Kuwait Liqueurs Market (2026-2032) | Companies, Analysis, Size, Share, Forecast, Trends, Industry, Outlook, Value, Growth & Revenue

Market Forecast By Type (Neutrals/Bitters, Creams, Fruit Flavored, Others), By Distribution Channel (Convenience Stores, On Premises, Retailers, Supermarkets), By Packaging (Glass, PET Bottle, Metal Can, Others) And Competitive Landscape

| Product Code: ETC044362 | Publication Date: Jan 2021 | Updated Date: Jun 2026 | Product Type: Report | |

| Publisher: 6Wresearch | Author: Summon Dutta | No. of Pages: 70 | No. of Figures: 35 | No. of Tables: 5 |

Kuwait Liqueurs Market Summary

The kuwait liqueurs market was estimated at USD 662 Million in 2025 and is projected to reach USD 1128 Million by 2032, growing at a CAGR of 9.1% from 2026 to 2032.

Kuwait Liqueurs Market Growth Rate Analysis (2021-2032)

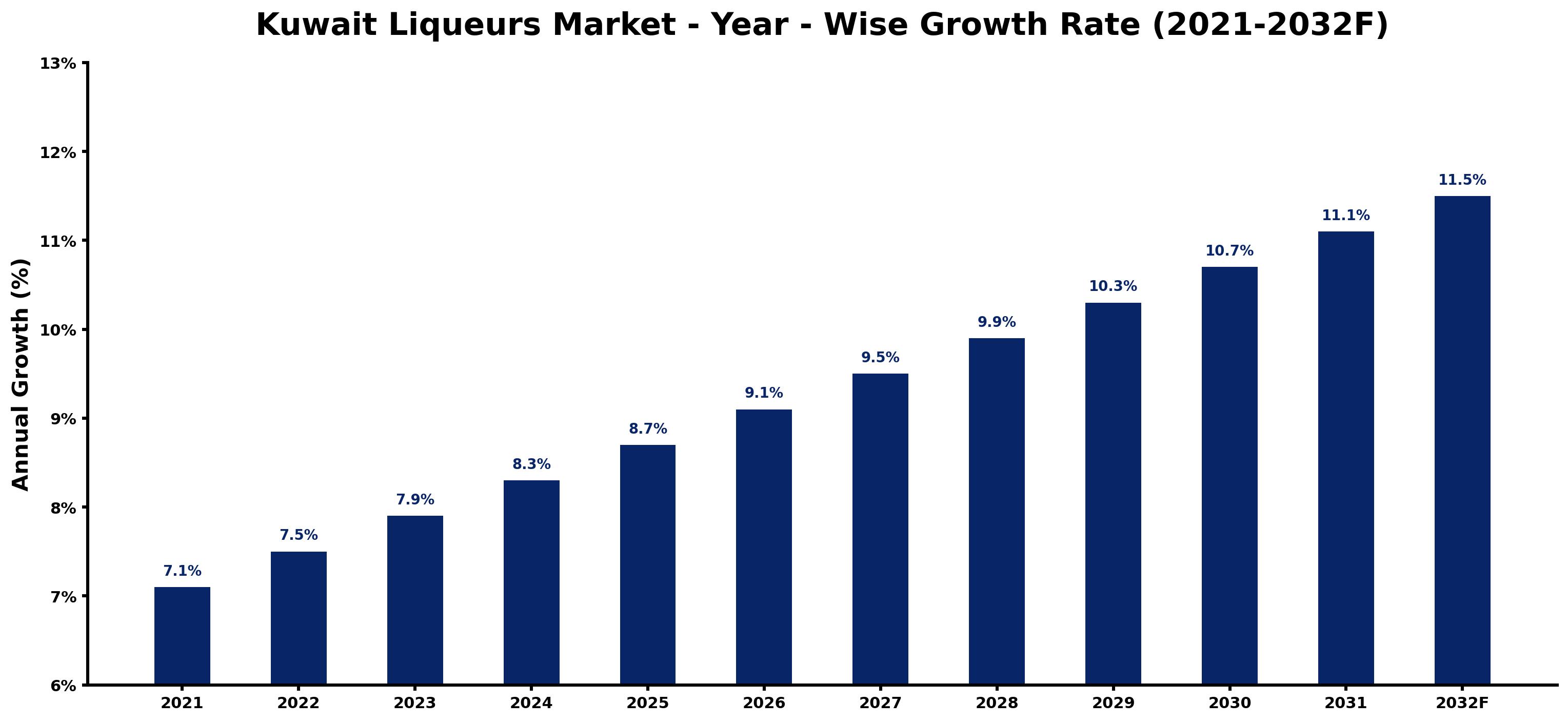

The Kuwait liqueurs market has showcased impressive growth, starting with a 7.1% increase in 2021 and accelerating to an anticipated 11.5% by 2032. This upward trend is primarily driven by rising consumer demand for premium and artisanal beverages, reflecting a broader shift towards quality and experience in the alcohol sector. Additionally, significant investments in local distillation capabilities and enhanced distribution channels have facilitated market accessibility, further fueling sales. The burgeoning tourism industry and changing social norms around alcohol consumption in Kuwait have also played pivotal roles in this expansion. As the market matures amidst ongoing digitalization efforts and evolving consumer preferences, liqueur brands are well-positioned for continued success.

Kuwait Liqueurs Market Year-wise Growth Rate and Key Drivers

This graph highlights how the Kuwait Liqueurs Market has steadily grown over the past five years, supported by major growth factors.

The table below presents the year wise growth rates along with the key drivers influencing the market

| Year | Growth Rate | Major Drivers |

| 2021 | 7.1% | The pandemic led to a surge in home consumption of alcoholic beverages in Kuwait. |

| 2022 | 7.5% | Local producers began emphasizing traditional flavors to attract younger consumers' interest. |

| 2023 | 7.9% | Increased disposable income among young professionals fostered new consumption patterns. |

| 2024 | 8.3% | Social media influencers began promoting premium liqueur brands, boosting brand visibility. |

| 2025 | 8.7% | Strategic partnerships with hotels enhanced the distribution of liqueurs in urban areas. |

| 2026 | 9.1% | Cultural shifts towards liberalization encouraged broader acceptance of liqueurs among consumers. |

| 2027 | 9.5% | Tourism revitalization initiatives opened new avenues for liqueur sales in nightlife sectors. |

| 2028 | 9.9% | Increased variety in flavors catered to diverse palates, attracting niche market segments. |

| 2029 | 10.3% | Sustainability trends led to organic and locally sourced liqueur options becoming popular. |

| 2030 | 10.7% | Innovations in packaging focused on eco-friendliness appealed to environmentally conscious customers. |

| 2031 | 11.1% | E-commerce platforms expanded, making liqueurs more accessible to a wider audience. |

| 2032 | 11.5% | The emergence of craft liqueur distilleries diversified the market with unique offerings. |

Note - Market size estimations and growth projections presented in this report are based on 6Wresearch's advanced forecasting approach, validated with industry datasets as of June 2026.

Kuwait Liqueurs Market Synopsis

The Kuwait Liqueurs Market is projected to reach 9.1% and witness significant growth during the forecast period (2026-2032). This market is shaped by a dual interest in traditional beverages and a rising inclination towards premium and imported liqueurs among the affluent segments of the population. Traditional options like arak and date-based liqueurs continue to dominate, but an increasing number of consumers are actively seeking out international brands and varied flavor profiles. The growth of this market is primarily driven by the country's robust economy, rising disposable incomes, and a burgeoning culture of socializing and home entertaining.

Kuwait Liqueurs Market Growth Drivers

Several key factors are fueling the expansion of the Kuwait liqueurs market:

- Economic Prosperity: A strong economy has led to increased disposable income among consumers, enabling them to explore premium liqueur options.

- Cultural Shifts: The growing preference for social gatherings and home entertainment promotes an increase in liqueur consumption, particularly in affluent communities.

- Experimentation with International Brands: Consumers are becoming more adventurous, showing a willingness to try various international liqueurs beyond traditional offerings.

- Emergence of Craft Cocktails: There is a rising trend towards craft cocktails and mixology, which in turn drives demand for unique and high-quality liqueurs.

- Health Consciousness: A growing awareness of health trends has led to an inclination towards lower-sugar and organic liqueurs, further diversifying the market offerings.

Kuwait Liqueurs Market Trends and Opportunities

In recent years, the Kuwait liqueurs market has seen a noticeable shift in consumer preferences that has opened several avenues for future growth:

- Premiumization: There is an evident trend towards premium and artisanal liqueurs, as consumers seek luxurious and sophisticated drinking experiences.

- Artisanal Products: Local and artisanal liqueurs, particularly those crafted from indigenous ingredients or traditional recipes, are gaining traction among discerning consumers.

- Innovative Flavors: With the ongoing interest in unique flavor profiles, brands have the opportunity to innovate and diversify their offerings to cater to evolving tastes.

- Healthier Options: The market is witnessing a surge in demand for healthier liqueurs, encouraging brands to explore lower-alcohol and organic alternatives.

- Consumer Education: Increased marketing and promotional activities focused on educating consumers about the versatility and variety of liqueurs can help enhance market visibility.

Kuwait Liqueurs Market Challenges and Restraints

Despite the promising growth prospects, the Kuwait liqueurs market faces several significant challenges:

- Regulatory Hurdles: Strict Islamic law prohibits alcohol consumption, leading to stringent regulations governing the production and distribution of liqueurs.

- Cultural Norms: Cultural resistance and societal norms surrounding alcohol consumption can limit market penetration and expansion efforts.

- Limited Distribution Channels: The availability of licensed retailers and distribution points is constrained, complicating access for consumers.

- Competition from Non-Alcoholic Beverages: A significant shift towards non-alcoholic alternatives poses a challenge to traditional liqueur consumption.

- Market Awareness: The need for enhanced consumer awareness regarding the quality and experience of premium liqueurs remains crucial for market growth.

Kuwait Liqueurs Market Investment Opportunities

The evolving dynamics of the Kuwait liqueurs market present various investment opportunities:

- Focus on Premium Brands: Investors have the chance to capitalize on the premiumization trend by developing or investing in high-quality liqueur brands.

- Niche Market Potential: Opportunities exist for artisanal and craft liqueur producers to penetrate the market with unique offerings.

- Partnerships with Distributors: Collaborating with local distributors can ensure better market reach and product visibility.

- Consumer Engagement: Investments in educational campaigns can foster brand loyalty and increase consumer interest in diverse liqueur options.

- Marketing Strategies: Allocating resources towards innovative marketing strategies can help elevate brand awareness and drive sales in a competitive market.

Kuwait Liqueurs Market Government Investment and Initiatives

Government policies related to the Kuwait liqueurs market are heavily influenced by Islamic law, which enforces strict regulations surrounding the production, sale, and consumption of alcohol. These include licensing and permits issued by the Public Authority for Industry, as well as taxation designed to deter excessive consumption. The government also limits advertising for alcoholic beverages, aiming to balance cultural and religious values with public health concerns. Compliance with these regulations is crucial for businesses seeking to establish a presence in the Kuwait liqueurs market, making it essential for them to navigate the complex regulatory landscape effectively.

Kuwait Liqueurs Market Latest Developments (May 2025 - June 2026)

Recent industry developments indicate a gradual but notable shift towards the acceptance of premium liqueurs among consumers in Kuwait. As social gatherings resume post-pandemic, there has been an uptick in demand for high-quality liqueurs, reflective of a broader trend towards luxury consumption. Additionally, brands are innovating to offer unique, limited-edition products that resonate with local preferences, while a rise in the number of specialty liquor retailers has improved accessibility for consumers. Despite the ongoing challenges posed by regulatory constraints, the market shows signs of resilience and adaptability, positioning itself for steady growth in the coming years.

Kuwait Liqueurs Market - Key Attractiveness of the Report

- 10 Years of Market Numbers

- Historical Data Starting from 2022 to 2025

- Base Year: 2025

- Forecast Data until 2032

- Key Performance Indicators Impacting the Market

- Major Upcoming Developments and Projects

Key Highlights of the Report:

- Kuwait Liqueurs Market Outlook

- Market Size of Kuwait Liqueurs Market, 2025

- Forecast of Kuwait Liqueurs Market, 2032F

- Historical Data and Forecast of Kuwait Liqueurs Revenues & Volume for the Period 2022-2032F

- Kuwait Liqueurs Market Trend Evolution

- Kuwait Liqueurs Market Drivers and Challenges

- Kuwait Liqueurs Price Trends

- Kuwait Liqueurs Porter's Five Forces

- Kuwait Liqueurs Industry Life Cycle

- Historical Data and Forecast of Kuwait Liqueurs Market Revenues & Volume By Type for the Period 2022-2032F

- Historical Data and Forecast of Kuwait Liqueurs Market Revenues & Volume By Neutrals/Bitters for the Period 2022-2032F

- Historical Data and Forecast of Kuwait Liqueurs Market Revenues & Volume By Creams for the Period 2022-2032F

- Historical Data and Forecast of Kuwait Liqueurs Market Revenues & Volume By Fruit Flavored for the Period 2022-2032F

- Historical Data and Forecast of Kuwait Liqueurs Market Revenues & Volume By Others for the Period 2022-2032F

- Historical Data and Forecast of Kuwait Liqueurs Market Revenues & Volume By Distribution Channel for the Period 2022-2032F

- Historical Data and Forecast of Kuwait Liqueurs Market Revenues & Volume By Convenience Stores for the Period 2022-2032F

- Historical Data and Forecast of Kuwait Liqueurs Market Revenues & Volume By On Premises for the Period 2022-2032F

- Historical Data and Forecast of Kuwait Liqueurs Market Revenues & Volume By Retailers for the Period 2022-2032F

- Historical Data and Forecast of Kuwait Liqueurs Market Revenues & Volume By Supermarkets for the Period 2022-2032F

- Historical Data and Forecast of Kuwait Liqueurs Market Revenues & Volume By Packaging for the Period 2022-2032F

- Historical Data and Forecast of Kuwait Liqueurs Market Revenues & Volume By Glass for the Period 2022-2032F

- Historical Data and Forecast of Kuwait Liqueurs Market Revenues & Volume By PET Bottle for the Period 2022-2032F

- Historical Data and Forecast of Kuwait Liqueurs Market Revenues & Volume By Metal Can for the Period 2022-2032F

- Historical Data and Forecast of Kuwait Liqueurs Market Revenues & Volume By Others for the Period 2022-2032F

- Kuwait Liqueurs Import Export Trade Statistics

- Market Opportunity Assessment By Type

- Market Opportunity Assessment By Distribution Channel

- Market Opportunity Assessment By Packaging

- Kuwait Liqueurs Top Companies Market Share

- Kuwait Liqueurs Competitive Benchmarking By Technical and Operational Parameters

- Kuwait Liqueurs Company Profiles

- Kuwait Liqueurs Key Strategic Recommendations

Frequently Asked Questions About the Market Study (FAQs):

The primary drivers include increasing disposable incomes, a growing preference for premium products, and a rising interest in social gatherings and cocktail culture.

Government regulations impose strict controls on alcohol production, sale, and marketing, which can limit market expansion but also create a niche for compliant brands.

Investors can explore premium liqueur brands, niche artisanal products, partnerships for better distribution, and consumer education initiatives to enhance market presence.

Trends include a focus on artisanal liqueurs, demand for healthier options, and a growing interest in innovative flavors and craft cocktails.

6Wresearch actively monitors the Kuwait Liqueurs Market and publishes its comprehensive annual report, highlighting emerging trends, growth drivers, revenue analysis, and forecast outlook. Our insights help businesses to make data-backed strategic decisions with ongoing market dynamics. Our analysts track relevent industries related to the Kuwait Liqueurs Market, allowing our clients with actionable intelligence and reliable forecasts tailored to emerging regional needs.

Yes, we provide customisation as per your requirements. To learn more, feel free to contact us on sales@6wresearch.com

1 Executive Summary |

2 Introduction |

2.1 Key Highlights of the Report |

2.2 Report Description |

2.3 Market Scope & Segmentation |

2.4 Research Methodology |

2.5 Assumptions |

3 Kuwait Liqueurs Market Overview |

3.1 Kuwait Country Macro Economic Indicators |

3.2 Kuwait Liqueurs Market Revenues & Volume, 2022 & 2032F |

3.3 Kuwait Liqueurs Market - Industry Life Cycle |

3.4 Kuwait Liqueurs Market - Porter's Five Forces |

3.5 Kuwait Liqueurs Market Revenues & Volume Share, By Type, 2022 & 2032F |

3.6 Kuwait Liqueurs Market Revenues & Volume Share, By Distribution Channel, 2022 & 2032F |

3.7 Kuwait Liqueurs Market Revenues & Volume Share, By Packaging, 2022 & 2032F |

4 Kuwait Liqueurs Market Dynamics |

4.1 Impact Analysis |

4.2 Market Drivers |

4.3 Market Restraints |

5 Kuwait Liqueurs Market Trends |

6 Kuwait Liqueurs Market, By Types |

6.1 Kuwait Liqueurs Market, By Type |

6.1.1 Overview and Analysis |

6.1.2 Kuwait Liqueurs Market Revenues & Volume, By Type, 2022-2032F |

6.1.3 Kuwait Liqueurs Market Revenues & Volume, By Neutrals/Bitters, 2022-2032F |

6.1.4 Kuwait Liqueurs Market Revenues & Volume, By Creams, 2022-2032F |

6.1.5 Kuwait Liqueurs Market Revenues & Volume, By Fruit Flavored, 2022-2032F |

6.1.6 Kuwait Liqueurs Market Revenues & Volume, By Others, 2022-2032F |

6.2 Kuwait Liqueurs Market, By Distribution Channel |

6.2.1 Overview and Analysis |

6.2.2 Kuwait Liqueurs Market Revenues & Volume, By Convenience Stores, 2022-2032F |

6.2.3 Kuwait Liqueurs Market Revenues & Volume, By On Premises, 2022-2032F |

6.2.4 Kuwait Liqueurs Market Revenues & Volume, By Retailers, 2022-2032F |

6.2.5 Kuwait Liqueurs Market Revenues & Volume, By Supermarkets, 2022-2032F |

6.3 Kuwait Liqueurs Market, By Packaging |

6.3.1 Overview and Analysis |

6.3.2 Kuwait Liqueurs Market Revenues & Volume, By Glass, 2022-2032F |

6.3.3 Kuwait Liqueurs Market Revenues & Volume, By PET Bottle, 2022-2032F |

6.3.4 Kuwait Liqueurs Market Revenues & Volume, By Metal Can, 2022-2032F |

6.3.5 Kuwait Liqueurs Market Revenues & Volume, By Others, 2022-2032F |

7 Kuwait Liqueurs Market Import-Export Trade Statistics |

7.1 Kuwait Liqueurs Market Export to Major Countries |

7.2 Kuwait Liqueurs Market Imports from Major Countries |

8 Kuwait Liqueurs Market Key Performance Indicators |

9 Kuwait Liqueurs Market - Opportunity Assessment |

9.1 Kuwait Liqueurs Market Opportunity Assessment, By Type, 2022 & 2032F |

9.2 Kuwait Liqueurs Market Opportunity Assessment, By Distribution Channel, 2022 & 2032F |

9.3 Kuwait Liqueurs Market Opportunity Assessment, By Packaging, 2022 & 2032F |

10 Kuwait Liqueurs Market - Competitive Landscape |

10.1 Kuwait Liqueurs Market Revenue Share, By Companies, 2025 |

10.2 Kuwait Liqueurs Market Competitive Benchmarking, By Operating and Technical Parameters |

11 Company Profiles |

12 Recommendations |

13 Disclaimer |

Global Go To Market Strategy - 2030

Export potential enables firms to identify high-growth global markets with greater confidence by combining advanced trade intelligence with a structured quantitative methodology. The framework analyzes emerging demand trends and country-level import patterns while integrating macroeconomic and trade datasets such as GDP and population forecasts, bilateral import–export flows, tariff structures, elasticity differentials between developed and developing economies, geographic distance, and import demand projections. Using weighted trade values from 2020–2024 as the base period to project country-to-country export potential for 2030, these inputs are operationalized through calculated drivers such as gravity model parameters, tariff impact factors, and projected GDP per-capita growth. Through an analysis of hidden potentials, demand hotspots, and market conditions that are most favorable to success, this method enables firms to focus on target countries, maximize returns, and global expansion with data, backed by accuracy.

By factoring in the projected importer demand gap that is currently unmet and could be potential opportunity, it identifies the potential for the Exporter (Country) among 190 countries, against the general trade analysis, which identifies the biggest importer or exporter.

To discover high-growth global markets and optimize your business strategy:

Click Here

Pricing

- Single User License$ 1,995

- Department License$ 2,400

- Site License$ 3,120

- Global License$ 3,795

Leadership Perspectives from Industry Events

Search

Thought Leadership and Analyst Meet

Our Clients

6WResearch In News

- India Air Conditioner Market Set for Strong Rebound in 2026 After Weather-Led Correction and GST-Driven Recovery: 6Wresearch

- ADAS in India: How Automatic Emergency Braking, Blind Spot Detection & Driver Monitoring are Transforming Road Safety

- Doha a strategic location for EV manufacturing hub: IPA Qatar

- Demand for luxury TVs surging in the GCC, says Samsung

- Empowering Growth: The Thriving Journey of Bangladesh’s Cable Industry

- Demand for luxury TVs surging in the GCC, says Samsung

Latest Reports

- Nicaragua RPG Gaming Market (2026-2032)

- New Zealand RPG Gaming Market (2026-2032)

- Netherlands RPG Gaming Market (2026-2032)

- Nauru RPG Gaming Market (2026-2032)

- Namibia RPG Gaming Market (2026-2032)

- Mozambique RPG Gaming Market (2026-2032)

- Montenegro RPG Gaming Market (2026-2032)

- Mongolia RPG Gaming Market (2026-2032)

- Monaco RPG Gaming Market (2026-2032)

- Micronesia RPG Gaming Market (2026-2032)

Industry Events and Analyst Meet

HIMTEX 2026

India Refining Summit 2026

India EV Show 2026

EV tech India Expo 2026

Auto Tech Asia 2026

Whitepaper

- Middle East & Africa Commercial Security Market Click here to view more.

- Middle East & Africa Fire Safety Systems & Equipment Market Click here to view more.

- GCC Drone Market Click here to view more.

- Middle East Lighting Fixture Market Click here to view more.

- GCC Physical & Perimeter Security Market Click here to view more.