United States (US) Cold Chain Market (2026-2032) Outlook | Value, Industry, Trends, Growth, Size, Companies, Forecast, Share, Analysis & Revenue

Market Forecast By Temperature Type (Frozen, Chilled), By Type (Refrigerated warehousing, Refrigerated transport), By Application (Dairy & frozen desserts, Fish, meat, and seafood products, Bakery & confectionery products, Fruits & vegetables, Others) And Competitive Landscape

| Product Code: ETC319561 | Publication Date: Aug 2022 | Updated Date: Jul 2026 | Product Type: Market Research Report | |

| Publisher: 6Wresearch | Author: Ravi Bhandari | No. of Pages: 75 | No. of Figures: 35 | No. of Tables: 20 |

United States (US) Cold Chain Market Size, Share & Growth Rate

The United States (US) Cold Chain Market was estimated at USD 231 Million in 2025 and is projected to reach USD 314 Million by 2032, growing at a CAGR of 4.5% from 2026 to 2032. This upward trajectory is being fueled by the increasing demand for perishable goods in sectors like food and pharmaceuticals, as well as advancements in technology that enhance operational efficiencies. With regulatory frameworks tightening around food safety and product integrity, the cold chain market is becoming an indispensable pillar of the logistics industry.

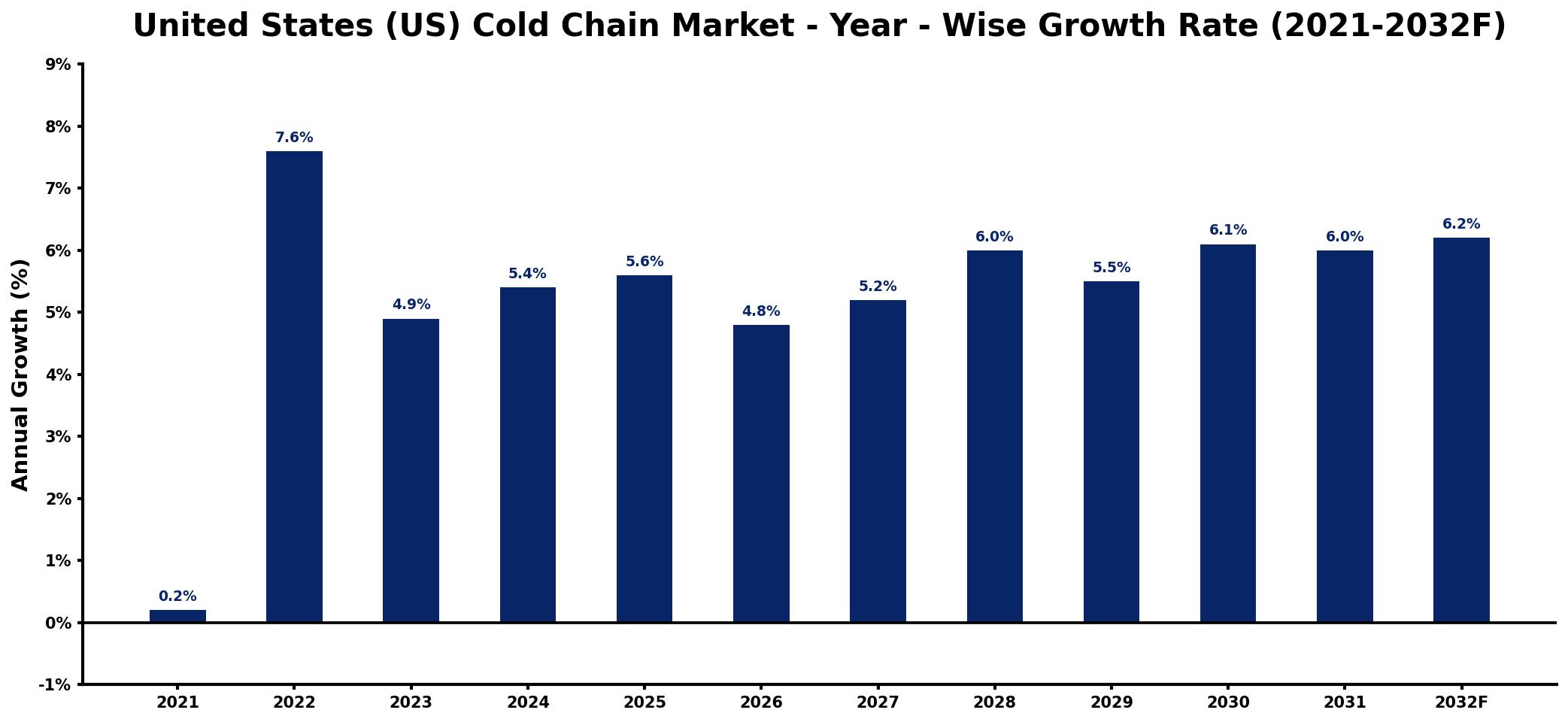

United States (US) Cold Chain Market Year-wise Growth Rate and Key Drivers

This graph highlights how the United States (US) Cold Chain Market has steadily grown over the years, supported by major growth factors.

The table below presents the year‑wise growth rates along with the key drivers influencing the market

| Year | Growth Rate | Major Drivers |

| 2021 | 0.2% | Rising demand for temperature-sensitive products |

| 2022 | 7.6% | Increased investments in logistics technology |

| 2023 | 4.9% | Growth in e-commerce food delivery |

| 2024 | 5.4% | Expansion of pharmaceutical distribution networks |

| 2025 | 5.6% | Surge in organic food consumption |

| 2026 | 4.8% | Innovations in packaging solutions |

| 2027 | 5.2% | increased overall sector activity |

| 2028 | 6.0% | expanding manufacturing base activity |

| 2029 | 5.5% | increased production capacity utilization |

| 2030 | 6.1% | Increase in online grocery shopping |

| 2031 | 6.0% | Emerging markets demand for quality |

| 2032 | 6.2% | Investments in renewable energy solutions |

Note: Market size estimations and growth projections presented in this report are based on 6Wresearch's proprietary forecasting methodology, utilizing the latest available industry data, government publications, and primary research inputs.

United States (US) Cold Chain Market Synopsis

In recent years, the United States Cold Chain Market has gained substantial momentum, driven by heightened consumer expectations for product quality and safety. This momentum is poised to escalate further as technological innovations and e-commerce continue to reshape the landscape of temperature-sensitive logistics.

The market is transitioning towards more sophisticated and sustainable practices, reflecting both the challenges posed by environmental regulations and the necessity of maintaining high standards for food and pharmaceutical products. As a result, key players are increasingly investing in advanced cold chain technologies that promise enhanced efficiency and compliance.

United States (US) Cold Chain Market Key Takeaways

- The market is projected to grow significantly, driven by escalating demand for perishable food and pharmaceutical products.

- Technological advancements, including IoT and automation, are becoming crucial for improving supply chain efficiency.

- Sustainability initiatives are gaining traction, compelling companies to adopt eco-friendly practices.

- Real-time monitoring and visibility are essential for maintaining product integrity and regulatory compliance.

- Investment opportunities are abundant, particularly in cold storage facilities and advanced logistics solutions.

Evaluation of Restraints in United States (US) Cold Chain Market

Despite its promising growth, the United States Cold Chain Market faces several restraints that could limit its full potential. One of the most significant challenges is ensuring the integrity of temperature-sensitive products throughout the supply chain. Additionally, companies must navigate complex regulatory landscapes to achieve compliance with food safety standards. High operational costs associated with cold storage and transportation can also impede market entry for new players. These factors necessitate ongoing innovation and investment in advanced technologies to maintain competitiveness and meet evolving customer expectations.

United States (US) Cold Chain Market Trends

Current trends in the United States Cold Chain Market reveal a strong inclination towards digitization and automation. Companies are increasingly adopting IoT-enabled monitoring systems, which provide real-time insights into temperature conditions, thereby enhancing transparency and accountability in the supply chain. Furthermore, there is an ongoing focus on sustainability, with many organizations opting for eco-friendly refrigeration solutions and biodegradable packaging materials. As the e-commerce sector expands, the demand for innovative cold chain logistics solutions tailored to meet direct-to-consumer delivery models is also on the rise.

United States (US) Cold Chain Market Opportunities

The United States Cold Chain Market presents a wealth of investment opportunities, particularly as the demand for temperature-sensitive products continues to soar. There is a notable need for expanding cold storage facilities, especially in urban areas where e-commerce is flourishing. Additionally, investing in advanced temperature monitoring technologies and cold chain management solutions promises lucrative returns. Companies that focus on automation and data analytics will find fertile ground for growth as they seek to optimize efficiency and mitigate risks within the logistics framework.

Government Initiatives in the United States (US) Cold Chain Market

Government policies play a pivotal role in shaping the United States Cold Chain Market. Regulatory bodies such as the FDA and USDA have established stringent guidelines to ensure the safety and quality of temperature-sensitive products during transportation and storage. These agencies also promote funding programs aimed at enhancing cold chain infrastructure, facilitating technological advancement, and fostering sustainability in logistics practices. Such initiatives are crucial for ensuring the reliability and efficiency of the cold chain network in the US.

Future Insights of the United States (US) Cold Chain Market

Looking ahead, the future of the United States Cold Chain Market appears bright, with significant growth anticipated through 2032. As the demand for pharmaceuticals, fresh produce, and vaccines rises, the market will increasingly rely on innovative logistics solutions to safeguard product integrity. Technological advancements will further enhance the efficiency of cold chain operations, paving the way for increased automation and data-driven decision-making. Sustainability will remain at the forefront, with industry players likely to adopt practices that not only comply with regulations but also contribute to a reduced carbon footprint.

United States (US) Cold Chain Market Latest Developments (2025 - 2026)

In recent months, the United States Cold Chain Market has witnessed a surge in developments focusing on technology and sustainability. Companies are increasingly investing in green refrigeration systems and energy-efficient practices to address environmental concerns. Moreover, partnerships among cold storage operators and technology firms have become more common, aimed at integrating advanced monitoring systems into existing infrastructures. These developments indicate a concerted effort to improve not only operational efficiency but also compliance with evolving regulatory standards.

United States (US) Cold Chain Market - Key Attractiveness of the Report

- 10 Years of Market Numbers

- Historical Data Starting from 2022 to 2025

- Base Year: 2025

- Forecast Data until 2032

- Key Performance Indicators Impacting the Market

- Major Upcoming Developments and Projects

Key Highlights of the Report:

- United States (US) Cold Chain Market Outlook

- Market Size of United States (US) Cold Chain Market, 2025

- Forecast of United States (US) Cold Chain Market, 2032

- Historical Data and Forecast of United States (US) Cold Chain Revenues & Volume for the Period 2022-2032F

- United States (US) Cold Chain Market Trend Evolution

- United States (US) Cold Chain Market Drivers and Challenges

- United States (US) Cold Chain Price Trends

- United States (US) Cold Chain Porter's Five Forces

- United States (US) Cold Chain Industry Life Cycle

- Historical Data and Forecast of United States (US) Cold Chain Market Revenues & Volume By Temperature Type for the Period 2022-2032F

- Historical Data and Forecast of United States (US) Cold Chain Market Revenues & Volume By Frozen for the Period 2022-2032F

- Historical Data and Forecast of United States (US) Cold Chain Market Revenues & Volume By Chilled for the Period 2022-2032F

- Historical Data and Forecast of United States (US) Cold Chain Market Revenues & Volume By Type for the Period 2022-2032F

- Historical Data and Forecast of United States (US) Cold Chain Market Revenues & Volume By Refrigerated warehousing for the Period 2022-2032F

- Historical Data and Forecast of United States (US) Cold Chain Market Revenues & Volume By Refrigerated transport for the Period 2022-2032F

- Historical Data and Forecast of United States (US) Cold Chain Market Revenues & Volume By Application for the Period 2022-2032F

- Historical Data and Forecast of United States (US) Cold Chain Market Revenues & Volume By Dairy & frozen desserts for the Period 2022-2032F

- Historical Data and Forecast of United States (US) Cold Chain Market Revenues & Volume By Fish, meat, and seafood products for the Period 2022-2032F

- Historical Data and Forecast of United States (US) Cold Chain Market Revenues & Volume By Bakery & confectionery products for the Period 2022-2032F

- Historical Data and Forecast of United States (US) Cold Chain Market Revenues & Volume By Fruits & vegetables for the Period 2022-2032F

- Historical Data and Forecast of United States (US) Cold Chain Market Revenues & Volume By Others for the Period 2022-2032F

- United States (US) Cold Chain Import Export Trade Statistics

- Market Opportunity Assessment By Temperature Type

- Market Opportunity Assessment By Type

- Market Opportunity Assessment By Application

- United States (US) Cold Chain Top Companies Market Share

- United States (US) Cold Chain Competitive Benchmarking By Technical and Operational Parameters

- United States (US) Cold Chain Company Profiles

- United States (US) Cold Chain Key Strategic Recommendations

Frequently Asked Questions About the Market Study (FAQs):

The growth is primarily driven by the increasing demand for perishable goods in the food and pharmaceutical sectors, as well as the adoption of advanced technologies for enhanced efficiency and compliance.

The United States Cold Chain Market was estimated at USD 231 Million in 2025 and is projected to reach USD 314 Million by 2032, growing at a CAGR of 4.5% from 2026 to 2032.

Key trends include increased automation, the adoption of IoT technology for real-time monitoring, and a growing emphasis on sustainability within the industry.

Investment opportunities lie in expanding cold storage facilities, incorporating advanced monitoring technology, and enhancing cold chain management solutions to meet rising consumer demands.

Government regulations ensure that temperature-sensitive products maintain their integrity during storage and transport, promoting best practices and providing funding for infrastructure improvements.

Companies grapple with maintaining product temperature integrity, navigating complex regulatory compliance, and managing operational costs while striving for efficiency.

6Wresearch actively monitors the United States (US) Cold Chain Market and publishes its comprehensive annual report, highlighting emerging trends, growth drivers, revenue analysis, and forecast outlook. Our insights help businesses to make data-backed strategic decisions with ongoing market dynamics. Our analysts track relevent industries related to the United States (US) Cold Chain Market, allowing our clients with actionable intelligence and reliable forecasts tailored to emerging regional needs.

Yes, we provide customisation as per your requirements. To learn more, feel free to contact us on sales@6wresearch.com

1 Executive Summary |

2 Introduction |

2.1 Key Highlights of the Report |

2.2 Report Description |

2.3 Market Scope & Segmentation |

2.4 Research Methodology |

2.5 Assumptions |

3 United States (US) Cold Chain Market Overview |

3.1 United States (US) Country Macro Economic Indicators |

3.2 United States (US) Cold Chain Market Revenues & Volume, 2022 & 2032F |

3.3 United States (US) Cold Chain Market - Industry Life Cycle |

3.4 United States (US) Cold Chain Market - Porter's Five Forces |

3.5 United States (US) Cold Chain Market Revenues & Volume Share, By Temperature Type, 2022 & 2032F |

3.6 United States (US) Cold Chain Market Revenues & Volume Share, By Type, 2022 & 2032F |

3.7 United States (US) Cold Chain Market Revenues & Volume Share, By Application, 2022 & 2032F |

4 United States (US) Cold Chain Market Dynamics |

4.1 Impact Analysis |

4.2 Market Drivers |

4.2.1 Increasing demand for perishable goods transportation |

4.2.2 Growing focus on food safety regulations |

4.2.3 Technological advancements in cold chain logistics infrastructure |

4.3 Market Restraints |

4.3.1 High initial investment costs |

4.3.2 Lack of skilled workforce in cold chain management |

4.3.3 Stringent regulatory requirements for temperature-controlled transportation |

5 United States (US) Cold Chain Market Trends |

6 United States (US) Cold Chain Market, By Types |

6.1 United States (US) Cold Chain Market, By Temperature Type |

6.1.1 Overview and Analysis |

6.1.2 United States (US) Cold Chain Market Revenues & Volume, By Temperature Type, 2022-2032F |

6.1.3 United States (US) Cold Chain Market Revenues & Volume, By Frozen, 2022-2032F |

6.1.4 United States (US) Cold Chain Market Revenues & Volume, By Chilled, 2022-2032F |

6.2 United States (US) Cold Chain Market, By Type |

6.2.1 Overview and Analysis |

6.2.2 United States (US) Cold Chain Market Revenues & Volume, By Refrigerated warehousing, 2022-2032F |

6.2.3 United States (US) Cold Chain Market Revenues & Volume, By Refrigerated transport, 2022-2032F |

6.3 United States (US) Cold Chain Market, By Application |

6.3.1 Overview and Analysis |

6.3.2 United States (US) Cold Chain Market Revenues & Volume, By Dairy & frozen desserts, 2022-2032F |

6.3.3 United States (US) Cold Chain Market Revenues & Volume, By Fish, meat, and seafood products, 2022-2032F |

6.3.4 United States (US) Cold Chain Market Revenues & Volume, By Bakery & confectionery products, 2022-2032F |

6.3.5 United States (US) Cold Chain Market Revenues & Volume, By Fruits & vegetables, 2022-2032F |

6.3.6 United States (US) Cold Chain Market Revenues & Volume, By Others, 2022-2032F |

7 United States (US) Cold Chain Market Import-Export Trade Statistics |

7.1 United States (US) Cold Chain Market Export to Major Countries |

7.2 United States (US) Cold Chain Market Imports from Major Countries |

8 United States (US) Cold Chain Market Key Performance Indicators |

8.1 Average transit time for perishable goods |

8.2 Percentage of compliance with food safety regulations |

8.3 Utilization rate of cold chain logistics infrastructure |

8.4 Percentage of reduction in cold chain disruptions |

8.5 Energy efficiency of cold chain operations |

9 United States (US) Cold Chain Market - Opportunity Assessment |

9.1 United States (US) Cold Chain Market Opportunity Assessment, By Temperature Type, 2022 & 2032F |

9.2 United States (US) Cold Chain Market Opportunity Assessment, By Type, 2022 & 2032F |

9.3 United States (US) Cold Chain Market Opportunity Assessment, By Application, 2022 & 2032F |

10 United States (US) Cold Chain Market - Competitive Landscape |

10.1 United States (US) Cold Chain Market Revenue Share, By Companies, 2025 |

10.2 United States (US) Cold Chain Market Competitive Benchmarking, By Operating and Technical Parameters |

11 Company Profiles |

12 Recommendations |

13 Disclaimer |

Global Go To Market Strategy - 2030

Export potential enables firms to identify high-growth global markets with greater confidence by combining advanced trade intelligence with a structured quantitative methodology. The framework analyzes emerging demand trends and country-level import patterns while integrating macroeconomic and trade datasets such as GDP and population forecasts, bilateral import–export flows, tariff structures, elasticity differentials between developed and developing economies, geographic distance, and import demand projections. Using weighted trade values from 2020–2024 as the base period to project country-to-country export potential for 2030, these inputs are operationalized through calculated drivers such as gravity model parameters, tariff impact factors, and projected GDP per-capita growth. Through an analysis of hidden potentials, demand hotspots, and market conditions that are most favorable to success, this method enables firms to focus on target countries, maximize returns, and global expansion with data, backed by accuracy.

By factoring in the projected importer demand gap that is currently unmet and could be potential opportunity, it identifies the potential for the Exporter (Country) among 190 countries, against the general trade analysis, which identifies the biggest importer or exporter.

To discover high-growth global markets and optimize your business strategy:

Click Here

Pricing

- Single User License$ 1,995

- Department License$ 2,400

- Site License$ 3,120

- Global License$ 3,795

Leadership Perspectives from Industry Events

Search

Thought Leadership and Analyst Meet

Our Clients

6WResearch In News

- India Export Attractiveness Tracker 2026

- India Air Conditioner Market Set for Strong Rebound in 2026 After Weather-Led Correction and GST-Driven Recovery: 6Wresearch

- ADAS in India: How Automatic Emergency Braking, Blind Spot Detection & Driver Monitoring are Transforming Road Safety

- Doha a strategic location for EV manufacturing hub: IPA Qatar

- Demand for luxury TVs surging in the GCC, says Samsung

- Empowering Growth: The Thriving Journey of Bangladesh’s Cable Industry

Latest Reports

- Greece Insulated Sandwich Panels Market (2026-2032)

- Qatar Access and Home Network Market (2026-2032)

- Nicaragua RPG Gaming Market (2026-2032)

- New Zealand RPG Gaming Market (2026-2032)

- Netherlands RPG Gaming Market (2026-2032)

- Nauru RPG Gaming Market (2026-2032)

- Namibia RPG Gaming Market (2026-2032)

- Mozambique RPG Gaming Market (2026-2032)

- Montenegro RPG Gaming Market (2026-2032)

- Mongolia RPG Gaming Market (2026-2032)

Industry Events and Analyst Meet

EV India Expo 2026

HIMTEX 2026

India Refining Summit 2026

India EV Show 2026

EV tech India Expo 2026

Whitepaper

- Middle East & Africa Commercial Security Market Click here to view more.

- Middle East & Africa Fire Safety Systems & Equipment Market Click here to view more.

- GCC Drone Market Click here to view more.

- Middle East Lighting Fixture Market Click here to view more.

- GCC Physical & Perimeter Security Market Click here to view more.