Mexico Antimony Market (2026-2032) Outlook | Companies, Growth, Share, Trends, Forecast, Value, Size, Industry, Revenue & Analysis

Market Forecast By Type (Metal Ingot, Antimony Trioxide, Antimony Pentoxide, Alloys, Other), By Application (Flame Retardant, Lead Acid Batteries, Alloy Strengthening Agent, Fiberglass Composites, Catalyst, Other) And Competitive Landscape

| Product Code: ETC087022 | Publication Date: Jun 2021 | Updated Date: Jun 2026 | Product Type: Report | |

| Publisher: 6Wresearch | Author: Ravi Bhandari | No. of Pages: 70 | No. of Figures: 35 | No. of Tables: 5 |

Mexico Antimony Market Size, Share & Growth Rate

The Mexico Antimony Market was estimated at USD 195 Million in 2025 and is projected to reach USD 225 Million by 2032, growing at a CAGR of 2.1% from 2026 to 2032. This growth trajectory is largely fueled by the robust demand for antimony in flame retardants, especially in textiles and plastics, along with increasing utilization in the automotive and electronics sectors. As regulatory frameworks evolve, emphasizing safety and environmental standards, the market is likely to adapt and thrive within these new constraints.

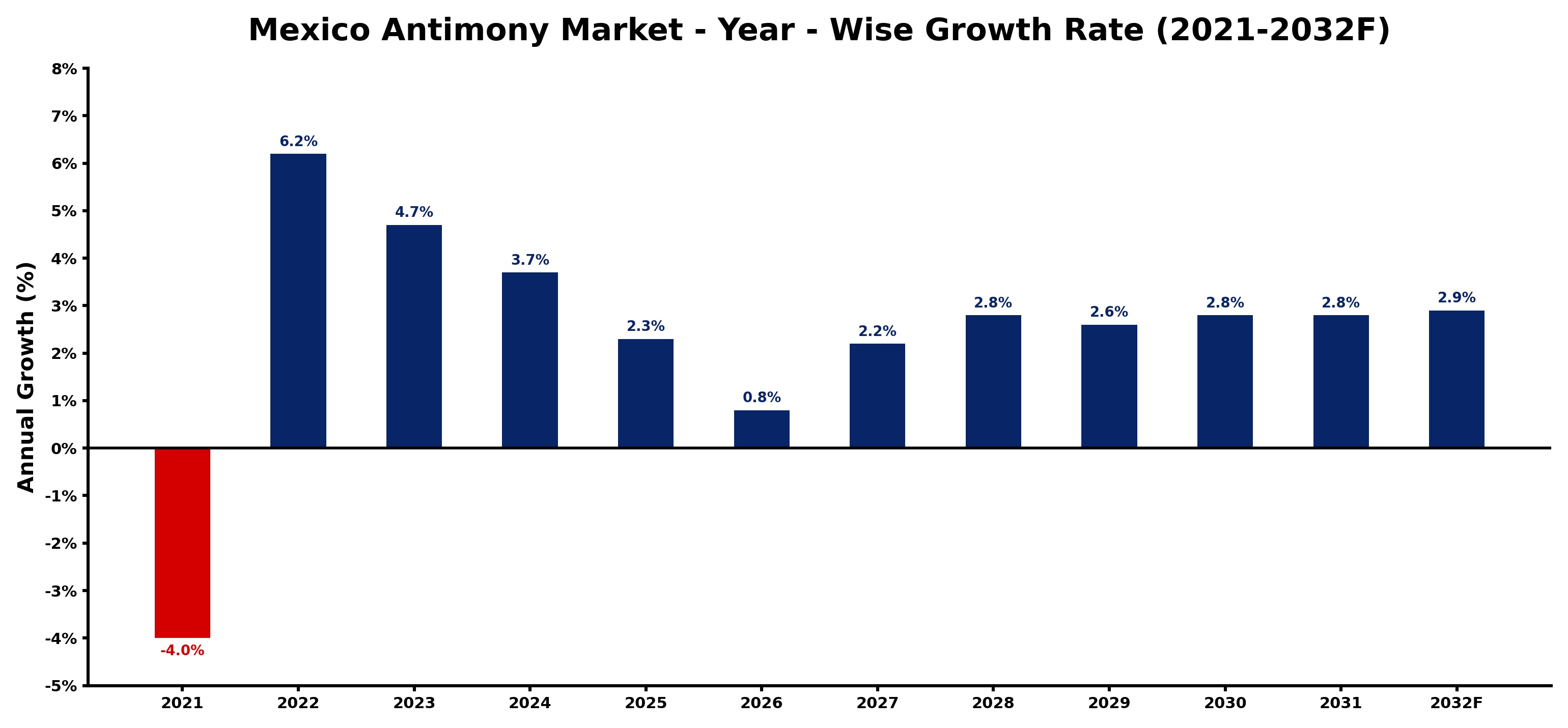

Mexico Antimony Market Growth Rate Analysis (2021-2032)

The antimony market in Mexico has seen an intriguing transition over recent years. After a decline of 4.0% in 2021, the market rebounded strongly with a 6.2% growth in 2022, fueled by heightened industrial demand, particularly from the electronics and automotive sectors, and increasing investments in mining and refining technologies. The upward trend continued with 4.7% growth in 2023 and is projected to stabilize at around 2.8% through 2032. Factors like infrastructure advancements and energy transition initiatives have contributed positively, although growth rates are expected to moderate due to potential shifts toward alternative materials and environmental regulations. Overall, Mexico’s strategic positioning in the global supply chain for antimony remains critical.

Mexico Antimony Market Year-wise Growth Rate and Key Drivers

This graph highlights how the Mexico Antimony Market has steadily grown over the past five years, supported by major growth factors.

The table below presents the year‑wise growth rates along with the key drivers influencing the market

| Year | Growth Rate | Major Drivers |

| 2021 | -4.0% | Government infrastructure modernization initiatives |

| 2022 | 6.2% | Expansion of commercial construction activities |

| 2023 | 4.7% | Expansion of commercial construction activities |

| 2024 | 3.7% | Rapid growth in telecom and data center sectors |

| 2025 | 2.3% | Expansion of manufacturing activities |

| 2026 | 0.8% | Expansion of transportation and logistics networks |

| 2027 | 2.2% | Rapid growth in telecom and data center sectors |

| 2028 | 2.8% | Rising electricity demand across industries |

| 2029 | 2.6% | Expansion of commercial construction activities |

| 2030 | 2.8% | Expansion of commercial construction activities |

| 2031 | 2.8% | Growing renewable energy integration projects |

| 2032 | 2.9% | Rapid growth in telecom and data center sectors |

Note - Market size estimations and growth projections presented in this report are based on 6Wresearch’s advanced forecasting approach, validated with industry datasets as of June 2026.

Mexico Antimony Market Synopsis

Mexico's antimony market is at a pivotal juncture, with increasing applications in various industries such as electronics and automotive driving demand. The country's strategic position as both a producer and consumer further cements its role in the global antimony landscape.

As the focus on sustainability intensifies, antimony’s multifunctionality, particularly in flame retardants and battery technology, positions it as a critical mineral in industrial applications. This trend reflects a growing awareness of safety standards and the need for innovation in material usage.

Mexico Antimony Market Key Takeaways

- The market is expected to grow steadily, driven by increased use in flame retardants and electronics.

- Regulatory pressures are shaping production and consumption practices, pushing for more sustainable methods.

- The automotive sector is emerging as a significant consumer of antimony, boosting its demand.

- Environmental concerns related to mining and processing are prompting a shift towards responsible sourcing.

- Research and development initiatives are opening pathways for alternative applications of antimony.

Evaluation of Restraints in Mexico Antimony Market

Despite the positive outlook, several constraints hinder the full potential of the Mexico antimony market. The fluctuation in demand from its diverse end-use industries can create volatility, complicating production strategies for manufacturers. Additionally, geopolitical factors, such as trade policies and international relations, contribute to market uncertainties that may affect export and import dynamics. Environmental concerns regarding mining practices are also growing, necessitating a commitment to sustainable practices to mitigate potential backlash and regulatory scrutiny.

Mexico Antimony Market Trends

Current trends indicate an upsurge in the demand for antimony compounds, particularly within the flame retardant sector, which is responding to stricter safety regulations. Additionally, the automotive industry’s shift towards more efficient battery technologies and lightweight materials continues to create a fertile ground for antimony applications. Moreover, the increasing focus on electronics manufacturing in Mexico further highlights the essential role of antimony in semiconductor production, ensuring sustained demand growth.

Mexico Antimony Market Opportunities

The Mexico antimony market presents numerous opportunities for growth and investment, particularly in the development of advanced flame retardant formulations that comply with stringent safety standards. With a strong electronics manufacturing base, opportunities abound in leveraging antimony's unique properties in semiconductor applications. Additionally, innovations in recycling and recovery technologies for antimony could enhance its sustainability profile, drawing in environmentally conscious investors and partners.

Government Initiatives in the Mexico Antimony Market

The Mexican government is actively involved in regulating the antimony market, implementing policies aimed at sustainable mining practices and public health safeguards. Through various regulatory frameworks, authorities are working to ensure that mining and processing operations adhere to environmental standards, thereby mitigating adverse impacts. Furthermore, there are initiatives promoting responsible sourcing and certification of antimony, which seek to address ethical mining practices and support local communities affected by extraction activities.

Future Insights of the Mexico Antimony Market

Looking ahead to 2026-2032, the Mexico antimony market is poised for steady growth, propelled by increasing industrial applications and a proactive regulatory environment. The demand for antimony in next-generation batteries and flame retardants is expected to gain momentum, reflecting ongoing shifts towards sustainability. As manufacturers adapt to new regulations and consumer preferences, innovation in applications and responsible sourcing will likely define the competitive landscape, ensuring that Mexico remains a key player in the global antimony supply chain.

Mexico Antimony Market Latest Developments (May 2025 - June 2026)

Recent developments in the Mexico antimony market indicate a strong push towards sustainability and responsible sourcing practices. Industry players are increasingly collaborating with government bodies to align with new regulatory frameworks aimed at reducing environmental impacts. Additionally, advancements in recycling technologies are being explored to enhance the efficiency of antimony usage in industrial applications, reflecting a growing commitment to sustainability across the sector.

Mexico Antimony Market - Key Attractiveness of the Report

- 10 Years of Market Numbers

- Historical Data Starting from 2022 to 2025

- Base Year: 2025

- Forecast Data until 2032

- Key Performance Indicators Impacting the Market

- Major Upcoming Developments and Projects

Key Highlights of the Report:

- Mexico Antimony Market Outlook

- Market Size of Mexico Antimony Market, 2025

- Forecast of Mexico Antimony Market, 2032

- Historical Data and Forecast of Mexico Antimony Revenues & Volume for the Period 2022-2032F

- Mexico Antimony Market Trend Evolution

- Mexico Antimony Market Drivers and Challenges

- Mexico Antimony Price Trends

- Mexico Antimony Porter's Five Forces

- Mexico Antimony Industry Life Cycle

- Historical Data and Forecast of Mexico Antimony Market Revenues & Volume By Type for the Period 2022-2032F

- Historical Data and Forecast of Mexico Antimony Market Revenues & Volume By Metal Ingot for the Period 2022-2032F

- Historical Data and Forecast of Mexico Antimony Market Revenues & Volume By Antimony Trioxide for the Period 2022-2032F

- Historical Data and Forecast of Mexico Antimony Market Revenues & Volume By Antimony Pentoxide for the Period 2022-2032F

- Historical Data and Forecast of Mexico Antimony Market Revenues & Volume By Alloys for the Period 2022-2032F

- Historical Data and Forecast of Mexico Antimony Market Revenues & Volume By Other for the Period 2022-2032F

- Historical Data and Forecast of Mexico Antimony Market Revenues & Volume By Application for the Period 2022-2032F

- Historical Data and Forecast of Mexico Antimony Market Revenues & Volume By Flame Retardant for the Period 2022-2032F

- Historical Data and Forecast of Mexico Antimony Market Revenues & Volume By Lead Acid Batteries for the Period 2022-2032F

- Historical Data and Forecast of Mexico Antimony Market Revenues & Volume By Alloy Strengthening Agent for the Period 2022-2032F

- Historical Data and Forecast of Mexico Antimony Market Revenues & Volume By Fiberglass Composites for the Period 2022-2032F

- Historical Data and Forecast of Mexico Antimony Market Revenues & Volume By Catalyst for the Period 2022-2032F

- Historical Data and Forecast of Mexico Antimony Market Revenues & Volume By Other for the Period 2022-2032F

- Mexico Antimony Import Export Trade Statistics

- Market Opportunity Assessment By Type

- Market Opportunity Assessment By Application

- Mexico Antimony Top Companies Market Share

- Mexico Antimony Competitive Benchmarking By Technical and Operational Parameters

- Mexico Antimony Company Profiles

- Mexico Antimony Key Strategic Recommendations

Mexico Antimony Market - Frequently Asked Questions

Antimony is primarily utilized in flame retardants, particularly in the plastics and textile industries, as well as in batteries and electronic components, particularly semiconductors.

The Mexico Antimony Market is a vital player in the global arena, with its estimated size of USD 195 Million in 2025 and a projection of USD 225 Million by 2032, underscoring its importance in both domestic consumption and export.

Major challenges include fluctuating demand driven by its diverse applications, environmental concerns related to mining practices, and geopolitical factors that can affect trade dynamics.

The automotive and electronics sectors are rapidly becoming significant consumers, with antimony playing a crucial role in the production of batteries and semiconductors.

Government policies are pivotal in regulating mining practices, ensuring environmental sustainability, and fostering responsible sourcing within the antimony market.

The Mexico Antimony Market is projected to grow at a CAGR of 2.1% from 2026 to 2032, reflecting a steady increase in demand across various industrial applications.

6Wresearch actively monitors the Mexico Antimony Market and publishes its comprehensive annual report, highlighting emerging trends, growth drivers, revenue analysis, and forecast outlook. Our insights help businesses to make data-backed strategic decisions with ongoing market dynamics. Our analysts track relevent industries related to the Mexico Antimony Market, allowing our clients with actionable intelligence and reliable forecasts tailored to emerging regional needs.

Yes, we provide customisation as per your requirements. To learn more, feel free to contact us on sales@6wresearch.com

1 Executive Summary |

2 Introduction |

2.1 Key Highlights of the Report |

2.2 Report Description |

2.3 Market Scope & Segmentation |

2.4 Research Methodology |

2.5 Assumptions |

3 Mexico Antimony Market Overview |

3.1 Mexico Country Macro Economic Indicators |

3.2 Mexico Antimony Market Revenues & Volume, 2022 & 2032F |

3.3 Mexico Antimony Market - Industry Life Cycle |

3.4 Mexico Antimony Market - Porter's Five Forces |

3.5 Mexico Antimony Market Revenues & Volume Share, By Type, 2022 & 2032F |

3.6 Mexico Antimony Market Revenues & Volume Share, By Form, 2022 & 2032F |

4 Mexico Antimony Market Dynamics |

4.1 Impact Analysis |

4.2 Market Drivers |

4.2.1 Growing demand from end-use industries like automotive, electronics, and construction |

4.2.2 Increasing investments in infrastructure projects in Mexico |

4.2.3 Rising focus on sustainable and environmentally friendly antimony mining practices |

4.3 Market Restraints |

4.3.1 Volatility in antimony prices due to global economic conditions |

4.3.2 Regulatory challenges related to environmental standards and mining regulations in Mexico |

5 Mexico Antimony Market Trends |

6 Mexico Antimony Market, By Types |

6.1 Mexico Antimony Market, By Type |

6.1.1 Overview and Analysis |

6.1.2 Mexico Antimony Market Revenues & Volume, By Type, 2022-2032F |

6.1.3 Mexico Antimony Market Revenues & Volume, By Metal Ingot, 2022-2032F |

6.1.4 Mexico Antimony Market Revenues & Volume, By Antimony Trioxide, 2022-2032F |

6.1.5 Mexico Antimony Market Revenues & Volume, By Antimony Pentoxide, 2022-2032F |

6.1.6 Mexico Antimony Market Revenues & Volume, By Alloys, 2022-2032F |

6.1.7 Mexico Antimony Market Revenues & Volume, By Other, 2022-2032F |

6.2 Mexico Antimony Market, By Application |

6.2.1 Overview and Analysis |

6.2.2 Mexico Antimony Market Revenues & Volume, By Flame Retardant, 2022-2032F |

6.2.3 Mexico Antimony Market Revenues & Volume, By Lead Acid Batteries, 2022-2032F |

6.2.4 Mexico Antimony Market Revenues & Volume, By Alloy Strengthening Agent, 2022-2032F |

6.2.5 Mexico Antimony Market Revenues & Volume, By Fiberglass Composites, 2022-2032F |

6.2.6 Mexico Antimony Market Revenues & Volume, By Catalyst, 2022-2032F |

6.2.7 Mexico Antimony Market Revenues & Volume, By Other, 2022-2032F |

7 Mexico Antimony Market Import-Export Trade Statistics |

7.1 Mexico Antimony Market Export to Major Countries |

7.2 Mexico Antimony Market Imports from Major Countries |

8 Mexico Antimony Market Key Performance Indicators |

8.1 Exploration and development activities in Mexican antimony mines |

8.2 Adoption rates of environmentally sustainable mining practices |

8.3 Market penetration of antimony in new applications and industries |

9 Mexico Antimony Market - Opportunity Assessment |

9.1 Mexico Antimony Market Opportunity Assessment, By Type, 2022 & 2032F |

9.2 Mexico Antimony Market Opportunity Assessment, By Application, 2022 & 2032F |

10 Mexico Antimony Market - Competitive Landscape |

10.1 Mexico Antimony Market Revenue Share, By Companies, 2025 |

10.2 Mexico Antimony Market Competitive Benchmarking, By Operating and Technical Parameters |

11 Company Profiles |

12 Recommendations |

13 Disclaimer |

Global Go To Market Strategy - 2030

Export potential enables firms to identify high-growth global markets with greater confidence by combining advanced trade intelligence with a structured quantitative methodology. The framework analyzes emerging demand trends and country-level import patterns while integrating macroeconomic and trade datasets such as GDP and population forecasts, bilateral import–export flows, tariff structures, elasticity differentials between developed and developing economies, geographic distance, and import demand projections. Using weighted trade values from 2020–2024 as the base period to project country-to-country export potential for 2030, these inputs are operationalized through calculated drivers such as gravity model parameters, tariff impact factors, and projected GDP per-capita growth. Through an analysis of hidden potentials, demand hotspots, and market conditions that are most favorable to success, this method enables firms to focus on target countries, maximize returns, and global expansion with data, backed by accuracy.

By factoring in the projected importer demand gap that is currently unmet and could be potential opportunity, it identifies the potential for the Exporter (Country) among 190 countries, against the general trade analysis, which identifies the biggest importer or exporter.

To discover high-growth global markets and optimize your business strategy:

Click Here

Pricing

- Single User License$ 1,995

- Department License$ 2,400

- Site License$ 3,120

- Global License$ 3,795

Leadership Perspectives from Industry Events

Search

Thought Leadership and Analyst Meet

Our Clients

6WResearch In News

- India Air Conditioner Market Set for Strong Rebound in 2026 After Weather-Led Correction and GST-Driven Recovery: 6Wresearch

- ADAS in India: How Automatic Emergency Braking, Blind Spot Detection & Driver Monitoring are Transforming Road Safety

- Doha a strategic location for EV manufacturing hub: IPA Qatar

- Demand for luxury TVs surging in the GCC, says Samsung

- Empowering Growth: The Thriving Journey of Bangladesh’s Cable Industry

- Demand for luxury TVs surging in the GCC, says Samsung

Latest Reports

- Poland Fire Protection Systems Market (2026-2032)

- Cape Verde Portable Hand-Thrown Extinguisher Market (2026-2032)

- Canada Portable Hand-Thrown Extinguisher Market (2026-2032)

- Cameroon Portable Hand-Thrown Extinguisher Market (2026-2032)

- Burundi Portable Hand-Thrown Extinguisher Market (2026-2032)

- Burkina Faso Portable Hand-Thrown Extinguisher Market (2026-2032)

- Bulgaria Portable Hand-Thrown Extinguisher Market (2026-2032)

- Brunei Portable Hand-Thrown Extinguisher Market (2026-2032)

- Botswana Portable Hand-Thrown Extinguisher Market (2026-2032)

- Bosnia and Herzegovina Portable Hand-Thrown Extinguisher Market (2026-2032)

Industry Events and Analyst Meet

HIMTEX 2026

India Refining Summit 2026

India EV Show 2026

EV tech India Expo 2026

Auto Tech Asia 2026

Whitepaper

- Middle East & Africa Commercial Security Market Click here to view more.

- Middle East & Africa Fire Safety Systems & Equipment Market Click here to view more.

- GCC Drone Market Click here to view more.

- Middle East Lighting Fixture Market Click here to view more.

- GCC Physical & Perimeter Security Market Click here to view more.