US Mercury Market (2025-2031) | Outlook, Share, Forecast, Analysis, Growth, Trends, Value, Size, Revenue, Companies, Industry

Market Forecast By Application (Chemical manufacturing, Artisanal gold mining, Batteries, Dentistry, Measurement And Control Devices, Electrical and lighting, Others) And Competitive Landscape

| Product Code: ETC194233 | Publication Date: May 2022 | Updated Date: Nov 2025 | Product Type: Market Research Report | |

| Publisher: 6Wresearch | Author: Ravi Bhandari | No. of Pages: 60 | No. of Figures: 40 | No. of Tables: 7 |

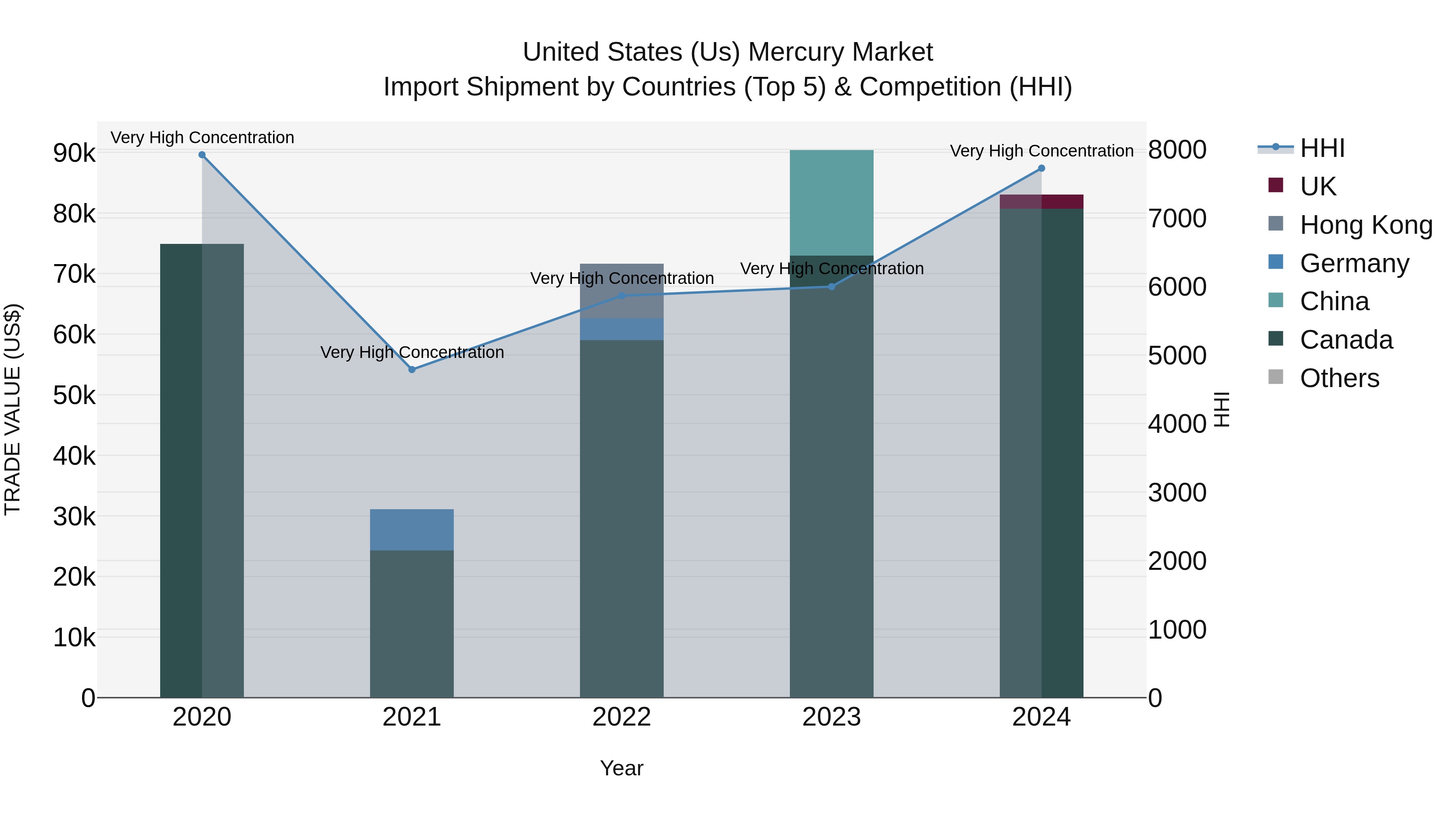

United States (US) Mercury Market Top 5 Importing Countries and Market Competition (HHI) Analysis

In 2024, the United States continued to see significant imports of mercury, with top exporters including Canada, UK, China, Germany, and Hong Kong. Despite a slight decrease in growth rate from 2023 to 2024, the compound annual growth rate (CAGR) over the four-year period remained positive at 2.62%. The high Herfindahl-Hirschman Index (HHI) indicates a concentrated market for mercury imports in the USA. This data suggests that the US market for mercury imports is stable and reliant on key trading partners for the foreseeable future.

US Mercury Market Highlights

| Report Name | US Mercury Market |

| Forecast period | 2025-2031 |

| CAGR | 1.2% |

| Growing Sector | Chemical |

Topics Covered in the US Mercury Market Report

The US Mercury market report thoroughly covers the market by application and competitive Landscape. The report provides an unbiased and detailed analysis of the on-going market trends, opportunities/high growth areas, and market drivers which would help the stakeholders to devise and align their market strategies according to the current and future market dynamics.

US Mercury Market Synopsis

The US Mercury Market has seen significant fluctuations over the past decades, influenced by both domestic legislation and international agreements. Strict environmental regulations and the Minamata Convention on Mercury, aimed at protecting human health and the environment from anthropogenic emissions and releases of mercury and mercury compounds, have contributed to a decline in demand for mercury in traditional sectors. However, niche applications in the fields of healthcare, dental amalgams, and certain industrial processes continue to sustain a limited market for mercury, albeit under stringent regulatory frameworks to mitigate environmental impact. Additionally, recent trends in the United States Mercury Market highlight a shift towards sustainable and mercury-free alternatives across various industries. This transition is driven by increased environmental awareness among consumers and businesses, as well as advancements in technology that offer viable substitutes for mercury in products and processes. Notably, the renewable energy sector has emerged as a significant player, with solar panels and wind turbines requiring no mercury for their operation, in contrast to traditional energy sources. Additionally, the medical field is witnessing a gradual phase-out of mercury-containing devices, replaced by digital instruments that ensure accuracy without environmental hazards. These trends reflect a broader movement towards reducing mercury usage, aligning with global efforts to minimize its environmental footprint.

According to 6Wresearch, United States Mercury market size is projected to grow at a CAGR of 1.2% during 2025-2031. The growth drivers of the mercury-free movement are multifaceted, encompassing regulatory pressures, technological advancements, and changing consumer preferences. Regulatory bodies worldwide have tightened legislation on mercury emissions and use, compelling industries to transition towards safer alternatives. Technological innovation plays a crucial role, as it provides economically viable and efficient substitutes for mercury in industrial applications, healthcare, and energy production. Consumer awareness and demand for environmentally friendly products further accelerate the shift towards mercury-free alternatives, pushing companies to adapt their practices and product lines to meet market expectations and regulatory requirements. These factors collectively propel the global effort towards sustainability and environmental preservation, marking a significant shift in production processes and consumer behavior towards reducing dependency on mercury.

Government Initiatives Introduced in the United States Mercury Market

Government Initiatives have played a crucial role in accelerating the transition towards mercury-free solutions across industries and sectors. Numerous countries have ratified international agreements, such as the Minamata Convention on Mercury, committing to substantial reductions in mercury use and emissions. These legislative actions are supplemented by funding for research into alternative materials and technologies, public awareness campaigns emphasizing the health and environmental risks of mercury, and incentives for businesses adopting mercury-free practices. Consistently, these plans have improved the United States Mercury Market Share. Further, through these comprehensive strategies, governments worldwide are not only ensuring compliance with global environmental standards but also fostering innovation and sustainable growth in the process.

Key Players in the United States Mercury Market

Leading the charge in the transition to mercury-free alternatives are key companies across various sectors. General Electric (GE) and Philips, for instance, have made significant strides in developing and marketing mercury-free lighting solutions. In the healthcare sector, companies like Thermo Fisher Scientific are pioneering mercury-free medical devices and instruments, aligning with global health and safety standards. The electronics industry, too, has seen giants such as Samsung and Apple move towards utilizing mercury-free materials in their products, showcasing their commitment to environmental sustainability. Further, the businesses’ clutch immense United States Mercury Market Revenues. Further, these companies not only exemplify the successful integration of eco-friendly practices into business models but also play a vital role in driving industry-wide shifts towards safer, mercury-free technologies.

Future Insights of the United States Mercury Market

The trajectory towards a mercury-free future is marked by both promise and challenges. As industries continue to innovate and adopt greener alternatives, the demand for mercury-free products is expected to rise, further driving research and development in this space. However, transitioning to mercury-free technologies requires overcoming significant obstacles, including high initial costs and the need for widespread education on mercury's hazards. Future efforts will likely focus on developing more cost-effective and efficient alternatives, alongside stronger regulatory frameworks to ensure comprehensive adoption. Additionally, international collaboration will be crucial in supporting countries with less resources to make this transition. The evolution towards a mercury-free global economy not only signifies a shift in how businesses operate but also reflects a growing societal commitment to environmental stewardship and public health.

Market Analysis by Type

According to Ravi Bhandari, Research Head, 6Wresearch, products such as medical thermometers, dental amalgams, blood pressure monitors, and various types of lighting including compact fluorescent lamps (CFLs), as well as certain types of batteries, have traditionally relied on mercury for their operation. Industries are now innovating to replace mercury in these items with safer, sustainable alternatives. For instance, digital thermometers and LED lighting are becoming more prevalent, offering mercury-free solutions that do not compromise on efficiency or functionality. These advancements highlight a broader trend towards designing products that are not only environmentally friendly but also adhere to the highest standards of public health and safety.

Market Analysis by Application

The push for mercury-free applications extends beyond medical and lighting equipment to include sectors such as the beauty industry, where mercury has been used in skin creams, and the electronics sector, where mercury-containing switches and relays are being phased out in favor of solid-state alternatives. Agricultural practices are also seeing innovation, with mercury-free solutions being developed for seed treatment and pest control, minimizing environmental contamination. Furthermore, the automotive industry is contributing to this trend by eliminating mercury in vehicles' lighting and electrical components, signaling a comprehensive shift across a wide range of applications towards safer, more sustainable technologies.

Key Attractiveness of the Report

- 10 Years Market Numbers.

- Historical Data Starting from 2021 to 2024.

- Base Year: 2024

- Forecast Data until 2031.

- Key Performance Indicators Impacting the Market.

- Major Upcoming Developments and Projects.

Key Highlights of the Report:

- United States Mercury Market Overview

- United States Mercury Market Outlook

- United States Mercury Market Forecast

- Market Size of US Mercury Market, 2024

- Forecast of US Mercury Market, 2031

- Historical Data and Forecast of US Mercury Revenues & Volume for the Period 2021 - 2031

- US Mercury Market Trend Evolution

- US Mercury Market Drivers and Challenges

- US Mercury Price Trends

- US Mercury Porter's Five Forces

- US Mercury Industry Life Cycle

- Historical Data and Forecast of US Mercury Market Revenues & Volume By Application for the Period 2021 - 2031

- Historical Data and Forecast of US Mercury Market Revenues & Volume By Chemical manufacturing for the Period 2021 - 2031

- Historical Data and Forecast of US Mercury Market Revenues & Volume By Artisanal gold mining for the Period 2021 - 2031

- Historical Data and Forecast of US Mercury Market Revenues & Volume By Batteries for the Period 2021 - 2031

- Historical Data and Forecast of US Mercury Market Revenues & Volume, By Dentistry for the Period 2021 - 2031

- Historical Data and Forecast of US Mercury Market Revenues & Volume, By Measurement and Control Devices for the Period 2021 - 2031

- Historical Data and Forecast of US Mercury Market Revenues & Volume, By Electrical and lighting for the Period 2021 - 2031

- Historical Data and Forecast of US Mercury Market Revenues & Volume, By Others for the Period 2021 - 2031

- US Mercury Import Export Trade Statistics

- Market Opportunity Assessment, By Application

- US Mercury Top Companies Market Share

- US Mercury Competitive Benchmarking, By Technical and Operational Parameters

- US Mercury Company Profiles

- US Mercury Key Strategic Recommendations

Markets Covered

The United States Mercury market report provides a detailed analysis of the following market segments:

By Application

- Chemical Manufacturing

- Artisanal Gold Mining

- Batteries

- Dentistry

- Measurement and Control Devices

- Electrical and Lighting, Others

US Mercury Market (2025-2031): FAQs

The growth drivers of the mercury-free movement are multifaceted, encompassing regulatory pressures, technological advancements, and changing consumer preferences.

Digital thermometers and LED lighting are becoming more prevalent. This category is expected to register enormous growth in future.

The batteries hold the highest market share.

General Electric (GE) and Philips are some of the prominent players in the United States Mercury market.

6Wresearch actively monitors the US Mercury Market and publishes its comprehensive annual report, highlighting emerging trends, growth drivers, revenue analysis, and forecast outlook. Our insights help businesses to make data-backed strategic decisions with ongoing market dynamics. Our analysts track relevent industries related to the US Mercury Market, allowing our clients with actionable intelligence and reliable forecasts tailored to emerging regional needs.

Yes, we provide customisation as per your requirements. To learn more, feel free to contact us on sales@6wresearch.com

| 1 Executive Summary |

| 2 Introduction |

| 2.1 Key Highlights of the Report |

| 2.2 Report Description |

| 2.3 Market Scope & Segmentation |

| 2.4 Research Methodology |

| 2.5 Assumptions |

| 3 US Mercury Market Overview |

| 3.1 US Country Macro Economic Indicators |

| 3.2 US Mercury Market Revenues & Volume, 2021 & 2031F |

| 3.3 US Mercury Market - Industry Life Cycle |

| 3.4 US Mercury Market - Porter's Five Forces |

| 3.5 US Mercury Market Revenues & Volume Share, By Application, 2021 & 2031F |

| 4 US Mercury Market Dynamics |

| 4.1 Impact Analysis |

| 4.2 Market Drivers |

| 4.2.1 Increasing demand for mercury in various industries such as healthcare, electronics, and automotive. |

| 4.2.2 Growing investments in research and development for innovative mercury-based products and technologies. |

| 4.2.3 Rising awareness and adoption of mercury-based products in renewable energy applications. |

| 4.3 Market Restraints |

| 4.3.1 Stringent regulations and bans on mercury usage in certain products and industries. |

| 4.3.2 Health and environmental concerns associated with mercury exposure. |

| 4.3.3 Volatility in mercury prices due to fluctuating supply and demand dynamics. |

| 5 US Mercury Market Trends |

| 6 US Mercury Market, By Types |

| 6.1 US Mercury Market, By Application |

| 6.1.1 Overview and Analysis |

| 6.1.2 US Mercury Market Revenues & Volume, By Application, 2021 - 2031F |

| 6.1.3 US Mercury Market Revenues & Volume, By Chemical manufacturing, 2021 - 2031F |

| 6.1.4 US Mercury Market Revenues & Volume, By Artisanal gold mining, 2021 - 2031F |

| 6.1.5 US Mercury Market Revenues & Volume, By Batteries, 2021 - 2031F |

| 6.1.6 US Mercury Market Revenues & Volume, By Dentistry, 2021 - 2031F |

| 6.1.7 US Mercury Market Revenues & Volume, By Measurement And Control Devices, 2021 - 2031F |

| 6.1.8 US Mercury Market Revenues & Volume, By Electrical and lighting, 2021 - 2031F |

| 7 US Mercury Market Import-Export Trade Statistics |

| 7.1 US Mercury Market Export to Major Countries |

| 7.2 US Mercury Market Imports from Major Countries |

| 8 US Mercury Market Key Performance Indicators |

| 8.1 Average selling price of mercury in the US market. |

| 8.2 Number of patents filed for mercury-related innovations. |

| 8.3 Percentage of mercury recycled or disposed of responsibly in the US. |

| 9 US Mercury Market - Opportunity Assessment |

| 9.1 US Mercury Market Opportunity Assessment, By Application, 2021 & 2031F |

| 10 US Mercury Market - Competitive Landscape |

| 10.1 US Mercury Market Revenue Share, By Companies, 2024 |

| 10.2 US Mercury Market Competitive Benchmarking, By Operating and Technical Parameters |

| 11 Company Profiles |

| 12 Recommendations |

| 13 Disclaimer |

Global Go To Market Strategy - 2030

Export potential enables firms to identify high-growth global markets with greater confidence by combining advanced trade intelligence with a structured quantitative methodology. The framework analyzes emerging demand trends and country-level import patterns while integrating macroeconomic and trade datasets such as GDP and population forecasts, bilateral import–export flows, tariff structures, elasticity differentials between developed and developing economies, geographic distance, and import demand projections. Using weighted trade values from 2020–2024 as the base period to project country-to-country export potential for 2030, these inputs are operationalized through calculated drivers such as gravity model parameters, tariff impact factors, and projected GDP per-capita growth. Through an analysis of hidden potentials, demand hotspots, and market conditions that are most favorable to success, this method enables firms to focus on target countries, maximize returns, and global expansion with data, backed by accuracy.

By factoring in the projected importer demand gap that is currently unmet and could be potential opportunity, it identifies the potential for the Exporter (Country) among 190 countries, against the general trade analysis, which identifies the biggest importer or exporter.

To discover high-growth global markets and optimize your business strategy:

Click Here

Pricing

- Single User License$ 1,995

- Department License$ 2,400

- Site License$ 3,120

- Global License$ 3,795

Leadership Perspectives from Industry Events

Search

Thought Leadership and Analyst Meet

Our Clients

6WResearch In News

- India Air Conditioner Market Set for Strong Rebound in 2026 After Weather-Led Correction and GST-Driven Recovery: 6Wresearch

- ADAS in India: How Automatic Emergency Braking, Blind Spot Detection & Driver Monitoring are Transforming Road Safety

- Doha a strategic location for EV manufacturing hub: IPA Qatar

- Demand for luxury TVs surging in the GCC, says Samsung

- Empowering Growth: The Thriving Journey of Bangladesh’s Cable Industry

- Demand for luxury TVs surging in the GCC, says Samsung

Latest Reports

- Nicaragua RPG Gaming Market (2026-2032)

- New Zealand RPG Gaming Market (2026-2032)

- Netherlands RPG Gaming Market (2026-2032)

- Nauru RPG Gaming Market (2026-2032)

- Namibia RPG Gaming Market (2026-2032)

- Mozambique RPG Gaming Market (2026-2032)

- Montenegro RPG Gaming Market (2026-2032)

- Mongolia RPG Gaming Market (2026-2032)

- Monaco RPG Gaming Market (2026-2032)

- Micronesia RPG Gaming Market (2026-2032)

Industry Events and Analyst Meet

EV India Expo 2026

HIMTEX 2026

India Refining Summit 2026

India EV Show 2026

EV tech India Expo 2026

Whitepaper

- Middle East & Africa Commercial Security Market Click here to view more.

- Middle East & Africa Fire Safety Systems & Equipment Market Click here to view more.

- GCC Drone Market Click here to view more.

- Middle East Lighting Fixture Market Click here to view more.

- GCC Physical & Perimeter Security Market Click here to view more.