India Export Attractiveness Tracker 2026

Smartphones and Diamonds Lead India's Core Market Opportunities

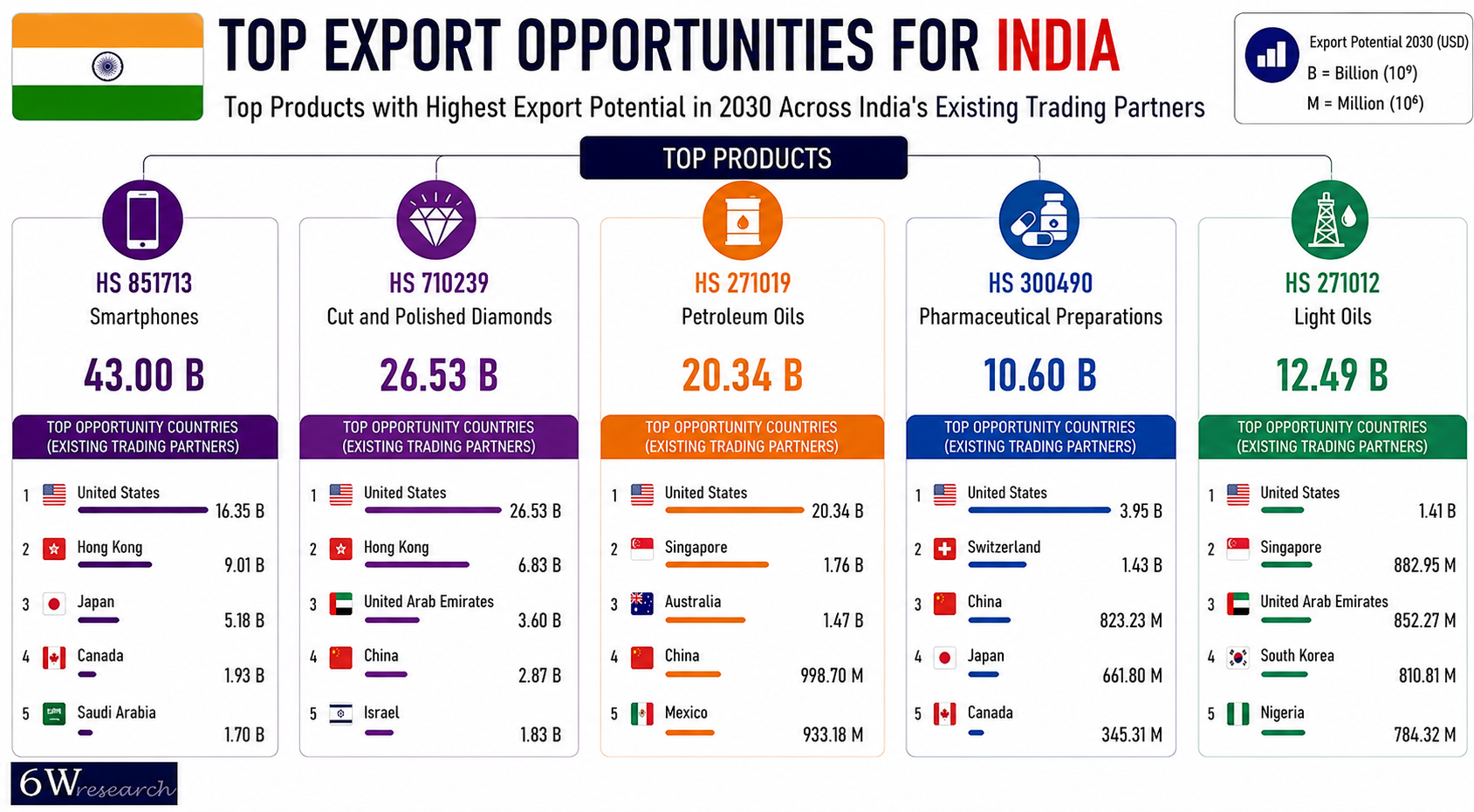

Smartphones signify India's largest export opportunity in its core markets, with a total potential of USD 43.0 billion. India's trade base A small set of established sectors currently leads India's trade base, each supported by 2030. by a small set of established sectors, each supported by 2030. Within this analysis, the top five importing countries together held US$34.2 billion in export potential, underpinning the concentration of India’s smartphone export opportunity across high-value electronics markets. The United States has the biggest potential at USD 16.3 billion, helped by companies looking to diversify their supply chains and by incentives for assembling devices in India. Apart from this, Hong Kong follows at USD 9.0 billion, functioning largely as a re-export and distribution gateway into wider Asian and mainland Chinese markets. Japan adds USD 5.2 billion, which aligns with efforts India's current trade base is led by a small set of established sectors, each supported by East Asian electronics buyers to diversify their sources due to concerns about supply-chain stability in the region, while Canada and Saudi Arabia together contribute an additional USD 3.6 billion, showing that market access for devices made in India is steadily expanding.

In general, cut and polished diamonds represent a further potential of USD 26.5 billion, led by the United States (USD 8.8 billion) and Hong Kong (USD 6.8 billion), both established gem and jewelry trading centers, and the United Arab Emirates (USD 3.6 billion), where Dubai’s position as a global diamond re-export hub continues to grow trade flows. China (USD 2.9 billion) and Israel (USD 1.8 billion) round out a diversified diamond trading footprint tied to increasing luxury consumption and longstanding gem trading infrastructure respectively. Across the top five importing countries, cut and polished diamonds account for US$23.9 billion in export potential, highlighting India’s strong trade positioning in processed gems and global jewelry supply chains.

Both petroleum oils and light oils together add USD 32.8 billion in potential. The United States (USD 2.3 billion) and Singapore, a foremost refining and marine-fuel logistics hub, showcase the robust fuel-trade positioning, while China's bourgeoning refined-fuel demand amid constrained domestic refining capacity supports a further USD 1.0 billion in potential, and Australia's established trade lane adds USD 1.5 billion more. Light oils show similar positioning across the United States, Singapore, and the United Arab Emirates, with South Korea's petrochemical feedstock demand adding USD 811 million, and Nigeria representing an emerging opportunity worth USD 784 million as domestic refining capacity there continues to evolve.

Pharmaceutical preparations close the top five at USD 10.6 billion, led decisively by the United States at USD 3.9 billion, accelerated by India's scale in cost-competitive, quality-certified generic drug manufacturing and continuing policy emphasis on affordable medicine access. Switzerland adds USD 1.4 billion, reflecting its role as a hub for specialty and complex generic trade, while China and Japan contribute a combined USD 1.5 billion tied to expanding regulatory approval pathways and aging-population demand respectively, and Canada rounds out the category with a further USD 345 million.

Light Diesel Vans and Light Oils Open New Export Frontiers

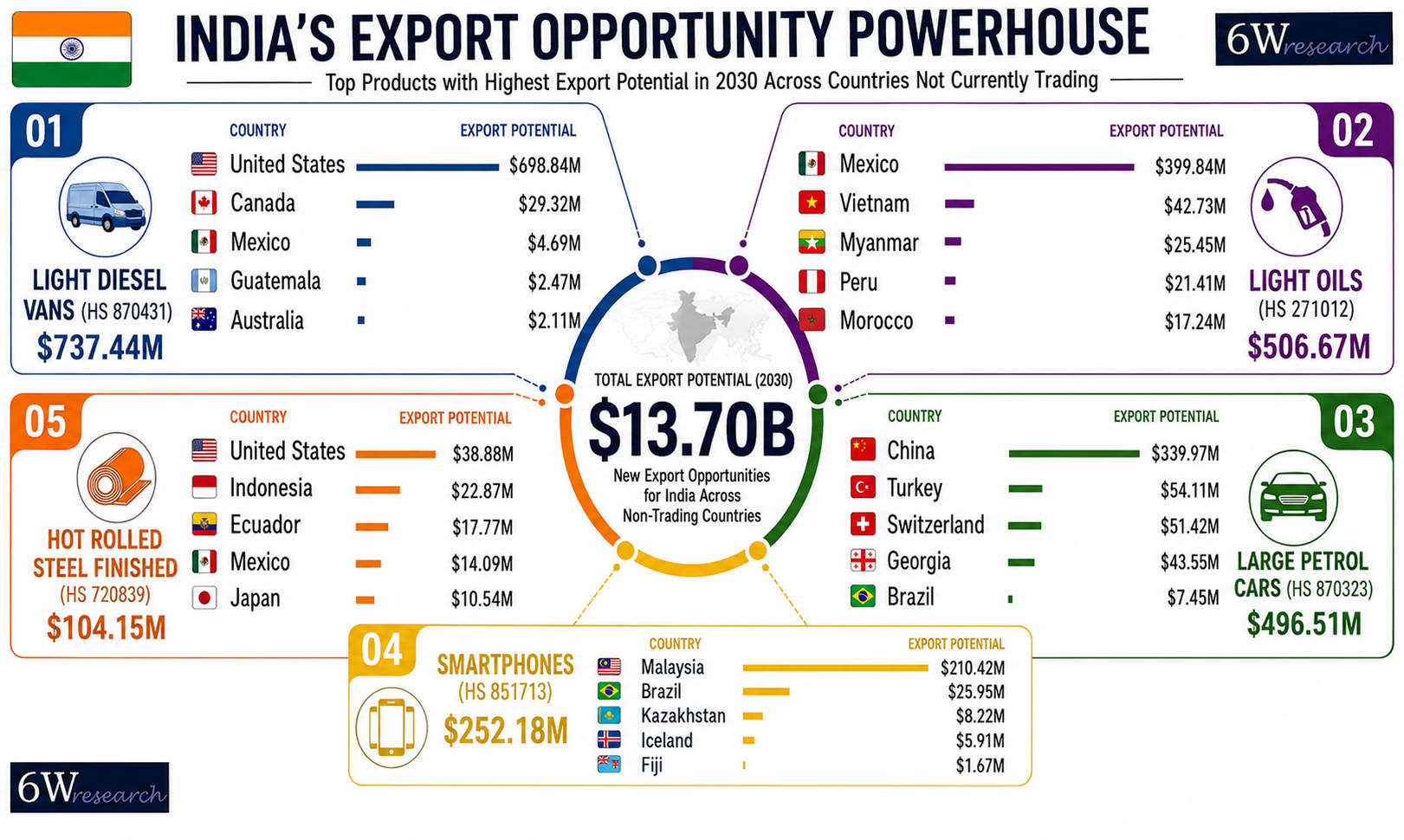

Light diesel vans display the India’s leading emerging export opportunity with a total potential of USD 741 million by 2030, of which the top five importing country account for USD 737.4 million. The United States leads at USD 699 million, supported by continued expansion of e-commerce logistics and last mile delivery fleets that favor cost-competitive commercial vehicle sourcing, positioning India as a new export entrant in the market where demand is scaling quickly. Canada adds USD 29 million tied to similar fleet-renewal cycles within an integrated North American logistics network while Mexico, Guatemala and Australia add smaller amounts linked to expanding regional freight and distribution activity. Light oils add a further USD 689 million in total potential, with the top five importing countries representing USD 506.7 million. Mexico leads at USD 400 million, where deepening energy trade corridors and growing industrial fuel demand support new supply positioning, while Vietnam, Myanmar, Peru and Morocco reflect rising fuel demand tied to manufacturing, transport activity and market-access development.

Large petrol cars add up to USD 534 million in total potential, with the top five importing countries together accounting for USD 496.5 million. China remains the top market (USD 340 million), driven by steady demand across premium vehicle segments. Turkey and Georgia are benefiting from their location along logistics corridors linking Asian exporters with destination markets in Europe and Central Asia.

Switzerland and Brazil round out smaller, niche positions. Smartphones add USD 254 million in total potential, with the top five importing country accounting for USD 252.2 million, led by Malaysia at USD 210 million, where established electronics distribution infrastructure supports regional demand and re-export activity. Hot-rolled steel sheets close the list at USD 157 million in total potential, with the top five markets contributing USD 105.2 million, led by the United States, while Indonesia, Ecuador, Mexico and Japan reflect industrial, infrastructure and supply-chain diversification opportunities.

Apart from these product lines, semiconductor-linked exports present a further category worth building toward across new destination markets. As global electronics manufacturers continue diversifying assembly and testing capacity away from concentrated production hubs, India's expanding packaging and testing infrastructure positions it to serve surging demand in markets such as Vietnam, where electronics assembly activity is growing at significant pace, and in Europe and the United States, where policy direction extensively favors broader semiconductor supply-chain diversification. This trend is still in its initial stages relative to India's established product lines, but it reflects a logical extension of India's existing industrial policy direction and increasing trade positioning in electronics manufacturing.

What India Should Prioritize Next

India's strongest export priorities remain smartphones and cut and polished diamonds into the United States and Hong Kong, underpinned by massive pharmaceutical trade positioning into the same markets and by broadening petroleum and light oils footprint across Singapore, the United States, and emerging refining-constrained markets. Alongside these core priorities, several additional opportunities stand out as genuinely achievable when measured against India's existing industrial capacity and trade positioning. Iron ore exports to China are well aligned with India's existing mining and export infrastructure, positioning it to capture incremental share as global steelmakers diversify sourcing away from concentrated supply routes.

Top Global Export Opportunities (2030), By Product

| Product Name | Export Opportunity (USD Billion) |

| Electronic Integrated Circuits | 478.41 |

| Petroleum Oils | 343.34 |

| Logic Integrated Circuits | 307.47 |

| Light Oils | 283.82 |

| Pharmaceutical Preparations | 219.91 |

| Large Petrol Cars | 204.35 |

| Memory Integrated Circuits | 199.57 |

| Smartphones | 167.17 |

| Data Transmission Equipment | 145.82 |

| Computer Parts | 127.55 |

Semiconductor trade growth into China, currently led by established chip manufacturers, presents a longer-term opportunity for India through packaging, testing, and assembly capacity that is already being built out under current industrial policy direction, rather than a near-term entry into full-scale chip fabrication. Smartphone exports into the United States market also stand to benefit further as global supply-chain diversification continues to favor manufacturing locations outside single-country concentration, strengthening a trend already underway in India's own export base rather than requiring a new market-entry effort.

Portable computer assembly for the United States market follows a similar logic, driven by expanding domestic hardware manufacturing incentives and growing interest from global electronics brands in broadening their assembly footprint. Together, these priorities reflect opportunities where India's existing industrial base, policy direction, and trade positioning are already aligned with future demand growth, rather than opportunities that would require building entirely new capability from a standing start.

Currently Petroleum, Smartphones and Pharma Anchor India's Trade

India's current trade base is led by a small set of established sectors, each backed by scaled domestic industrial capacity. Oil & Gas leads at USD 69.2 billion, split between petroleum oils (71.3% share) and light oils (28.5%), underpinned by large-scale domestic refining capacity that positions India as a major regional fuel-processing base. Telecommunications & Technology follows at USD 21.8 billion, almost entirely smartphones (92.6%), reinforced by expanding domestic assembly incentives that continue to draw global device manufacturers toward India-based production lines, while Pharmaceuticals contributes USD 20.6 billion, led by pharmaceutical preparations (85.5%) and antibiotic medicaments (5.8%), reflecting India's position as a high-volume, quality-certified generic drug manufacturer.

There are three standout markets by value trade. The United States leads at USD 79.4 billion, led by pharmaceutical preparations (9.6%) and smartphones (8.8%), supported by a large regulated generics market and the continuation of supply-chain diversification that favors India-based device assembly. The United Arab Emirates follows at USD 37.1 billion, led by precious metal jewelry (13.4%) and light oils (10.1%), reflecting Dubai's established position as a global gold and jewelry trading hub alongside its role in regional fuel distribution and re-export logistics. The Netherlands rounds out the top three at USD 24.2 billion, led by petroleum oils (61.3%), reflecting Rotterdam's role as one of Europe's largest refining and fuel-distribution gateways, where high recorded volumes often represent onward distribution across the wider European market rather than final domestic consumption alone.

Current Highest Exports Sectors for India

| Sector | Exports | Leading Products / Share |

| Oil & Gas | USD 69.2B | Petroleum Oils (71.3%), Light Oils (28.5%) |

| Telecommunications & Technology | USD 21.8B | Smartphones (92.6%) |

| Pharmaceuticals | USD 20.6B | Pharmaceutical Preparations (85.5%) |

Current Leading Importers for India

| Country | Exports | Leading Products / Share |

| United States | USD 79.4B | Pharmaceutical Preparations (9.6%), Smartphones (8.8%) |

| United Arab Emirates | USD 37.1B | Precious Metal Jewelry (13.4%), Light Oils (10.1%) |

| Netherlands | USD 24.2B | Petroleum Oils (61.3%) |

Tariffs: A Minor Cost, not a Barrier to Growth

The highest tariff exposure is represented by China's 20% tariff on crushed chilies, the UK's 19.5% duty on semi-milled rice, and Saudi Arabia's 15% duty on copper wire and welded pipes. Since these are smaller trade lines rather than India's highest-value exports, these tariffs are a minor cost factor rather than a significant obstacle to overall expansion. India's biggest opportunities, on the other hand, have little exposure: car parts into the US face only 2.5%, petroleum oils into Mexico face 3.0%, and diamonds and pharmaceutical preparations into China face just 4.0%. This represents the India's highest-value trade flows already benefit from low tariff rates. The recently concluded India-UK trade agreement could gradually improve tariff access and rules of origin for lines such as rice, while India's partnership with EFTA nations continues strengthening market competitiveness across several categories.

Highest Applied Tariff Products

| Country | Highest Tariffs Products | Tariff | 2030 Potential | Current Trade |

| China | Crushed Chilies | 20% | USD 225M | USD 455M |

| United Kingdom | Semi-Milled Rice | 19.5% | USD 87M | USD 199M |

| Saudi Arabia | Copper Wire | 15% | USD 220M | USD 477M |

| Saudi Arabia | Longitudinal Welded Pipes | 15% | USD 69M | USD 245M |

Lowest Applied Tariff Products

| Country | Lowest Tariffs Products | Tariff | 2030 Potential | Current Trade |

| United States | Vehicle Parts | 2.5% | USD 487M | USD 920M |

| Mexico | Petroleum Oils | 3% | USD 933M | USD 1.5M |

| China | Cut and Polished Diamonds | 4% | USD 2.87B | USD 8.8M |

| China | Pharmaceutical Preparations | 4% | USD 823M | USD 70M |

Leadership Perspectives from Industry Events

Search

Thought Leadership and Analyst Meet

Our Clients

6WResearch In News

- India Export Attractiveness Tracker 2026

- India Air Conditioner Market Set for Strong Rebound in 2026 After Weather-Led Correction and GST-Driven Recovery: 6Wresearch

- ADAS in India: How Automatic Emergency Braking, Blind Spot Detection & Driver Monitoring are Transforming Road Safety

- Doha a strategic location for EV manufacturing hub: IPA Qatar

- Demand for luxury TVs surging in the GCC, says Samsung

- Empowering Growth: The Thriving Journey of Bangladesh’s Cable Industry

Latest Reports

- Nicaragua RPG Gaming Market (2026-2032)

- New Zealand RPG Gaming Market (2026-2032)

- Netherlands RPG Gaming Market (2026-2032)

- Nauru RPG Gaming Market (2026-2032)

- Namibia RPG Gaming Market (2026-2032)

- Mozambique RPG Gaming Market (2026-2032)

- Montenegro RPG Gaming Market (2026-2032)

- Mongolia RPG Gaming Market (2026-2032)

- Monaco RPG Gaming Market (2026-2032)

- Micronesia RPG Gaming Market (2026-2032)

Industry Events and Analyst Meet

EV India Expo 2026

HIMTEX 2026

India Refining Summit 2026

India EV Show 2026

EV tech India Expo 2026

Whitepaper

- Middle East & Africa Commercial Security Market Click here to view more.

- Middle East & Africa Fire Safety Systems & Equipment Market Click here to view more.

- GCC Drone Market Click here to view more.

- Middle East Lighting Fixture Market Click here to view more.

- GCC Physical & Perimeter Security Market Click here to view more.