United States (US) Structured Cabling Market Outlook | Forecast, Share, Industry, Revenue, Companies, Analysis, Growth, COVID-19 IMPACT, Trends, Value & Size

Market Forecast By Cable Type (Category 5E, Category 6, Category 6A), By Offering (Hardware, Services, Software), By Industry Vertical (IT & Telecommunications, Residential & Commercial, Government & Education, Transportation, Industrial, Others) And Competitive Landscape

| Product Code: ETC4460882 | Publication Date: Jul 2023 | Updated Date: Aug 2025 | Product Type: Report | |

| Publisher: 6Wresearch | Author: Bhawna Singh | No. of Pages: 85 | No. of Figures: 45 | No. of Tables: 25 |

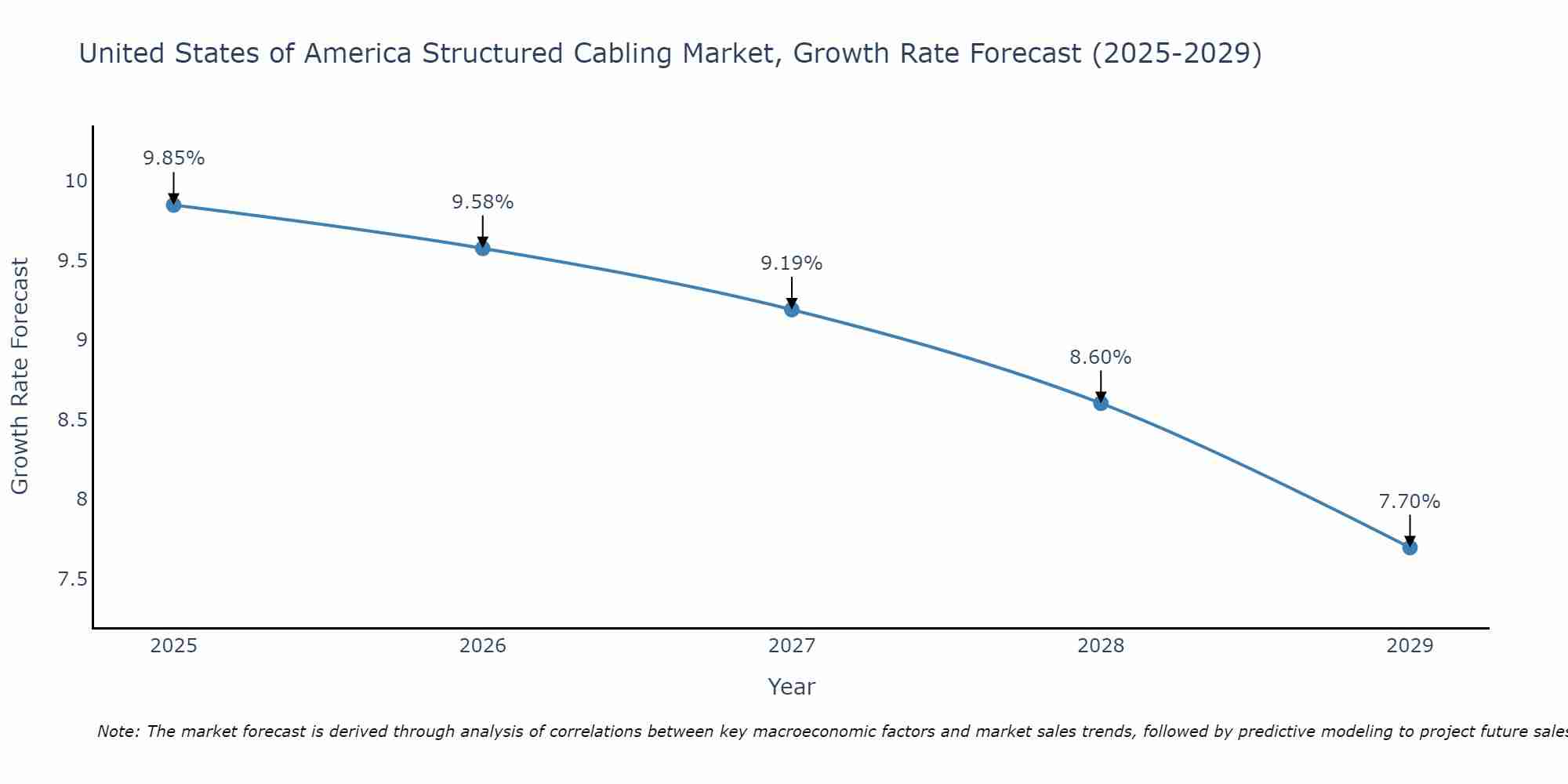

United States of America Structured Cabling Market Size Growth Rate

The United States of America Structured Cabling Market may undergo a gradual slowdown in growth rates between 2025 and 2029. Starting high at 9.85% in 2025, the market steadily declines to 7.70% by 2029.

United States (US) Structured Cabling Market Overview

The United States Structured Cabling Market is a highly competitive and rapidly growing sector driven by the increasing demand for high-speed internet connectivity, data centers, and advanced communication networks. The market encompasses a wide range of products such as copper cables, fiber optic cables, racks, cabinets, and connectors, catering to various industries including IT, telecommunications, healthcare, and government sectors. Key players in the US market include CommScope, Panduit, Corning Incorporated, and Legrand. The market is witnessing a shift towards advanced technologies like Category 6A and Category 8 cables to support faster data transmission speeds. Factors such as the growing adoption of cloud services, IoT devices, and smart technologies are expected to further drive the growth of the structured cabling market in the US.

United States (US) Structured Cabling Market Trends and Opportunities

The US Structured Cabling Market is experiencing significant growth driven by the increasing demand for high-speed internet connectivity, cloud services, and the adoption of IoT devices across various industries. The trend towards digital transformation and the need for reliable and scalable network infrastructure are driving the market. Opportunities in the market include the expansion of data centers, the deployment of 5G networks, and the implementation of smart building solutions. Technological advancements such as the development of Category 8 cabling standards and fiber optic cabling solutions are also contributing to market growth. With the rise in remote work and the growing importance of data security, the structured cabling market in the US is poised for continued expansion and innovation.

United States (US) Structured Cabling Market Challenges

In the US Structured Cabling Market, some key challenges include rapidly evolving technology, increasing demand for higher bandwidth, and the need for skilled labor to design, install, and maintain complex cabling systems. Keeping up with the latest advancements in cabling technology and ensuring compatibility with various devices can be a significant challenge for businesses. Additionally, the growing reliance on data-intensive applications and cloud services has led to a higher demand for cabling solutions that can support faster data transmission speeds and increased network capacity. Another challenge is the shortage of qualified technicians with the expertise to handle intricate cabling installations, which can lead to delays and increased costs for projects. Overall, addressing these challenges requires continuous training, investment in infrastructure, and strategic planning to meet the evolving needs of the market.

United States (US) Structured Cabling Market Drivers

The United States structured cabling market is being driven by several key factors. Firstly, the increasing demand for high-speed internet and data connectivity in both residential and commercial sectors is fueling the growth of structured cabling systems. Additionally, the rising adoption of advanced technologies such as Internet of Things (IoT), cloud computing, and Big Data analytics is driving the need for robust and reliable cabling infrastructure to support these applications. Moreover, the trend towards smart homes and smart buildings is also contributing to the market growth, as structured cabling is essential for enabling seamless connectivity and communication within these environments. Furthermore, the need for efficient and scalable network infrastructure to accommodate the growing volume of data traffic is further propelling the demand for structured cabling solutions in the US market.

United States (US) Structured Cabling Market Government Policies

In the United States, the Structured Cabling Market is governed by various policies and regulations aimed at ensuring quality, safety, and efficiency. The Telecommunications Industry Association (TIA) standards, including TIA-568 and TIA-569, set guidelines for the design and installation of cabling systems to support data and voice communication networks. Additionally, the National Electrical Code (NEC) mandates proper installation practices to maintain safety standards. Government initiatives such as the Federal Communication Commission`s (FCC) E-rate program provide funding for schools and libraries to improve their cabling infrastructure. Overall, these policies promote the use of high-quality cabling solutions, foster innovation, and support the growth of the Structured Cabling Market in the US.

United States (US) Structured Cabling Market Future Outlook

The future outlook for the United States Structured Cabling Market appears positive, driven by the increasing demand for high-speed data connectivity and the proliferation of Internet of Things (IoT) devices in various industries. The deployment of advanced technologies such as 5G, cloud computing, and smart infrastructure will further boost the demand for structured cabling solutions to support reliable and efficient data transmission. With the ongoing digital transformation across sectors like healthcare, education, and manufacturing, the market is expected to witness steady growth in the coming years. Additionally, the adoption of structured cabling systems to enhance network performance, scalability, and manageability will create opportunities for market players to offer innovative solutions tailored to meet evolving customer needs.

Key Highlights of the Report:

- United States (US) Structured Cabling Market Outlook

- Market Size of United States (US) Structured Cabling Market, 2022

- Forecast of United States (US) Structured Cabling Market, 2031

- Historical Data and Forecast of United States (US) Structured Cabling Revenues & Volume for the Period 2021 - 2031

- United States (US) Structured Cabling Market Trend Evolution

- United States (US) Structured Cabling Market Drivers and Challenges

- United States (US) Structured Cabling Price Trends

- United States (US) Structured Cabling Porter's Five Forces

- United States (US) Structured Cabling Industry Life Cycle

- Historical Data and Forecast of United States (US) Structured Cabling Market Revenues & Volume By Cable Type for the Period 2021 - 2031

- Historical Data and Forecast of United States (US) Structured Cabling Market Revenues & Volume By Category 5E for the Period 2021 - 2031

- Historical Data and Forecast of United States (US) Structured Cabling Market Revenues & Volume By Category 6 for the Period 2021 - 2031

- Historical Data and Forecast of United States (US) Structured Cabling Market Revenues & Volume By Category 6A for the Period 2021 - 2031

- Historical Data and Forecast of United States (US) Structured Cabling Market Revenues & Volume By Offering for the Period 2021 - 2031

- Historical Data and Forecast of United States (US) Structured Cabling Market Revenues & Volume By Hardware for the Period 2021 - 2031

- Historical Data and Forecast of United States (US) Structured Cabling Market Revenues & Volume By Services for the Period 2021 - 2031

- Historical Data and Forecast of United States (US) Structured Cabling Market Revenues & Volume By Software for the Period 2021 - 2031

- Historical Data and Forecast of United States (US) Structured Cabling Market Revenues & Volume By Industry Vertical for the Period 2021 - 2031

- Historical Data and Forecast of United States (US) Structured Cabling Market Revenues & Volume By IT & Telecommunications for the Period 2021 - 2031

- Historical Data and Forecast of United States (US) Structured Cabling Market Revenues & Volume By Residential & Commercial for the Period 2021 - 2031

- Historical Data and Forecast of United States (US) Structured Cabling Market Revenues & Volume By Government & Education for the Period 2021 - 2031

- Historical Data and Forecast of United States (US) Structured Cabling Market Revenues & Volume By Transportation for the Period 2021 - 2031

- Historical Data and Forecast of United States (US) Structured Cabling Market Revenues & Volume By Industrial for the Period 2021 - 2031

- Historical Data and Forecast of United States (US) Structured Cabling Market Revenues & Volume By Others for the Period 2021 - 2031

- United States (US) Structured Cabling Import Export Trade Statistics

- Market Opportunity Assessment By Cable Type

- Market Opportunity Assessment By Offering

- Market Opportunity Assessment By Industry Vertical

- United States (US) Structured Cabling Top Companies Market Share

- United States (US) Structured Cabling Competitive Benchmarking By Technical and Operational Parameters

- United States (US) Structured Cabling Company Profiles

- United States (US) Structured Cabling Key Strategic Recommendations

Frequently Asked Questions About the Market Study (FAQs):

6Wresearch actively monitors the United States (US) Structured Cabling Market and publishes its comprehensive annual report, highlighting emerging trends, growth drivers, revenue analysis, and forecast outlook. Our insights help businesses to make data-backed strategic decisions with ongoing market dynamics. Our analysts track relevent industries related to the United States (US) Structured Cabling Market, allowing our clients with actionable intelligence and reliable forecasts tailored to emerging regional needs.

Yes, we provide customisation as per your requirements. To learn more, feel free to contact us on sales@6wresearch.com

1 Executive Summary |

2 Introduction |

2.1 Key Highlights of the Report |

2.2 Report Description |

2.3 Market Scope & Segmentation |

2.4 Research Methodology |

2.5 Assumptions |

3 United States (US) Structured Cabling Market Overview |

3.1 United States (US) Country Macro Economic Indicators |

3.2 United States (US) Structured Cabling Market Revenues & Volume, 2022 & 2031F |

3.3 United States (US) Structured Cabling Market - Industry Life Cycle |

3.4 United States (US) Structured Cabling Market - Porter's Five Forces |

3.5 United States (US) Structured Cabling Market Revenues & Volume Share, By Cable Type, 2022 & 2031F |

3.6 United States (US) Structured Cabling Market Revenues & Volume Share, By Offering, 2022 & 2031F |

3.7 United States (US) Structured Cabling Market Revenues & Volume Share, By Industry Vertical, 2022 & 2031F |

4 United States (US) Structured Cabling Market Dynamics |

4.1 Impact Analysis |

4.2 Market Drivers |

4.2.1 Increasing demand for high-speed connectivity and data transmission |

4.2.2 Growing adoption of IoT devices and smart technologies |

4.2.3 Expansion of data centers and cloud computing services |

4.3 Market Restraints |

4.3.1 High initial investment and installation costs |

4.3.2 Long replacement cycle for structured cabling systems |

4.3.3 Competition from wireless technologies |

5 United States (US) Structured Cabling Market Trends |

6 United States (US) Structured Cabling Market, By Types |

6.1 United States (US) Structured Cabling Market, By Cable Type |

6.1.1 Overview and Analysis |

6.1.2 United States (US) Structured Cabling Market Revenues & Volume, By Cable Type, 2021 - 2031F |

6.1.3 United States (US) Structured Cabling Market Revenues & Volume, By Category 5E, 2021 - 2031F |

6.1.4 United States (US) Structured Cabling Market Revenues & Volume, By Category 6, 2021 - 2031F |

6.1.5 United States (US) Structured Cabling Market Revenues & Volume, By Category 6A, 2021 - 2031F |

6.2 United States (US) Structured Cabling Market, By Offering |

6.2.1 Overview and Analysis |

6.2.2 United States (US) Structured Cabling Market Revenues & Volume, By Hardware, 2021 - 2031F |

6.2.3 United States (US) Structured Cabling Market Revenues & Volume, By Services, 2021 - 2031F |

6.2.4 United States (US) Structured Cabling Market Revenues & Volume, By Software, 2021 - 2031F |

6.3 United States (US) Structured Cabling Market, By Industry Vertical |

6.3.1 Overview and Analysis |

6.3.2 United States (US) Structured Cabling Market Revenues & Volume, By IT & Telecommunications, 2021 - 2031F |

6.3.3 United States (US) Structured Cabling Market Revenues & Volume, By Residential & Commercial, 2021 - 2031F |

6.3.4 United States (US) Structured Cabling Market Revenues & Volume, By Government & Education, 2021 - 2031F |

6.3.5 United States (US) Structured Cabling Market Revenues & Volume, By Transportation, 2021 - 2031F |

6.3.6 United States (US) Structured Cabling Market Revenues & Volume, By Industrial, 2021 - 2031F |

6.3.7 United States (US) Structured Cabling Market Revenues & Volume, By Others, 2021 - 2031F |

7 United States (US) Structured Cabling Market Import-Export Trade Statistics |

7.1 United States (US) Structured Cabling Market Export to Major Countries |

7.2 United States (US) Structured Cabling Market Imports from Major Countries |

8 United States (US) Structured Cabling Market Key Performance Indicators |

8.1 Average project completion time for structured cabling installations |

8.2 Percentage of buildings equipped with Category 6 or higher cabling |

8.3 Percentage of companies investing in network infrastructure upgrades |

8.4 Average data transmission speeds achieved with structured cabling |

8.5 Rate of adoption of fiber-optic cabling technologies |

9 United States (US) Structured Cabling Market - Opportunity Assessment |

9.1 United States (US) Structured Cabling Market Opportunity Assessment, By Cable Type, 2022 & 2031F |

9.2 United States (US) Structured Cabling Market Opportunity Assessment, By Offering, 2022 & 2031F |

9.3 United States (US) Structured Cabling Market Opportunity Assessment, By Industry Vertical, 2022 & 2031F |

10 United States (US) Structured Cabling Market - Competitive Landscape |

10.1 United States (US) Structured Cabling Market Revenue Share, By Companies, 2022 |

10.2 United States (US) Structured Cabling Market Competitive Benchmarking, By Operating and Technical Parameters |

11 Company Profiles |

12 Recommendations |

13 Disclaimer |

Export potential assessment - trade Analytics for 2030

Export potential enables firms to identify high-growth global markets with greater confidence by combining advanced trade intelligence with a structured quantitative methodology. The framework analyzes emerging demand trends and country-level import patterns while integrating macroeconomic and trade datasets such as GDP and population forecasts, bilateral import–export flows, tariff structures, elasticity differentials between developed and developing economies, geographic distance, and import demand projections. Using weighted trade values from 2020–2024 as the base period to project country-to-country export potential for 2030, these inputs are operationalized through calculated drivers such as gravity model parameters, tariff impact factors, and projected GDP per-capita growth. Through an analysis of hidden potentials, demand hotspots, and market conditions that are most favorable to success, this method enables firms to focus on target countries, maximize returns, and global expansion with data, backed by accuracy.

By factoring in the projected importer demand gap that is currently unmet and could be potential opportunity, it identifies the potential for the Exporter (Country) among 190 countries, against the general trade analysis, which identifies the biggest importer or exporter.

To discover high-growth global markets and optimize your business strategy:

Click Here

Pricing

- Single User License$ 1,995

- Department License$ 2,400

- Site License$ 3,120

- Global License$ 3,795

Search

Thought Leadership and Analyst Meet

Our Clients

Latest Reports

- Canada Cloud CFD Market (2026-2032) | Size & Revenue, Industry, Growth, Competitive Landscape, Forecast, Segmentation, Value, Outlook, Trends, Share, Analysis, Companies

- Taiwan Food Delivery Platform Market (2026-2032) | Companies, Outlook, Analysis, Trends, Value, Revenue, Segmentation, Share, Forecast, Competitive Landscape, Growth, Size & Forecast

- United Kingdom (UK) Long-term Care Insurance Market (2026-2032) | Growth, Share, Consumer Insights, Drivers, Opportunities, Competition, Pricing Analysis, Segments, Restraints, Companies, Competitive, Value, Outlook, Size, Demand, Analysis, Challenges, Strategic Insights, Investment Trends, Revenue, Trends, Supply, Forecast

- United Kingdom (UK) Long Term Care Market (2026-2032) | Companies, Outlook, Analysis, Trends, Value, Revenue, Segmentation, Share, Forecast, Competitive Landscape, Growth, Size & Forecast

- Iraq Insulation and Waterproofing Market (2026-2032) | Outlook, Drivers, Growth, Size, Share, Industry, Revenue, Trends, Demand, Competitive, Strategic Insights, Opportunities, Segments, Companies, Challenges, Strategy, Consumer Insights, Analysis, Investment Trends, Value, Segmentation, Forecast, Restraints

- India Switchgear Market Outlook (2026-2032) | Size, Share, Trends, Growth, Revenue, Forecast, Analysis, Value, Outlook

- Pakistan Contraceptive Implants Market (2025-2031) | Demand, Growth, Size, Share, Industry, Pricing Analysis, Competitive, Strategic Insights, Strategy, Consumer Insights, Analysis, Investment Trends, Opportunities, Revenue, Segments, Value, Segmentation, Supply, Forecast, Restraints, Outlook, Competition, Drivers, Trends, Companies, Challenges

- Sri Lanka Packaging Market (2026-2032) | Outlook, Competition, Drivers, Trends, Demand, Pricing Analysis, Competitive, Strategic Insights, Companies, Challenges, Strategy, Consumer Insights, Analysis, Investment Trends, Opportunities, Growth, Size, Share, Industry, Revenue, Segments, Value, Segmentation, Supply, Forecast, Restraints

- India Kids Watches Market (2026-2032) | Strategy, Consumer Insights, Analysis, Investment Trends, Opportunities, Growth, Size, Share, Industry, Revenue, Segments, Value, Segmentation, Supply, Forecast, Restraints, Outlook, Competition, Drivers, Trends, Demand, Pricing Analysis, Competitive, Strategic Insights, Companies, Challenges

- Saudi Arabia Core Assurance Service Market (2025-2031) | Strategy, Consumer Insights, Analysis, Investment Trends, Opportunities, Growth, Size, Share, Industry, Revenue, Segments, Value, Segmentation, Supply, Forecast, Restraints, Outlook, Competition, Drivers, Trends, Demand, Pricing Analysis, Competitive, Strategic Insights, Companies, Challenges

Industry Events and Analyst Meet

India EV Show 2026

EV tech India Expo 2026

Auto Tech Asia 2026

Battery Tech India 2026

Smart Production Solutions Guangzhou 2026

Whitepaper

- Middle East & Africa Commercial Security Market Click here to view more.

- Middle East & Africa Fire Safety Systems & Equipment Market Click here to view more.

- GCC Drone Market Click here to view more.

- Middle East Lighting Fixture Market Click here to view more.

- GCC Physical & Perimeter Security Market Click here to view more.

6WResearch In News

- Doha a strategic location for EV manufacturing hub: IPA Qatar

- Demand for luxury TVs surging in the GCC, says Samsung

- Empowering Growth: The Thriving Journey of Bangladesh’s Cable Industry

- Demand for luxury TVs surging in the GCC, says Samsung

- Video call with a traditional healer? Once unthinkable, it’s now common in South Africa

- Intelligent Buildings To Smooth GCC’s Path To Net Zero