Segmentation, Supply, Forecast, Restraints

- India Kids Watches Market (2026-2032) | Strategy, Consumer Insights, Analysis, Investment Trends, Opportunities, Growth, Size, Share, Industry, Revenue, Segments, Value, Segmentation, Supply, Forecast, Restraints, Outlook, Competition, Drivers, Trends, Demand, Pricing Analysis, Competitive, Strategic Insights, Companies, Challenges

- Saudi Arabia Core Assurance Service Market (2025-2031) | Strategy, Consumer Insights, Analysis, Investment Trends, Opportunities, Growth, Size, Share, Industry, Revenue, Segments, Value, Segmentation, Supply, Forecast, Restraints, Outlook, Competition, Drivers, Trends, Demand, Pricing Analysis, Competitive, Strategic Insights, Companies, Challenges

Industry Events and Analyst Meet

India EV Show 2026

EV tech India Expo 2026

Auto Tech Asia 2026

Battery Tech India 2026

Smart Production Solutions Guangzhou 2026

Whitepaper

- Middle East & Africa Commercial Security Market Click here to view more.

- Middle East & Africa Fire Safety Systems & Equipment Market Click here to view more.

- GCC Drone Market Click here to view more.

- Middle East Lighting Fixture Market Click here to view more.

- GCC Physical & Perimeter Security Market Click here to view more.

6WResearch In News

- Doha a strategic location for EV manufacturing hub: IPA Qatar

- Demand for luxury TVs surging in the GCC, says Samsung

- Empowering Growth: The Thriving Journey of Bangladesh’s Cable Industry

- Demand for luxury TVs surging in the GCC, says Samsung

- Video call with a traditional healer? Once unthinkable, it’s now common in South Africa

- Intelligent Buildings To Smooth GCC’s Path To Net Zero