Thailand Oil & Gas Upstream Market (2026-2032) | Industry, Outlook, Share, Forecast, Size & Revenue, Companies, Segmentation, Analysis, Trends, Competitive Landscape, Growth, Value

Market Forecast By Type (Oil, Natural Gas) And Competitive Landscape

| Product Code: ETC9681014 | Publication Date: Sep 2024 | Updated Date: May 2026 | Product Type: Market Research Report | |

| Publisher: 6Wresearch | Author: Sumit Sagar | No. of Pages: 75 | No. of Figures: 35 | No. of Tables: 20 |

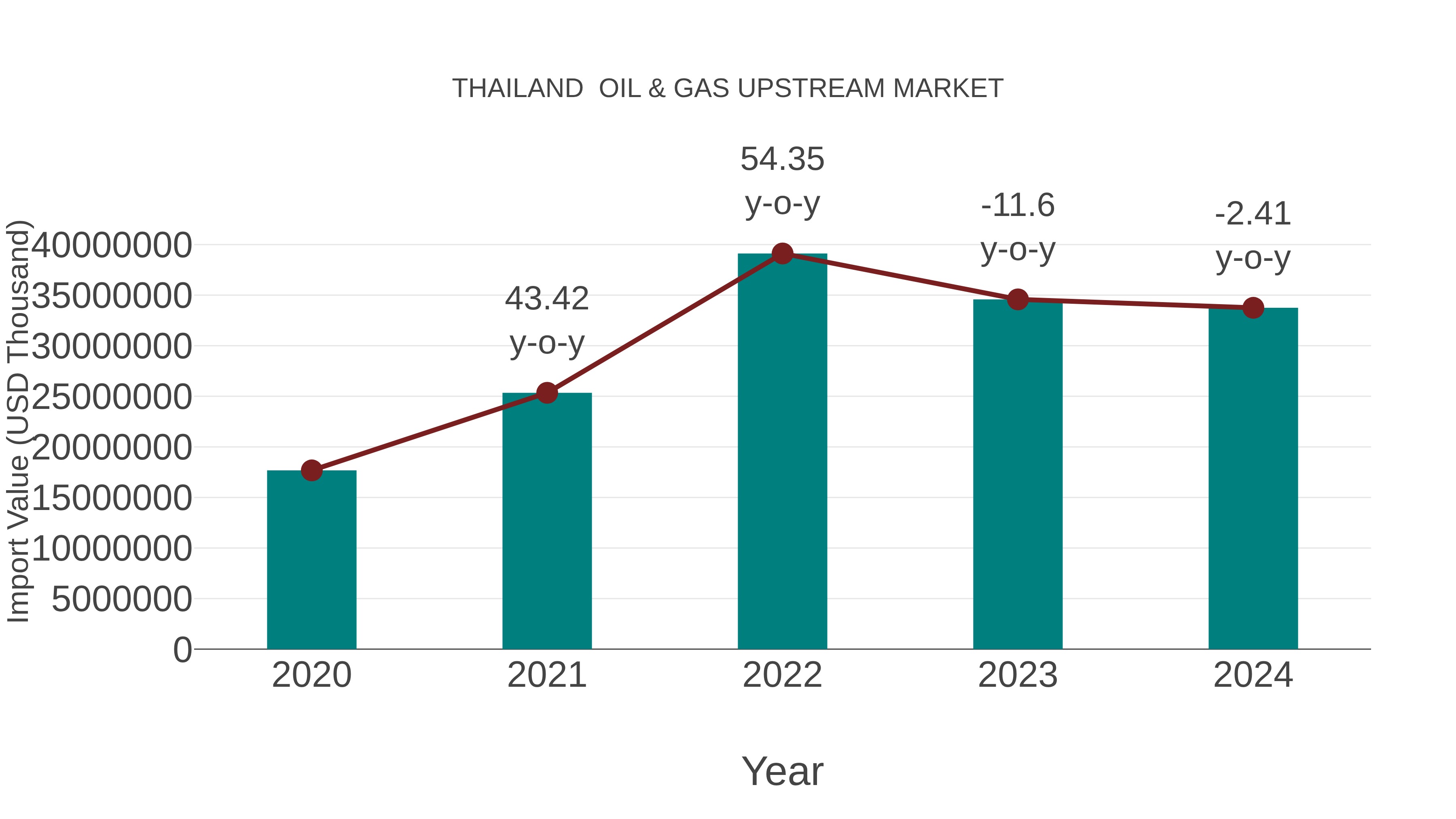

Thailand Oil & Gas Upstream Market: Import Trend Analysis

Thailand import trend for the oil & gas upstream market experienced a -2.41% decline from 2023 to 2024, with a compound annual growth rate (CAGR) of 17.55% from 2020 to 2024. This negative growth in 2024 could be attributed to a temporary decrease in demand due to global market conditions affecting import momentum.

Thailand Oil & Gas Upstream Market Growth Rate

According to 6Wresearch internal database and industry insights, the Thailand Oil & Gas Upstream Market is anticipated to grow at a compound annual growth rate (CAGR) of 5.8% during the forecast period (2026–2032).

Topics Covered in the Thailand Oil & Gas Upstream Market Report

Thailand Oil & Gas Upstream Market report thoroughly covers the market by type. The market report provides an unbiased and detailed analysis of ongoing market trends, opportunities/high growth areas, and market drivers, which would help stakeholders devise and align their market strategies according to the current and future market dynamics.

Thailand Oil & Gas Upstream Market Highlights

| Report Name |

Thailand Oil & Gas Upstream Market |

| Forecast period | 2026-2032 |

| CAGR | 5.8% |

| Market Size |

Energy & Natural Resources Sector |

Thailand Oil & Gas Upstream Market Synopsis

The Thailand Oil & Gas Upstream Industry has been securing a steady growth on account of the country's heavy dependency on domestic hydrocarbon production, rising energy security priorities, and active exploration in the Gulf of Thailand. Thailand has long depended on its offshore gas fields to power its electricity generation and industrial sectors, and this dependence continues to drive upstream investment. The market is also benefiting from improved drilling technologies and growing collaboration between state-owned entities and international oil companies to maximise recovery from both existing and newly discovered reserves.

Evaluation of Growth Drivers in Thailand Oil & Gas Upstream Market

Below mentioned are some growth drivers and their impact on market dynamics:

| Drivers | Primary Segment Affected | Why It Matters (Evidence) |

| Strong Domestic Energy Demand | Oil, Natural Gas | Thailand's growing industrial and power generation needs keep upstream production a national priority. |

| Government Licensing and Concession Awards | Oil, Natural Gas | New exploration blocks and renewed concessions attract fresh upstream investment into the country. |

| Advancements in Drilling Technology | Oil, Natural Gas | Improved exploration and recovery techniques help extract more from both new and ageing fields. |

| Energy Security Priorities | Natural Gas | Reducing dependence on energy imports pushes the government to support domestic gas production. |

| Rising Global Oil Prices | Oil | Higher oil prices improve the commercial viability of exploration and production projects in Thailand. |

The Thailand Oil & Gas Upstream Market is deemed to grow at a steady pace of 5.8% CAGR over the forecast period (2026–2032) owing to some important factors, such as domestic energy demand, government concession activity, and continued investment in offshore production. The transition of major gas field concessions and the entry of new operators are further supporting market activity. Aside from that, country's push for energy self-sufficiency and its position as a regional energy hub are contributing to sustained upstream exploration, and production activity.

Evaluation of Restraints in Thailand Oil & Gas Upstream Market

Below mentioned are some major restraints and their influence on market dynamics:

| Restraints | Primary Segment Affected | What This Means (Evidence) |

| Declining Output from Mature Fields | Oil, Natural Gas | Ageing offshore fields are producing less over time, requiring costly enhanced recovery efforts. |

| High Exploration and Production Costs | Oil, Natural Gas | Offshore drilling and deepwater operations involve significant capital expenditure and financial risk. |

| Regulatory and Concession Uncertainty | Oil, Natural Gas | Delays in concession renewals and policy changes can slow investment decisions and project timelines. |

| Environmental and Community Concerns | Oil, Natural Gas | There is a growing scrutiny over offshore drilling's environmental impact which adds compliance costs. |

| Global Energy Transition Pressure | Oil | Increasing focus on renewable energy alternatives reduces long-term investor appetite for oil upstream projects |

Thailand Oil & Gas Upstream Market Challenges

Despite steady growth prospects, the Thailand Oil & Gas Upstream Market faces a number of real challenges. Declining production from mature fields in the Gulf of Thailand remains a key problem, as operators need to invest heavily in improved recovery just to maintain existing output levels. Besides that, rising pressure to transition toward cleaner energy sources means upstream oil and gas projects face increasing scrutiny from both regulators and the public. Addressing these challenges will require clear government policy and continued investment in modern production technologies.

Thailand Oil & Gas Upstream Market Trends

Listed below are some of the major trends responsible for Thailand Oil & Gas Upstream Market Growth:

- Concessions Transitioning and New Entrants: The passing of the significant concession areas into the hands of newly granted licensees introduces new dynamics to the Thailand upstream industry through increased investments and technologies.

- Increasing Preference for Natural Gas over Oil: The Thailand upstream industry is increasingly shifting towards the extraction of natural gas due to its relatively lower pollution and use in electricity production in Thailand.

- Digital Oilfields: The adoption of digital technology in upstream activities such as automation, remote monitoring, and data analysis is increasing, assisting the operator to cut down costs and improve safety and production from offshore oilfields.

Investment Opportunities in Thailand Oil & Gas Upstream Industry

The following is an outline of the main investment opportunities in Thailand Oil & Gas Upstream Industry:

- Exploration of Undeveloped Offshore Blocks: The Gulf of Thailand and Andaman Sea contain several undeveloped offshore blocks. New rounds of licensing provide ample opportunities to local and foreign firms.

- Development of Natural Gas Fields: Thailand is very much dependent on gas-based electricity production. Therefore, there are stable opportunities to generate income by developing natural gas fields.

- Enhanced Oil Recovery Projects: Mature oil fields still hold significant recoverable reserves. Investment in EOR technologies and services presents a commercially attractive opportunity to increase production rate without the risk of greenfield exploration.

Top 5 Leading Players in Thailand Oil & Gas Upstream Market

Stated below are some of the leading companies holding majority of Thailand Oil & Gas Upstream Market Shares:

1. PTT Exploration and Production Public Company Limited (PTTEP)

| Company Name | PTT Exploration and Production Public Company Limited (PTTEP) |

|---|---|

| Established Year | 1985 |

| Headquarters | Bangkok, Thailand |

| Official Website | Click Here |

PTTEP is Thailand's national upstream oil and gas company and the dominant force in the country's upstream sector. As a subsidiary of PTT Group, it holds exploration and production rights across multiple blocks in the Gulf of Thailand and internationally.

2. Chevron Thailand Exploration and Production

| Company Name | Chevron Thailand Exploration and Production |

|---|---|

| Established Year | 1962 (Thailand operations) |

| Headquarters | Bangkok, Thailand (Global HQ: San Ramon, USA) |

| Official Website | Click Here |

Chevron has been one of the longest-standing and most significant upstream operators in Thailand, historically managing some of the country's largest offshore gas fields.

3. TotalEnergies EP Thailand

| Company Name | TotalEnergies EP Thailand |

|---|---|

| Established Year | 1990s (Thailand operations) |

| Headquarters | Bangkok, Thailand (Global HQ: Paris, France) |

| Official Website | Click Here |

TotalEnergies is an active upstream operator in Thailand, holding working interests in several offshore blocks in the Gulf of Thailand. The company brings strong deepwater and offshore technical expertise and is committed to responsible energy development aligned with Thailand's production sharing framework and environmental standards.

4. Mubadala Petroleum (Thailand)

| Company Name | Mubadala Petroleum (Thailand) |

|---|---|

| Established Year | 2012 (Thailand entry) |

| Headquarters | Abu Dhabi, UAE (Thailand Operations: Bangkok) |

| Official Website | - |

Mubadala Petroleum is a growing upstream investor in Thailand, holding stakes in several offshore exploration and production blocks. The company has steadily increased its footprint in Southeast Asia, including Thailand, bringing state-backed financial strength and a long-term investment outlook to its upstream portfolio.

5. Tap Oil (Thailand)

| Company Name | Tap Oil (Thailand) |

|---|---|

| Established Year | 1994 |

| Headquarters | Perth, Australia (Thailand Operations: Bangkok) |

| Official Website | - |

Tap Oil is an independent upstream operator with exploration and production interests in Thailand's offshore sector. It represents the category of smaller independent companies that play an important role in the Thai upstream market by developing niche blocks and contributing to the country's overall production diversity.

Government Initiatives Being Implemented in the Thailand Oil & Gas Upstream Market

According to Thai government data, the authority has a significant influence on the upstream oil and gas market through regulation, policies, and licences. The Ministry of Energy is responsible for the allocation of petroleum licences and production-sharing agreements. There is a systematic approach to the issuance of licences for upstream activities. The Department of Mineral Fuels undertakes regular licence rounds to facilitate investments in underused blocks. Thailand’s National Energy Policy also places a premium on the domestic production of gas as one of the pillars of energy security.

Future Insights of the Thailand Oil & Gas Upstream Market

The Thailand Oil & Gas Upstream Market will see consistent growth owing to Thailand’s continued reliance on domestic energy production. Natural gas will continue to be the dominant upstream focus, given its critical role in power generation and industrial use. New concession awards, adoption of advanced drilling technologies, and growing joint venture activity between state and international operators will support production volumes.

Market Segmentation Analysis

The report offers a comprehensive study of the following market segments and their leading categories in Thailand Oil & Gas Upstream Market:

By Type – Natural Gas Dominates the Market

According to Mansi, Senior Research Analyst, 6Wresearch, Natural gas dominates Thailand's upstream sector, primarily because the country's power generation infrastructure is heavily dependent on domestically produced gas. Thailand's major offshore fields in the Gulf of Thailand have historically been gas-producing assets, and gas continues to attract the highest share of upstream investment and production activity.

Key Attractiveness of the Report:

- 10 Years of Market Numbers

- Historical Data Starting from 2022 to 2025

- Base Year: 2025

- Forecast Data until 2032

- Key Performance Indicators Impacting the Market

- Major Upcoming Developments and Projects

Key Highlights of the Report:

- Thailand Oil & Gas Upstream Market Outlook

- Market Size of Thailand Oil & Gas Upstream Market, 2025

- Forecast of Thailand Oil & Gas Upstream Market, 2032

- Historical Data and Forecast of Thailand Oil & Gas Upstream Revenues & Volume for the Period 2022–2032

- Thailand Oil & Gas Upstream Market Trend Evolution

- Thailand Oil & Gas Upstream Market Drivers and Challenges

- Thailand Oil & Gas Upstream Price Trends

- Thailand Oil & Gas Upstream Porter's Five Forces

- Thailand Oil & Gas Upstream Industry Life Cycle

- Historical Data and Forecast of Thailand Oil & Gas Upstream Market Revenues & Volume By Type for the Period 2022–2032

- Historical Data and Forecast of Thailand Oil & Gas Upstream Market Revenues & Volume By Oil for the Period 2022–2032

- Historical Data and Forecast of Thailand Oil & Gas Upstream Market Revenues & Volume By Natural Gas for the Period 2022–2032

- Thailand Oil & Gas Upstream Import Export Trade Statistics

- Market Opportunity Assessment By Type

- Thailand Oil & Gas Upstream Top Companies Market Share

- Thailand Oil & Gas Upstream Competitive Benchmarking By Technical and Operational Parameters

- Thailand Oil & Gas Upstream Company Profiles

- Thailand Oil & Gas Upstream Key Strategic Recommendations

Market Covered

The report offers an extensive study of the following market segments:

By Type

- Oil

- Natural Gas

Thailand Oil & Gas Upstream Market (2026-2032): FAQs

Thailand Oil & Gas Upstream Market is anticipated to grow at the compound annual growth rate (CAGR) of 5.8% during the forecast period (2026–2032).

Thailand Oil & Gas Upstream Market is evolving with new concession transitions and increasing use of digital oilfield management systems.

The Ministry of Energy's petroleum licensing rounds and Thailand's National Energy Plan are collectively strengthening the upstream market.

Thailand Oil & Gas Upstream Market offers strong growth opportunities through underdeveloped offshore block exploration, and joint ventures with PTTEP.

6Wresearch actively monitors the Thailand Oil & Gas Upstream Market and publishes its comprehensive annual report, highlighting emerging trends, growth drivers, revenue analysis, and forecast outlook. Our insights help businesses to make data-backed strategic decisions with ongoing market dynamics. Our analysts track relevent industries related to the Thailand Oil & Gas Upstream Market, allowing our clients with actionable intelligence and reliable forecasts tailored to emerging regional needs.

Yes, we provide customisation as per your requirements. To learn more, feel free to contact us on sales@6wresearch.com

| 1 Executive Summary |

| 2 Introduction |

| 2.1 Key Highlights of the Report |

| 2.2 Report Description |

| 2.3 Market Scope & Segmentation |

| 2.4 Research Methodology |

| 2.5 Assumptions |

| 3 Thailand Oil & Gas Upstream Market Overview |

| 3.1 Thailand Country Macro Economic Indicators |

| 3.2 Thailand Oil & Gas Upstream Market Revenues & Volume, 2022 & 2032F |

| 3.3 Thailand Oil & Gas Upstream Market - Industry Life Cycle |

| 3.4 Thailand Oil & Gas Upstream Market - Porter's Five Forces |

| 3.5 Thailand Oil & Gas Upstream Market Revenues & Volume Share, By Type, 2022 & 2032F |

| 4 Thailand Oil & Gas Upstream Market Dynamics |

| 4.1 Impact Analysis |

| 4.2 Market Drivers |

| 4.2.1 Growing energy demand in Thailand |

| 4.2.2 Government initiatives to attract investment in the oil gas sector |

| 4.2.3 Technological advancements in exploration and production techniques |

| 4.3 Market Restraints |

| 4.3.1 Volatility in global oil prices |

| 4.3.2 Environmental concerns and regulations |

| 4.3.3 Competition from renewable energy sources |

| 5 Thailand Oil & Gas Upstream Market Trends |

| 6 Thailand Oil & Gas Upstream Market, By Types |

| 6.1 Thailand Oil & Gas Upstream Market, By Type |

| 6.1.1 Overview and Analysis |

| 6.1.2 Thailand Oil & Gas Upstream Market Revenues & Volume, By Type, 2022-2032F |

| 6.1.3 Thailand Oil & Gas Upstream Market Revenues & Volume, By Oil, 2022-2032F |

| 6.1.4 Thailand Oil & Gas Upstream Market Revenues & Volume, By Natural Gas, 2022-2032F |

| 7 Thailand Oil & Gas Upstream Market Import-Export Trade Statistics |

| 7.1 Thailand Oil & Gas Upstream Market Export to Major Countries |

| 7.2 Thailand Oil & Gas Upstream Market Imports from Major Countries |

| 8 Thailand Oil & Gas Upstream Market Key Performance Indicators |

| 8.1 Exploration success rate |

| 8.2 Average daily production rate |

| 8.3 Operating efficiency of oil rigs |

| 8.4 Cost per barrel of oil produced |

| 8.5 Number of new exploration licenses obtained |

| 9 Thailand Oil & Gas Upstream Market - Opportunity Assessment |

| 9.1 Thailand Oil & Gas Upstream Market Opportunity Assessment, By Type, 2022 & 2032F |

| 10 Thailand Oil & Gas Upstream Market - Competitive Landscape |

| 10.1 Thailand Oil & Gas Upstream Market Revenue Share, By Companies, 2025 |

| 10.2 Thailand Oil & Gas Upstream Market Competitive Benchmarking, By Operating and Technical Parameters |

| 11 Company Profiles |

| 12 Recommendations |

| 13 Disclaimer |

Global Go To Market Strategy - 2030

Export potential enables firms to identify high-growth global markets with greater confidence by combining advanced trade intelligence with a structured quantitative methodology. The framework analyzes emerging demand trends and country-level import patterns while integrating macroeconomic and trade datasets such as GDP and population forecasts, bilateral import–export flows, tariff structures, elasticity differentials between developed and developing economies, geographic distance, and import demand projections. Using weighted trade values from 2020–2024 as the base period to project country-to-country export potential for 2030, these inputs are operationalized through calculated drivers such as gravity model parameters, tariff impact factors, and projected GDP per-capita growth. Through an analysis of hidden potentials, demand hotspots, and market conditions that are most favorable to success, this method enables firms to focus on target countries, maximize returns, and global expansion with data, backed by accuracy.

By factoring in the projected importer demand gap that is currently unmet and could be potential opportunity, it identifies the potential for the Exporter (Country) among 190 countries, against the general trade analysis, which identifies the biggest importer or exporter.

To discover high-growth global markets and optimize your business strategy:

Click Here

Pricing

- Single User License$ 1,995

- Department License$ 2,400

- Site License$ 3,120

- Global License$ 3,795

Leadership Perspectives from Industry Events

Search

Thought Leadership and Analyst Meet

Our Clients

6WResearch In News

- India Export Attractiveness Tracker 2026

- India Air Conditioner Market Set for Strong Rebound in 2026 After Weather-Led Correction and GST-Driven Recovery: 6Wresearch

- ADAS in India: How Automatic Emergency Braking, Blind Spot Detection & Driver Monitoring are Transforming Road Safety

- Doha a strategic location for EV manufacturing hub: IPA Qatar

- Demand for luxury TVs surging in the GCC, says Samsung

- Empowering Growth: The Thriving Journey of Bangladesh’s Cable Industry

Latest Reports

- Nicaragua RPG Gaming Market (2026-2032)

- New Zealand RPG Gaming Market (2026-2032)

- Netherlands RPG Gaming Market (2026-2032)

- Nauru RPG Gaming Market (2026-2032)

- Namibia RPG Gaming Market (2026-2032)

- Mozambique RPG Gaming Market (2026-2032)

- Montenegro RPG Gaming Market (2026-2032)

- Mongolia RPG Gaming Market (2026-2032)

- Monaco RPG Gaming Market (2026-2032)

- Micronesia RPG Gaming Market (2026-2032)

Industry Events and Analyst Meet

EV India Expo 2026

HIMTEX 2026

India Refining Summit 2026

India EV Show 2026

EV tech India Expo 2026

Whitepaper

- Middle East & Africa Commercial Security Market Click here to view more.

- Middle East & Africa Fire Safety Systems & Equipment Market Click here to view more.

- GCC Drone Market Click here to view more.

- Middle East Lighting Fixture Market Click here to view more.

- GCC Physical & Perimeter Security Market Click here to view more.