United States (US) Flour Market (2026-2032) | Size, Forecast, Industry, Share, Growth, Revenue, Analysis, Trends, Value & Outlook

Market Forecast By Raw Material (Wheat, Rice, Maize, Others), By Applications (Bread & Bakery Products, Noodles & Pasta, Animal Feed, Wafers, Crackers, & Biscuits, Non-Food Application, Others), By Technology (Dry Technology, Wet Technology) And Competitive Landscape

| Product Code: ETC039942 | Publication Date: Oct 2022 | Updated Date: Jun 2026 | Product Type: Report | |

| Publisher: 6Wresearch | Author: Ravi Bhandari | No. of Pages: 70 | No. of Figures: 35 | No. of Tables: 5 |

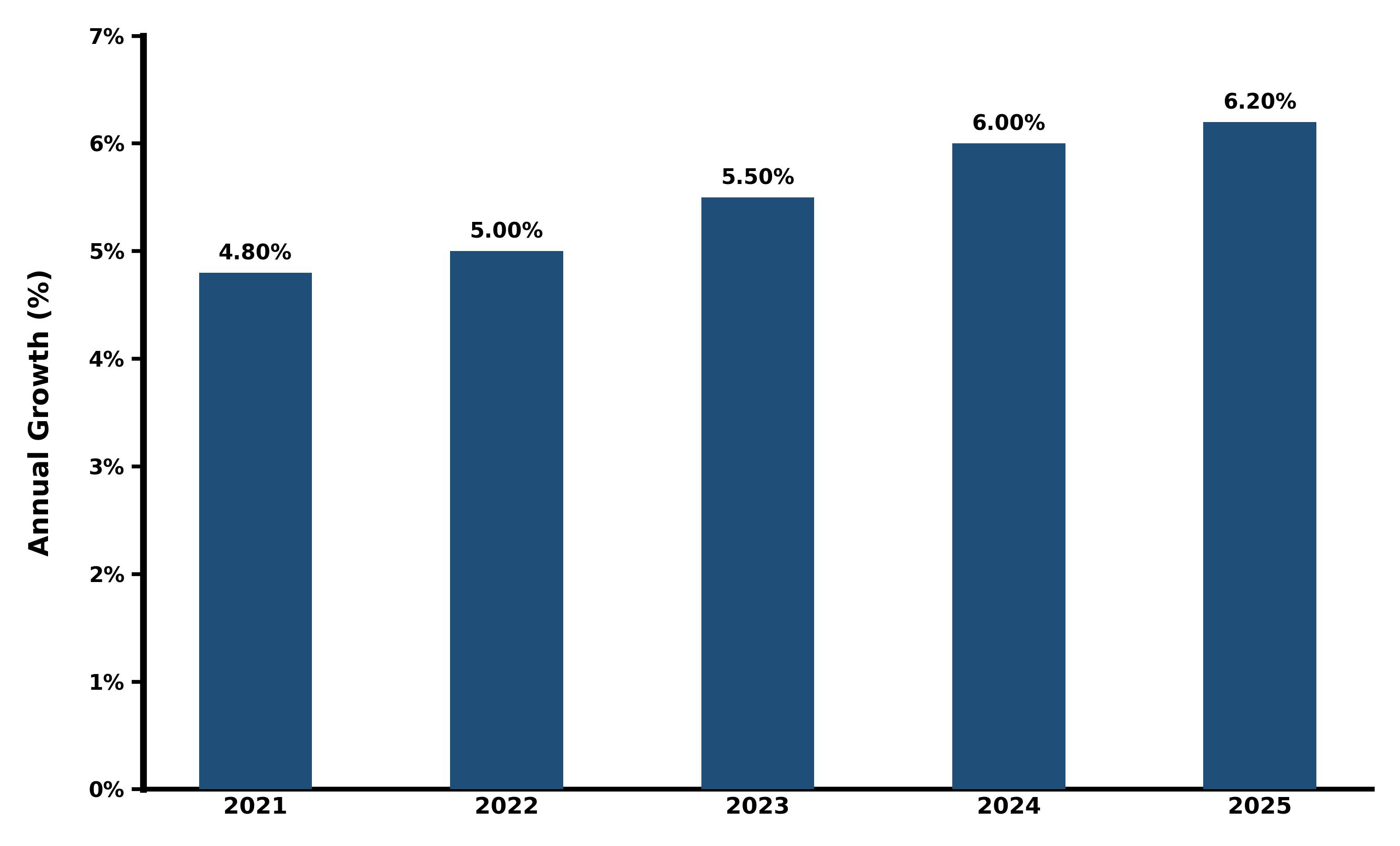

United States (US) Flour Market Growth Rate

According to 6Wresearch internal database and industry insights, the United States (US) Flour Market is growing at a compound annual growth rate (CAGR) of 6.5% during the forecast period (2026-2032).

United States (US) Flour Market Year-wise Growth Rate and Key Drivers

This graph highlights how the United States (US) Flour Market has steadily grown over the past five years, supported by major growth factors.

The table below presents the year‑wise growth rates along with the key drivers influencing the market

| Years | Est. Annual Growth in % | Growth Drivers |

| 2021 | 4.8% | Increased consumption of bakery products in both residential and non-residential sectors. |

| 2022 | 5% | Growing demand for gluten-free, organic, and healthy flour alternatives. |

| 2023 | 5.5% | Innovations in milling technologies and product diversification. |

| 2024 | 6% | Increasing demand for ready-to-eat bakery products and convenience foods. |

| 2025 | 6.2% | Expansion of flour exports and product innovation in premium flour varieties. |

Topics Covered in the United States (US) Flour Market Report

The United States (US) Flour Market report comprehensively covers the market by raw materials, applications, and technology. The report provides an unbiased analysis of ongoing market trends, opportunities, high-growth areas, and market drivers, which will assist stakeholders in shaping their strategies according to the market dynamics.

United States Flour Market Highlights

| Report Name | United States Flour Market |

| Forecast Period | 2026–2032 |

| CAGR | 6.5% |

| Growing Sector | Export |

United States (US) Flour Market Synopsis

The United States (US) flour market is expected to have robust growth. The market growth is driven by rising demand for flour-based products in the domestic market and abroad. The flour is widely used in the bakery industry, pasta production, and animal feed manufacturing. Due to growing health awareness among consumers, there is a higher demand for whole wheat and gluten-free flour types. The market growth is expected to accelerate due to innovations in milling technologies and improvements in processing efficiency. The government policies encouraging agriculture and flour production growth are expected to contribute significantly to this industry growth.

Evaluation of Growth Drivers in the United States (US) Flour Market

Below are some key growth drivers and their impact on market dynamics:

| Drivers | Primary Segments Affected | Why It Matters |

| Growing Demand for Healthy Flour Alternatives | Raw Materials (Whole Wheat, Gluten-Free Flour) | There is high demand for gluten free an organic flour by the consumers. |

| Technological Advancements in Milling | Technology (Dry and Wet Technology) | Increase production efficiency, flour quality, and product diversification. |

| Flour's Versatility in Applications | Applications (Bread & Bakery, Noodles & Pasta, Animal Feed) | Makes the usage of flour high in various sectors. |

| Rising Popularity of Gluten-Free and Organic Flour | Raw Materials (Gluten-Free Flour, Organic Flour) | Addresses the growing health-conscious consumer base and special dietary needs. |

| Government Support for Agricultural Expansion | Raw Materials (Wheat, Rice, Maize) | Promotes local production and strengthens the flour supply chain. |

The United States (US) flour market is expected to grow at a CAGR of 6.5% during the forecast period of 2026-2032. The market is growing significantly due to multiple factors, including the growing demand for bakery products, mainly bread and pastries. Further, the changing consumer lifestyles and healthier food intake are driving the demand for gluten-free and organic flour. The production efficiency and quality of product are increasing due to more and more technological advancements in milling processes. Additionally, the rise of e-commerce platforms is proliferating this industry demand by providing ease of accessibility and a wide range of product offerings. The growing export of flour-based products and demand for convenience foods are expected to accelerate this industry growth.

Evaluation of Restraints in the United States (US) Flour Market

Below mentioned are some major restraints and their influence on market dynamics:

| Restraints | Primary Segments Affected | What This Means |

| Price Volatility of Raw Materials | Raw Materials (Wheat, Rice, Maize) | Leads to fluctuations in the final cost of flour, affecting profitability. |

| Competition from Alternative Flours | Raw Materials (Rice Flour, Corn Flour, etc.) | Reduces the demand for traditional wheat flour due to the popularity of alternative options. |

| Regulatory Challenges | Raw Materials (Gluten-Free Flour, Organic Flour) | Imposes additional costs and compliance requirements, potentially limiting market growth. |

| Supply Chain and Distribution Issues | All Segments | The market growth gets hampered due to logistical challenges. |

| Labor Shortages | Production (Milling Process) | A shortage of skilled labor can impact production efficiency, leading to delays and increased operational costs in the milling process. |

United States (US) Flour Market Challenges

The market faces several challenges in its path of growth. Mainly including fluctuations in raw material prices, such as wheat, which can increase the production cost. The increasing popularity of various substitutes also presents significant challenges to this industry growth. In addition to this, the strict regulatory challenges in the production and labeling of organic and gluten-free flour products impose challenges for this industry growth. The increasing supply chain disruptions, mainly in the sourcing of raw materials, remain a significant challenge.

United States (US) Flour Market Trends

Some major trends contributing to the development of the United States (US) Flour Market Growth are:

- E-Commerce Flour Sales Growth: The growth of online retail platforms provides consumers with wide range product offering and convenience of purchase for wide range of products.

- Rise of Plant-Based Diets: A growing trend toward plant-based diets has significantly increased the demand for alternative flours, further driving the market for non-wheat flour products.

- Technological Innovations in Milling: The growing technological upgrades in milling processes is increasing the quality and nutritional value of flour and flour related products.

Investment Opportunities in the United States Flour Market

Here are some investment opportunities in the United States (US) Flour Industry:

- Sustainable Milling Practices: The eco-friendly milling technologies are going to be really beneficial for attracting eco-conscious consumer base.

- Flour Product Innovation: The consumers are preferring for low carbs and organic flour products due to growing health consciousness and change in lifestyles.

- E-commerce Platforms for Flour: The growth in online purchasing have accelerated this industry growth by providing with wide range product offering at an ease of click.

Top 5 Leading Players in the United States (US) Flour Market

Here are some top companies contributing to the United States (US) Flour Market Share:

1. General Mills, Inc.

| Company Name | General Mills, Inc. |

| Established Year | 1866 |

| Headquarters | Minneapolis, Minnesota |

| Official Website | Click Here |

General Mills is a major player in the US flour market, offering a wide range of products, including premium flours for both home and commercial use. Their product offerings include gluten-free, organic, and enriched flour varieties that cater to evolving consumer demands for healthier and functional products.

2. Archer Daniels Midland Company (ADM)

| Company Name | Archer Daniels Midland Company (ADM) |

| Established Year | 1902 |

| Headquarters | Chicago, Illinois |

| Official Website | Click Here |

ADM is a leading global agricultural processor and flour producer. They offer a variety of flours, including whole wheat, enriched, and gluten-free, and are known for their strong emphasis on sustainability and innovation within the milling industry.

3. Miller Milling Company LLC

| Company Name | Miller Milling Company LLC |

| Established Year | 1985 |

| Headquarters | Minneapolis, Minnesota |

| Official Website | - |

Miller Milling is one of the top flour milling companies in the United States, offering high-quality flour products for both domestic and industrial uses. The company is a major player in the bakery products segment, producing various types of flour.

4. Bunge Limited

| Company Name | Bunge Limited |

| Established Year | 1818 |

| Headquarters | St. Louis, Missouri |

| Official Website | Click Here |

Bunge is a global leader in food production, specializing in flour milling and offering a range of wheat, maize, and other grain-based products. Their focus on innovation and technology is helping them capture a larger share of the flour market.

5. King Arthur Baking Company

| Company Name | King Arthur Baking Company |

| Established Year | 1790 |

| Headquarters | Norwich, Vermont |

| Official Website | Click Here |

King Arthur is a well-known flour brand that has gained popularity for its high-quality, organic, and specialty flours. They emphasize consumer education and quality, which helps them maintain a loyal customer base in the US flour market.

Government Regulations Introduced in the United States (US) Flour Market

According to the American government data, the market is well regulated by various government regulations that support the growth of the industry. The Food Safety Modernization Act (FSMA) ensures that the manufacturing practices involve proper hygiene and safety standards. On the other hand, the U.S. Department of Agriculture (USDA) oversees the National Organic Program (NOP) and provides proper certifications and grading to the flour products to increase consumer trust. Additionally, government initiatives such as the U.S. Wheat and Barley Scab work towards improving wheat production practices and increasing the quality of raw material used in the production of flour.

Future Insights of the United States (US) Flour Market

The United States (US) flour market is expected to have steady growth. The growing health-conscious consumer base is expected to increase the demand for healthy flour alternatives such as organic and gluten-free options. The increasing pasta and bakery industries are also expected to increase the industry growth in the coming years. As well as, increasing technological advancements are increasing this industry growth by developing advancements in milling processes with the integration of artificial intelligence and automation. On top of that, growing government support for agriculture and export is expected to drive the industry growth ahead.

Market Segmentation Analysis

The report offers a comprehensive study of the subsequent market segments and their leading categories.

Wheat to Dominate the Market - By Raw Material

According to Guneet Kaur, Senior Research Analyst, 6Wresearch, wheat dominates the US flour market due to its extensive use in bakery products, pasta, and other staple foods. Its versatility and widespread cultivation make it the preferred raw material for flour production across various sectors.

Bread & Bakery Products to Dominate the Market – By Application

Bread and bakery products are leading the market. This is mainly due to the continuous demand for important bakery items such as bread, cakes, and pastries. These products are integral to daily consumption, ensuring sustained growth in flour usage for both residential and commercial sectors.

Dry Technology to Dominate the Market - By Technology

Dry technology is the fastest-growing in the market. It is preferred mainly due to its ability to produce high-quality flour with higher yields. Dry milling offers better efficiency and is commonly used for a wide range of flour products.

Key Attractiveness of the Report

- 10 Years Market Numbers.

- Historical Data Starting from 2022 to 2025.

- Base Year: 2025

- Forecast Data until 2032.

- Key Performance Indicators Impacting the Market.

- Major Upcoming Developments and Projects.

Key Highlights of the Report:

- US Flour Market Outlook

- Market Size of US Flour Market, 2025

- Forecast of US Flour Market, 2032

- Historical Data and Forecast of US Flour Revenues & Volume for the Period 2022-2032

- US Flour Market Trend Evolution

- US Flour Market Drivers and Challenges

- US Flour Price Trends

- US Flour Porter's Five Forces

- US Flour Industry Life Cycle

- Historical Data and Forecast of US Flour Market Revenues & Volume By Raw Material for the Period 2022-2032

- Historical Data and Forecast of US Flour Market Revenues & Volume By Wheat for the Period 2022-2032

- Historical Data and Forecast of US Flour Market Revenues & Volume By Rice for the Period 2022-2032

- Historical Data and Forecast of US Flour Market Revenues & Volume By Maize for the Period 2022-2032

- Historical Data and Forecast of US Flour Market Revenues & Volume By Others for the Period 2022-2032

- Historical Data and Forecast of US Flour Market Revenues & Volume By Applications for the Period 2022-2032

- Historical Data and Forecast of US Flour Market Revenues & Volume By Bread & Bakery Products for the Period 2022-2032

- Historical Data and Forecast of US Flour Market Revenues & Volume By Noodles & Pasta for the Period 2022-2032

- Historical Data and Forecast of US Flour Market Revenues & Volume By Animal Feed for the Period 2022-2032

- Historical Data and Forecast of US Flour Market Revenues & Volume By Wafers, Crackers, & Biscuits for the Period 2022-2032

- Historical Data and Forecast of US Flour Market Revenues & Volume By Non-Food Application for the Period 2022-2032

- Historical Data and Forecast of US Flour Market Revenues & Volume By Others for the Period 2022-2032

- Historical Data and Forecast of US Flour Market Revenues & Volume By Technology for the Period 2022-2032

- Historical Data and Forecast of US Flour Market Revenues & Volume By Dry Technology for the Period 2022-2032

- Historical Data and Forecast of US Flour Market Revenues & Volume By Wet Technology for the Period 2022-2032

- US Flour Import Export Trade Statistics

- Market Opportunity Assessment By Raw Material

- Market Opportunity Assessment By Applications

- Market Opportunity Assessment By Technology

- US Flour Top Companies Market Share

- US Flour Competitive Benchmarking By Technical and Operational Parameters

- US Flour Company Profiles

- US Flour Key Strategic Recommendations

Market Covered

The report subsequently covers the market by following segments and subsegments:

By Raw Material

- Wheat

- Rice

- Maize

- Others

By Applications

- Bread & Bakery Products

- Noodles & Pasta

- Animal Feed

- Wafers, Crackers, & Biscuits

- Non-Food Application

- Others

By Technology

- Dry Technology

- Wet Technology

United States (US) Flour Market (2026-2032): FAQ's

The United States (US) Flour Market is projected to grow at a CAGR of 6.5% during the forecast period.

The market follows FDA’s FSMA regulations, USDA’s Organic Program, and other food safety measures to ensure high standards in flour production.

The market opportunities include of the increasing demand for gluten-free flour and expansion of e-commerce platforms for flour sales.

The technological advancements in milling automation, cold-chain logistics, and AI-driven processes are increasing product quality and lowering wastage,

6Wresearch actively monitors the United States (US) Flour Market and publishes its comprehensive annual report, highlighting emerging trends, growth drivers, revenue analysis, and forecast outlook. Our insights help businesses to make data-backed strategic decisions with ongoing market dynamics. Our analysts track relevent industries related to the United States (US) Flour Market, allowing our clients with actionable intelligence and reliable forecasts tailored to emerging regional needs.

Yes, we provide customisation as per your requirements. To learn more, feel free to contact us on sales@6wresearch.com

| 1 Executive Summary |

| 2 Introduction |

| 2.1 Key Highlights of the Report |

| 2.2 Report Description |

| 2.3 Market Scope & Segmentation |

| 2.4 Research Methodology |

| 2.5 Assumptions |

| 3 United States (US) Flour Market Overview |

| 3.1 United States (US) Country Macro Economic Indicators |

| 3.2 United States (US) Flour Market Revenues & Volume, 2022 & 2032F |

| 3.3 United States (US) Flour Market - Industry Life Cycle |

| 3.4 United States (US) Flour Market - Porter's Five Forces |

| 3.5 United States (US) Flour Market Revenues & Volume Share, By Raw Material, 2022 & 2032F |

| 3.6 United States (US) Flour Market Revenues & Volume Share, By Applications, 2022 & 2032F |

| 3.7 United States (US) Flour Market Revenues & Volume Share, By Technology, 2022 & 2032F |

| 4 United States (US) Flour Market Dynamics |

| 4.1 Impact Analysis |

| 4.2 Market Drivers |

| 4.2.1 Increasing demand for convenience foods and baked goods |

| 4.2.2 Growing awareness about the health benefits of whole grain flour |

| 4.2.3 Rise in home baking and cooking activities during the COVID-19 pandemic |

| 4.3 Market Restraints |

| 4.3.1 Fluctuating prices of wheat and other grains |

| 4.3.2 Competition from alternative flours like almond flour and coconut flour |

| 4.3.3 Regulatory challenges related to food safety and labeling |

| 5 United States (US) Flour Market Trends |

| 6 United States (US) Flour Market, By Types |

| 6.1 United States (US) Flour Market, By Raw Material |

| 6.1.1 Overview and Analysis |

| 6.1.2 United States (US) Flour Market Revenues & Volume, By Raw Material, 2022-2032F |

| 6.1.3 United States (US) Flour Market Revenues & Volume, By Wheat, 2022-2032F |

| 6.1.4 United States (US) Flour Market Revenues & Volume, By Rice, 2022-2032F |

| 6.1.5 United States (US) Flour Market Revenues & Volume, By Maize, 2022-2032F |

| 6.1.6 United States (US) Flour Market Revenues & Volume, By Others, 2022-2032F |

| 6.2 United States (US) Flour Market, By Applications |

| 6.2.1 Overview and Analysis |

| 6.2.2 United States (US) Flour Market Revenues & Volume, By Bread & Bakery Products, 2022-2032F |

| 6.2.3 United States (US) Flour Market Revenues & Volume, By Noodles & Pasta, 2022-2032F |

| 6.2.4 United States (US) Flour Market Revenues & Volume, By Animal Feed, 2022-2032F |

| 6.2.5 United States (US) Flour Market Revenues & Volume, By Wafers, Crackers, & Biscuits, 2022-2032F |

| 6.2.6 United States (US) Flour Market Revenues & Volume, By Non-Food Application, 2022-2032F |

| 6.2.7 United States (US) Flour Market Revenues & Volume, By Others, 2022-2032F |

| 6.3 United States (US) Flour Market, By Technology |

| 6.3.1 Overview and Analysis |

| 6.3.2 United States (US) Flour Market Revenues & Volume, By Dry Technology, 2022-2032F |

| 6.3.3 United States (US) Flour Market Revenues & Volume, By Wet Technology, 2022-2032F |

| 7 United States (US) Flour Market Import-Export Trade Statistics |

| 7.1 United States (US) Flour Market Export to Major Countries |

| 7.2 United States (US) Flour Market Imports from Major Countries |

| 8 United States (US) Flour Market Key Performance Indicators |

| 8.1 Average selling price of flour products |

| 8.2 Consumer sentiment towards whole grain flour |

| 8.3 Number of new product launches in the flour market |

| 8.4 Adoption rate of gluten-free flour options |

| 8.5 Investment in research and development for innovative flour products |

| 9 United States (US) Flour Market - Opportunity Assessment |

| 9.1 United States (US) Flour Market Opportunity Assessment, By Raw Material, 2022 & 2032F |

| 9.2 United States (US) Flour Market Opportunity Assessment, By Applications, 2022 & 2032F |

| 9.3 United States (US) Flour Market Opportunity Assessment, By Technology, 2022 & 2032F |

| 10 United States (US) Flour Market - Competitive Landscape |

| 10.1 United States (US) Flour Market Revenue Share, By Companies, 2025 |

| 10.2 United States (US) Flour Market Competitive Benchmarking, By Operating and Technical Parameters |

| 11 Company Profiles |

| 12 Recommendations |

| 13 Disclaimer |

Global Go To Market Strategy - 2030

Export potential enables firms to identify high-growth global markets with greater confidence by combining advanced trade intelligence with a structured quantitative methodology. The framework analyzes emerging demand trends and country-level import patterns while integrating macroeconomic and trade datasets such as GDP and population forecasts, bilateral import–export flows, tariff structures, elasticity differentials between developed and developing economies, geographic distance, and import demand projections. Using weighted trade values from 2020–2024 as the base period to project country-to-country export potential for 2030, these inputs are operationalized through calculated drivers such as gravity model parameters, tariff impact factors, and projected GDP per-capita growth. Through an analysis of hidden potentials, demand hotspots, and market conditions that are most favorable to success, this method enables firms to focus on target countries, maximize returns, and global expansion with data, backed by accuracy.

By factoring in the projected importer demand gap that is currently unmet and could be potential opportunity, it identifies the potential for the Exporter (Country) among 190 countries, against the general trade analysis, which identifies the biggest importer or exporter.

To discover high-growth global markets and optimize your business strategy:

Click Here

Pricing

- Single User License$ 1,995

- Department License$ 2,400

- Site License$ 3,120

- Global License$ 3,795

Leadership Perspectives from Industry Events

Search

Thought Leadership and Analyst Meet

Our Clients

6WResearch In News

- India Air Conditioner Market Set for Strong Rebound in 2026 After Weather-Led Correction and GST-Driven Recovery: 6Wresearch

- ADAS in India: How Automatic Emergency Braking, Blind Spot Detection & Driver Monitoring are Transforming Road Safety

- Doha a strategic location for EV manufacturing hub: IPA Qatar

- Demand for luxury TVs surging in the GCC, says Samsung

- Empowering Growth: The Thriving Journey of Bangladesh’s Cable Industry

- Demand for luxury TVs surging in the GCC, says Samsung

Latest Reports

- Nicaragua RPG Gaming Market (2026-2032)

- New Zealand RPG Gaming Market (2026-2032)

- Netherlands RPG Gaming Market (2026-2032)

- Nauru RPG Gaming Market (2026-2032)

- Namibia RPG Gaming Market (2026-2032)

- Mozambique RPG Gaming Market (2026-2032)

- Montenegro RPG Gaming Market (2026-2032)

- Mongolia RPG Gaming Market (2026-2032)

- Monaco RPG Gaming Market (2026-2032)

- Micronesia RPG Gaming Market (2026-2032)

Industry Events and Analyst Meet

EV India Expo 2026

HIMTEX 2026

India Refining Summit 2026

India EV Show 2026

EV tech India Expo 2026

Whitepaper

- Middle East & Africa Commercial Security Market Click here to view more.

- Middle East & Africa Fire Safety Systems & Equipment Market Click here to view more.

- GCC Drone Market Click here to view more.

- Middle East Lighting Fixture Market Click here to view more.

- GCC Physical & Perimeter Security Market Click here to view more.