China Meat Market (2025 - 2029) | Trends, Analysis, Revenue, Value, Growth, Companies, Forecast, Share, Industry, Outlook & Size

Market Forecast By Product (Chicken, Beef, Pork, Mutton, Others), By Type (Raw, Processed), By Distribution Channel (Departmental Stores, Specialty Stores, Hypermarket/ Supermarket, Online Sales Channel, Others) And Competitive Landscape

| Product Code: ETC171340 | Publication Date: Jan 2022 | Updated Date: Sep 2025 | Product Type: Market Research Report | |

| Publisher: 6Wresearch | Author: Shubham Deep | No. of Pages: 70 | No. of Figures: 35 | No. of Tables: 5 |

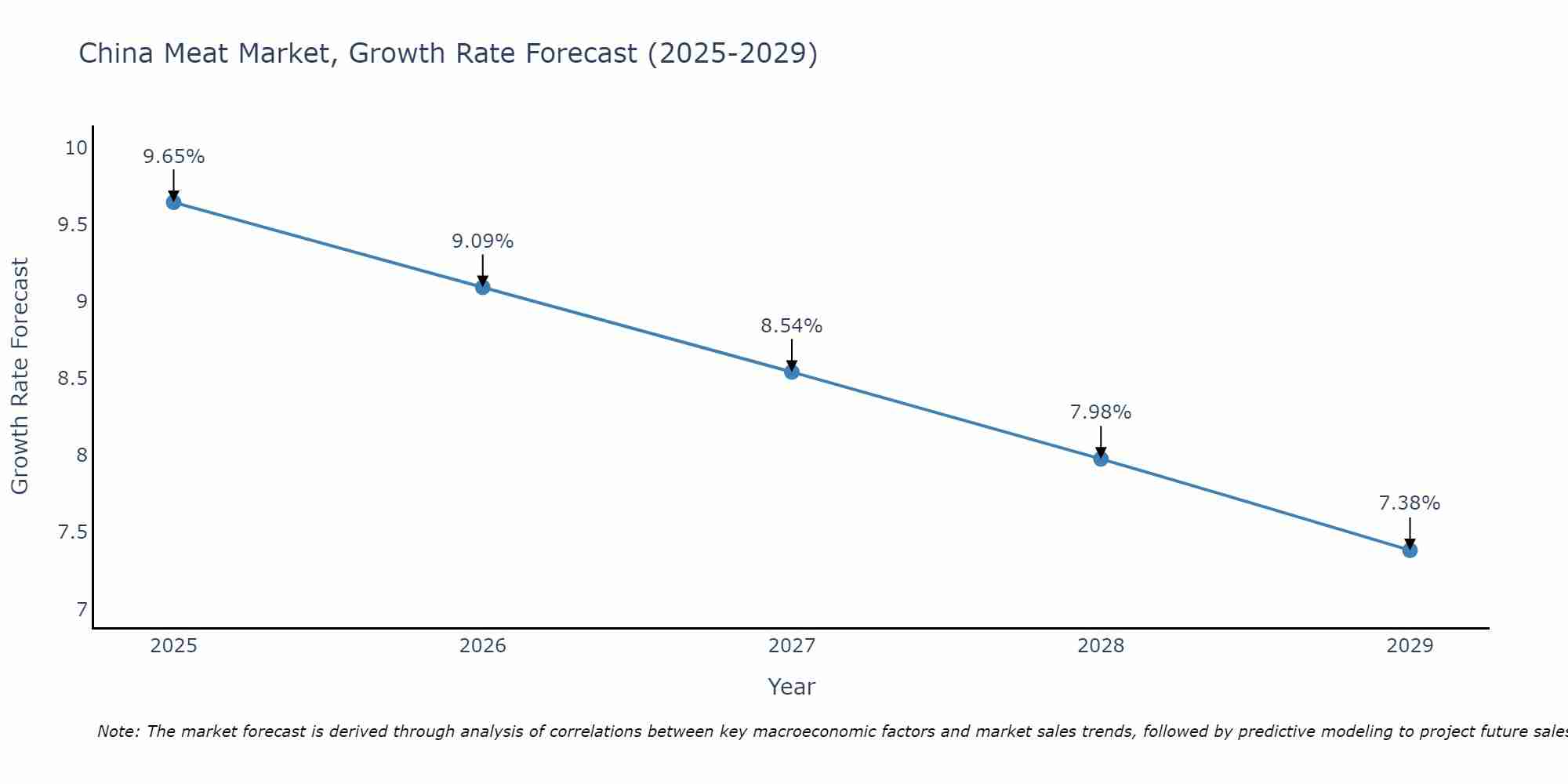

China Meat Market Size Growth Rate

The China Meat Market could see a tapering of growth rates over 2025 to 2029. Although the growth rate starts strong at 9.65% in 2025, it steadily loses momentum, ending at 7.38% by 2029.

China Meat Market Highlights

| Report Name | China Meat Market |

| Forecast Period | 2025–2029 |

| CAGR | 7.38% |

| Growing Sector | Food Processing & Animal Protein |

Topics Covered in the China Meat Market Report

The China Meat Market report thoroughly covers the market by product, type, and distribution channels. The market report provides an unbiased and detailed analysis of ongoing market trends, opportunities/high growth areas, and market drivers, which would help stakeholders to devise and align their market strategies according to the current and future market dynamics.

China Meat Market Synopsis

The China Meat Market is experiencing steady growth, supported by increasing disposable incomes, urbanization, and evolving dietary preferences. Pork remains the dominant meat, though demand for beef, poultry, and lamb is increasing due to changing consumer tastes and higher protein intake. Expanding cold-chain logistics and e-commerce platforms are improving distribution and accessibility nationwide. Furthermore, growing interest in premium, organic, and processed meat products is reshaping market dynamics. These factors collectively position China as a leading global meat consumer.

Evaluation of Growth Drivers in the China Meat Market

Below mentioned are some prominent drivers and their influence to the market dynamics:

| Driver | Primary Segments Affected | Why it matters (evidence) |

| Rising Urbanization & Lifestyle Change | Processed Meat, Supermarkets, Online Channels | Working-class urban households are turning more toward processed and convenient ready-to-eat meat products. |

| Increasing Protein Demand | Chicken, Beef, Pork | Rising health consciousness has boosted meat consumption as a primary protein source. |

| E-Commerce Expansion | Online Sales Channels, Processed Meat | Meat delivery services are accelerating with the rise of online platforms like JD Fresh and Tmall Fresh. |

| Cold Chain Infrastructure Development | Processed Meat, Specialty Stores | Rising investments in cold storage and logistics are enhancing the efficiency of meat distribution. |

| Government Food Security Initiatives | Pork, Beef, Departmental Stores | National initiatives for pork stabilization guarantee consistent availability and strengthen market stability. |

The China Meat Market size is projected to grow at the CAGR of 7.38% during the forecast period of 2025–2029. The China Meat Market is primarily driven by rising disposable incomes, urbanization, and shifting dietary habits toward higher protein consumption. While pork remains the primary choice, interest in beef, poultry, and lamb is accelerating as dietary preferences broaden. China Meat Market Growth benefits from the expansion of digital platforms such as JD Fresh and Tmall Fresh, supported by investments in cold-chain infrastructure to strengthen delivery efficiency. In addition, state-backed pork stabilization measures and the surging popularity of organic, high-quality, and ready-to-cook meat products are sustaining strong demand and ensuring steady expansion across the sector.

Evaluation of Restraints in the China Meat Market

Below mentioned are some major restraints and their influence to the market dynamics:

| Restraint | Primary Segments Affected | What this means (evidence) |

| Environmental Regulations | Beef, Pork, Processed Meat | Strict policies to control livestock emissions and pollution raise compliance costs. |

| Price Volatility | Pork & Beef | Fluctuations in feed and livestock prices affect consumer affordability. |

| Rising Vegetarian & Vegan Trends | All Meat Segments | Growing awareness of plant-based diets poses long-term risks to meat demand. |

| Health & Safety Concerns | Processed Meat, Online Sales | Food safety scandals reduce consumer trust in mass meat suppliers. |

| Import Dependency for Beef & Mutton | Beef, Mutton | Heavy reliance on imports from Australia, Brazil, and New Zealand raises vulnerability. |

China Meat Market Challenges

Despite strong demand, the China Meat Industry struggles with several constraints. Unstable pork prices create uncertainty throughout the supply chain. Dependence on beef and lamb imports leaves the market vulnerable to global trade disruptions and supply shortages. Stringent regulations on labeling, safety, and inspections drive up compliance expenses. Furthermore, underdeveloped cold-chain systems, particularly in rural areas, restrict efficient distribution. Growing consumer demand for organic, traceable, and clean-label products places further pressure on producers to invest in certification processes and transparency initiatives, adding to industry costs and operational challenges.

China Meat Market Trends

Several prominent trends reshaping the market growth include:

- Meat Product Premiumization: Increased demand for organic, hormone-free, and high-quality meat options.

- Online Meat Delivery Growth: Platforms like Hema Fresh, JD Fresh, and Dingdong are changing supply chains.

- Processed & Ready-to-Cook Products: Growing preference for sausages, frozen meat, and instant meal kits.

- Traceability Systems Adoption: Meat safety and authenticity via blockchain and QR-code traceability.

Investment Opportunities in the China Meat Industry

There are some main areas of investment opportunity in the market which includes:

- Processed Meat Growth – Create ready-to-cook and frozen product lines for urban households.

- Cold Chain Logistics – Investment in cold storage, transport, and packaging.

- Premium Organic Meat Brands – Introducing hormone and antibiotic-free meat for health-conscious consumers.

- Cross-Border Import Partnerships – Source beef and mutton from a stable and reliable supply.

Top 5 Leading Players in the China Meat Market

Some leading players dominating the market include:

1. WH Group Limited (Shuanghui Development)

| Company Name | WH Group Limited (Shuanghui Development) |

| Establishment Year | 1958 |

| Headquarter | Luohe, Henan, China |

| Official Website | Click here |

The largest meat processing company in China, known for pork products, processed meat, and cold-chain logistics.

2. Yurun Group Limited

| Company Name | Yurun Group Limited |

| Establishment Year | 1993 |

| Headquarter | Nanjing, Jiangsu, China |

| Official Website | Click here |

A leading meat supplier offering chilled, frozen, and processed meat products with a strong domestic distribution network.

3. Delisi Food Co., Ltd.

| Company Name | Delisi Food Co., Ltd. |

| Establishment Year | 1989 |

| Headquarter | Shandong, China |

| Official Website | Click here |

Focuses on pork and processed meat, with significant exports and partnerships in Asia.

4. Chongqing Yurun Food Co., Ltd.

| Company Name | Chongqing Yurun Food Co., Ltd. |

| Establishment Year | 1998 |

| Headquarter | Chongqing, China |

| Official Website | Click here |

A major supplier of pork and processed meat, focusing on regional demand in western China.

5. Tyson Foods China (Subsidiary of Tyson Foods Inc.)

| Company Name | Tyson Foods China (Subsidiary of Tyson Foods Inc.) |

| Establishment Year | 2001 (China operations) |

| Headquarter | Shanghai, China |

| Official Website | - |

Provides chicken and processed meat products with strong integration into China’s retail and e-commerce platforms.

Government Regulations Introduced in the China Meat Market

According to Chinese Government data, The Chinese government has launched initiatives to modernize and stabilize its meat industry. The Pork Reserve System helps maintain supply balance by storing pork during shortages. The 14th Five-Year Agricultural Plan focuses on better livestock farming practices and stricter food safety standards. Subsidies have been provided to strengthen cold-chain logistics, ensuring efficient meat distribution. Subsequently, China is growing international partnerships, particularly with Brazil and Australia, to secure consistent supplies of beef and mutton, enhancing long-term food security.

Future Insights of the China Meat Market

The China Meat Market Share is estimated to increase significantly in the coming years. Increasing disposable incomes, the expansion of online channels, and a preference for processed and premium meat products will drive growth. The industry will also see an increase in demand for traceability solutions and eco-friendly farming practices to meet environmental and safety regulations. Growing cold-chain logistics investments will further enhance distribution efficiency and product quality. Furthermore, international trade partnerships will help secure stable supplies of beef and lamb.

Market Segmentation Analysis

The report offers a comprehensive study of the subsequent market segments and their leading categories.

Pork to Dominate the Market -By Product

According to Ritika Kalra, Senior Research Analyst at 6Wresearch, The Pork segment holds the largest market share, as pork remains the staple meat in Chinese cuisine. It is consumed across all demographics, supported by government programs to ensure pork supply stability.

Processed Meat to Dominate the Market -By Type

The Processed Meat segment dominates due to rising demand for sausages, bacon, frozen meats, and convenience-based food products. Busy lifestyles and urbanization have accelerated the preference for ready-to-cook options.

Online Sales Channels to Dominate the Market -By Distribution Channel

The Online Sales Channel segment leads the market, supported by the growth of digital grocery platforms such as Hema Fresh, JD Fresh, and Dingdong. Discounts, home delivery, and product traceability features make online the preferred channel for younger consumers.

Key Attractiveness of the Report

- 10 Years of Market Numbers.

- Historical Data Starting from 2021 to 2024.

- Base Year: 2024.

- Forecast Data until 2029.

- Key Performance Indicators Impacting the Market.

- Major Upcoming Developments and Projects.

Key Highlights of the Report:

- China Meat Market Outlook

- Market Size of China Meat Market, 2024

- Forecast of China Meat Market, 2029

- Historical Data and Forecast of China Meat Revenues & Volume for the Period 2019 - 2029

- China Meat Market Trend Evolution

- China Meat Market Drivers and Challenges

- China Meat Price Trends

- China Meat Porter's Five Forces

- China Meat Industry Life Cycle

- Historical Data and Forecast of China Meat Market Revenues & Volume By Product for the Period 2019 - 2029

- Historical Data and Forecast of China Meat Market Revenues & Volume By Chicken for the Period 2019 - 2029

- Historical Data and Forecast of China Meat Market Revenues & Volume By Beef for the Period 2019 - 2029

- Historical Data and Forecast of China Meat Market Revenues & Volume By Pork for the Period 2019 - 2029

- Historical Data and Forecast of China Meat Market Revenues & Volume By Mutton for the Period 2019 - 2029

- Historical Data and Forecast of China Meat Market Revenues & Volume By Others for the Period 2019 - 2029

- Historical Data and Forecast of China Meat Market Revenues & Volume By Type for the Period 2019 - 2029

- Historical Data and Forecast of China Meat Market Revenues & Volume By Raw for the Period 2019 - 2029

- Historical Data and Forecast of China Meat Market Revenues & Volume By Processed for the Period 2019 - 2029

- Historical Data and Forecast of China Meat Market Revenues & Volume By Distribution Channel for the Period 2019 - 2029

- Historical Data and Forecast of China Meat Market Revenues & Volume By Departmental Stores for the Period 2019 - 2029

- Historical Data and Forecast of China Meat Market Revenues & Volume By Specialty Stores for the Period 2019 - 2029

- Historical Data and Forecast of China Meat Market Revenues & Volume By Hypermarket/ Supermarket for the Period 2019 - 2029

- Historical Data and Forecast of China Meat Market Revenues & Volume By Online Sales Channel for the Period 2019 - 2029

- Historical Data and Forecast of China Meat Market Revenues & Volume By Others for the Period 2019 - 2029

- China Meat Import Export Trade Statistics

- Market Opportunity Assessment By Product

- Market Opportunity Assessment By Type

- Market Opportunity Assessment By Distribution Channel

- China Meat Top Companies Market Share

- China Meat Competitive Benchmarking By Technical and Operational Parameters

- China Meat Company Profiles

- China Meat Key Strategic Recommendations

Market Covered

The report offers a comprehensive study of the subsequent market segments:

By Product

- Chicken

- Beef

- Pork

- Mutton

- Others

By Type

- Raw

- Processed

By Distribution Channel

- Departmental Stores

- Specialty Stores

- Hypermarket/Supermarket

- Online Sales Channel

- Others

China Meat Market (2025 - 2029): FAQs

The China Meat Market is projected to grow at a CAGR of approximately 7.38% during the forecast period.

Rising demand for premium, safe, traceable, and e-commerce-driven meat products.

Growth in processed meats, cold-chain logistics, organic brands, and online delivery.

WH Group, Muyuan Foodstuff, Wens Foodstuff, Yurun Group, and Tyson China.

6Wresearch actively monitors the China Meat Market and publishes its comprehensive annual report, highlighting emerging trends, growth drivers, revenue analysis, and forecast outlook. Our insights help businesses to make data-backed strategic decisions with ongoing market dynamics. Our analysts track relevent industries related to the China Meat Market, allowing our clients with actionable intelligence and reliable forecasts tailored to emerging regional needs.

Yes, we provide customisation as per your requirements. To learn more, feel free to contact us on sales@6wresearch.com

| 1 Executive Summary |

| 2 Introduction |

| 2.1 Key Highlights of the Report |

| 2.2 Report Description |

| 2.3 Market Scope & Segmentation |

| 2.4 Research Methodology |

| 2.5 Assumptions |

| 3 China Meat Market Overview |

| 3.1 China Country Macro Economic Indicators |

| 3.2 China Meat Market Revenues & Volume, 2019 & 2029F |

| 3.3 China Meat Market - Industry Life Cycle |

| 3.4 China Meat Market - Porter's Five Forces |

| 3.5 China Meat Market Revenues & Volume Share, By Product, 2019 & 2029F |

| 3.6 China Meat Market Revenues & Volume Share, By Type, 2019 & 2029F |

| 3.7 China Meat Market Revenues & Volume Share, By Distribution Channel, 2019 & 2029F |

| 4 China Meat Market Dynamics |

| 4.1 Impact Analysis |

| 4.2 Market Drivers |

| 4.2.1 Increasing disposable income leading to higher meat consumption |

| 4.2.2 Urbanization and changing lifestyles favoring convenience of meat products |

| 4.2.3 Growing awareness of health benefits of consuming quality meat products |

| 4.3 Market Restraints |

| 4.3.1 Concerns over food safety and quality leading to lower trust in meat products |

| 4.3.2 Environmental impact and sustainability issues associated with meat production |

| 4.3.3 Competition from alternative protein sources like plant-based meat substitutes |

| 5 China Meat Market Trends |

| 6 China Meat Market, By Types |

| 6.1 China Meat Market, By Product |

| 6.1.1 Overview and Analysis |

| 6.1.2 China Meat Market Revenues & Volume, By Product, 2019 - 2029F |

| 6.1.3 China Meat Market Revenues & Volume, By Chicken, 2019 - 2029F |

| 6.1.4 China Meat Market Revenues & Volume, By Beef, 2019 - 2029F |

| 6.1.5 China Meat Market Revenues & Volume, By Pork, 2019 - 2029F |

| 6.1.6 China Meat Market Revenues & Volume, By Mutton, 2019 - 2029F |

| 6.1.7 China Meat Market Revenues & Volume, By Others, 2019 - 2029F |

| 6.2 China Meat Market, By Type |

| 6.2.1 Overview and Analysis |

| 6.2.2 China Meat Market Revenues & Volume, By Raw, 2019 - 2029F |

| 6.2.3 China Meat Market Revenues & Volume, By Processed, 2019 - 2029F |

| 6.3 China Meat Market, By Distribution Channel |

| 6.3.1 Overview and Analysis |

| 6.3.2 China Meat Market Revenues & Volume, By Departmental Stores, 2019 - 2029F |

| 6.3.3 China Meat Market Revenues & Volume, By Specialty Stores, 2019 - 2029F |

| 6.3.4 China Meat Market Revenues & Volume, By Hypermarket/ Supermarket, 2019 - 2029F |

| 6.3.5 China Meat Market Revenues & Volume, By Online Sales Channel, 2019 - 2029F |

| 6.3.6 China Meat Market Revenues & Volume, By Others, 2019 - 2029F |

| 7 China Meat Market Import-Export Trade Statistics |

| 7.1 China Meat Market Export to Major Countries |

| 7.2 China Meat Market Imports from Major Countries |

| 8 China Meat Market Key Performance Indicators |

| 8.1 Consumer demand for organic or sustainable meat products |

| 8.2 Adoption rates of new technologies in meat production and processing |

| 8.3 Trends in meat consumption preferences towards specific types of meat |

| 8.4 Regulatory changes impacting meat imports and exports |

| 8.5 Consumer sentiment towards meat industry practices and transparency |

| 9 China Meat Market - Opportunity Assessment |

| 9.1 China Meat Market Opportunity Assessment, By Product, 2019 & 2029F |

| 9.2 China Meat Market Opportunity Assessment, By Type, 2019 & 2029F |

| 9.3 China Meat Market Opportunity Assessment, By Distribution Channel, 2019 & 2029F |

| 10 China Meat Market - Competitive Landscape |

| 10.1 China Meat Market Revenue Share, By Companies, 2024 |

| 10.2 China Meat Market Competitive Benchmarking, By Operating and Technical Parameters |

| 11 Company Profiles |

| 12 Recommendations |

| 13 Disclaimer |

Export potential assessment - trade Analytics for 2030

Export potential enables firms to identify high-growth global markets with greater confidence by combining advanced trade intelligence with a structured quantitative methodology. The framework analyzes emerging demand trends and country-level import patterns while integrating macroeconomic and trade datasets such as GDP and population forecasts, bilateral import–export flows, tariff structures, elasticity differentials between developed and developing economies, geographic distance, and import demand projections. Using weighted trade values from 2020–2024 as the base period to project country-to-country export potential for 2030, these inputs are operationalized through calculated drivers such as gravity model parameters, tariff impact factors, and projected GDP per-capita growth. Through an analysis of hidden potentials, demand hotspots, and market conditions that are most favorable to success, this method enables firms to focus on target countries, maximize returns, and global expansion with data, backed by accuracy.

By factoring in the projected importer demand gap that is currently unmet and could be potential opportunity, it identifies the potential for the Exporter (Country) among 190 countries, against the general trade analysis, which identifies the biggest importer or exporter.

To discover high-growth global markets and optimize your business strategy:

Click Here

Pricing

- Single User License$ 1,995

- Department License$ 2,400

- Site License$ 3,120

- Global License$ 3,795

Search

Thought Leadership and Analyst Meet

Our Clients

Latest Reports

- United Kingdom (UK) Long-term Care Insurance Market (2026-2032) | Growth, Share, Consumer Insights, Drivers, Opportunities, Competition, Pricing Analysis, Segments, Restraints, Companies, Competitive, Value, Outlook, Size, Demand, Analysis, Challenges, Strategic Insights, Investment Trends, Revenue, Trends, Supply, Forecast

- United Kingdom (UK) Long Term Care Market (2026-2032) | Companies, Outlook, Analysis, Trends, Value, Revenue, Segmentation, Share, Forecast, Competitive Landscape, Growth, Size & Forecast

- Iraq Insulation and Waterproofing Market (2026-2032) | Outlook, Drivers, Growth, Size, Share, Industry, Revenue, Trends, Demand, Competitive, Strategic Insights, Opportunities, Segments, Companies, Challenges, Strategy, Consumer Insights, Analysis, Investment Trends, Value, Segmentation, Forecast, Restraints

- India Switchgear Market Outlook (2026-2032) | Size, Share, Trends, Growth, Revenue, Forecast, Analysis, Value, Outlook

- Pakistan Contraceptive Implants Market (2025-2031) | Demand, Growth, Size, Share, Industry, Pricing Analysis, Competitive, Strategic Insights, Strategy, Consumer Insights, Analysis, Investment Trends, Opportunities, Revenue, Segments, Value, Segmentation, Supply, Forecast, Restraints, Outlook, Competition, Drivers, Trends, Companies, Challenges

- Sri Lanka Packaging Market (2026-2032) | Outlook, Competition, Drivers, Trends, Demand, Pricing Analysis, Competitive, Strategic Insights, Companies, Challenges, Strategy, Consumer Insights, Analysis, Investment Trends, Opportunities, Growth, Size, Share, Industry, Revenue, Segments, Value, Segmentation, Supply, Forecast, Restraints

- India Kids Watches Market (2026-2032) | Strategy, Consumer Insights, Analysis, Investment Trends, Opportunities, Growth, Size, Share, Industry, Revenue, Segments, Value, Segmentation, Supply, Forecast, Restraints, Outlook, Competition, Drivers, Trends, Demand, Pricing Analysis, Competitive, Strategic Insights, Companies, Challenges

- Saudi Arabia Core Assurance Service Market (2025-2031) | Strategy, Consumer Insights, Analysis, Investment Trends, Opportunities, Growth, Size, Share, Industry, Revenue, Segments, Value, Segmentation, Supply, Forecast, Restraints, Outlook, Competition, Drivers, Trends, Demand, Pricing Analysis, Competitive, Strategic Insights, Companies, Challenges

- Romania Uninterruptible Power Supply (UPS) Market (2026-2032) | Industry, Analysis, Revenue, Size, Forecast, Outlook, Value, Trends, Share, Growth & Companies

- Saudi Arabia Car Window Tinting Film, Paint Protection Film (PPF), and Ceramic Coating Market (2025-2031) | Strategy, Consumer Insights, Analysis, Investment Trends, Opportunities, Growth, Size, Share, Industry, Revenue, Segments, Value, Segmentation, Supply, Forecast, Restraints, Outlook, Competition, Drivers, Trends, Demand, Pricing Analysis, Competitive, Strategic Insights, Companies, Challenges

Industry Events and Analyst Meet

India EV Show 2026

EV tech India Expo 2026

Auto Tech Asia 2026

Battery Tech India 2026

Smart Production Solutions Guangzhou 2026

Whitepaper

- Middle East & Africa Commercial Security Market Click here to view more.

- Middle East & Africa Fire Safety Systems & Equipment Market Click here to view more.

- GCC Drone Market Click here to view more.

- Middle East Lighting Fixture Market Click here to view more.

- GCC Physical & Perimeter Security Market Click here to view more.

6WResearch In News

- Doha a strategic location for EV manufacturing hub: IPA Qatar

- Demand for luxury TVs surging in the GCC, says Samsung

- Empowering Growth: The Thriving Journey of Bangladesh’s Cable Industry

- Demand for luxury TVs surging in the GCC, says Samsung

- Video call with a traditional healer? Once unthinkable, it’s now common in South Africa

- Intelligent Buildings To Smooth GCC’s Path To Net Zero